Mon-T Weekly Review — w/e 29 May 2026

Crude oil finally breaks the bears' drought, wheat breaks the bulls' hearts, and the Nasdaq quietly sets another record nobody asked about.

Two stories define this week, and they could not be more different. In one corner, crude oil crashed 8.85% as the US-Iran ceasefire extended by 60 days with unrestricted Strait of Hormuz shipping reportedly on the table. WTI fell below $88 per barrel, its lowest since before the war fundamentally repriced energy markets in late February. The desk called BEARISH at minimum conviction and collected the single best individual market result since the 14.78% CL call back on April 17. In the other corner, wheat was called BULLISH at 7/10, the desk's joint-highest conviction of the week, and promptly dropped 5.68% as the worst US production shortfall since 1972 apparently failed to impress a market more interested in seasonal harvest pressure than drought drama.

Five of seven directional calls landed on the right side, a 71.4% hit rate that sustains the desk's recent run of respectability. The Nasdaq surged 2.85% to fresh all-time highs above 30,400, the S&P added 1.43%, copper gained 1.16%, and silver edged lower as called. Eight markets received the NO CALL treatment, and among those, gold dropped another 3.25% while platinum fell 2.39%, both misses that the desk will feel in its bones even if the procedure was followed to the letter.

The broader picture is one of cautious competence. The desk is picking its spots, committing where conviction is genuine, and sitting out the rest. Whether that discipline is a feature or a bug depends on how you feel about watching gold drop three percent while your prediction desk shrugs its shoulders and says 'not our problem this week.'

|

15

Markets

|

7

Directional

|

5

Correct

|

71.4%

Accuracy

|

8

No Calls

|

Seven directional calls this week, with five landing on the right side. The other eight markets got the NO CALL treatment. A 71.4% directional accuracy rate continues the improved trajectory since the 12.5% catastrophe of late April, and the average confidence of 6 across the directional calls reflects measured conviction rather than desperate swinging.

The confidence calibration was inverted in the worst possible way. The two highest-conviction calls at 7/10, NQ BULLISH and ZW BULLISH, produced a split result: Nasdaq delivered a clean 2.85% win while wheat collapsed 5.68% in the wrong direction. The two lowest-conviction calls at 5/10, CL BEARISH and ZB BEARISH, also split: crude oil delivered the week's headline 8.85% win while bonds rallied 1.44% against the call. When your highest-conviction hit and your lowest-conviction hit both deliver while the misses are scattered across both confidence tiers, the system is telling you it can identify direction but not yet calibrate its own certainty about that direction.

|

53/96

Correct / Total

|

55.2%

Accuracy

|

96 / 99

Directional / No Call

|

The rolling twelve-week figure sits at 55.2% across 96 directional calls, with 99 no-call abstentions. That engagement split tells you the desk is calling direction on fewer than half of all market-weeks, a rate that reflects the wartime caution that has defined 2026. This week's 71.4% helps modestly, but the mid-April catastrophes and May 15 CPI-driven miss cluster continue to weigh on the trailing number. The desk needs several more weeks above 65% to crack through the 57-58% ceiling that has been its permanent residence since the Iran conflict began.

|

Bias Called

BEARISH

|

Confidence

6/10

|

Result

CORRECT

|

Grade

C+

|

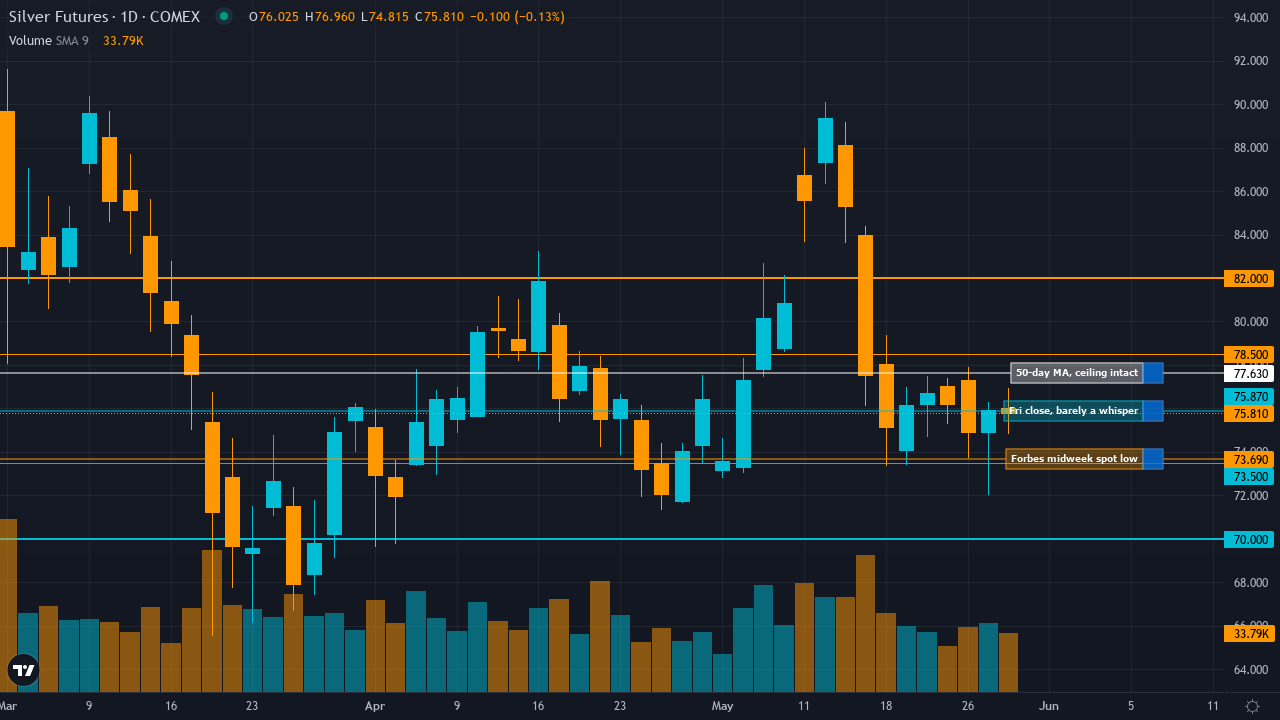

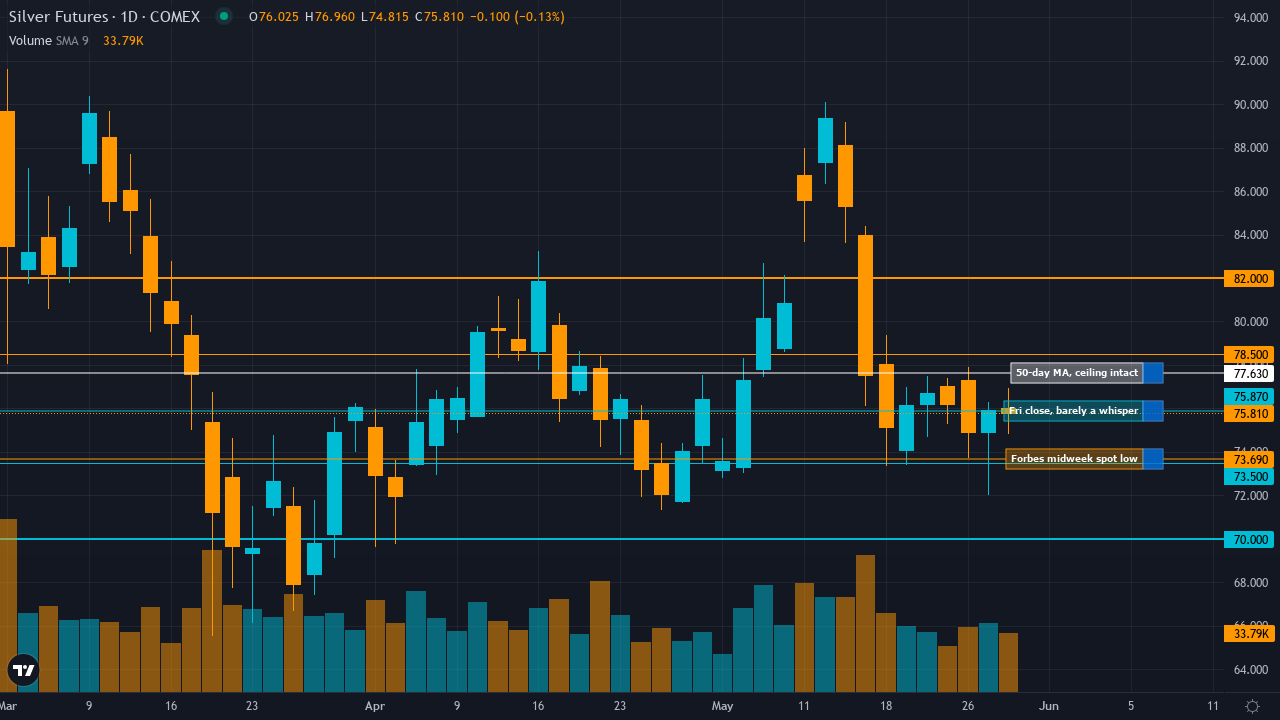

| Monday Open | 76.2 |

| Friday Close | 75.87 |

| Move | -0.43 |

| ▼ R2 | 82 |

| ▼ R1 | 78.5 |

| ▲ S1 | 73.5 |

| ▲ S2 | 70 |

Neither support nor resistance was seriously tested this week, which is itself a statement about the quality of the call. R1 at $78.50 was never remotely threatened, consistent with the bearish lean, while S1 at $73.50 provided a distant floor that silver never approached. Friday's close at $75.87 settled comfortably in the middle of the range, roughly $2.40 above S1 and $2.60 below R1. Forbes reported silver at $73.69 on May 28, suggesting the spot market dipped lower intraweek than the futures close implies, potentially testing closer to S1 territory before recovering. Fortune confirmed silver at $75.37 on Friday morning. The levels framework provided a clean bracket for the week's action, though the lack of any level interaction means they served as context rather than actionable reference points.

The called edge identified the May 12-15 inflation surprise as the dominant near-term driver, with real yields above 2.0% and the Fed's hawkish stance sustaining mathematical headwinds for non-yielding silver. The desk also flagged extreme retail positioning at 90% long as a contrarian bearish overhang, and the UBS demand deterioration data showing industrial fabrication falling 2-3% to a four-year low from photovoltaic substitution. That edge call was directionally correct but the magnitude was slim. Silver barely moved, suggesting the market had already priced the bearish thesis the desk identified. Trading Economics confirmed silver rose 3.04% over the past month, which means the weekly decline of 0.43% sits against a modestly positive backdrop. The edge identification was sound in principle but the market's near-total lack of response suggests the desk was correct about direction while adding little insight about timing or magnitude.

The Economic agent carried the heaviest weight at 30% and drove the bearish thesis through its identification of elevated real yields at 2.30% as structural headwinds. It was directionally correct, if understated. The Technical agent at 15% called BEARISH on the breakdown below the 50-day MA at $77.63, and price indeed never reclaimed that level, though the move was modest enough that 'breakdown' feels generous. The Fundamental agent at 25% weight called BULLISH on the sixth-year structural deficit with 59% industrial demand, and while it was wrong for the week, the 0.43% move barely qualifies as vindication for either side. The Sentiment agent at 10% called BEARISH on extreme retail long positioning, which proved correct in direction. The Institutional agent at 20% called BEARISH on washed-out managed money, adding to the consensus. The Options agent provided no data. The synthesis correctly overrode the Fundamental agent's bullish lean to follow the majority bearish signal, which is the framework doing its job if not exactly setting the world alight.

Silver returns as Market of the Week for what must be approximately the ninth time since I started keeping count, and this time the headline is not a 9% explosion or a 7% collapse but something far quieter: a 0.43% drift lower that the desk called correctly and the market barely noticed.

The week opened with silver at $76.20 and closed at $75.87, a move of 33 cents on a metal that routinely swings five dollars in a session. Forbes reported silver at $73.69 on May 28, down 3.89% compared to the prior week, suggesting the spot market experienced more volatility than the Monday-to-Friday futures window captured. Fortune confirmed silver at $75.37 per ounce on Friday morning, consistent with a quiet end to a quiet week. CoinCodex is forecasting a further 2.26% decline to $73.87 by June 4, which would bring silver back toward the desk's S1 at $73.50.

The bearish thesis rested on three pillars: the May 12-15 inflation surprise sustaining elevated real yields above 2.0%, extreme retail positioning at 90% long creating forced liquidation risk, and emerging evidence from UBS that industrial demand is falling 2-3% as photovoltaic manufacturers substitute away from silver at elevated prices. All three pillars remain standing, but none produced the kind of selling pressure the desk expected. The free MOTW report, published on the Ghost site Sunday evening, laid out the full thesis with specific levels and the UBS revision as the fresh headwind. Readers who used S1 at $73.50 as a downside target and R1 at $78.50 as a cap had a useful framework, even if price refused to approach either boundary.

The grade is C+ rather than B because, while direction was technically correct, a 0.43% move on a metal with 50% annualised volatility is the thinnest of wins. The desk called BEARISH at 6/10 conviction on a market that barely moved, which is the analytical equivalent of predicting rain and getting a light mist. The thesis was right. The result was negligible. Silver's structural story, six consecutive years of deficit with 59% industrial demand, remains the long-term anchor. The short-term reality is that the metal is stuck in a $73-78 range waiting for the June 17-18 FOMC to provide the directional catalyst it has been lacking since the May 15 crash.

For subscribers who have followed the silver saga since February's four consecutive weeks of MOTW glory that produced 30% cumulative gains, the current chapter is a different kind of story. The desk is no longer riding momentum. It is reading consolidation. Less exciting, less profitable, but arguably more honest about what the data supports.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 6/10 | 7491 | 7597.75 | 1.43 | CORRECT | B+ |

| BULLISH at 6/10 and the S&P gained 1.43% to fresh records near 7,600. The fifth consecutive correct BULLISH call on ES, a streak that stretches back to early May and has now delivered roughly 5.6% cumulative gains. The Q1 earnings thesis and RISK-ON regime continue to do the heavy lifting. | |||||||

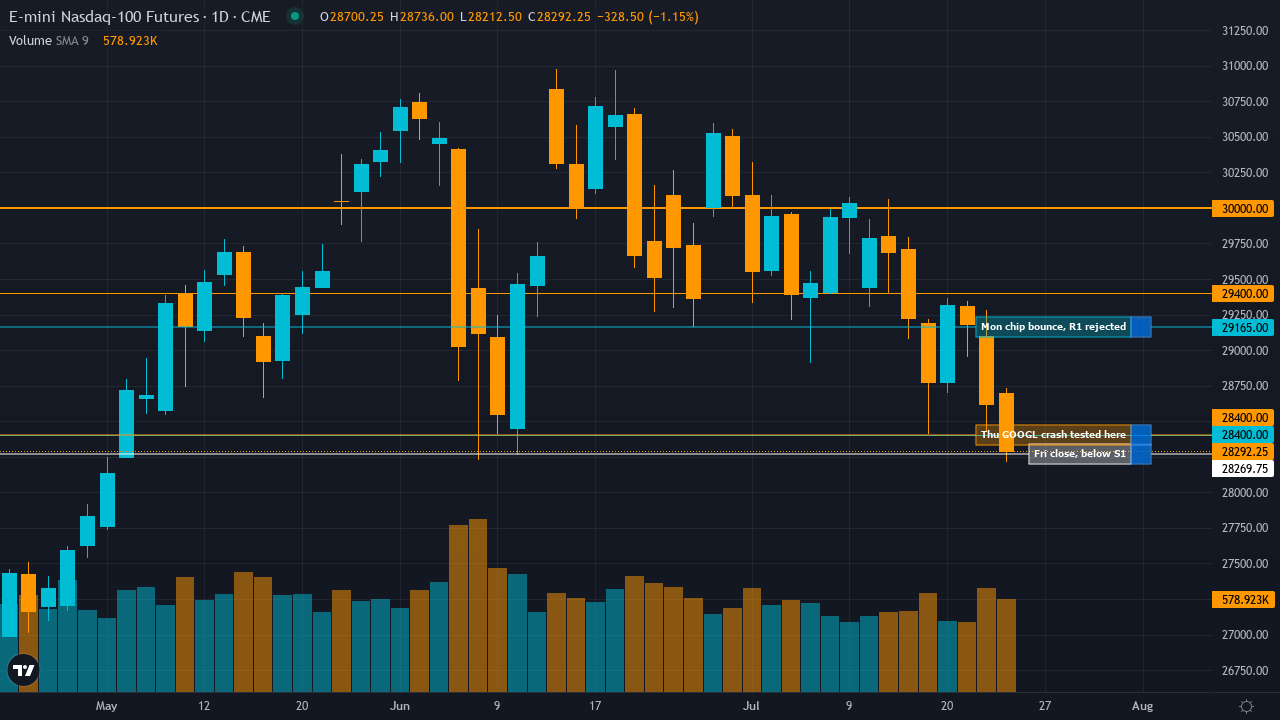

|

Nasdaq 100

CORE

|

BULLISH | 7/10 | 29558.75 | 30402.25 | 2.85 | CORRECT | A |

| BULLISH at 7/10 and the Nasdaq surged 2.85% to fresh all-time highs above 30,400. The Manufacturing PMI surge to 55.3, the strongest since 2022, validated the demand acceleration thesis the desk flagged as underweighted by consensus. After months of agonising NO CALL abstentions that I criticised in every review, the desk has now strung together consecutive correct BULLISH calls on tech. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | 96.42 | 87.89 | -8.85 | CORRECT | A+ |

| BEARISH at minimum conviction and crude collapsed 8.85% as the US-Iran ceasefire extended by 60 days with Hormuz shipping reportedly reopening. Trading Economics confirmed WTI fell below $88 on Friday. Back-to-back bearish wins totalling over 15% in two weeks. The best call on the board by a country mile. | |||||||

|

Gold

CORE

|

NO CALL | — | 4730.7 | 4577 | -3.25 | — | — |

| NO CALL at 5/10 per mandatory miss reset after four consecutive missed calls, and gold dropped another 3.25% to $4,577. The desk was procedurally locked out by its own integrity rules while the metal it once championed continued its decline from January's $5,626 peak. A 3.25% move on a NO CALL is the kind of miss that the miss reset protocol is supposed to prevent by forcing recalibration rather than allowing stubborn repetition. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1594 | 1.1672 | 0.67 | — | — |

| NO CALL for the thirteenth consecutive week, and the euro gained 0.67%, a move that clears the noise threshold and scores as a miss. The desk and EUR/USD have now been in a committed non-relationship for three months. The ECB meeting on June 5, with markets pricing three rate hikes, should finally force a directional view. Or it won't. At this point, I'm not placing bets. | |||||||

|

Silver

EXTENDED

|

BEARISH | 6/10 | 76.2 | 75.87 | -0.43 | CORRECT | C+ |

| This week's MOTW. BEARISH at 6/10 and silver drifted lower by 0.43%, a technically correct call on a market that barely moved. Forbes reported silver at $73.69 midweek before recovering. The full deep-dive is above. The free report is on the Ghost site. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.006312 | 0.006287 | -0.4 | — | — |

| NO CALL at 5/10, the yen drifted 0.4%, well within noise for this pair. The thirteenth consecutive NO CALL on 6J. The desk's yen discipline, refusing to call direction on a pair where intervention risk and rate differential create unpredictable two-way volatility, remains its smartest FX habit. The June 15-16 BoJ meeting looms as the next test. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.3438 | 1.3465 | 0.2 | — | — |

| NO CALL at 5/10 and sterling drifted 20 pips higher, firmly within noise. The mandatory miss reset after four consecutive misses kept the desk sensibly on the sidelines. The eleventh consecutive NO CALL on cable. The June 18 BoE meeting is now the obvious catalyst, and the desk needs to decide whether its prolonged silence on FX is discipline or abdication. | |||||||

|

Copper

EXTENDED

|

BULLISH | 6/10 | 6.32 | 6.393 | 1.16 | CORRECT | B |

| BULLISH at 6/10 and copper gained 1.16%. The US Manufacturing PMI surge to 55.3 provided the fresh demand catalyst the desk identified as underweighted by consensus. Direction correct, modest move, conviction appropriate. The desk's copper analysis has been quietly consistent when it commits. | |||||||

|

Russell 2000

EXTENDED

|

NO CALL | — | 2872.1 | 2924.6 | 1.83 | — | — |

| NO CALL at 5/10 per mandatory miss reset after three consecutive missed calls, and the Russell rallied 1.83%. The desk's three-miss spiral on RTY, from NO CALL to BULLISH to BEARISH with each one wrong, earned the mandatory reset. A 1.83% rally while the desk sits out is frustrating, but the reset protocol exists precisely to break this kind of losing streak before it becomes entrenched. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | 0.7118 | 0.7184 | 0.93 | — | — |

| NO CALL at 5/10 and the Aussie gained 0.93%, a meaningful move the desk missed. The fundamental paradox between the RBA's hawkish action at 4.35% and Governor Bullock's dovish growth warning kept the agents gridlocked. The June 3-4 RBA meeting should resolve this conflict one way or another. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | 110.875 | 112.469 | 1.44 | MISSED | D |

| BEARISH at 5/10 and bonds rallied 1.44%. The desk's long-running bearish bond thesis, which has been its most consistent performer across 2026, finally ran headlong into a week where collapsing oil prices from the Iran ceasefire extension removed the energy-driven inflation fear that had been sustaining the sell-off. When crude drops 8.85% in a week, duration gets a reprieve. The desk's thesis was internally coherent but failed to price the cross-asset implications of its own best call on CL. | |||||||

|

Wheat

FULL DESK

|

BULLISH | 7/10 | 647 | 610.25 | -5.68 | MISSED | F |

| BULLISH at 7/10, the desk's joint-highest conviction call, and wheat dropped 5.68%. The worst US production shortfall since 1972 with 69% of winter wheat areas in drought was not enough to overcome seasonal June harvest pressure and 951.5 million tonnes of global stocks. An F is warranted when your second-strongest conviction call misses by 5.68% in the wrong direction. The desk's wheat record since the March WASDE has been a rollercoaster that nobody asked to ride. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | — | 1197.25 | 1186.5 | -0.9 | — | — |

| NO CALL at confidence 6 with signal below the minimum threshold, and soybeans fell 0.9%. The desk's caution on a market where the signal sat at 0.8, just below the 1.0 minimum for agricultural directional bias, was rewarded by a modest decline that validated the uncertainty. Sometimes the most honest call is 'I don't know enough to commit.' | |||||||

|

Platinum

FULL DESK

|

NO CALL | — | 1973.6 | 1926.5 | -2.39 | — | — |

| NO CALL at 5/10 per disciplined reset after three consecutive misses, and platinum fell 2.39%. The WPIC May 18 report paradox, Q1 surplus versus full-year deficit upgrade, continues to confuse both the desk and the market. A 2.39% decline while the desk abstains scores as a miss, but after last week's F-grade on a BULLISH call that missed by 6.69%, the mandatory neutral stance is the lesser of two evils. | |||||||

|

✦ Best Call: Crude Oil (CL)

BEARISH at 5/10 and crude oil collapsed 8.85% from $96.42 to $87.89. Trading Economics confirmed WTI fell below $88 on Friday as reports emerged that the US and Iran had tentatively agreed to extend their ceasefire by 60 days with unrestricted Hormuz shipping. After months of bearish calls being incinerated by Hormuz headlines, after the 21% moonshot in March and the 13% surge in April, crude oil has now delivered back-to-back weekly bearish wins totalling over 15% in two weeks. The desk whispered its view at minimum conviction, which given the recent history of getting crude spectacularly wrong in both directions is entirely appropriate humility. But whispered or shouted, an 8.85% directional win on the most geopolitically sensitive commodity on the planet is the call of the week. |

⚠️ Worst Call: Wheat (ZW)

BULLISH at 7/10 and wheat crashed 5.68% from 647 to 610.25. The desk doubled down on the May 12 WASDE production shortfall thesis, the worst US wheat crop since 1972 with 69% of winter wheat areas in drought, and the market responded by dumping five and a half percent as seasonal harvest pressure overwhelmed the supply scare. I noted last week that the desk's first directional call on wheat since the mandatory miss-streak reset had landed correctly at +1.77%. One week later, at higher conviction, the thesis has been demolished. Global stocks at 951.5 million tonnes apparently outweigh domestic production drama, and entering the seasonally weak June-August window with 7/10 conviction BULLISH was a timing error that the desk's own analysis identified as a risk and then chose to dismiss. |

The Economic agent had the strongest week across the board. Its identification of the OPEC demand downgrade and IEA contraction forecast as the catalyst for crude oil's collapse proved to be the most valuable single insight on the desk. Its reading of the RISK-ON macro regime with VIX sub-17 correctly supported the equity bullish calls on ES and NQ. And its stagflation framework for bonds, while directionally wrong this week as Treasury bonds rallied on the ceasefire-driven collapse in oil prices, at least had the intellectual coherence to explain why it missed.

The Fundamental agent had a mixed week that exposed its persistent vulnerability. Its supply-deficit work on silver was overridden correctly by the synthesis, but its BULLISH thesis on wheat, built around the WASDE production shortfall, drove the week's worst call. The pattern is familiar: the Fundamental agent identifies real supply-side dynamics but consistently underweights the macro and seasonal forces that determine whether those dynamics translate into price. On copper, its Grasberg deficit thesis produced a correct BULLISH call, so the discipline is not broken, just unreliable when agricultural seasonality enters the equation.

June is a month of catalysts. The ECB meets June 5, with markets fully pricing three rate hikes in 2026 and the desk's thirteen-week EUR/USD NO CALL streak begging for resolution. The June 10 WASDE will determine whether this week's 5.68% wheat collapse was an overreaction or the beginning of a genuine repricing as harvest pressure meets drought reality. The June 15-16 BoJ and June 16-17 FOMC, Kevin Warsh's first full meeting as Chair, form a wall of central bank catalysts that should reshape the rate and FX landscape. Crude oil at $88 is approaching the EIA's Q4 forecast level three months early, raising the question of whether the Hormuz ceasefire is the beginning of a full geopolitical premium unwind or just another false dawn. The desk will have its Sunday views. Given the catalyst density, I expect the NO CALL count to decrease and the directional engagement to increase.