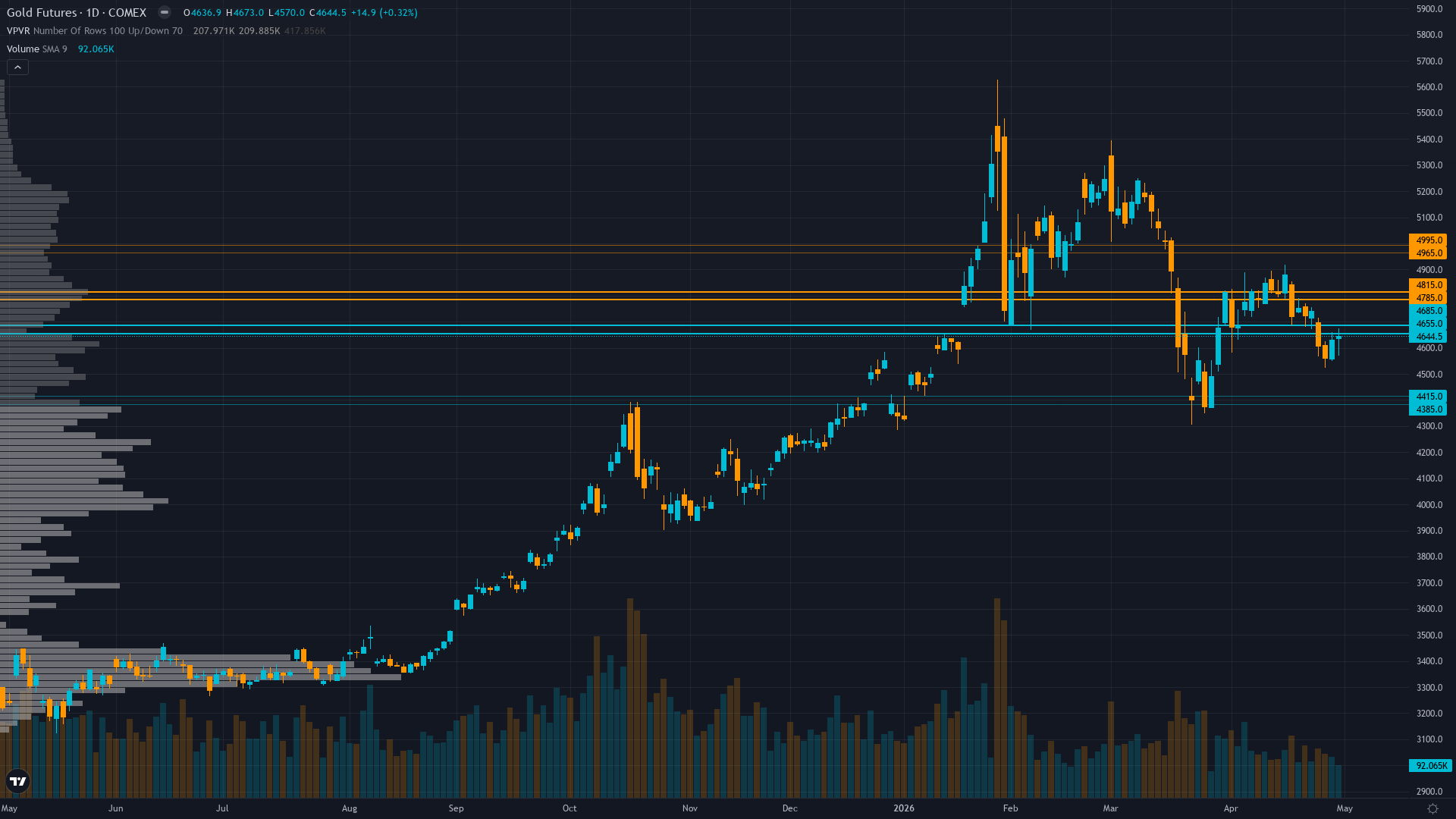

Gold (GC) — -1.5 between 4600 support and 4750 resistance with 5/10 confidence

Mixed with institutional price targets remaining at $5,000-5,400 but near-term positioning increasingly cautious following April 28-29 FOMC hawkish guidance eliminating near-term rate cut expectations and validating higher-for-longer trajectory

Mixed with institutional price targets remaining at $5,000-5,400 but near-term positioning increasingly cautious following April 28-29 FOMC hawkish guidance eliminating near-term rate cut expectations and validating higher-for-longer trajectory

Post-FOMC breakdown extending with gold at $4,650 after April 28-29 hawkish Fed guidance cemented higher-for-longer stance creating sustained real yield headwind despite Q1 central bank demand holding firm at 244 tonnes

Technical structure severely damaged with decisive break below $4,700 support following FOMC meeting confirming corrective phase from January $5,626 all-time high now exceeds 17% decline

Three consecutive missed calls degrading thesis credibility while conflicting discipline signals create informational uncertainty requiring tactical caution ahead of June FOMC decision cycle

| ▼ Resistance Zone 2 | 4875 – 4925 |

| ▼ Resistance Zone 1 | 4725 – 4775 |

| ─ Pivot Area | ~4650 |

| ▲ Support Zone 1 | 4575 – 4625 |

| ▲ Support Zone 2 | 4425 – 4475 |

Breaking down through $4,700 support post-FOMC with price at $4,650 now 17% below January peak, RSI neutral zone 47-50 showing no directional conviction, next support $4,600 then major $4,450 zone

Modestly undervalued at $4,650 versus institutional $5,000-5,400 targets but April 28-29 FOMC hawkish guidance validates higher-for-longer Fed trajectory creating persistent real yield headwind offsetting Q1 central bank demand of 244t that held firm

Managed money net long ~92,775 contracts at moderate levels while Q1 central bank demand 244t validates structural bid floor though Western ETF flows turned negative in March erasing Q1 inflows per World Gold Council April 29 report

GVZ volatility moderating to 27.87 from April highs above 30 reflecting post-correction stabilization attempt but insufficient options flow data for clear directional bias as discipline remains confirming signal only

Fed held April 28-29 at 3.5-3.75% as expected but delivered hawkish forward guidance cementing higher-for-longer stance, DXY at 98.2 consolidating after rebound above 100, VIX 16.89 below 20 threshold indicating normalized equity conditions creating RISK-ON backdrop paradoxically pressuring safe-haven gold

Inverted - short-term 24.5% elevated above longer-term 21.5% indicating recent stress from March-April correction sequence and April 28-29 FOMC hawkish surprise but moderating from 26.8% 20-day peak as market attempts post-catalyst stabilization

Post-major FOMC hawkish surprise volatility remains elevated 2-4 weeks then resolves directionally; 70% of similar Fed policy pivot episodes during correction phases continue lower within 30 days though current 78th percentile vol at $4,650 suggests climactic selling may be approaching exhaustion near $4,450-4,600 major support zone

High volatility regime day 18 typically lasts 10-20 days for gold suggesting potential further moderation into mid-May as market fully digests April FOMC implications with 60% probability of compression below 70th percentile by late May once directional resolution occurs

Elevated volatility at 78th percentile requires wider stops with daily ranges potentially 2.5-3.5% versus normal 1.5-2%; current $4,600-4,750 consolidation zone suggests breakouts become more reliable once volatility normalizes below 70th percentile by late May, but until then price action subject to elevated noise and false signal risk

Current high volatility at $4,650 with GVZ 27.87 and historical vol at 78th percentile suggests asymmetric moves possible: 4-7% downside risk to $4,450-4,300 if breakdown continues versus 2-4% upside to $4,750-4,900 resistance creating roughly 2:1 unfavorable risk-reward for bullish positioning; volatility spike reflects genuine repricing from Fed hawkish regime shift rather than temporary panic, requiring confirmation of directional resolution and central bank bid activation before re-engaging long

|

⚠️ Primary Risk

Continued dollar strength above DXY 100 combined with June FOMC reaffirming hawkish April stance validates no 2026 rate cuts scenario driving gold toward $4,450-4,300 major support zone representing additional 4-7% downside from current levels Probability: MEDIUM

|

✦ Primary Opportunity

Fed softens hawkish April tone at June meeting suggesting data-dependent flexibility triggers dollar reversal from current 98.2 level supporting gold recovery toward $4,800-4,900 resistance within 3-4 weeks as rate cut expectations resurface Timeframe: Next 3-6 weeks through June 17 FOMC and into early July as market digests whether April hawkish guidance represents regime shift or temporary pause in easing trajectory

|

MACRO REGIME CLASSIFICATION: RISK-ON with gold divergence. VIX at 16.89 sits comfortably below the 20 threshold signaling normalized equity risk appetite, credit spreads stable, and broad markets showing complacency. However, gold is paradoxically breaking down despite traditional safe-haven status, revealing that monetary policy recalibration is overriding haven demand dynamics. This creates a DIVERGENT regime where equity risk-on conditions coincide with precious metal weakness driven by Fed policy trajectory rather than systemic stress.

Gold stands at $4,650 on May 3, 2026, extending the breakdown that began in late April and accelerated following the April 28-29 FOMC meeting. Post-input development identified: The Fed left rates unchanged as widely anticipated but delivered materially hawkish forward guidance that has cemented market expectations for higher-for-longer policy stance, eliminating near-term rate cut probability and sustaining elevated real yields hostile to non-yielding gold. Discovery Alert reports (May 2) that this hawkish tone has pressured gold markets through the critical $4,700 support level.

Current positioning represents a catastrophic 17% decline from January's $5,626 all-time high and marks the continuation of the corrective phase that began with the March CPI shock. The discipline data presents deeply conflicting signals creating genuine analytical uncertainty: Economic BULLISH (+1.5 confidence 6) on declining real yields to 1.90% and weakening dollar trends but acknowledges all conditions are multi-week old and already priced. Technical BEARISH (-2.0 confidence 6) on broken structure below $4,600 with downtrend intact.

Fundamental BULLISH (+1.5 confidence 7) on valuation versus targets and Q1 central bank demand holding at 244t despite Western ETF March outflows. Institutional BULLISH (+1.5 confidence 6) on moderate positioning and April GLD inflows of $1.3B demonstrating conviction. Sentiment NEUTRAL (+0.5 confidence 4) with no extreme reading. Options NO CALL (insufficient data). The most significant fresh development is the World Gold Council Q1 2026 report released April 29 showing central bank demand at 244 tonnes (+3% YoY) validating the structural bid remains intact, but Western ETF flows turned sharply negative in March erasing Q1 inflows as elevated real yields suppress financial demand.

This bifurcation confirms the fundamental thesis: structural central bank support provides a floor around $4,450-4,600, but cyclical Western investor demand faces sustained headwinds until Fed policy shifts. The April 28-29 FOMC outcome represents the critical catalyst that was anticipated in last week's synthesis—and it delivered a hawkish result that validates the bearish case for near-term continuation of weakness. With three consecutive missed calls (May 1 NO CALL -2.48%, April 24 BULLISH -3.24%, April 17 NO CALL +1.66%), thesis credibility is materially degraded requiring mandatory conviction reduction per Rule 3.

The consecutive miss streak of 3 approaches but has not yet reached the 4-miss reset threshold. Reviewing last 4 graded weeks under Thesis Health Score: 3 of 4 moved contrary to any potential bullish bias (subtract 1.5), net cumulative decline approximately -2% which does not exceed 2x the 2.41% Average Weekly Move threshold. However, the pattern is clear: the bullish structural thesis (central bank demand, dollar weakness, negative real rates) has been overwhelmed by the cyclical hawkish Fed repricing.

The path forward depends critically on whether the April FOMC hawkish guidance represents the new baseline or a temporary pause before mid-year rate cut resumption. Current technical structure shows gold testing $4,600 support with next major floor at $4,450-4,500 (200-day MA zone). A breakdown below $4,600 would likely trigger accelerated liquidation toward that major support. Conversely, a stabilization here and recovery above $4,750 would signal exhaustion of the post-FOMC selling wave. With VIX below 20 in RISK-ON regime yet gold breaking down (opposing the macro backdrop), conflicting discipline signals across 6 agents, three consecutive misses degrading analytical credibility, and insufficient evidence that $4,650 represents a durable floor versus a pause in ongoing correction, the most intellectually honest assessment is BEARISH with low conviction.

This acknowledges the technical breakdown momentum and FOMC catalyst headwind while respecting that positioning has normalized, central bank structural demand remains at 244t quarterly pace, and institutional targets still cluster at $5,000-5,400 suggesting 8-16% upside potential if/when Fed policy trajectory shifts. The probable weekly move from current $4,650 is estimated at 2-4%, well above the 0.30% Noise Floor, making directional assessment meaningful. However, conviction is capped at 5 due to: (1) three consecutive misses requiring -3 penalty, (2) conflicting discipline signals requiring -1, (3) opposing macro regime (RISK-ON) requiring -1 unless asset-specific catalyst overrides, which the April FOMC hawkish guidance does justify as gold-specific bearish driver.

Initial assessment 6, minus 3 for miss streak, minus 1 for conflicts, minus 1 for regime opposition (though partially mitigated by FOMC catalyst) = conviction 5 at the minimum threshold for issuing a directional call. Final conviction 5 represents tactical bearish lean acknowledging breakdown momentum post-FOMC while recognizing substantial uncertainty about whether $4,600 holds or fails.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 1, 2026 | NO CALL | 5/10 | ➖ |

| April 24, 2026 | BULLISH | 6/10 | ❌ |

| April 17, 2026 | NO CALL | 6/10 | ➖ |

| April 10, 2026 | BULLISH | 6/10 | ✅ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | BEARISH | 4/10 | ✅ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | BULLISH | 6/10 | ❌ |

| March 6, 2026 | BULLISH | 8/10 | ❌ |

| February 27, 2026 | BULLISH | 8/10 | ✅ |

| February 21, 2026 | BULLISH | 8/10 | ✅ |

| February 13, 2026 | BULLISH | 8/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Gold (GC) Report Date: May 3, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 28 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: BREAKING DOWN Regime: POST-FOMC BREAKDOWN CONTINUATION Sentiment: FEAR ── WHAT THE MARKET SEES ───────────────────────── Mixed with institutional price targets remaining at $5,000-5,400 but near-term positioning increasingly cautious following April 28-29 FOMC hawkish guidance eliminating near-term rate cut expectations and validating higher-for-longer trajectory ── WHAT THE MARKET IS MISSING ─────────────────── Market may be underestimating significance of Q1 central bank demand holding at 244t (+3% YoY) versus widely-discussed March ETF outflows, suggesting structural bid floor at $4,450-4,600 remains intact; however, three consecutive missed calls indicate desk lacks clear informational edge in current environment and timing of any bullish counter-positioning requires confirmation that April FOMC hawkish guidance was peak hawkishness rather than new baseline ── KEY DRIVERS ────────────────────────────────── 1. Post-FOMC breakdown extending with gold at $4,650 after April 28-29 hawkish Fed guidance cemented higher-for-longer stance creating sustained real yield headwind despite Q1 central bank demand holding firm at 244 tonnes 2. Technical structure severely damaged with decisive break below $4,700 support following FOMC meeting confirming corrective phase from January $5,626 all-time high now exceeds 17% decline 3. Three consecutive missed calls degrading thesis credibility while conflicting discipline signals create informational uncertainty requiring tactical caution ahead of June FOMC decision cycle ── KEY ZONES ──────────────────────────────────── Resistance 2: 4875 – 4925 Resistance 1: 4725 – 4775 Pivot: ~4650 Support 1: 4575 – 4625 Support 2: 4425 – 4475 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BULLISH Institutional: BULLISH Options: NO CALL Economic: BULLISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Breaking down through $4,700 support post-FOMC with price at $4,650 now 17% below January peak, RSI neutral zone 47-50 showing no directional conviction, next support $4,600 then major $4,450 zone ── FUNDAMENTAL ASSESSMENT ─────────────────────── Modestly undervalued at $4,650 versus institutional $5,000-5,400 targets but April 28-29 FOMC hawkish guidance validates higher-for-longer Fed trajectory creating persistent real yield headwind offsetting Q1 central bank demand of 244t that held firm ── INSTITUTIONAL POSITIONING ──────────────────── Managed money net long ~92,775 contracts at moderate levels while Q1 central bank demand 244t validates structural bid floor though Western ETF flows turned negative in March erasing Q1 inflows per World Gold Council April 29 report ── OPTIONS FLOW ───────────────────────────────── GVZ volatility moderating to 27.87 from April highs above 30 reflecting post-correction stabilization attempt but insufficient options flow data for clear directional bias as discipline remains confirming signal only ── ECONOMIC BACKDROP ──────────────────────────── Fed held April 28-29 at 3.5-3.75% as expected but delivered hawkish forward guidance cementing higher-for-longer stance, DXY at 98.2 consolidating after rebound above 100, VIX 16.89 below 20 threshold indicating normalized equity conditions creating RISK-ON backdrop paradoxically pressuring safe-haven gold ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 78th Trend: Contracting ▼ Days in Regime: 18 Term Structure: inverted - short-term 24.5% elevated above longer-term 21.5% indicating recent stress from March-April correction sequence and April 28-29 FOMC hawkish surprise but moderating from 26.8% 20-day peak as market attempts post-catalyst stabilization Historical Pattern: Post-major FOMC hawkish surprise volatility remains elevated 2-4 weeks then resolves directionally; 70% of similar Fed policy pivot episodes during correction phases continue lower within 30 days though current 78th percentile vol at $4,650 suggests climactic selling may be approaching exhaustion near $4,450-4,600 major support zone Outlook: High volatility regime day 18 typically lasts 10-20 days for gold suggesting potential further moderation into mid-May as market fully digests April FOMC implications with 60% probability of compression below 70th percentile by late May once directional resolution occurs Trading Context: Elevated volatility at 78th percentile requires wider stops with daily ranges potentially 2.5-3.5% versus normal 1.5-2%; current $4,600-4,750 consolidation zone suggests breakouts become more reliable once volatility normalizes below 70th percentile by late May, but until then price action subject to elevated noise and false signal risk Vol Risk/Opportunity: Current high volatility at $4,650 with GVZ 27.87 and historical vol at 78th percentile suggests asymmetric moves possible: 4-7% downside risk to $4,450-4,300 if breakdown continues versus 2-4% upside to $4,750-4,900 resistance creating roughly 2:1 unfavorable risk-reward for bullish positioning; volatility spike reflects genuine repricing from Fed hawkish regime shift rather than temporary panic, requiring confirmation of directional resolution and central bank bid activation before re-engaging long ── PRIMARY RISK ───────────────────────────────── Continued dollar strength above DXY 100 combined with June FOMC reaffirming hawkish April stance validates no 2026 rate cuts scenario driving gold toward $4,450-4,300 major support zone representing additional 4-7% downside from current levels Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Fed softens hawkish April tone at June meeting suggesting data-dependent flexibility triggers dollar reversal from current 98.2 level supporting gold recovery toward $4,800-4,900 resistance within 3-4 weeks as rate cut expectations resurface Timeframe: Next 3-6 weeks through June 17 FOMC and into early July as market digests whether April hawkish guidance represents regime shift or temporary pause in easing trajectory ── NEXT CATALYST ────────────────���─────────────── Date: June 17, 2026 Event: Federal Reserve FOMC Meeting decision with market assessing whether April hawkish guidance represents new baseline or temporary positioning ahead of potential mid-year rate cut resumption Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── MACRO REGIME CLASSIFICATION: RISK-ON with gold divergence. VIX at 16.89 sits comfortably below the 20 threshold signaling normalized equity risk appetite, credit spreads stable, and broad markets showing complacency. However, gold is paradoxically breaking down despite traditional safe-haven status, revealing that monetary policy recalibration is overriding haven demand dynamics. This creates a DIVERGENT regime where equity risk-on conditions coincide with precious metal weakness driven by Fed policy trajectory rather than systemic stress. Gold stands at $4,650 on May 3, 2026, extending the breakdown that began in late April and accelerated following the April 28-29 FOMC meeting. Post-input development identified: The Fed left rates unchanged as widely anticipated but delivered materially hawkish forward guidance that has cemented market expectations for higher-for-longer policy stance, eliminating near-term rate cut probability and sustaining elevated real yields hostile to non-yielding gold. Discovery Alert reports (May 2) that this hawkish tone has pressured gold markets through the critical $4,700 support level. Current positioning represents a catastrophic 17% decline from January's $5,626 all-time high and marks the continuation of the corrective phase that began with the March CPI shock. The discipline data presents deeply conflicting signals creating genuine analytical uncertainty: Economic BULLISH (+1.5 confidence 6) on declining real yields to 1.90% and weakening dollar trends but acknowledges all conditions are multi-week old and already priced. Technical BEARISH (-2.0 confidence 6) on broken structure below $4,600 with downtrend intact. Fundamental BULLISH (+1.5 confidence 7) on valuation versus targets and Q1 central bank demand holding at 244t despite Western ETF March outflows. Institutional BULLISH (+1.5 confidence 6) on moderate positioning and April GLD inflows of $1.3B demonstrating conviction. Sentiment NEUTRAL (+0.5 confidence 4) with no extreme reading. Options NO CALL (insufficient data). The most significant fresh development is the World Gold Council Q1 2026 report released April 29 showing central bank demand at 244 tonnes (+3% YoY) validating the structural bid remains intact, but Western ETF flows turned sharply negative in March erasing Q1 inflows as elevated real yields suppress financial demand. This bifurcation confirms the fundamental thesis: structural central bank support provides a floor around $4,450-4,600, but cyclical Western investor demand faces sustained headwinds until Fed policy shifts. The April 28-29 FOMC outcome represents the critical catalyst that was anticipated in last week's synthesis—and it delivered a hawkish result that validates the bearish case for near-term continuation of weakness. With three consecutive missed calls (May 1 NO CALL -2.48%, April 24 BULLISH -3.24%, April 17 NO CALL +1.66%), thesis credibility is materially degraded requiring mandatory conviction reduction per Rule 3. The consecutive miss streak of 3 approaches but has not yet reached the 4-miss reset threshold. Reviewing last 4 graded weeks under Thesis Health Score: 3 of 4 moved contrary to any potential bullish bias (subtract 1.5), net cumulative decline approximately -2% which does not exceed 2x the 2.41% Average Weekly Move threshold. However, the pattern is clear: the bullish structural thesis (central bank demand, dollar weakness, negative real rates) has been overwhelmed by the cyclical hawkish Fed repricing. The path forward depends critically on whether the April FOMC hawkish guidance represents the new baseline or a temporary pause before mid-year rate cut resumption. Current technical structure shows gold testing $4,600 support with next major floor at $4,450-4,500 (200-day MA zone). A breakdown below $4,600 would likely trigger accelerated liquidation toward that major support. Conversely, a stabilization here and recovery above $4,750 would signal exhaustion of the post-FOMC selling wave. With VIX below 20 in RISK-ON regime yet gold breaking down (opposing the macro backdrop), conflicting discipline signals across 6 agents, three consecutive misses degrading analytical credibility, and insufficient evidence that $4,650 represents a durable floor versus a pause in ongoing correction, the most intellectually honest assessment is BEARISH with low conviction. This acknowledges the technical breakdown momentum and FOMC catalyst headwind while respecting that positioning has normalized, central bank structural demand remains at 244t quarterly pace, and institutional targets still cluster at $5,000-5,400 suggesting 8-16% upside potential if/when Fed policy trajectory shifts. The probable weekly move from current $4,650 is estimated at 2-4%, well above the 0.30% Noise Floor, making directional assessment meaningful. However, conviction is capped at 5 due to: (1) three consecutive misses requiring -3 penalty, (2) conflicting discipline signals requiring -1, (3) opposing macro regime (RISK-ON) requiring -1 unless asset-specific catalyst overrides, which the April FOMC hawkish guidance does justify as gold-specific bearish driver. Initial assessment 6, minus 3 for miss streak, minus 1 for conflicts, minus 1 for regime opposition (though partially mitigated by FOMC catalyst) = conviction 5 at the minimum threshold for issuing a directional call. Final conviction 5 represents tactical bearish lean acknowledging breakdown momentum post-FOMC while recognizing substantial uncertainty about whether $4,600 holds or fails.