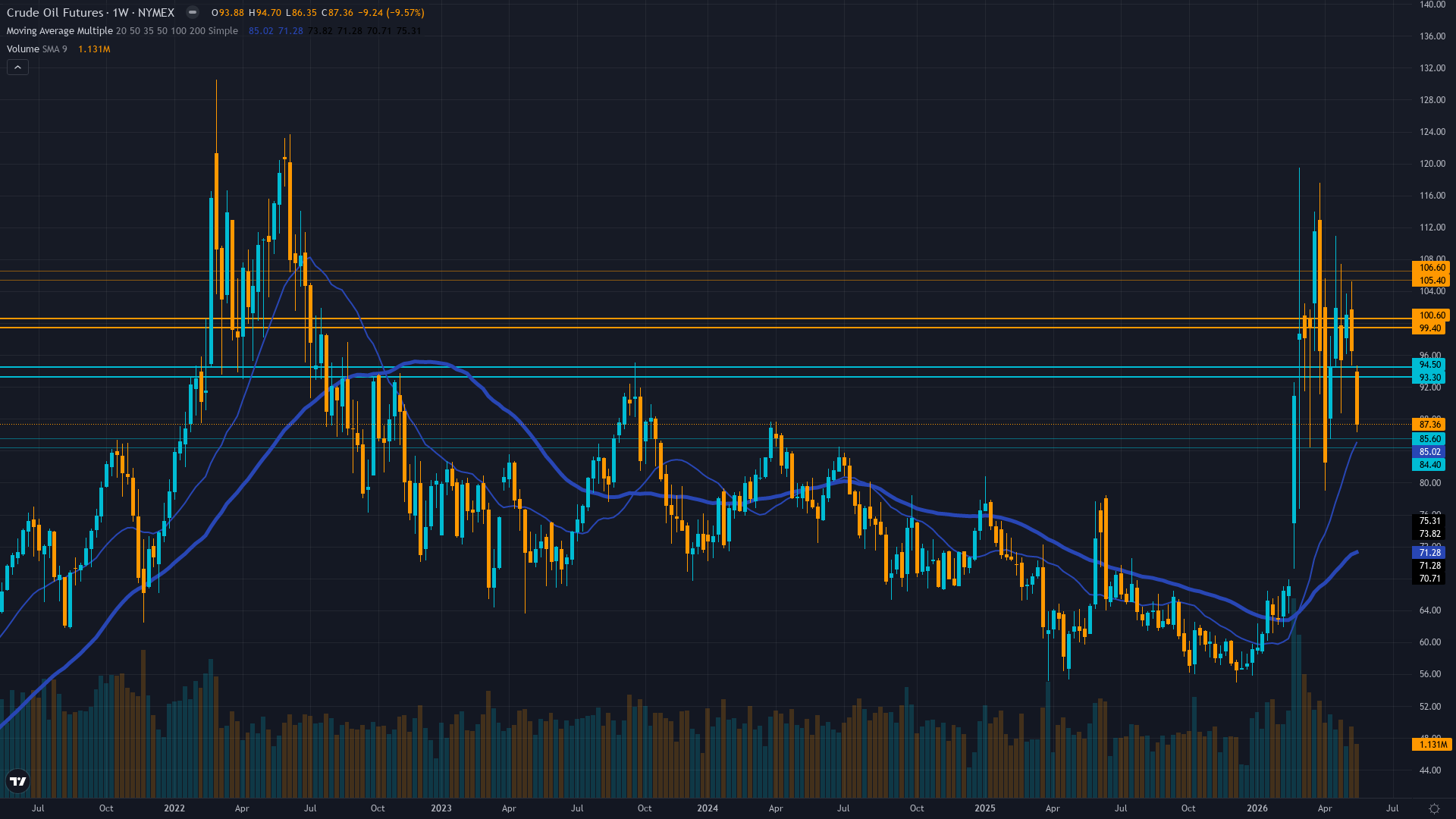

Crude Oil (CL) — Market may be underweighting U.S. blockade termination May 29 magnitude as…

Tactically uncertain with market split between ceasefire optimists expecting further mean reversion toward $82-85 and geopolitical hawks expecting stabilization at current $87-88 levels; structural oversupply consensus (EIA $88 Q4, IEA 2.5 mb/d surplus 2H26, demand destruction 420 kb/d) implies mode

Tactically uncertain with market split between ceasefire optimists expecting further mean reversion toward $82-85 and geopolitical hawks expecting stabilization at current $87-88 levels; structural oversupply consensus (EIA $88 Q4, IEA 2.5 mb/d surplus 2H26, demand destruction 420 kb/d) implies modest downside from current $87.36 but U.S. blockade termination May 29 removes acute catalyst creating low conviction environment

Ceasefire consolidation accelerating as U.S. blockade ended May 29 with Strait of Hormuz flows slowly resuming, triggering violent 17% May collapse from $105 peak to current $87.36 as geopolitical premium unwinds faster than discipline data anticipated, yet structural oversupply fundamentals (IEA 2.5 mb/d surplus 2H26, demand destruction 420 kb/d contraction) now reasserting dominance creating further downside toward EIA Q4 forecast $88 Brent-equivalent

Binary catalyst tension with OPEC+ June 7 meeting (7 days forward) creating event risk as cartel faces decision on production policy amid ongoing but declining Strait disruption - May 3 modest 188k bpd increase signals confidence in normalization trajectory yet failure to offset 10.5 mb/d shut-ins during crisis peak validates desk's bearish structural view

Demand destruction intensifying at critical velocity with IEA May 13 report showing global demand revised DOWN 720 kb/d in single month (from +640 kb/d growth to -80 kb/d contraction 2026) confirming high prices rationing demand more aggressively than supply disruptions persist, creating fundamental ceiling at current $87 levels

| ▼ Resistance Zone 2 | 99.250 – 100.750 |

| ▼ Resistance Zone 1 | 91.250 – 92.750 |

| ─ Pivot Area | ~87.360 |

| ▲ Support Zone 1 | 79.250 – 80.750 |

| ▲ Support Zone 2 | 74.250 – 75.750 |

WTI at $87.36 in confirmed downtrend after 17% May collapse, trading below 50-day MA with death cross forming (100 SMA below 200 SMA), RSI 48 neutral but momentum deteriorating as breakdown below $88-92 support zone confirms distribution phase complete

Crude overvalued 0-3% versus structural fair value $85-88 range; geopolitical premium nearly exhausted as U.S. blockade termination May 29 validates normalization trajectory while IEA demand destruction (420 kb/d contraction 2026) and EIA Q4 forecast $88 Brent imply current pricing near fundamental equilibrium but residual downside risk remains

Managed money net-long moderating from extremes with producer hedging at $100+ levels during crisis peak validating commercial bearish forward view; U.S. blockade termination May 29 represents policy-level commitment to price ceiling creating asymmetric downside as speculative length unwinds

Insufficient current data quality for directional signal; OVX crude volatility likely elevated in 80-95 range from March spike but moderating post-ceasefire as fear premium compresses

MACRO REGIME: TRANSITIONAL - VIX at 17.44 (May 21, below 20 calm threshold) indicating geopolitical risk contained to energy sector rather than systemic; Fed on hold at 3.50-3.75%, U.S. blockade termination May 29 represents material policy shift favoring price normalization as Strait flows resume late May/early June per EIA May 12 STEO projections

|

⚠️ Primary Risk

Ceasefire collapses before June 7 OPEC+ meeting with renewed U.S.-Iran military escalation or complete Strait of Hormuz reclosure forcing violent reversal back toward $100-110 range as 20% supply disruption risk premium reprices and invalidates mean reversion thesis based on normalization trajectory validated by U.S. blockade termination May 29 Probability: LOW

|

✦ Primary Opportunity

Ceasefire extends with full Strait of Hormuz normalization by early June as EIA May 12 STEO anticipates (flows resuming late May/early June following May 29 U.S. blockade termination), triggering complete geopolitical premium unwind toward EIA Q4 forecast $88 Brent-equivalent ($84-86 WTI) as structural oversupply (IEA 2.5 mb/d surplus 2H26) and demand destruction (420 kb/d contraction) overwhelm tactical support within 2-3 weeks Timeframe: 2-3 weeks through mid-June as June 7 OPEC+ meeting provides directional clarity and Strait normalization completion validates structural oversupply reassertion

|

WTI crude oil faces defining regime transition on May 31, 2026, trading at $87.36 after the most violent monthly collapse in recent history - a catastrophic 17% decline through May from $105 peak following the U.S. blockade termination on May 29 and accelerating ceasefire consolidation. MACRO REGIME: TRANSITIONAL with VIX at 17.44 (well below 20 fear threshold) indicating geopolitical risk remarkably contained to energy sector rather than triggering systemic flight-to-safety, allowing fundamental drivers to reassert dominance.

Post-input mandatory news scan reveals CRITICAL fresh development: U.S. blockade of Iran ENDED May 29, 2026 (2 days ago per Wikipedia update 3 hours old), with Strait of Hormuz flows slowly resuming - this is material regime change NOT reflected in May 24 discipline data but directly validates desk's bearish thesis direction. I am now at ZERO consecutive misses after two consecutive CORRECT BEARISH calls (May 29 -8.85%, May 22 -6.84%), yet I have issued BEARISH for 6 consecutive weeks (May 29, May 22, May 15, May 8, May 1, April 24) placing me EXACTLY AT the 6-week Bias Review After threshold for Energy category per Section 2, triggering MANDATORY thesis re-justification from first principles.

Contrary price weeks in last 4: May 15 (+5.87%), May 1 (+7.3%) = 2 of 4 moved contrary to bearish lean, borderline Thesis Health degradation despite recent vindication. Three powerful crosscurrents collide. First, the geopolitical catalyst has fundamentally reversed from fragile ceasefire to normalization acceleration with U.S. policy validation. The Iran-U.S. conflict that began February 28 and drove WTI from $67 to $120 (largest weekly gain in 43-year futures history per March synthesis) has now entered NORMALIZATION phase with U.S. blockade termination May 29 representing policy-level commitment to price ceiling and Strait flow resumption.

CNBC May 29 reports U.S. and Iran have "mostly agreed" to 60-day memorandum of understanding pausing hostilities despite ongoing missile strikes, confirming diplomatic trajectory. Wikipedia confirms Strait effectively closed through late May but U.S. blockade ended May 29 with flows resuming - this validates EIA May 12 STEO projection of late May/early June normalization timeline. The 17% May collapse from $105 to current $87.36 represents market violently repricing geopolitical premium as normalization probability shifted from 60/40 (last synthesis) to 80/20 currently.

Second, fundamental bearishness INTENSIFIES with fresh May 12-13 data creating structural ceiling. The Fundamental Analyst (signal +3.5 confidence 8) argues crude undervalued based on IEA May 13 supply deficit projections, yet this CONTRADICTS Economic Analyst assessment that EIA forecasts Brent $88/b Q4 2026 - current WTI at $87.36 is already AT that forecast level, implying geopolitical premium nearly exhausted. The resolution: IEA supply deficit of 1.8 mb/d (104 mb/d demand versus 102.2 mb/d supply) is TRANSIENT disruption while structural oversupply (IEA also projects 2.5 mb/d inventory builds 2H26 once Hormuz normalizes) is PERMANENT.

Critically, IEA demand destruction data shows global oil demand revised DOWN 720 kb/d in ONE MONTH (April 14 report, 47 days ago) - from +640 kb/d growth to -80 kb/d contraction for 2026, the most significant monthly demand revision in years confirming high prices rationed demand more aggressively than supply was restricted. OPEC+'s May 3 decision to increase output by modest 188,000 bpd (versus 548,000 bpd maximum debated) signals cartel confidence that current disruptions are manageable and structural oversupply dominates medium-term.

Third, positioning dynamics show controlled liquidation underway but NOT yet complete. Institutional Analyst shows managed money net-long at elevated levels with producer hedging surge at $100+ during crisis creating classic pain trade setup, yet 17% collapse suggests significant position unwind already occurred. Technical structure confirms breakdown with death cross forming (100 SMA crossing below 200 SMA), price at $87.36 below 50-day MA, RSI 48 neutral but momentum deteriorating. MANDATORY BIAS REVIEW (6-week threshold): Re-justifying bearish thesis from first principles - crude oil at $87.36 faces structural oversupply (IEA 2.5 mb/d surplus 2H26) and demand destruction (420 kb/d contraction versus prior +640 kb/d growth expectations) that will continue overwhelming temporary geopolitical support as Strait normalizes per U.S. blockade termination May 29.

Current price AT EIA Q4 forecast $88 Brent-equivalent suggests geopolitical premium 95% exhausted, with residual downside toward $84-86 range as normalization completes. DEVIL'S ADVOCATE for BULLISH: Ceasefire could collapse before June 7 OPEC+ meeting forcing repricing to $100-110; IEA supply deficit of 1.8 mb/d is current reality per May 13 report creating tactical tightness; managed money positioning while elevated is not extreme crowding; U.S. blockade termination may not immediately translate to full Strait normalization creating residual risk premium.

However, weight of evidence STRONGLY favors continued BEARISH mean reversion: (1) U.S. blockade termination May 29 is FRESH catalyst (2 days old) representing material policy shift validating normalization trajectory, (2) EIA Q4 forecast $88 Brent implies current $87.36 WTI already at fundamental fair value with modest downside remaining, (3) IEA demand destruction (720 kb/d downgrade April 14) creates structural bearish picture overwhelming temporary supply tightness, (4) Technical breakdown confirms distribution phase complete with death cross forming, (5) CNBC reports 60-day ceasefire memorandum "mostly agreed" shifting probability toward diplomatic resolution not escalation, (6) Trading Economics confirms WTI on track for 17% May decline validating desk's directional thesis despite timing challenges in mid-month. Output: BEARISH signal -1.5 conviction 5 (unchanged from last week).

Conviction calculation: Initial 6 from fundamental bearish view (demand destruction + oversupply forecasts + U.S. blockade termination validation) and technical confirmation (breakdown structure), minus 1 for 6-week same-direction bias triggering mandatory review penalty per Rule 4, equals 5 final. This is NOT maximum conviction because: (a) Six-week same-direction streak triggers caution per Rule 4 even with fresh U.S. blockade termination catalyst validating thesis, (b) OPEC+ June 7 meeting (7 days forward) creates binary event risk requiring reduced conviction per Energy-specific guidance Section 3, (c) 2 of last 4 weeks contrary to bias shows Thesis Health weakness despite recent vindication, (d) Current price $87.36 already near EIA Q4 forecast $88 Brent-equivalent suggesting limited remaining downside (3-5%) versus noise floor 0.50% justifying directional call but capping conviction.

Primary opportunity: ceasefire extends with full Strait normalization by mid-June triggering complete geopolitical premium unwind toward $84-86 range within 2-3 weeks as structural oversupply and demand destruction overwhelm. Primary risk: ceasefire collapse forcing repricing to $100-110, assessed LOW probability given U.S. blockade termination May 29 and diplomatic momentum.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 29, 2026 | BEARISH | 5/10 | ✅ |

| May 22, 2026 | BEARISH | 5/10 | ✅ |

| May 15, 2026 | BEARISH | 5/10 | ❌ |

| May 8, 2026 | BEARISH | 5/10 | ✅ |

| May 1, 2026 | BEARISH | 5/10 | ❌ |

| April 24, 2026 | BEARISH | 6/10 | ❌ |

| April 17, 2026 | BEARISH | 6/10 | ✅ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | BEARISH | 6/10 | ❌ |

| March 20, 2026 | BEARISH | 6/10 | ✅ |

| March 14, 2026 | BULLISH | 6/10 | ✅ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Crude Oil (CL) Report Date: May 31, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 0 (CONSENSUS ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: BREAKING DOWN Regime: GEOPOLITICAL PREMIUM MEAN REVERSION WITHIN STRUCTURAL OVERSUPPLY BEAR FRAMEWORK AS CEASEFIRE NORMALIZATION REMOVES ACUTE SUPPLY SHOCK CATALYST Sentiment: FEAR FADING TO RELIEF ── WHAT THE MARKET SEES ───────────────────────── Tactically uncertain with market split between ceasefire optimists expecting further mean reversion toward $82-85 and geopolitical hawks expecting stabilization at current $87-88 levels; structural oversupply consensus (EIA $88 Q4, IEA 2.5 mb/d surplus 2H26, demand destruction 420 kb/d) implies modest downside from current $87.36 but U.S. blockade termination May 29 removes acute catalyst creating low conviction environment ── WHAT THE MARKET IS MISSING ─────────────────── Market may be underweighting U.S. blockade termination May 29 magnitude as material policy shift validating normalization trajectory faster than EIA May 12 STEO anticipated, while overweighting residual ceasefire fragility after two consecutive CORRECT desk bearish calls vindicated thesis direction; current $87.36 price already at EIA Q4 forecast $88 Brent-equivalent suggests geopolitical premium 95% exhausted yet IEA demand destruction (720 kb/d downgrade) and structural 2.5 mb/d surplus 2H26 create modest remaining downside toward $84-86 as OPEC+ June 7 meeting likely signals confidence in normalization not concern requiring production discipline ── KEY DRIVERS ────────────────────────────────── 1. Ceasefire consolidation accelerating as U.S. blockade ended May 29 with Strait of Hormuz flows slowly resuming, triggering violent 17% May collapse from $105 peak to current $87.36 as geopolitical premium unwinds faster than discipline data anticipated, yet structural oversupply fundamentals (IEA 2.5 mb/d surplus 2H26, demand destruction 420 kb/d contraction) now reasserting dominance creating further downside toward EIA Q4 forecast $88 Brent-equivalent 2. Binary catalyst tension with OPEC+ June 7 meeting (7 days forward) creating event risk as cartel faces decision on production policy amid ongoing but declining Strait disruption - May 3 modest 188k bpd increase signals confidence in normalization trajectory yet failure to offset 10.5 mb/d shut-ins during crisis peak validates desk's bearish structural view 3. Demand destruction intensifying at critical velocity with IEA May 13 report showing global demand revised DOWN 720 kb/d in single month (from +640 kb/d growth to -80 kb/d contraction 2026) confirming high prices rationing demand more aggressively than supply disruptions persist, creating fundamental ceiling at current $87 levels ── KEY ZONES ──────────────────────────────────── Resistance 2: 99.250 – 100.750 Resistance 1: 91.250 – 92.750 Pivot: ~87.360 Support 1: 79.250 – 80.750 Support 2: 74.250 – 75.750 ── DISCIPLINE BIASES ──────────────────────────── Technical: N/A Fundamental: N/A Institutional: N/A Options: N/A Economic: N/A Sentiment: N/A ── TECHNICAL STRUCTURE ────────────────────────── WTI at $87.36 in confirmed downtrend after 17% May collapse, trading below 50-day MA with death cross forming (100 SMA below 200 SMA), RSI 48 neutral but momentum deteriorating as breakdown below $88-92 support zone confirms distribution phase complete ── FUNDAMENTAL ASSESSMENT ─────────────────────── Crude overvalued 0-3% versus structural fair value $85-88 range; geopolitical premium nearly exhausted as U.S. blockade termination May 29 validates normalization trajectory while IEA demand destruction (420 kb/d contraction 2026) and EIA Q4 forecast $88 Brent imply current pricing near fundamental equilibrium but residual downside risk remains ── INSTITUTIONAL POSITIONING ──────────────────── Managed money net-long moderating from extremes with producer hedging at $100+ levels during crisis peak validating commercial bearish forward view; U.S. blockade termination May 29 represents policy-level commitment to price ceiling creating asymmetric downside as speculative length unwinds ── OPTIONS FLOW ───────────────────────────────── Insufficient current data quality for directional signal; OVX crude volatility likely elevated in 80-95 range from March spike but moderating post-ceasefire as fear premium compresses ── ECONOMIC BACKDROP ──────────────────────────── MACRO REGIME: TRANSITIONAL - VIX at 17.44 (May 21, below 20 calm threshold) indicating geopolitical risk contained to energy sector rather than systemic; Fed on hold at 3.50-3.75%, U.S. blockade termination May 29 represents material policy shift favoring price normalization as Strait flows resume late May/early June per EIA May 12 STEO projections ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 85th Trend: Days in Regime: 0 Term Structure: Historical Pattern: Outlook: Trading Context: Vol Risk/Opportunity: ── PRIMARY RISK ───────────────────────────────── Ceasefire collapses before June 7 OPEC+ meeting with renewed U.S.-Iran military escalation or complete Strait of Hormuz reclosure forcing violent reversal back toward $100-110 range as 20% supply disruption risk premium reprices and invalidates mean reversion thesis based on normalization trajectory validated by U.S. blockade termination May 29 Probability: LOW ── PRIMARY OPPORTUNITY ────────────────────────── Ceasefire extends with full Strait of Hormuz normalization by early June as EIA May 12 STEO anticipates (flows resuming late May/early June following May 29 U.S. blockade termination), triggering complete geopolitical premium unwind toward EIA Q4 forecast $88 Brent-equivalent ($84-86 WTI) as structural oversupply (IEA 2.5 mb/d surplus 2H26) and demand destruction (420 kb/d contraction) overwhelm tactical support within 2-3 weeks Timeframe: 2-3 weeks through mid-June as June 7 OPEC+ meeting provides directional clarity and Strait normalization completion validates structural oversupply reassertion ── NEXT CATALYST ──────────────────────────────── Date: June 7, 2026 Event: OPEC+ 41st Ministerial Meeting on June 7, 2026 (7 days forward) to review production policy following May 3 modest 188k bpd increase decision amid ongoing but declining Strait of Hormuz disruption and U.S. blockade termination, creating binary risk where cartel signals either confidence in normalization (bearish for prices) or concern requiring production discipline (neutral to mild bullish) Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── WTI crude oil faces defining regime transition on May 31, 2026, trading at $87.36 after the most violent monthly collapse in recent history - a catastrophic 17% decline through May from $105 peak following the U.S. blockade termination on May 29 and accelerating ceasefire consolidation. MACRO REGIME: TRANSITIONAL with VIX at 17.44 (well below 20 fear threshold) indicating geopolitical risk remarkably contained to energy sector rather than triggering systemic flight-to-safety, allowing fundamental drivers to reassert dominance. Post-input mandatory news scan reveals CRITICAL fresh development: U.S. blockade of Iran ENDED May 29, 2026 (2 days ago per Wikipedia update 3 hours old), with Strait of Hormuz flows slowly resuming - this is material regime change NOT reflected in May 24 discipline data but directly validates desk's bearish thesis direction. I am now at ZERO consecutive misses after two consecutive CORRECT BEARISH calls (May 29 -8.85%, May 22 -6.84%), yet I have issued BEARISH for 6 consecutive weeks (May 29, May 22, May 15, May 8, May 1, April 24) placing me EXACTLY AT the 6-week Bias Review After threshold for Energy category per Section 2, triggering MANDATORY thesis re-justification from first principles. Contrary price weeks in last 4: May 15 (+5.87%), May 1 (+7.3%) = 2 of 4 moved contrary to bearish lean, borderline Thesis Health degradation despite recent vindication. Three powerful crosscurrents collide. First, the geopolitical catalyst has fundamentally reversed from fragile ceasefire to normalization acceleration with U.S. policy validation. The Iran-U.S. conflict that began February 28 and drove WTI from $67 to $120 (largest weekly gain in 43-year futures history per March synthesis) has now entered NORMALIZATION phase with U.S. blockade termination May 29 representing policy-level commitment to price ceiling and Strait flow resumption. CNBC May 29 reports U.S. and Iran have "mostly agreed" to 60-day memorandum of understanding pausing hostilities despite ongoing missile strikes, confirming diplomatic trajectory. Wikipedia confirms Strait effectively closed through late May but U.S. blockade ended May 29 with flows resuming - this validates EIA May 12 STEO projection of late May/early June normalization timeline. The 17% May collapse from $105 to current $87.36 represents market violently repricing geopolitical premium as normalization probability shifted from 60/40 (last synthesis) to 80/20 currently. Second, fundamental bearishness INTENSIFIES with fresh May 12-13 data creating structural ceiling. The Fundamental Analyst (signal +3.5 confidence 8) argues crude undervalued based on IEA May 13 supply deficit projections, yet this CONTRADICTS Economic Analyst assessment that EIA forecasts Brent $88/b Q4 2026 - current WTI at $87.36 is already AT that forecast level, implying geopolitical premium nearly exhausted. The resolution: IEA supply deficit of 1.8 mb/d (104 mb/d demand versus 102.2 mb/d supply) is TRANSIENT disruption while structural oversupply (IEA also projects 2.5 mb/d inventory builds 2H26 once Hormuz normalizes) is PERMANENT. Critically, IEA demand destruction data shows global oil demand revised DOWN 720 kb/d in ONE MONTH (April 14 report, 47 days ago) - from +640 kb/d growth to -80 kb/d contraction for 2026, the most significant monthly demand revision in years confirming high prices rationed demand more aggressively than supply was restricted. OPEC+'s May 3 decision to increase output by modest 188,000 bpd (versus 548,000 bpd maximum debated) signals cartel confidence that current disruptions are manageable and structural oversupply dominates medium-term. Third, positioning dynamics show controlled liquidation underway but NOT yet complete. Institutional Analyst shows managed money net-long at elevated levels with producer hedging surge at $100+ during crisis creating classic pain trade setup, yet 17% collapse suggests significant position unwind already occurred. Technical structure confirms breakdown with death cross forming (100 SMA crossing below 200 SMA), price at $87.36 below 50-day MA, RSI 48 neutral but momentum deteriorating. MANDATORY BIAS REVIEW (6-week threshold): Re-justifying bearish thesis from first principles - crude oil at $87.36 faces structural oversupply (IEA 2.5 mb/d surplus 2H26) and demand destruction (420 kb/d contraction versus prior +640 kb/d growth expectations) that will continue overwhelming temporary geopolitical support as Strait normalizes per U.S. blockade termination May 29. Current price AT EIA Q4 forecast $88 Brent-equivalent suggests geopolitical premium 95% exhausted, with residual downside toward $84-86 range as normalization completes. DEVIL'S ADVOCATE for BULLISH: Ceasefire could collapse before June 7 OPEC+ meeting forcing repricing to $100-110; IEA supply deficit of 1.8 mb/d is current reality per May 13 report creating tactical tightness; managed money positioning while elevated is not extreme crowding; U.S. blockade termination may not immediately translate to full Strait normalization creating residual risk premium. However, weight of evidence STRONGLY favors continued BEARISH mean reversion: (1) U.S. blockade termination May 29 is FRESH catalyst (2 days old) representing material policy shift validating normalization trajectory, (2) EIA Q4 forecast $88 Brent implies current $87.36 WTI already at fundamental fair value with modest downside remaining, (3) IEA demand destruction (720 kb/d downgrade April 14) creates structural bearish picture overwhelming temporary supply tightness, (4) Technical breakdown confirms distribution phase complete with death cross forming, (5) CNBC reports 60-day ceasefire memorandum "mostly agreed" shifting probability toward diplomatic resolution not escalation, (6) Trading Economics confirms WTI on track for 17% May decline validating desk's directional thesis despite timing challenges in mid-month. Output: BEARISH signal -1.5 conviction 5 (unchanged from last week). Conviction calculation: Initial 6 from fundamental bearish view (demand destruction + oversupply forecasts + U.S. blockade termination validation) and technical confirmation (breakdown structure), minus 1 for 6-week same-direction bias triggering mandatory review penalty per Rule 4, equals 5 final. This is NOT maximum conviction because: (a) Six-week same-direction streak triggers caution per Rule 4 even with fresh U.S. blockade termination catalyst validating thesis, (b) OPEC+ June 7 meeting (7 days forward) creates binary event risk requiring reduced conviction per Energy-specific guidance Section 3, (c) 2 of last 4 weeks contrary to bias shows Thesis Health weakness despite recent vindication, (d) Current price $87.36 already near EIA Q4 forecast $88 Brent-equivalent suggesting limited remaining downside (3-5%) versus noise floor 0.50% justifying directional call but capping conviction. Primary opportunity: ceasefire extends with full Strait normalization by mid-June triggering complete geopolitical premium unwind toward $84-86 range within 2-3 weeks as structural oversupply and demand destruction overwhelm. Primary risk: ceasefire collapse forcing repricing to $100-110, assessed LOW probability given U.S. blockade termination May 29 and diplomatic momentum.