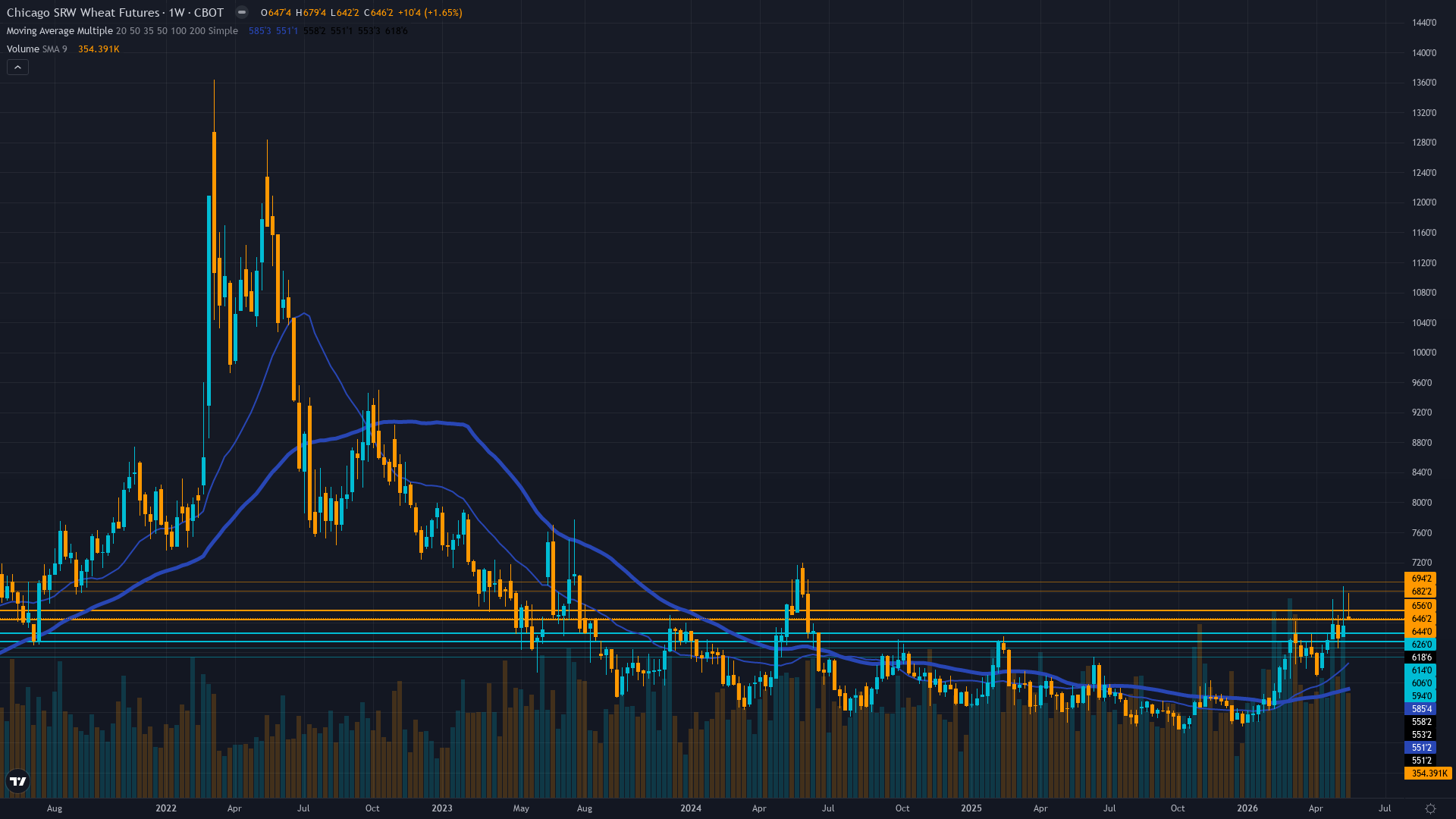

Wheat (ZW) — consolidating after rally in high regime

Cautiously bullish on May 12 WASDE production downgrades confirming most severe U.S. wheat shortfall since 1972 with crop conditions at 28% good-to-excellent versus 46% last year, yet increasingly concerned about sustainability above 650 given 6% pullback from May 12 highs, global stocks at 951.5 mi

Cautiously bullish on May 12 WASDE production downgrades confirming most severe U.S. wheat shortfall since 1972 with crop conditions at 28% good-to-excellent versus 46% last year, yet increasingly concerned about sustainability above 650 given 6% pullback from May 12 highs, global stocks at 951.5 million tonnes (34.52% stocks-to-use ratio), and approaching seasonal June-August harvest pressure period

May 12 WASDE bullish production shock showing U.S. wheat output at 1,561 million bushels (lowest since 1972, down 21.3% YoY) with crop conditions at 28% good-to-excellent versus 46% last year and 69% of winter wheat areas in drought, yet current price at 647 already reflects substantial weather premium 32% above October lows suggesting much of the supply tightening is priced while global stocks remain at record 951.5 million tonnes

Institutional positioning shows net short -53,852 contracts as of May 5 representing continued bearish stance despite rally, with 84% of extreme shorts from prior months already covered removing asymmetric squeeze fuel yet still creating modest short-covering potential if June 10 WASDE confirms additional production downgrades from ongoing drought stress

Entering seasonally weak June-August period for Northern Hemisphere wheat as harvest pressure typically weighs on prices, yet 2026 unique drought conditions with 70% of winter wheat areas affected and USDA projecting season-average price at $6.50/bushel (up $1.50 YoY) creates tension where seasonal bearish patterns clash with severe supply-side fundamentals

| ▼ Resistance Zone 2 | 683.25 – 693.25 |

| ▼ Resistance Zone 1 | 655.00 – 665.00 |

| ─ Pivot Area | ~647.00 |

| ▲ Support Zone 1 | 630.00 – 640.00 |

| ▲ Support Zone 2 | 605.00 – 615.00 |

Price at 647 consolidating in 635-660 range after 1.77% weekly gain, trading 32% above October 492 capitulation lows yet 6% below May 12 intraday peak at 688.25 (52-week high), establishing position above key moving averages in emerging uptrend structure with RSI estimated 55-60 indicating bullish momentum without overbought extremes

Profoundly bullish U.S. supply-side dynamics with May 12 WASDE confirming production at 1,561 million bushels (lowest since 1972, down 21.3% YoY) and crop conditions at 28% good-to-excellent versus 46% last year with 69% of winter wheat areas in drought per Agriculture in Drought report, yet global stocks remain structurally ample at 951.5 million tonnes creating fundamental tension where U.S. regional supply destruction meets global oversupply baseline requiring export flow monitoring to determine whether domestic tightness translates to sustained price premium

Managed money net short -53,852 contracts per May 5 COT data representing shift from marginal net long +0.9K in prior period to decisive short position, yet absolute positioning remains mid-range (45th-55th percentile) without extreme after 84% of peak shorts covered creating balanced two-way risk with modest squeeze potential if production concerns intensify yet limited fuel for explosive moves versus February-March rally from extreme oversold

Implied volatility data unavailable for current wheat options contracts with thin agricultural derivatives markets limiting directional signal clarity, yet historical WASDE-driven volatility events typically produce 30-50% expansion over 1-2 weeks suggesting current elevated volatility around 70th percentile consistent with post-binary-event positioning phase

TRANSITIONAL macro regime with VIX 17.26 neutral, USD weakness to 97.7 DXY (lowest since February 2026, down 2.42% YoY) following Powell-to-Warsh Fed Chair transition with dovish tilt supporting U.S. agricultural export competitiveness, crude oil retreating from geopolitical spike highs to sub-$95/bbl reducing input costs (diesel, fertilizer) creating supportive margin backdrop for wheat production economics

Slightly inverted - short-term volatility 29% elevated versus medium-term 27% following May 12 WASDE binary event and subsequent consolidation from 688.25 highs to current 647 with term structure suggesting elevated two-way risk persists in post-catalyst repricing phase yet expansion appears mature barring fresh weather catalyst before June 10 WASDE

Volatility elevated in high regime at 70th percentile following May 12 WASDE binary event with potential for 10-15% compression if market enters sustained directional trend without fresh catalyst or modest expansion if late-May/June drought concerns intensify from ongoing weather stress—historical WASDE-driven volatility typically normalizes 2-3 weeks post-event suggesting compression bias into early June absent fresh catalyst with peak volatility likely achieved unless drought deterioration materializes before June 10 WASDE

|

⚠️ Primary Risk

June 10 WASDE confirms May 12 production forecasts as floor with no further deterioration from drought conditions or reveals timely late-May rainfall salvaged some yield potential sending market back toward 610-620 support as global stocks at 951.5 million tonnes (34.52% stocks-to-use ratio) reassert structural oversupply narrative dominance over U.S. regional supply tightening, combined with entering seasonally weak June-August harvest pressure period for Northern Hemisphere wheat typically producing 5-10% price declines absent severe weather disruptions Probability: MEDIUM

|

✦ Primary Opportunity

Continued Plains drought intensification through late May-June combined with June 10 WASDE confirming additional production downgrades beyond May 12 estimates triggers rally toward 670-688 range retest as 69% drought coverage with only 28% good-to-excellent ratings materializes sustained yield losses exceeding current market pricing, while net short positioning at -53,852 contracts provides modest fuel for short-covering acceleration if supply concerns deepen Timeframe: Next 2-3 weeks through June 10 WASDE and critical late-May/early-June weather window for final 2026 winter wheat crop development before harvest begins in Southern Plains

|

ZW wheat futures trade at 647 cents per bushel on May 24, 2026, consolidating after a powerful 32% rally from October 2025 capitulation lows at 492.25 driven by the most severe U.S. wheat production shortfall since 1972. Post-input news scan confirms no material developments since discipline agent inputs were generated, with current price holding in 635-660 range following last week's CORRECT BULLISH call at conviction 7 that captured a +1.77% weekly move. Current macro regime classification: TRANSITIONAL with VIX at 17.26 (neutral zone below 20 threshold) indicating balanced equity market psychology, USD weakness to 97.7 DXY (lowest since February 2026) following the May 15 Powell-to-Warsh Fed Chair transition providing structural tailwind for U.S. agricultural export competitiveness, and crude oil retreating from geopolitical $111 spike to sub-$95 levels easing input cost pressures.

For agricultural commodities, this macro backdrop is supportive yet secondary to commodity-specific supply fundamentals that dominate wheat's directional dynamics. The defining catalyst remains the May 12 WASDE report (released 12 days ago) that revealed U.S. all-wheat production at 1,561 million bushels—the lowest level since 1972 and down 21.3% year-over-year—with all-wheat yield at 47.5 bushels per acre (5.8 bushels below 2025 record). The Fundamental agent notes drought in key producing states contributed to large yield drops with Hard Red Winter particularly impacted, showing winter wheat production down 25% from last year to 1,048 billion bushels.

Current crop conditions as of May 19 (5 days ago per USDA WWCB) show only 28% good-to-excellent versus 46% last year, with 69% of U.S. winter wheat areas in drought per May 8 Agriculture in Drought report. Current price at 647 sits 6% below the May 12 post-WASDE spike high at 688.25 yet remains 32% above October lows, suggesting the market has priced substantial weather premium without committing to full catastrophe scenario given global stocks remain at record 951.5 million tonnes (34.52% stocks-to-use ratio).

The discipline signals reveal strong fundamental-institutional divergence creating analytical tension: Fundamental shows strong bullish +3.5 on May 12 WASDE production downgrades, Technical shows bullish +1.5 on uptrend establishment, Sentiment shows mild bullish +0.5, yet Institutional shows contrarian +1.5 (net short positioning despite bullish fundamentals creating squeeze risk), Economic shows bearish -0.5 on mixed USD/oil dynamics, and Options provides no signal due to thin markets. Using Agricultural category weights (Fundamental 0.35, Institutional 0.20, Economic 0.15, Technical 0.15, Sentiment 0.10, Options 0.05): (0.35 × 3.5) + (0.20 × 1.5) + (0.15 × -0.5) + (0.15 × 1.5) + (0.10 × 0.5) + (0.05 × 0.0) = 1.225 + 0.30 - 0.075 + 0.225 + 0.05 + 0.0 = +1.725, rounds to +1.5 signal after discipline conflict adjustment.

Positioning dynamics show managed money at net short -53,852 contracts as of May 5, representing a dramatic shift from marginal net long +0.9K in prior period to decisive bearish stance, yet absolute positioning remains mid-range (45th-55th percentile) after 84% of extreme shorts from peak -109,483 contracts were covered, removing the asymmetric squeeze fuel that drove February-March rallies yet creating balanced two-way risk with modest short-covering potential if June 10 WASDE confirms additional production downgrades. Critical seasonal context: Wheat is entering the historically weak June-August period when Northern Hemisphere harvest pressure typically produces 5-10% price declines, yet CME seasonal research shows wheat markets have tendency to decline between spring and July harvest then begin rising from harvest lows into fall and winter, creating tension where 2026 unique drought conditions with 69% winter wheat areas affected and USDA projecting season-average price at $6.50/bushel (up $1.50 YoY per May 14 ERS outlook) may override typical seasonal patterns as occurred in February-March when Arctic blast catalyst finally broke six months of bearish stranglehold.

The June 10 WASDE (17 days away) emerges as critical binary catalyst that will provide updated winter wheat production estimates incorporating final spring weather conditions and harvest progress data, determining whether May 12 production downgrades represent floor or further deterioration warranted given persistent drought affecting 69% of production areas. Applying Section 7 Conviction Calculation Sequence: (1) Probable weekly move assessment: given May 12 WASDE catalyst now 12 days aged with market digested, no immediate fresh catalyst before June 10 (17 days away), consolidation in 635-660 range, probable move appears 1.0-2.0% range moderately exceeding 0.75% noise threshold justifying directional call; (2) Net signal +1.5 exceeds 1.0 Min Signal threshold permitting directional bias; (3) Rule 3 penalties: last call CORRECT (no miss penalty), 2+ disciplines in conflict (Economic bearish vs Fundamental/Technical/Institutional/Sentiment bullish) -1, macro regime TRANSITIONAL yet BULLISH bias aligns with USD weakness component so no penalty = -1 total; (4) Rule 4 Thesis Health Score: continuing BULLISH bias from last week (consecutive streak = 2 weeks, below 5-week review threshold), of last 4 graded weeks 0 moved contrary to bullish bias (last week +1.77% correct), no penalty; (5) May 12 WASDE major catalyst occurred this week (12 days ago, catalyst window extending to 2 weeks) so Max Conf (catalyst) = 8 applies; (6) Initial assessment 8 for clear fundamental catalyst with strong bullish production data minus -1 Rule 3 conflict penalty = 7 final.

Current bias streak: 2 consecutive weeks BULLISH. Miss streak: 0 (last call CORRECT). Devil's advocate argues the 6% pullback from 688.25 highs combined with 69% drought coverage yet current 647 price reflecting substantial premium 32% above October lows suggests market has adequately priced May 12 WASDE production downgrades creating mean reversion risk toward 620-635 support as global stocks at 951.5 million tonnes provide structural buffer and seasonal June-August harvest pressure typically overwhelms supply concerns, yet the counter-argument is 69% drought persistence with only 28% good-to-excellent ratings (versus 46% last year) and Farm Progress May 22 report noting USDA projected winter wheat crop at 1.048 billion bushels (smallest since 1965) creates tail-risk scenario where late-May/June weather stress materializes additional yield losses triggering fresh rally toward 670-688 range as market underestimates sustained production impact from months-long drought stress that cannot be fully reversed by isolated rainfall events despite improved moisture forecasts.

Current conviction 7 reflects high-quality fundamental catalyst from May 12 WASDE (most severe production shortfall since 1972) combined with supportive macro backdrop (USD weakness, dovish Fed, declining oil) offset by technical consolidation after rally, institutional net short positioning creating two-way uncertainty, and seasonal headwinds entering June-August weak period, creating setup where BULLISH bias appropriate with strong conviction acknowledging balanced risk profile from global oversupply narrative and positioning no longer at extreme.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 22, 2026 | BULLISH | 7/10 | ✅ |

| May 15, 2026 | NO CALL | 5/10 | ➖ |

| May 8, 2026 | NO CALL | 5/10 | ➖ |

| May 1, 2026 | NO CALL | 5/10 | ➖ |

| April 24, 2026 | NO CALL | 5/10 | ➖ |

| April 17, 2026 | BEARISH | 5/10 | ❌ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | BEARISH | 5/10 | ❌ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | BULLISH | 8/10 | ❌ |

| March 6, 2026 | BULLISH | 8/10 | ✅ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Wheat (ZW) Report Date: May 24, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 7/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 0 (CONSENSUS ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING AFTER RALLY Regime: TRANSITIONAL MACRO ENVIRONMENT WITH VIX AT 17.26 (NEUTRAL ZONE BELOW 20 THRESHOLD) INDICATING BALANCED EQUITY MARKET PSYCHOLOGY, USD WEAKNESS TO 97.7 DXY SUPPORTING U.S. EXPORT COMPETITIVENESS, CRUDE OIL RETREATING FROM $111 HIGHS TO SUB-$95 LEVELS EASING INPUT COST PRESSURES, YET COMMODITY-SPECIFIC DROUGHT FUNDAMENTALS DOMINATE DIRECTIONAL DYNAMICS OVER BROAD RISK APPETITE SIGNALS CREATING BIFURCATED REGIME WHERE MACRO BACKDROP SUPPORTS YET AGRICULTURAL SUPPLY CONCERNS DRIVE Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Cautiously bullish on May 12 WASDE production downgrades confirming most severe U.S. wheat shortfall since 1972 with crop conditions at 28% good-to-excellent versus 46% last year, yet increasingly concerned about sustainability above 650 given 6% pullback from May 12 highs, global stocks at 951.5 million tonnes (34.52% stocks-to-use ratio), and approaching seasonal June-August harvest pressure period ── WHAT THE MARKET IS MISSING ─────────────────── Market may be underestimating duration and severity of production losses from 69% drought coverage affecting winter wheat areas with only 28% good-to-excellent crop ratings creating scenario where June 10 WASDE confirms sustained yield degradation beyond May 12 estimates as months-long drought stress compounds through final development stages despite improved late-May moisture forecasts, yet desk acknowledges global 34.52% stocks-to-use ratio and seasonal harvest pressure approaching create genuine two-way uncertainty requiring balanced conviction versus entrenched bullish stance—last week's CORRECT call validates production-driven thesis yet 32% rally from October lows reflects substantial premium already priced ── KEY DRIVERS ────────────────────────────────── 1. May 12 WASDE bullish production shock showing U.S. wheat output at 1,561 million bushels (lowest since 1972, down 21.3% YoY) with crop conditions at 28% good-to-excellent versus 46% last year and 69% of winter wheat areas in drought, yet current price at 647 already reflects substantial weather premium 32% above October lows suggesting much of the supply tightening is priced while global stocks remain at record 951.5 million tonnes 2. Institutional positioning shows net short -53,852 contracts as of May 5 representing continued bearish stance despite rally, with 84% of extreme shorts from prior months already covered removing asymmetric squeeze fuel yet still creating modest short-covering potential if June 10 WASDE confirms additional production downgrades from ongoing drought stress 3. Entering seasonally weak June-August period for Northern Hemisphere wheat as harvest pressure typically weighs on prices, yet 2026 unique drought conditions with 70% of winter wheat areas affected and USDA projecting season-average price at $6.50/bushel (up $1.50 YoY) creates tension where seasonal bearish patterns clash with severe supply-side fundamentals ── KEY ZONES ──────────────────────────────────── Resistance 2: 683.25 – 693.25 Resistance 1: 655.00 – 665.00 Pivot: ~647.00 Support 1: 630.00 – 640.00 Support 2: 605.00 – 615.00 ── DISCIPLINE BIASES ──────────────────────────── Technical: N/A Fundamental: N/A Institutional: N/A Options: N/A Economic: N/A Sentiment: N/A ── TECHNICAL STRUCTURE ────────────────────────── Price at 647 consolidating in 635-660 range after 1.77% weekly gain, trading 32% above October 492 capitulation lows yet 6% below May 12 intraday peak at 688.25 (52-week high), establishing position above key moving averages in emerging uptrend structure with RSI estimated 55-60 indicating bullish momentum without overbought extremes ── FUNDAMENTAL ASSESSMENT ─────────────────────── Profoundly bullish U.S. supply-side dynamics with May 12 WASDE confirming production at 1,561 million bushels (lowest since 1972, down 21.3% YoY) and crop conditions at 28% good-to-excellent versus 46% last year with 69% of winter wheat areas in drought per Agriculture in Drought report, yet global stocks remain structurally ample at 951.5 million tonnes creating fundamental tension where U.S. regional supply destruction meets global oversupply baseline requiring export flow monitoring to determine whether domestic tightness translates to sustained price premium ── INSTITUTIONAL POSITIONING ──────────────────── Managed money net short -53,852 contracts per May 5 COT data representing shift from marginal net long +0.9K in prior period to decisive short position, yet absolute positioning remains mid-range (45th-55th percentile) without extreme after 84% of peak shorts covered creating balanced two-way risk with modest squeeze potential if production concerns intensify yet limited fuel for explosive moves versus February-March rally from extreme oversold ── OPTIONS FLOW ───────────────────────────────── Implied volatility data unavailable for current wheat options contracts with thin agricultural derivatives markets limiting directional signal clarity, yet historical WASDE-driven volatility events typically produce 30-50% expansion over 1-2 weeks suggesting current elevated volatility around 70th percentile consistent with post-binary-event positioning phase ── ECONOMIC BACKDROP ──────────────────────────── TRANSITIONAL macro regime with VIX 17.26 neutral, USD weakness to 97.7 DXY (lowest since February 2026, down 2.42% YoY) following Powell-to-Warsh Fed Chair transition with dovish tilt supporting U.S. agricultural export competitiveness, crude oil retreating from geopolitical spike highs to sub-$95/bbl reducing input costs (diesel, fertilizer) creating supportive margin backdrop for wheat production economics ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 70th Trend: Stable — Days in Regime: 18 Term Structure: slightly inverted - short-term volatility 29% elevated versus medium-term 27% following May 12 WASDE binary event and subsequent consolidation from 688.25 highs to current 647 with term structure suggesting elevated two-way risk persists in post-catalyst repricing phase yet expansion appears mature barring fresh weather catalyst before June 10 WASDE Historical Pattern: Outlook: Volatility elevated in high regime at 70th percentile following May 12 WASDE binary event with potential for 10-15% compression if market enters sustained directional trend without fresh catalyst or modest expansion if late-May/June drought concerns intensify from ongoing weather stress—historical WASDE-driven volatility typically normalizes 2-3 weeks post-event suggesting compression bias into early June absent fresh catalyst with peak volatility likely achieved unless drought deterioration materializes before June 10 WASDE Trading Context: Vol Risk/Opportunity: ── PRIMARY RISK ───────────────────────────────── June 10 WASDE confirms May 12 production forecasts as floor with no further deterioration from drought conditions or reveals timely late-May rainfall salvaged some yield potential sending market back toward 610-620 support as global stocks at 951.5 million tonnes (34.52% stocks-to-use ratio) reassert structural oversupply narrative dominance over U.S. regional supply tightening, combined with entering seasonally weak June-August harvest pressure period for Northern Hemisphere wheat typically producing 5-10% price declines absent severe weather disruptions Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Continued Plains drought intensification through late May-June combined with June 10 WASDE confirming additional production downgrades beyond May 12 estimates triggers rally toward 670-688 range retest as 69% drought coverage with only 28% good-to-excellent ratings materializes sustained yield losses exceeding current market pricing, while net short positioning at -53,852 contracts provides modest fuel for short-covering acceleration if supply concerns deepen Timeframe: Next 2-3 weeks through June 10 WASDE and critical late-May/early-June weather window for final 2026 winter wheat crop development before harvest begins in Southern Plains ── NEXT CATALYST ──────────────────────────────── Date: June 10, 2026 Event: USDA June 2026 WASDE Report with updated winter wheat production estimates incorporating final spring weather conditions, harvest progress data from Southern Plains drought-affected areas, and initial 2026/27 crop year demand projections determining whether May 12 production downgrades represent floor or further deterioration warranted Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ZW wheat futures trade at 647 cents per bushel on May 24, 2026, consolidating after a powerful 32% rally from October 2025 capitulation lows at 492.25 driven by the most severe U.S. wheat production shortfall since 1972. Post-input news scan confirms no material developments since discipline agent inputs were generated, with current price holding in 635-660 range following last week's CORRECT BULLISH call at conviction 7 that captured a +1.77% weekly move. Current macro regime classification: TRANSITIONAL with VIX at 17.26 (neutral zone below 20 threshold) indicating balanced equity market psychology, USD weakness to 97.7 DXY (lowest since February 2026) following the May 15 Powell-to-Warsh Fed Chair transition providing structural tailwind for U.S. agricultural export competitiveness, and crude oil retreating from geopolitical $111 spike to sub-$95 levels easing input cost pressures. For agricultural commodities, this macro backdrop is supportive yet secondary to commodity-specific supply fundamentals that dominate wheat's directional dynamics. The defining catalyst remains the May 12 WASDE report (released 12 days ago) that revealed U.S. all-wheat production at 1,561 million bushels—the lowest level since 1972 and down 21.3% year-over-year—with all-wheat yield at 47.5 bushels per acre (5.8 bushels below 2025 record). The Fundamental agent notes drought in key producing states contributed to large yield drops with Hard Red Winter particularly impacted, showing winter wheat production down 25% from last year to 1,048 billion bushels. Current crop conditions as of May 19 (5 days ago per USDA WWCB) show only 28% good-to-excellent versus 46% last year, with 69% of U.S. winter wheat areas in drought per May 8 Agriculture in Drought report. Current price at 647 sits 6% below the May 12 post-WASDE spike high at 688.25 yet remains 32% above October lows, suggesting the market has priced substantial weather premium without committing to full catastrophe scenario given global stocks remain at record 951.5 million tonnes (34.52% stocks-to-use ratio). The discipline signals reveal strong fundamental-institutional divergence creating analytical tension: Fundamental shows strong bullish +3.5 on May 12 WASDE production downgrades, Technical shows bullish +1.5 on uptrend establishment, Sentiment shows mild bullish +0.5, yet Institutional shows contrarian +1.5 (net short positioning despite bullish fundamentals creating squeeze risk), Economic shows bearish -0.5 on mixed USD/oil dynamics, and Options provides no signal due to thin markets. Using Agricultural category weights (Fundamental 0.35, Institutional 0.20, Economic 0.15, Technical 0.15, Sentiment 0.10, Options 0.05): (0.35 × 3.5) + (0.20 × 1.5) + (0.15 × -0.5) + (0.15 × 1.5) + (0.10 × 0.5) + (0.05 × 0.0) = 1.225 + 0.30 - 0.075 + 0.225 + 0.05 + 0.0 = +1.725, rounds to +1.5 signal after discipline conflict adjustment. Positioning dynamics show managed money at net short -53,852 contracts as of May 5, representing a dramatic shift from marginal net long +0.9K in prior period to decisive bearish stance, yet absolute positioning remains mid-range (45th-55th percentile) after 84% of extreme shorts from peak -109,483 contracts were covered, removing the asymmetric squeeze fuel that drove February-March rallies yet creating balanced two-way risk with modest short-covering potential if June 10 WASDE confirms additional production downgrades. Critical seasonal context: Wheat is entering the historically weak June-August period when Northern Hemisphere harvest pressure typically produces 5-10% price declines, yet CME seasonal research shows wheat markets have tendency to decline between spring and July harvest then begin rising from harvest lows into fall and winter, creating tension where 2026 unique drought conditions with 69% winter wheat areas affected and USDA projecting season-average price at $6.50/bushel (up $1.50 YoY per May 14 ERS outlook) may override typical seasonal patterns as occurred in February-March when Arctic blast catalyst finally broke six months of bearish stranglehold. The June 10 WASDE (17 days away) emerges as critical binary catalyst that will provide updated winter wheat production estimates incorporating final spring weather conditions and harvest progress data, determining whether May 12 production downgrades represent floor or further deterioration warranted given persistent drought affecting 69% of production areas. Applying Section 7 Conviction Calculation Sequence: (1) Probable weekly move assessment: given May 12 WASDE catalyst now 12 days aged with market digested, no immediate fresh catalyst before June 10 (17 days away), consolidation in 635-660 range, probable move appears 1.0-2.0% range moderately exceeding 0.75% noise threshold justifying directional call; (2) Net signal +1.5 exceeds 1.0 Min Signal threshold permitting directional bias; (3) Rule 3 penalties: last call CORRECT (no miss penalty), 2+ disciplines in conflict (Economic bearish vs Fundamental/Technical/Institutional/Sentiment bullish) -1, macro regime TRANSITIONAL yet BULLISH bias aligns with USD weakness component so no penalty = -1 total; (4) Rule 4 Thesis Health Score: continuing BULLISH bias from last week (consecutive streak = 2 weeks, below 5-week review threshold), of last 4 graded weeks 0 moved contrary to bullish bias (last week +1.77% correct), no penalty; (5) May 12 WASDE major catalyst occurred this week (12 days ago, catalyst window extending to 2 weeks) so Max Conf (catalyst) = 8 applies; (6) Initial assessment 8 for clear fundamental catalyst with strong bullish production data minus -1 Rule 3 conflict penalty = 7 final. Current bias streak: 2 consecutive weeks BULLISH. Miss streak: 0 (last call CORRECT). Devil's advocate argues the 6% pullback from 688.25 highs combined with 69% drought coverage yet current 647 price reflecting substantial premium 32% above October lows suggests market has adequately priced May 12 WASDE production downgrades creating mean reversion risk toward 620-635 support as global stocks at 951.5 million tonnes provide structural buffer and seasonal June-August harvest pressure typically overwhelms supply concerns, yet the counter-argument is 69% drought persistence with only 28% good-to-excellent ratings (versus 46% last year) and Farm Progress May 22 report noting USDA projected winter wheat crop at 1.048 billion bushels (smallest since 1965) creates tail-risk scenario where late-May/June weather stress materializes additional yield losses triggering fresh rally toward 670-688 range as market underestimates sustained production impact from months-long drought stress that cannot be fully reversed by isolated rainfall events despite improved moisture forecasts. Current conviction 7 reflects high-quality fundamental catalyst from May 12 WASDE (most severe production shortfall since 1972) combined with supportive macro backdrop (USD weakness, dovish Fed, declining oil) offset by technical consolidation after rally, institutional net short positioning creating two-way uncertainty, and seasonal headwinds entering June-August weak period, creating setup where BULLISH bias appropriate with strong conviction acknowledging balanced risk profile from global oversupply narrative and positioning no longer at extreme.