Extended

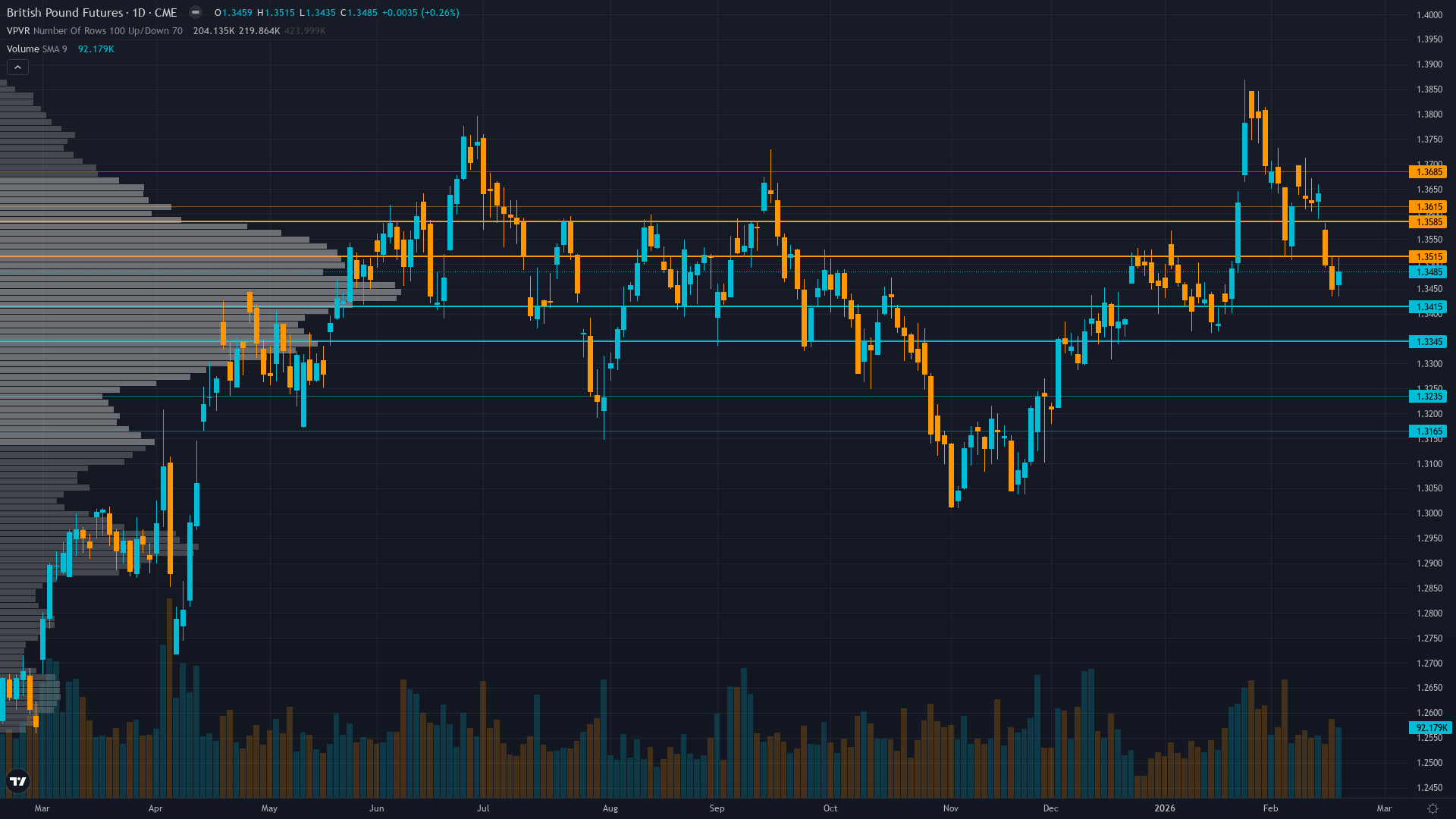

GBP/USD (6B) — consolidating in normal regime

Neutral to mildly bearish consolidation expected with defensive positioning ahead of March 19 BoE meeting as declining UK inflation to 3.0% supports easing expectations

Extended

Neutral to mildly bearish consolidation expected with defensive positioning ahead of March 19 BoE meeting as declining UK inflation to 3.0% supports easing expectations

Full Desk

Constructive consolidation within structural bull market as extraordinary 2025 gains digest against 2026 balanced forecast, with February seasonal support providing near-term floor before next directional move

Full Desk

Shifting from aggressive bullish expecting continued RBA tightening toward cautious constructive recognizing inflation-driven hawkish floor creates support but acknowledging 12% rally extension and approaching major resistance requires consolidation

Full Desk

Cautiously constructive on February short-covering rally from extreme October oversold levels with Arctic blast providing first genuine supply catalyst yet skeptical about sustainability given structural oversupply fundamentals

Full Desk

Cautiously bullish on Trump-Xi breakthrough potential 20 MMT upgrade but concerned about pricing execution risk and whether deal represents consideration versus confirmed commitment requiring follow-through validation

Full Desk

Treasury bonds experiencing technical relief rally after December panic exhaustion but fundamentals remain challenged with Fed terminal rate near 3% and sticky inflation limiting sustained duration rally potential

Most analysts targeting $75-85 consolidation near-term with longer-term forecasts extending to $90-150 by mid-2026 if supply deficit and China restrictions persist though CME intervention creates uncertainty and regulatory overhang capping near-term upside

Core

Defensive and fearful near-term given violent AI spending concerns selloff but acknowledging oversold technicals and upcoming March seasonal strength could provide recovery catalyst

Core

Cautiously neutral awaiting February catalysts with DeepSeek disruption concerns tempering seasonal optimism amid Fed hawkish December shock and elevated valuations

Core

Cautiously bearish expecting structural oversupply and weak Chinese demand to push prices toward $55-58 range over 2026 despite OPEC+ Q1 production freeze providing temporary support

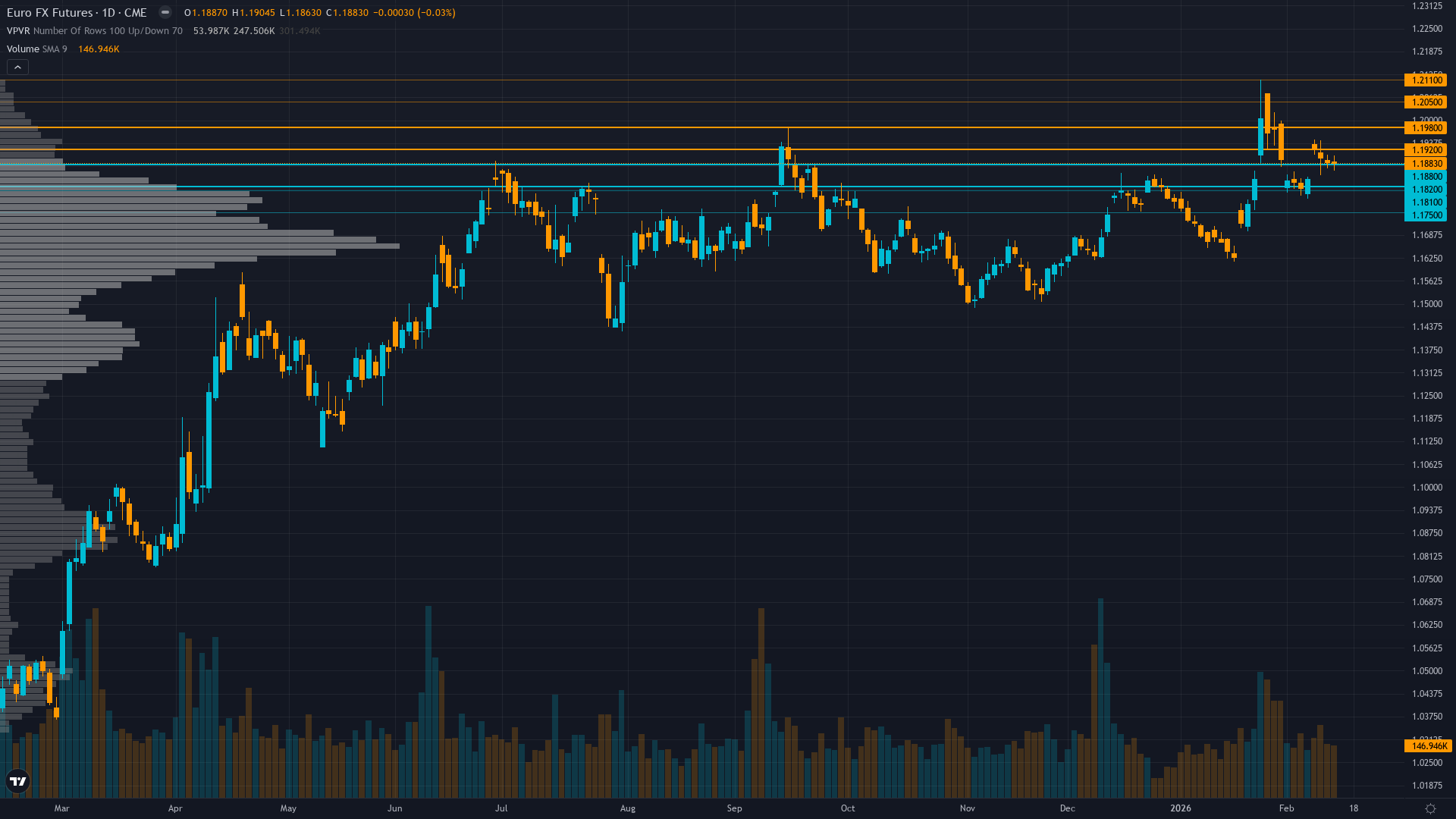

Core

EUR range-bound near 1.19 as both Fed and ECB signal patience with modest consensus targets of 1.18-1.22 through Q2 2026 awaiting fresh catalysts from March dual central bank meetings

Core

Bullish medium-term with structural central bank support intact and Fed maintaining accommodative bias creating constructive backdrop for continuation toward $5200-5600 despite January profit-taking consolidation