Full Desk

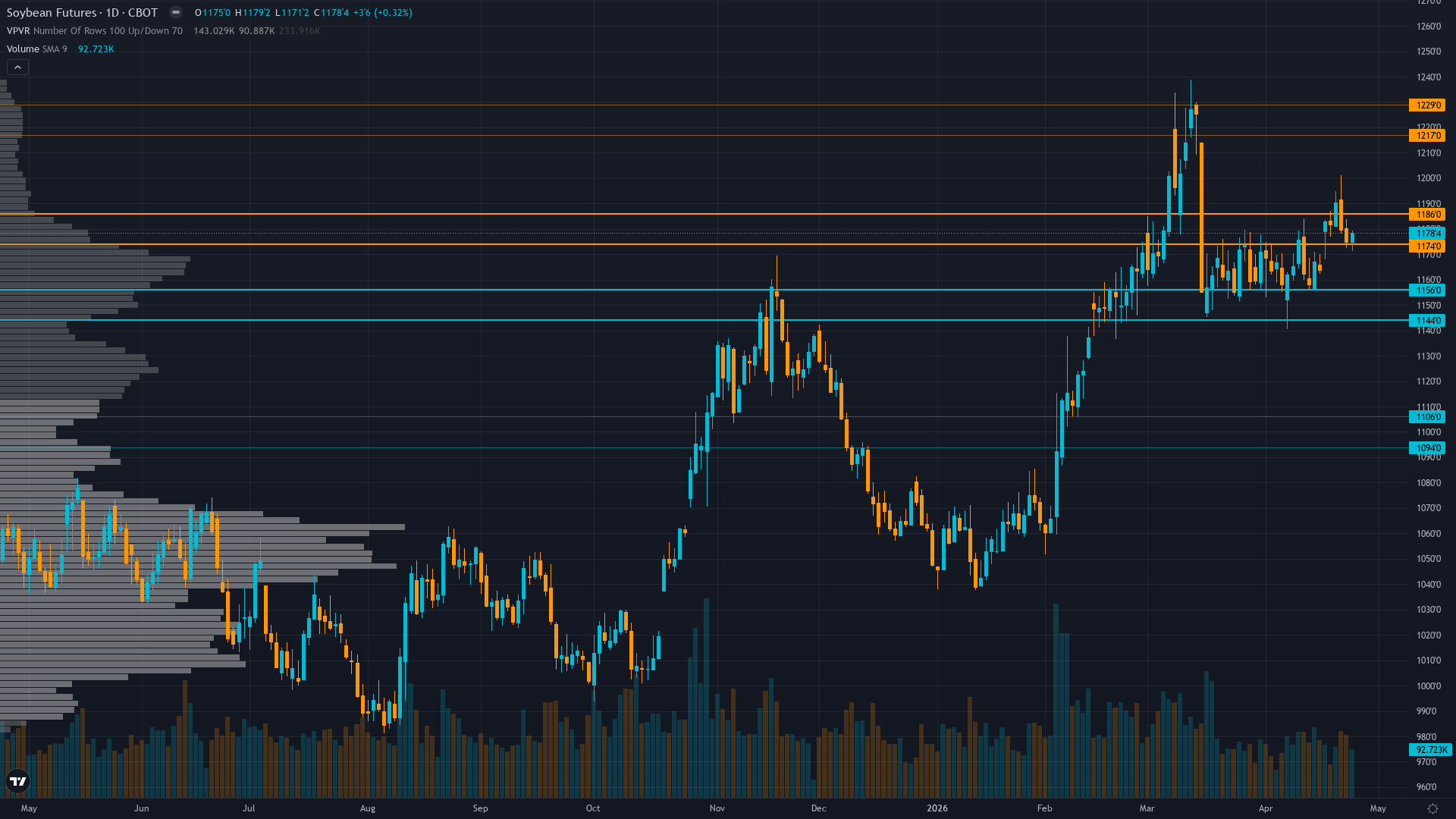

Soybeans (ZS) — 0.3 between 1175 support and 1210 resistance with 5/10 confidence

Mixed with technical bulls citing intact uptrend and renewable diesel structural support offset by positioning analysts warning of extreme crowding at 90th+ percentile and fundamental analysts noting Brazilian pricing advantages creating two-way uncertainty