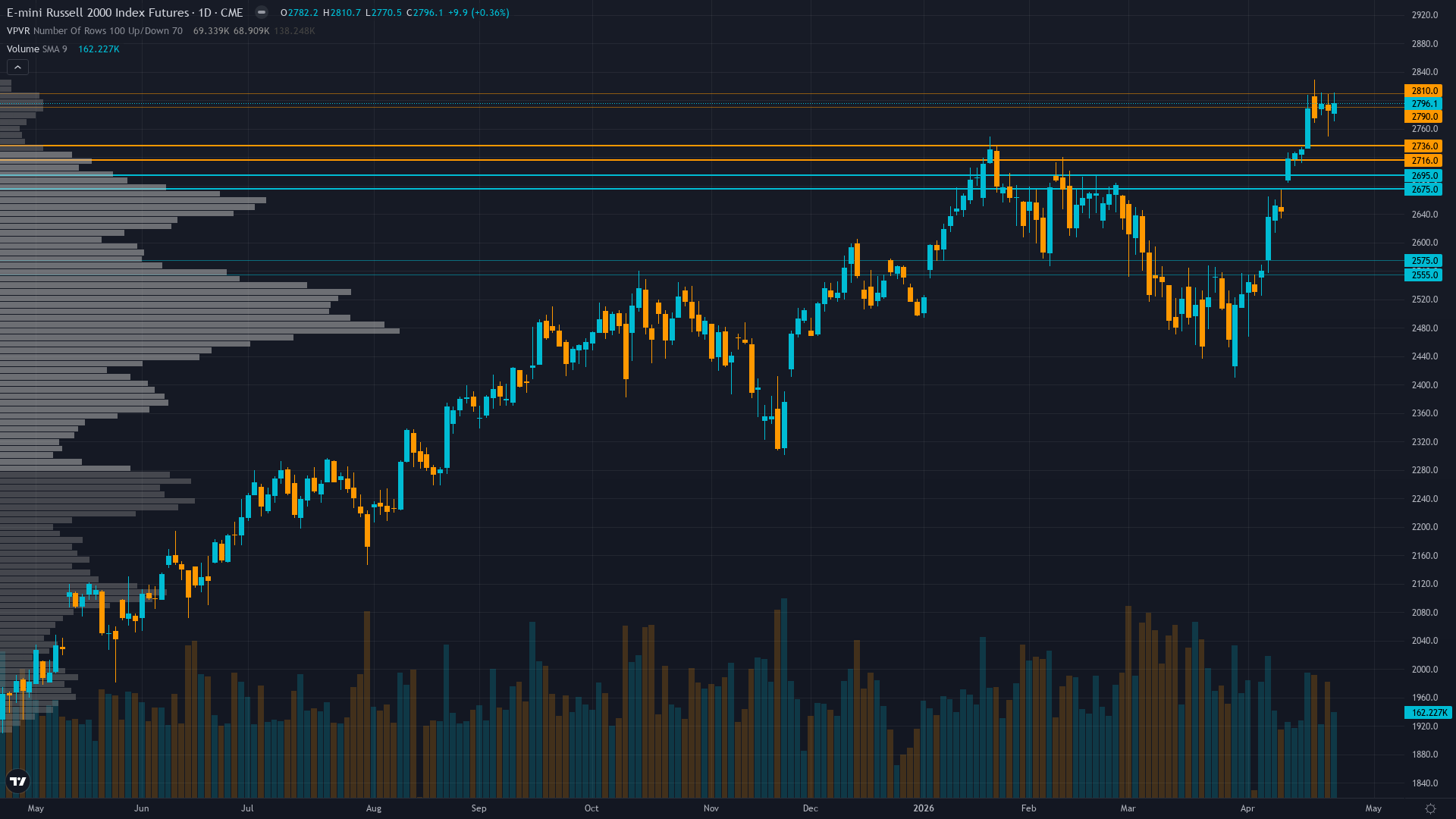

Russell 2000 Forecast This Week — Outlook, Drivers & Key Levels

This week's Russell 2000 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

This week's Russell 2000 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

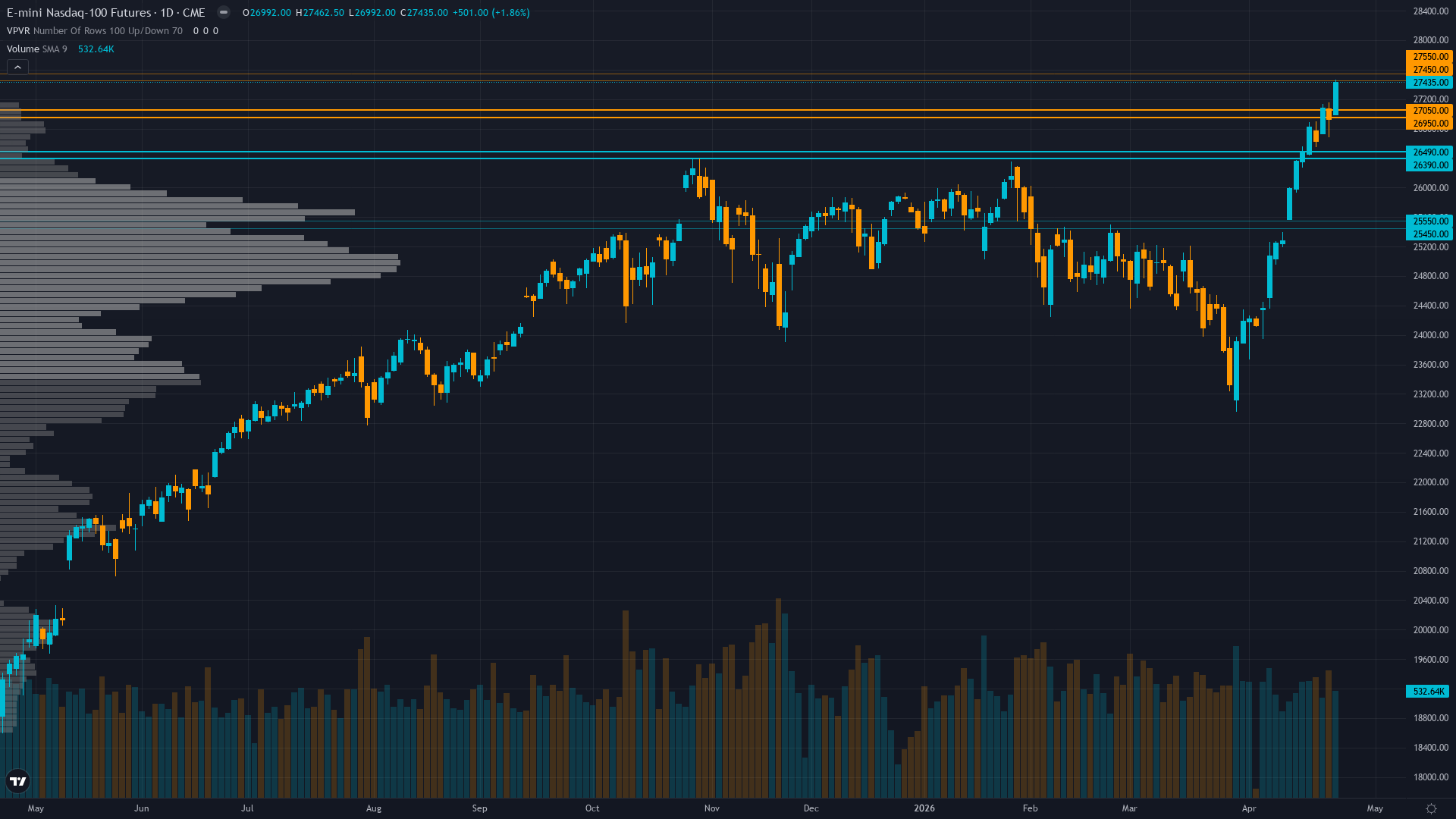

Nasdaq 100 institutional positioning: COT data, sentiment analysis and smart money flow assessment.

Nasdaq 100 key levels breakdown: support zones, resistance zones, confluence and price structure.

S&P 500 institutional positioning: COT data, sentiment analysis and smart money flow assessment.

This week's S&P 500 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Russell 2000 key levels breakdown: support zones, resistance zones, confluence and price structure.

Russell 2000 institutional positioning: COT data, sentiment analysis and smart money flow assessment.

S&P 500 key levels breakdown: support zones, resistance zones, confluence and price structure.

This week's Nasdaq 100 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Core

Constructively bullish on Q1 earnings validation and VIX normalization driving continued upside with all-time high breakout confirmed, though acknowledging deeply overbought technicals and complacent sentiment create near-term consolidation risk

Core

Cautiously bullish on Q1 earnings season strength and FOMC event uncertainty but aware 7,200 resistance remains formidable barrier with equity put/call 0.51 complacency creating asymmetric downside risk

Extended

Small-caps celebrating new all-time highs with 'Great Rotation' narrative gaining mainstream traction, Q1 earnings season providing validation catalyst, bullish positioning dominant