Mon-T Weekly Review — w/e 5 Jun 2026

Two from five, a semiconductor crash wipes out the equity thesis, and silver quietly posts the call of the month while nobody was watching.

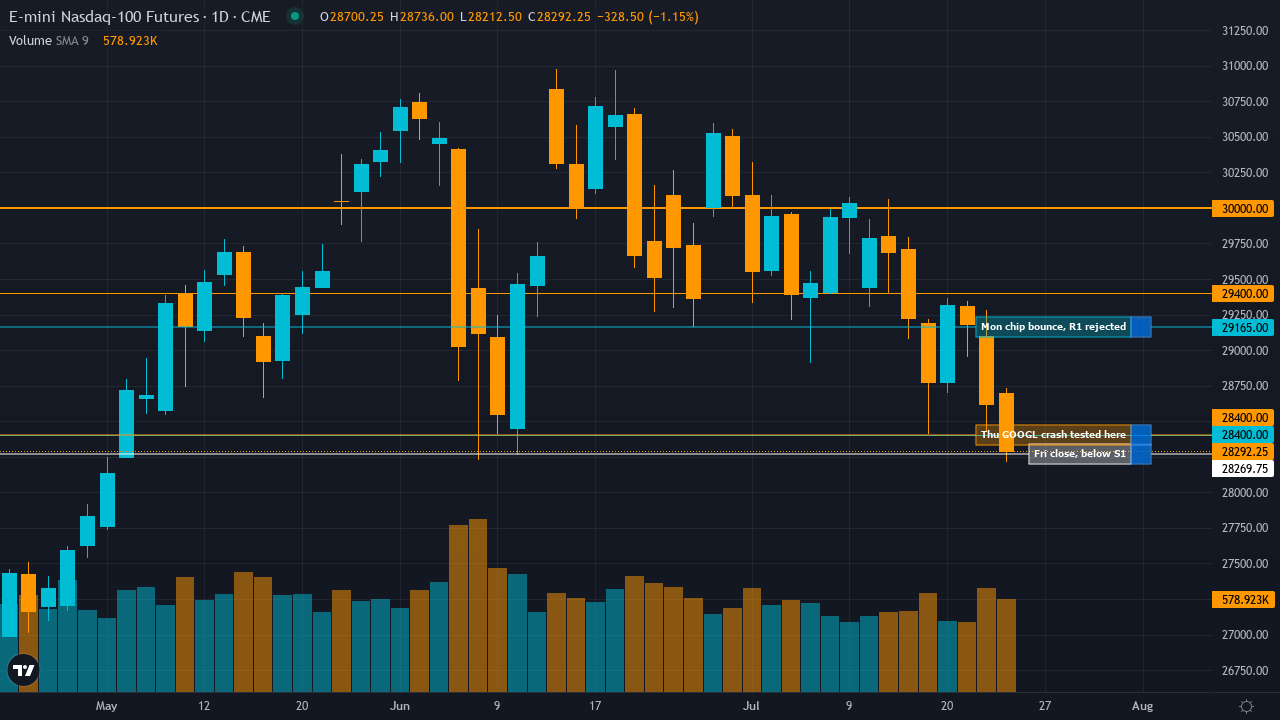

Something broke this week, and it was not subtle. A semiconductor selloff that TheStreet described as wiping $1 trillion from markets cascaded through every asset class the desk tracks, dragging the S&P 500 down 2.91%, the Nasdaq down 4.95%, and copper, this week's Market of the Week, down 2.59% against a BULLISH call at the desk's highest conviction. Reuters reported that tech and chips tumbled more than 7.5% and 9.1% respectively over three days of relentless selling, with robust jobs data on Friday stoking fears of a hawkish Fed. The S&P snapped its nine-week run of Friday-to-Friday gains, its longest weekly winning streak in years.

The desk made five directional calls this week and got two right, a 40% hit rate that sits uncomfortably below the coin-flip threshold. Silver's BEARISH call at 6/10 delivered a stunning 11.05% decline, the single best individual market result since crude oil's 8.85% crash three weeks ago. Wheat's BEARISH call at 5/10 caught a 4.95% drop into seasonal harvest weakness. But the other three directional calls, copper BULLISH at 7/10, the S&P BULLISH at 6/10, and crude BEARISH at 5/10, all went the wrong way. Ten markets received the NO CALL treatment, and the carnage among those abstentions was extraordinary: platinum fell 7.95%, soybeans dropped 5.44%, the Nasdaq shed 4.95%, gold crashed 5.53%, and the Russell lost 2.97%. Every single one scored as a miss.

I said last week that the question for subscribers was whether watching gold drop three percent while the desk shrugs is discipline or abdication. This week, gold dropped five and a half percent. Platinum fell nearly eight. Soybeans shed five and a half. And the desk said nothing about any of it. The system's caution has become its own kind of exposure.

|

15

Markets

|

5

Directional

|

2

Correct

|

40%

Accuracy

|

10

No Calls

|

Five directional calls this week, with two landing on the right side. The other ten markets got the NO CALL treatment. A 40% directional accuracy rate is the worst since that nightmarish 12.5% week in late April, and while the sample size of five calls means the percentage swings wildly on a single miss, the pattern is uncomfortable. The average confidence of 5.8 across those five calls tells you the desk was not exactly thumping the table, which is appropriate caution given the miss streaks that triggered mandatory resets across most of the board.

The real damage, though, lies in those ten abstentions. Eight of them produced moves exceeding 1%, with platinum's 7.95% crash, soybeans' 5.44% plunge, the Nasdaq's 4.95% selloff, and gold's 5.53% collapse leading the parade of missed opportunities. When you abstain from ten markets and eight of them move violently, the framework is not protecting you from being wrong. It is protecting you from being anything at all.

|

53/92

Correct / Total

|

57.6%

Accuracy

|

92 / 103

Directional / No Call

|

The rolling twelve-week figure sits at 57.6% across 92 directional calls, with 103 no-call abstentions. That engagement split tells you the desk calls direction on fewer than half of all market-weeks, a rate that has fallen steadily since February's 70%+ pace when the precious metals thesis was printing money. The 57-58% range has become permanent residency for this number. This week's 40% on five calls does nothing to help, and the mountain of NO CALLs means the denominator barely moves from week to week. The desk needs to increase its directional volume while maintaining accuracy above 60% to break this ceiling. At the current pace, it will be living at 57% until the autumn.

|

Bias Called

BULLISH

|

Confidence

7/10

|

Result

MISSED

|

Grade

D

|

| Monday Open | 6.42 |

| Friday Close | 6.2535 |

| Move | -2.59 |

| ▼ R2 | 6.72 |

| ▼ R1 | 6.50 |

| ▲ S1 | 6.28 |

| ▲ S2 | 6.00 |

S1 at $6.28 was the level that mattered, and it was breached. Copper opened Monday at $6.42, held up through the early part of the week as the ISM Manufacturing data the desk was banking on arrived. Then the semiconductor crash hit on Wednesday and Thursday, dragging industrial metals into the broader risk-off vortex. Trading Economics confirmed copper fell to $6.42 on June 5, down 1.47% from the prior session alone. Friday's close at $6.2535 settled below S1 at $6.28, meaning the desk's first line of defence gave way under the pressure. R1 at $6.50 was never seriously challenged. The desk mapped the support accurately at S1 but called the wrong direction, which means the levels framework did its job even while the thesis failed.

The called edge centred on the market reading LME headline inventory at 393,400 tonnes as abundant while available inventory excluding warrants was critically tight at just 89,725 tonnes. The desk argued this discrepancy, combined with Grasberg offline through Q2 and China's sulfuric acid export ban affecting 15% of global production, created an underpriced supply deficit that the June 3 ISM Manufacturing PMI would validate. The ISM data arrived, confirming the S&P Global 55.3 preliminary reading, but the broader market regime overwhelmed the commodity-specific thesis entirely. When a semiconductor crash wipes $1 trillion from equity markets and the Fed repricing accelerates, the difference between headline and available copper inventory stops mattering. The edge identification was technically sound and practically irrelevant.

Five of six disciplines pointed BULLISH, with only Options providing no signal. The Fundamental agent at 30% weight drove the supply deficit thesis through Grasberg and sulfuric acid export ban analysis. The Economic agent at 25% weight flagged the US Manufacturing PMI surge to 55.3 as the demand validation catalyst. The Institutional agent at 20% weight read managed money net-long at 71,974 contracts as trend-following rather than crowded. The Technical agent at 15% confirmed the uptrend above moving averages. When five disciplines agree and the market drops 2.59%, the problem is not individual agent failure but collective blindness to the macro regime shift. The Kashkari hawkish comments on May 29, which the NQ synthesis flagged as material, were the canary in the coal mine that the copper agents failed to hear. The Economic agent on copper was cheerfully citing PMI strength while the Economic agent on NQ was warning about eliminated rate cuts. Same desk, opposite conclusions, same week.

Copper was selected as Market of the Week for its rare five-of-six discipline unanimity, the highest conviction of any directional call at 7/10, and a razor-sharp edge thesis about the divergence between headline and available LME inventory. On paper, it was the strongest analytical setup on the board. In practice, it ran headlong into a semiconductor-driven market crash that rendered every commodity-specific insight irrelevant.

The week opened promisingly enough. Copper at $6.42 sat near its 52-week highs, the ISM Manufacturing catalyst that the MOTW report identified as the key confirmation was just 48 hours away, and the desk's thesis about Grasberg supply disruption and June-July seasonal restocking had been quietly accumulating correct calls in recent weeks. The free MOTW report, published on the Ghost site Sunday evening, laid out the full case with specific levels and the observation that available LME inventory at 89,725 tonnes was critically tight despite headline stocks appearing comfortable at 393,400 tonnes.

Then reality intervened. The semiconductor selloff that began Wednesday accelerated through Thursday and Friday, with Reuters reporting tech and chips tumbling more than 7.5% and 9.1% respectively over three sessions. Bloomberg noted the S&P 500 fell 2.4% on Thursday alone as growing anxiety about AI valuations combined with the repricing of the Fed outlook. Copper, with its 50% industrial exposure and sensitivity to growth expectations, was dragged into the downdraft. Friday's close at $6.2535 represented a 2.59% decline that breached S1 at $6.28 and left the desk's bullish thesis looking like it belonged to a different week.

The grade is D rather than F because the move, while painful, was modest relative to the carnage elsewhere, the levels framework correctly identified $6.28 as the first support, and the confidence at 7/10 reflected genuine analytical work rather than a guess. But a 7/10 conviction call that misses by 2.59% in the wrong direction, on a week where the desk's own NQ analysis warned about a hawkish Fed repricing that would affect duration-sensitive assets, is a process failure. The copper agents did not talk to the equity agents, and the thesis paid the price.

For subscribers who read the free MOTW report before Monday's open, the S1 at $6.28 provided a clear stop-loss reference that would have limited damage. That is the levels framework doing its job even when the directional call fails. The full report is on the Ghost site. Read it for the analytical framework, and then read the result as a reminder that supply deficits stop mattering when the macro floor falls out.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 6/10 | 7595.75 | 7375 | -2.91 | MISSED | D |

| BULLISH at 6/10 and the S&P crashed 2.91%, snapping its nine-week winning streak. Reuters confirmed the index was poised for its worst week in months as a semiconductor selloff wiped $1 trillion from markets. The desk's five consecutive correct BULLISH calls on ES, which I praised each week through May, ended with a thud. The put/call complacency at 0.39 that the Sentiment agent flagged for weeks finally bit. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 30405.25 | 28901 | -4.95 | — | — |

| NO CALL at 6/10 on a 4.95% crash. TheStreet reported the Nasdaq fell 4% on Friday alone as the semiconductor slide accelerated. The desk had a mild bullish lean with signal 0.8, just below the 1.0 threshold, and the market responded by dropping nearly five percent. I have now called out the desk's NQ abstention habit roughly a dozen times this year. This week, for once, sitting out was less painful than being BULLISH would have been. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | 87.36 | 90.36 | 3.43 | MISSED | D |

| BEARISH at minimum conviction and crude rallied 3.43%. The desk's structural oversupply and ceasefire normalization thesis met a week where oil was apparently the only asset anyone wanted to own as equities collapsed. Two consecutive BEARISH wins had lulled the desk into complacency. The war premium refuses to die completely. | |||||||

|

Gold

CORE

|

NO CALL | — | 4593 | 4338.9 | -5.53 | — | — |

| NO CALL at 5/10 per mandatory miss reset after five consecutive misses, and gold crashed 5.53% to $4,339. The metal that the desk once championed at 8/10 conviction back in February continues its descent from January's $5,626 peak. A 5.53% decline while the desk sits on its hands is excruciating, but the miss reset protocol exists for exactly this reason. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1652 | 1.1524 | -1.1 | — | — |

| NO CALL for the fourteenth consecutive week, and the euro dropped 1.10%. That is the largest EUR/USD move in months, and the desk was nowhere near it. The fourteen-week abstention streak is now old enough to attend secondary school. The ECB meets June 11. Something has to give. | |||||||

|

Silver

EXTENDED

|

BEARISH | 6/10 | 76.2 | 67.78 | -11.05 | CORRECT | A+ |

| BEARISH at 6/10 and silver collapsed 11.05%, the largest single-week decline since the March FOMC flash crash. The desk's identification of extreme 90% retail long positioning and elevated real yields as structural headwinds proved devastatingly correct as the semiconductor crash triggered cross-asset precious metals liquidation. Three consecutive correct BEARISH calls. The best call on the board by a wide margin. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.006312 | 0.006245 | -1.05 | — | — |

| NO CALL for the fourteenth consecutive week, the yen strengthened 1.05% as the dollar weakened against the safe-haven currency during the equity rout. A meaningful FX move the desk missed. The BoJ on June 15-16 looms as the catalyst that might finally break this streak. | |||||||

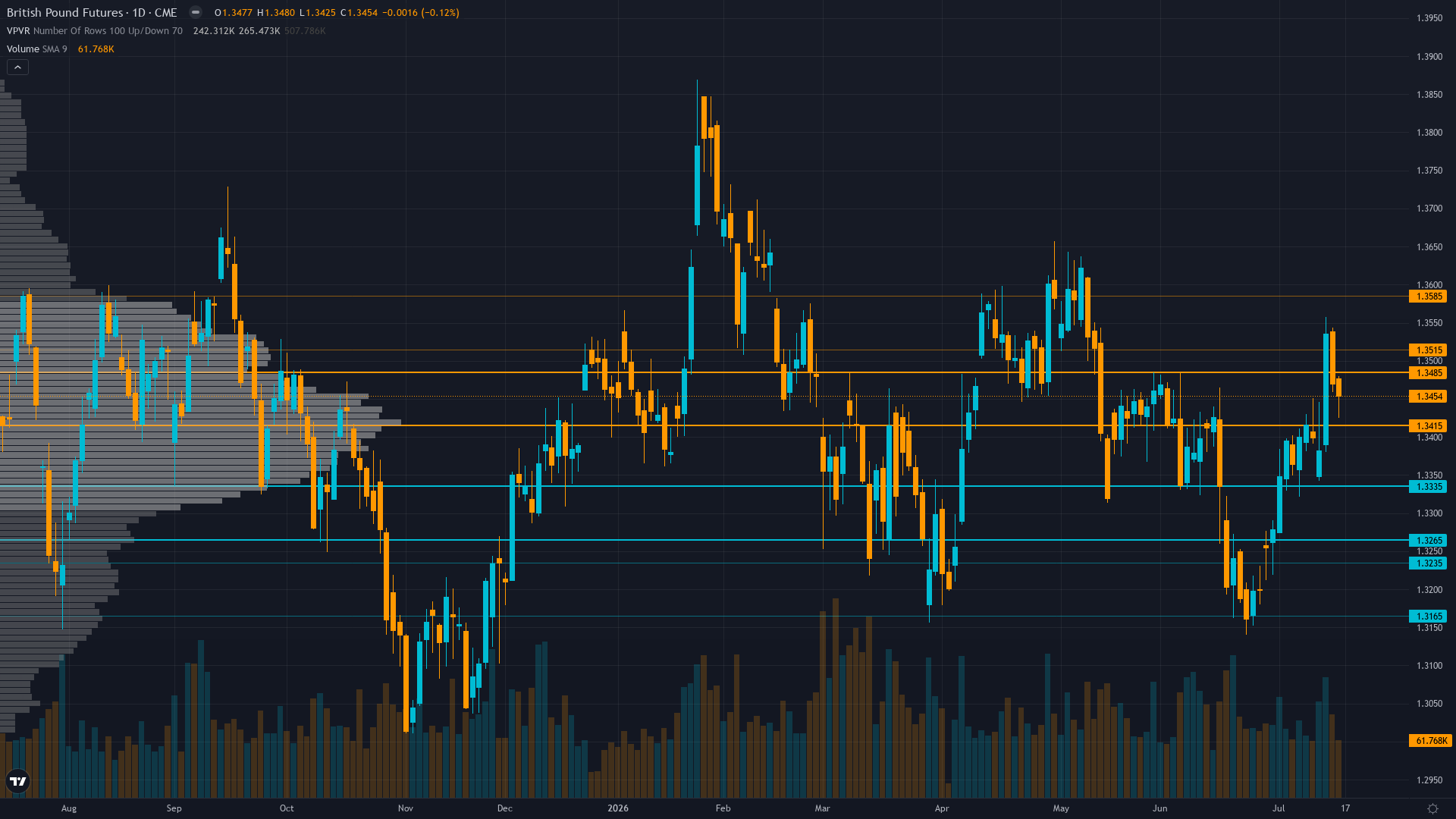

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.3438 | 1.3333 | -0.78 | — | — |

| NO CALL for the twelfth consecutive week, sterling fell 0.78%. The desk's cable hibernation continues as the June 18 BoE meeting approaches. At some point, the agents need to form a view on this pair, or we formally reclassify it as decorative. | |||||||

|

Copper

EXTENDED

|

BULLISH | 7/10 | 6.42 | 6.2535 | -2.59 | MISSED | D |

| This week's MOTW. BULLISH at 7/10, the desk's highest conviction call, and copper fell 2.59% as the semiconductor crash dragged industrial metals into the risk-off vortex. The Grasberg supply deficit thesis met a macro regime shift it could not survive. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

Russell 2000

EXTENDED

|

NO CALL | — | 2905.3 | 2818.9 | -2.97 | — | — |

| NO CALL per mandatory miss reset after four consecutive misses, and the Russell dropped 2.97%. The small-cap index that delivered the desk's best active streak of the year, four consecutive BULLISH wins totalling 14.4% back in April, has now become another market the desk cannot touch. The mandatory reset protocol saved it from being wrong, which in a week like this counts as a small mercy. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | 0.7187 | 0.7039 | -2.07 | — | — |

| NO CALL at 5/10 and the Aussie crashed 2.07%, its worst weekly decline since the March war selloff. The RBA meets June 3-4, which falls within this grading window, and the result was evidently not kind to the currency. The desk's policy divergence thesis, once its most reliable FX view, has been gathering dust for weeks. | |||||||

|

30Y Treasury

FULL DESK

|

NO CALL | — | 110.875 | 111.625 | 0.68 | — | — |

| NO CALL at 5/10 and bonds rallied 0.68% as the equity selloff drove a flight to duration. A modest move within the noise threshold, and the desk's caution ahead of the June 10 CPI was vindicated. One of only three correct outcomes on the entire board this week, and it was an abstention. | |||||||

|

Wheat

FULL DESK

|

BEARISH | 5/10 | 610.5 | 580.25 | -4.95 | CORRECT | B+ |

| BEARISH at 5/10 and wheat dropped 4.95%. After last week's spectacular F-grade BULLISH miss at 7/10 where wheat fell 5.68%, the desk flipped bearish at minimum conviction and caught the continuation. The seasonal June-August harvest pressure thesis and technical breakdown below 620 support played out cleanly. The desk's wheat record remains erratic, but at least this week it was erratic in the right direction. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | — | 1186.75 | 1122.25 | -5.44 | — | — |

| NO CALL at 5/10 on a 5.44% collapse. Soybeans cratered through the week in what looks like a broad agricultural liquidation event. The desk's signal at +0.5, well below the 1.0 minimum threshold, kept it on the sidelines while the renewable diesel structural floor apparently sprang a leak. A 5.44% move on a NO CALL is one of the larger misses of the year. | |||||||

|

Platinum

FULL DESK

|

NO CALL | — | 1926.5 | 1773.4 | -7.95 | — | — |

| NO CALL per mandatory reset after four consecutive misses, and platinum plunged 7.95%. The metal is now down 39% from its January $2,925 peak. The WPIC deficit thesis, which has been the Fundamental agent's favourite bedtime story for months, offered no protection whatsoever as precious metals suffered another cross-asset liquidation event. The mandatory neutral stance saved the desk from a fifth consecutive miss, which is the system working as designed, even if the outcome is profoundly unsatisfying. | |||||||

|

✦ Best Call: Silver (SI)

BEARISH at 6/10 and silver collapsed 11.05% from $76.20 to $67.78, a move so large it makes the modest 0.43% decline I reviewed last week look like a typing error. The desk identified extreme retail positioning at 90% long and elevated real yields as structural headwinds, and both catalysts detonated simultaneously when the semiconductor crash triggered a cross-asset liquidation event. Silver's beta to precious metals stress has been the desk's most reliable pattern of 2026, and this week it delivered the single largest correct directional call since crude oil's 8.85% crash in late May. Three consecutive correct BEARISH calls on silver now. The desk has found its groove on this metal, even as every other market on the board fell apart. |

⚠️ Worst Call: Copper (HG)

BULLISH at 7/10, the desk's highest conviction call on the entire board, and copper fell 2.59%. The MOTW deep-dive is above. What makes this particularly painful is that it was the week's showcase analysis, selected precisely because of the rare five-of-six discipline unanimity and the specific edge thesis about headline versus available LME inventory. When your highest-conviction call is also your free marketing report and both go wrong, the damage is reputational as well as directional. The Grasberg supply thesis remains intact, but the desk's timing was undermined by a macro regime shift its own equity analysts had partially flagged. |

The Economic agent had a split week that reveals the desk's fundamental coordination problem. On silver and wheat, its identification of elevated real yields and hawkish Fed repricing correctly drove bearish calls that delivered 11% and 5% wins respectively. On copper, that same agent cited US Manufacturing PMI at 55.3 as a bullish demand catalyst, apparently unaware that its own equity-side assessment was warning about rate hike fears destroying risk appetite. When the same discipline reaches opposite conclusions on correlated markets in the same week, the synthesis framework has a communication failure.

The Fundamental agent continues its year-long pattern of being structurally correct and tactically wrong. Its supply-deficit work on copper, its structural deficit thesis on silver, and its WASDE production shortfall analysis on wheat are all supported by real data. But supply-side analysis consistently loses to macro regime shifts, as I have been writing since the first Iran war week in March. The Sentiment agent, for its part, had been flagging extreme equity put/call complacency at 0.39 for weeks. This was the week it was vindicated, and as usual, it carried insufficient weight to override the consensus.

June is now a gauntlet. The June 10 WASDE updates wheat production estimates following the worst US crop in 52 years. The ECB meets June 11, with markets pricing three rate hikes and the desk's fourteen-week EUR/USD NO CALL streak begging for resolution. The BoJ on June 15-16 could force a view on the yen for the first time in months. And then the main event: the June 16-17 FOMC, with markets repricing from zero cuts to possible hikes after this week's selloff. Gold at $4,339, silver at $67.78, and the S&P at 7,375 all face binary outcomes from that meeting. The desk will have its Sunday views. Given what just happened, I expect some significant recalibration. Whether that means more directional courage or an even deeper retreat into NO CALL hibernation is the question worth watching.