Platinum Forecast This Week — Outlook, Drivers & Key Levels

This week's Platinum outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

This week's Platinum outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

This week's Silver outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Gold (GC): Market may be underestimating depth of central bank demand deterioration (January 5t versus 27t average) while overweighting geopolitical safe-haven narrative that failed to support gold during March 19 6% intraday crash; desk recognizes breakdown is real but timing of BEARISH call after

Core

Divided between extreme fear capitulation suggesting oversold bounce and technical breakdown continuation with majority positioning defensively into quarter-end despite contrarian sentiment signals

Core

Defensive and fearful with 52% AAII bears expecting further downside, but institutional positioning moderately bearish rather than capitulating suggests tactical caution without full panic

Core

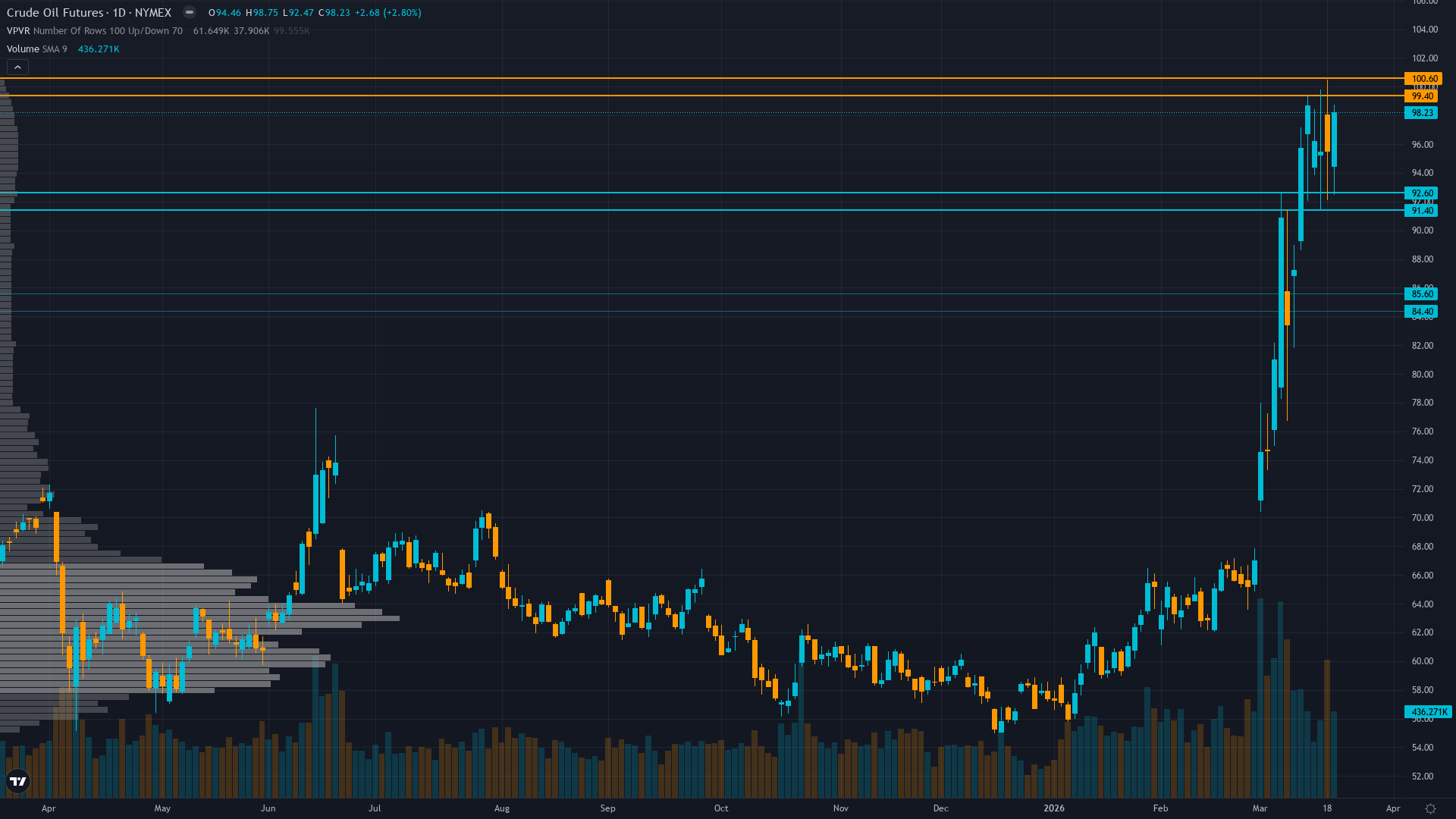

Tactically bullish short-term on geopolitical disruption sustaining but increasingly acknowledging Goldman Sachs Q4 forecast $71 Brent implies significant downside from current $98 WTI as structural oversupply fundamentals expected to reassert once Hormuz normalizes

Core

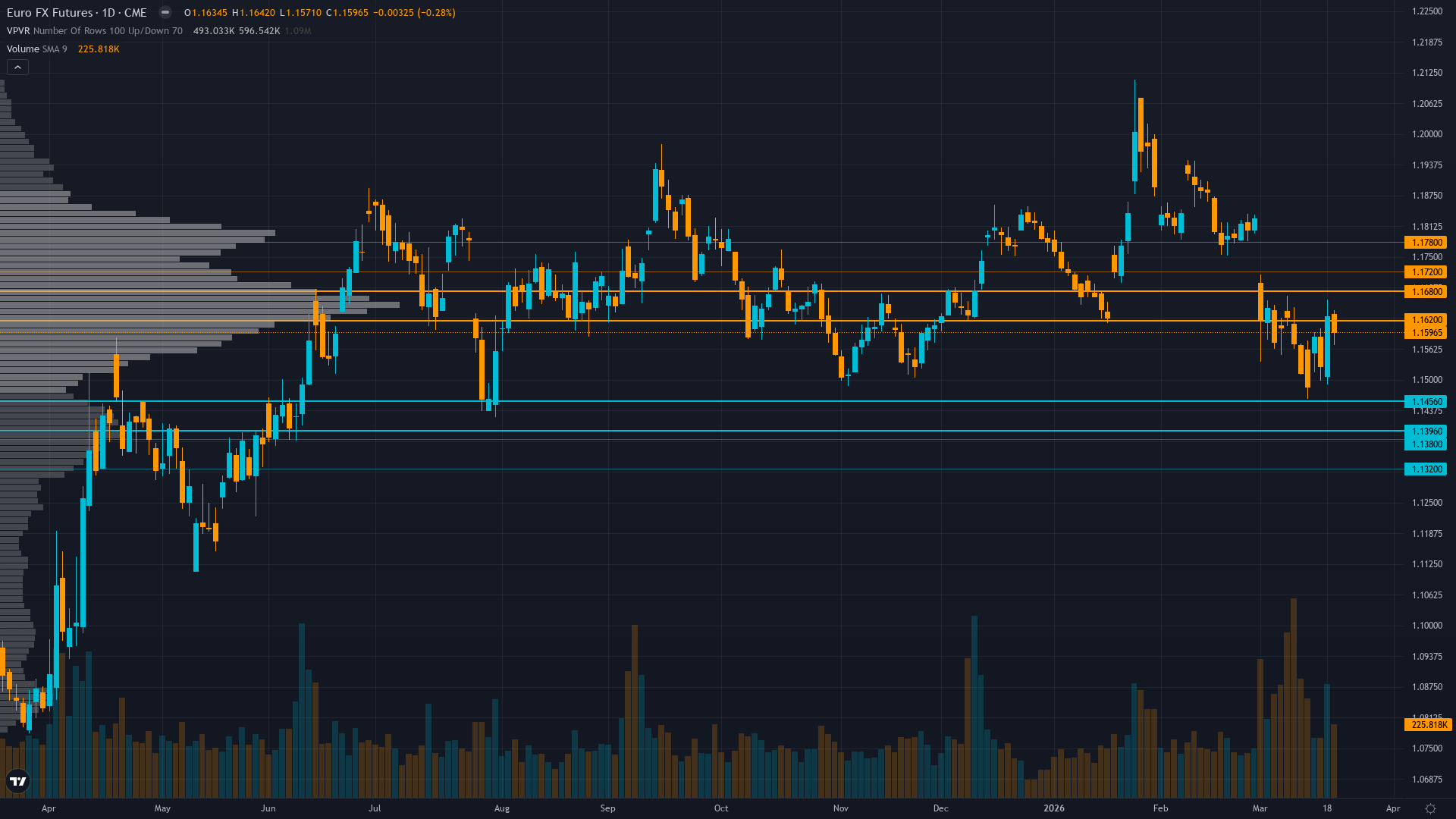

EUR/USD consolidation in 1.15-1.18 range through March with neutral bias after dual central banks delivered expected holds removing catalyst

Extended

Copper elevated on supply deficit narrative but near-term consolidation expected with elevated inventories, China demand uncertainty, and risk-off sentiment creating volatility

Extended

Market consensus fractured between structural bulls targeting $75-85 consolidation and capitulation bears projecting $60-65 test, with CoinCodex algorithm predicting -7.96% decline to $74.20 by March 26 though this forecast predates the March 18-20 hawkish Fed shock

Extended

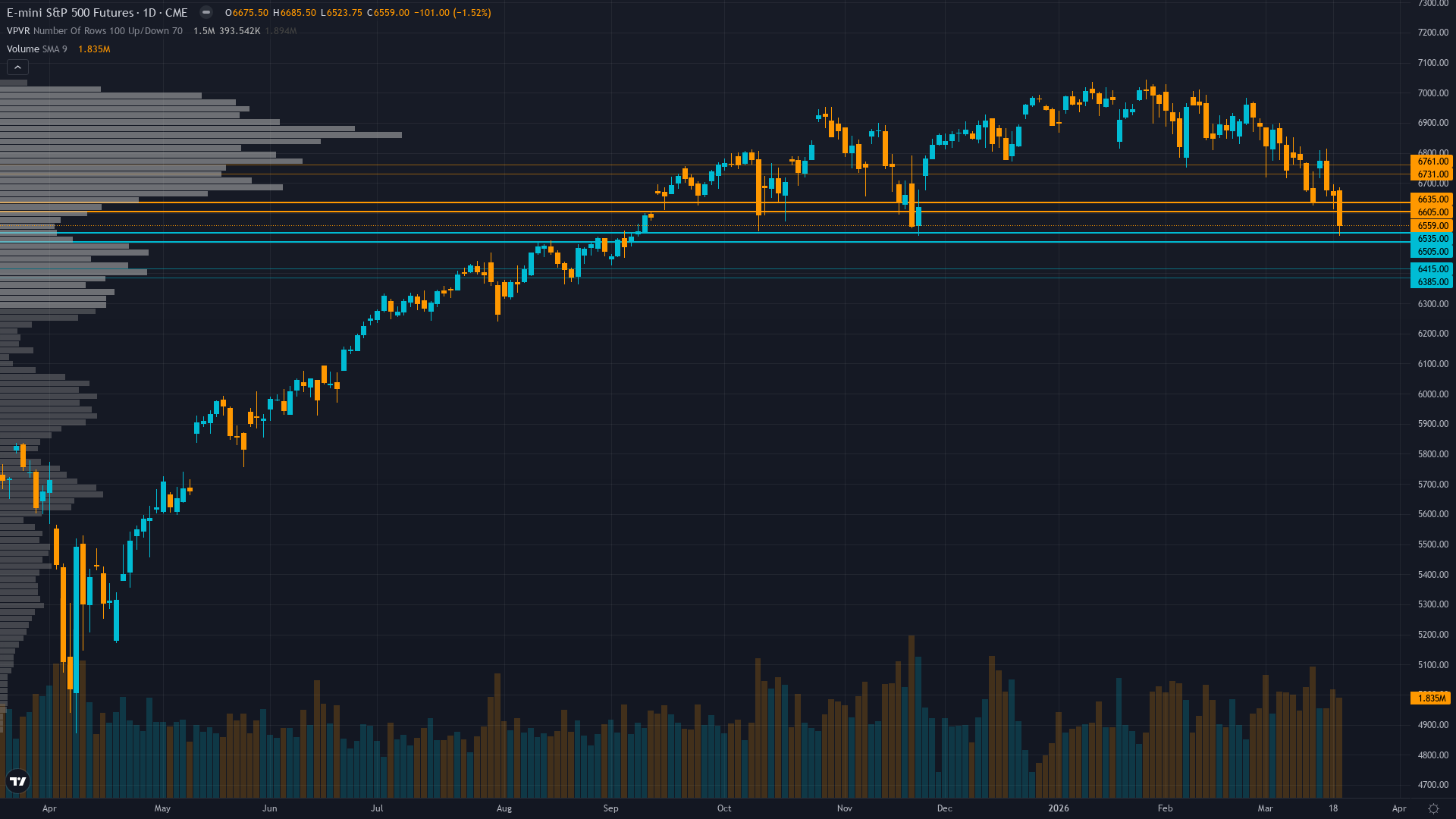

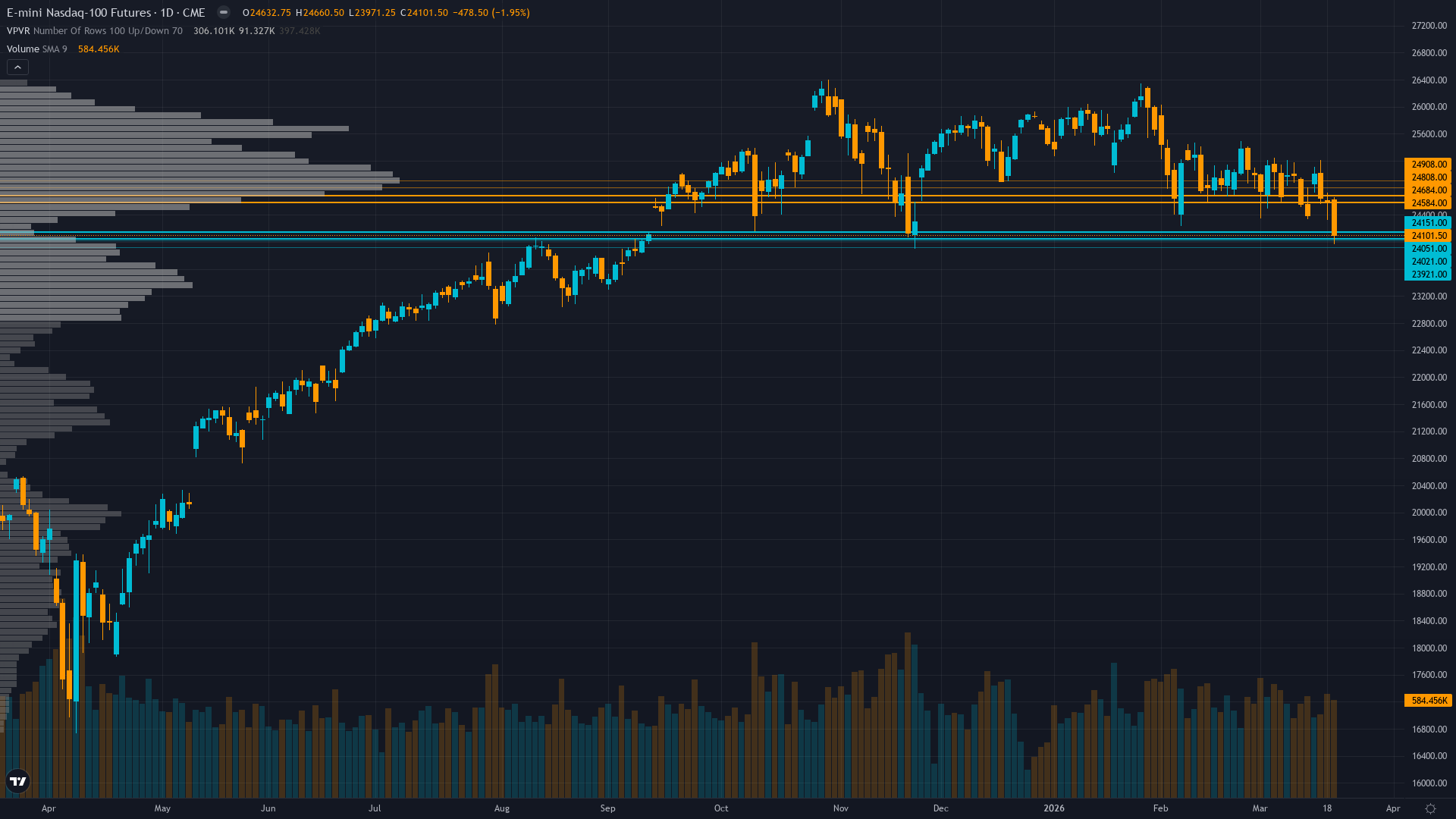

Small-caps under severe pressure from FOMC hawkish pivot removing easing catalyst, but retaining fundamental appeal from 17-22% earnings growth outlook once volatility settles and Fed clarity emerges

Extended

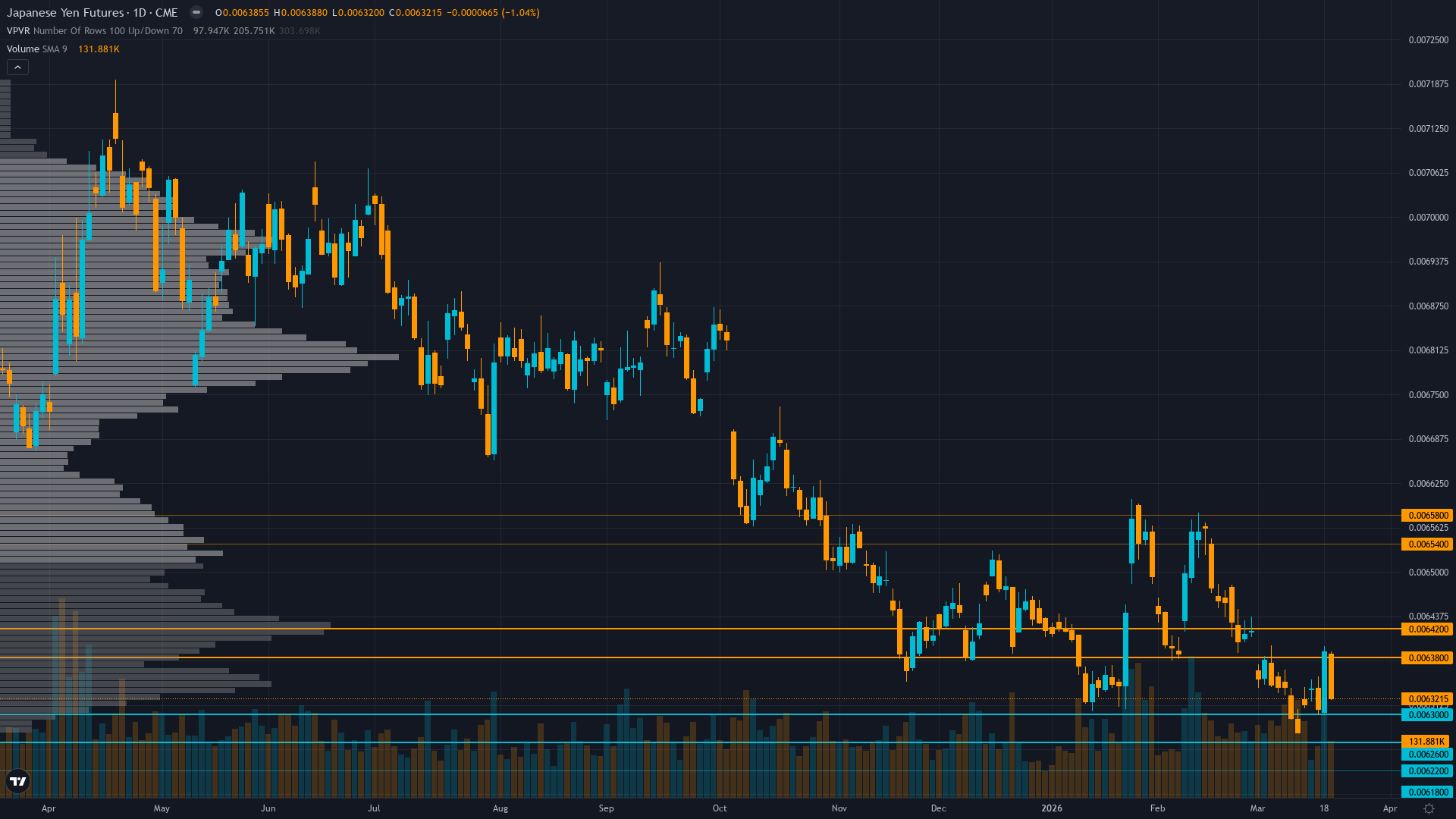

Market expects continued USD/JPY consolidation 156-160 range with slight bearish yen bias on persistent rate differentials; BoJ March hold seen as dovish despite maintained forward guidance

Extended

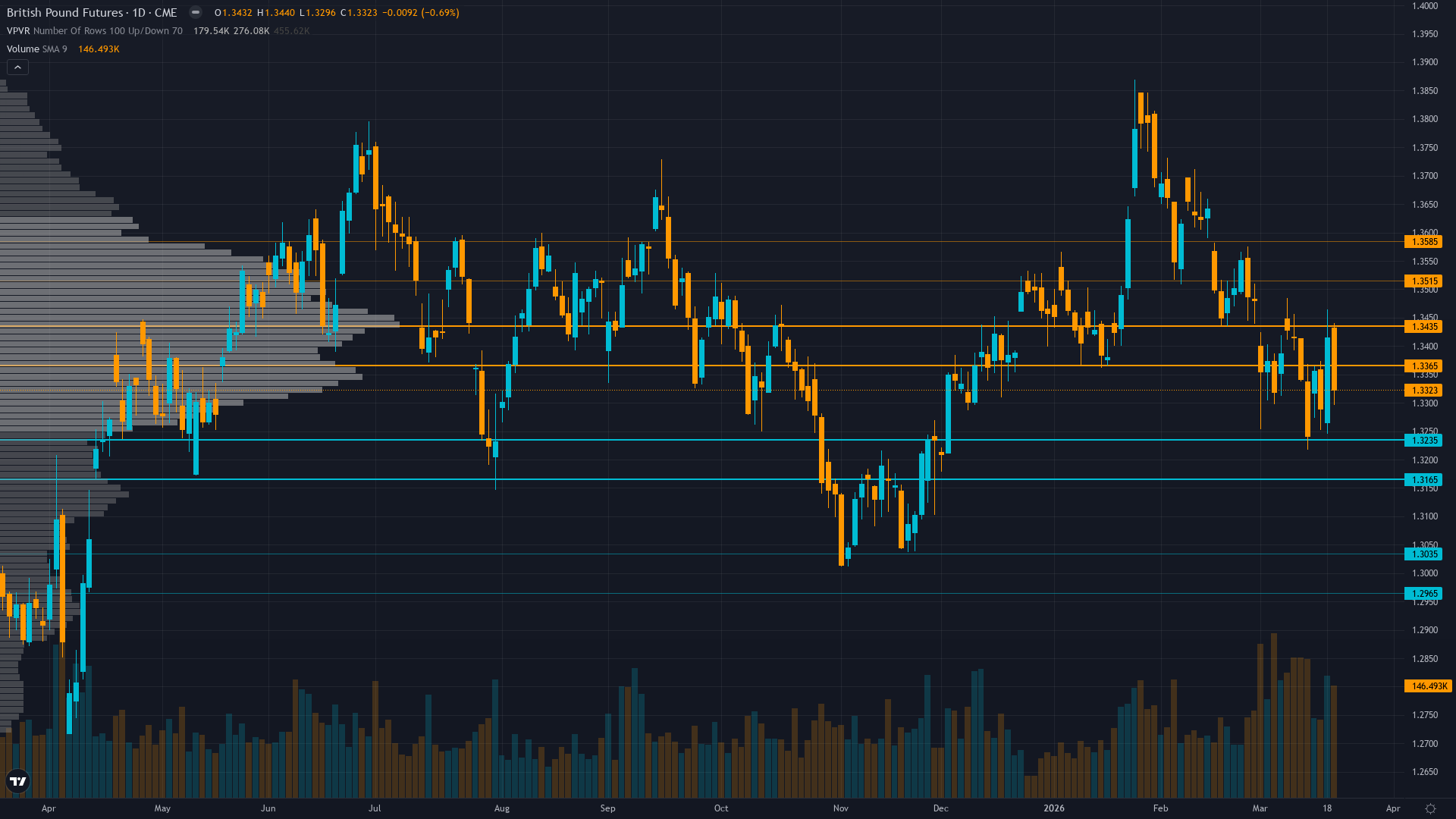

Neutral to mildly bearish consolidation expected with defensive positioning as markets digest BoE's hawkish inflation revision to 3.0-3.5% range following Iran conflict energy shock