S&P 500 Key Levels This Week — Support, Resistance & Confluence Zones

S&P 500 key levels breakdown: support zones, resistance zones, confluence and price structure.

S&P 500 key levels breakdown: support zones, resistance zones, confluence and price structure.

Gold institutional positioning: COT data, sentiment analysis and smart money flow assessment.

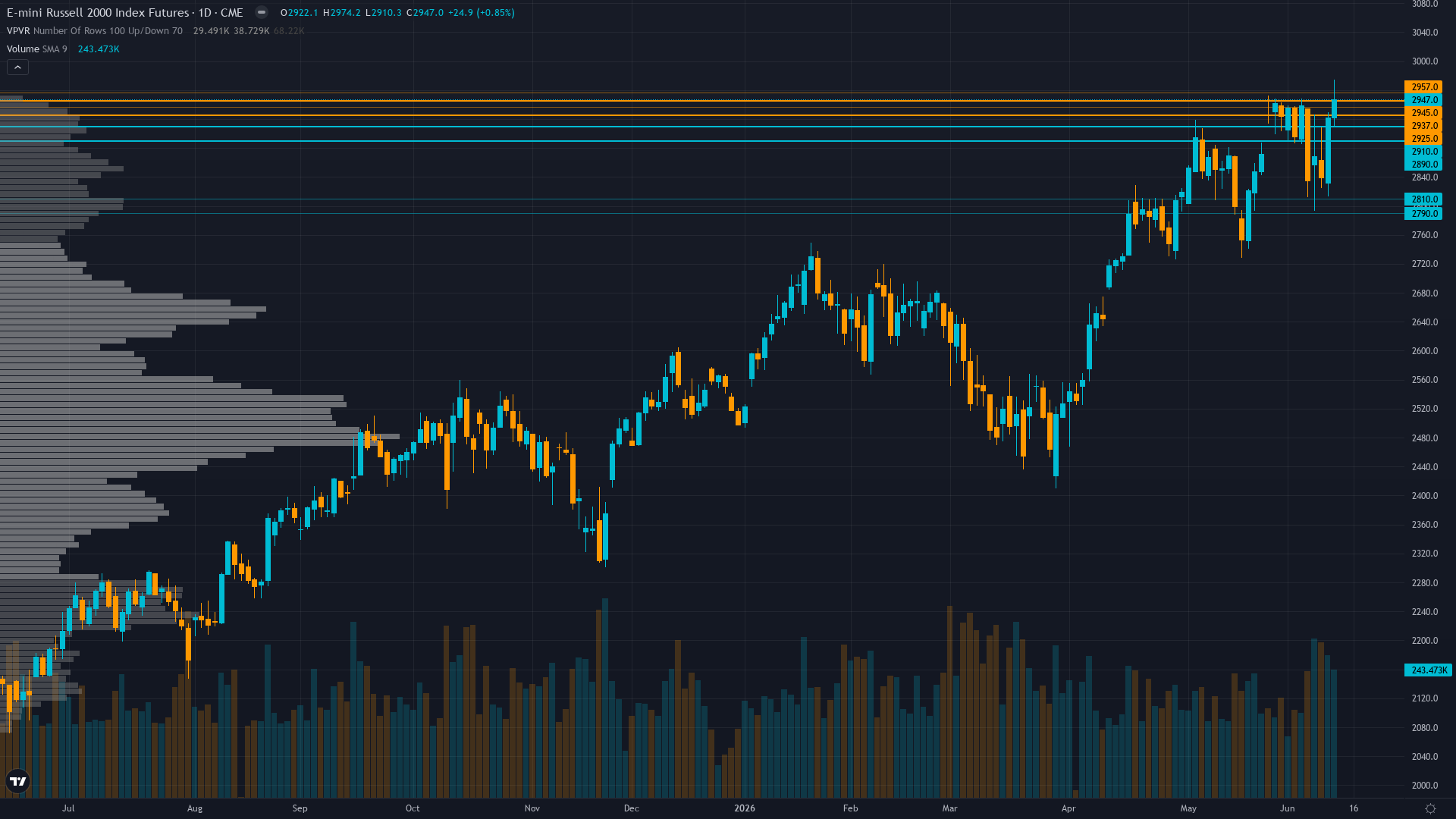

Russell 2000 institutional positioning: COT data, sentiment analysis and smart money flow assessment.

Crude Oil key levels breakdown: support zones, resistance zones, confluence and price structure.

This week's Russell 2000 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

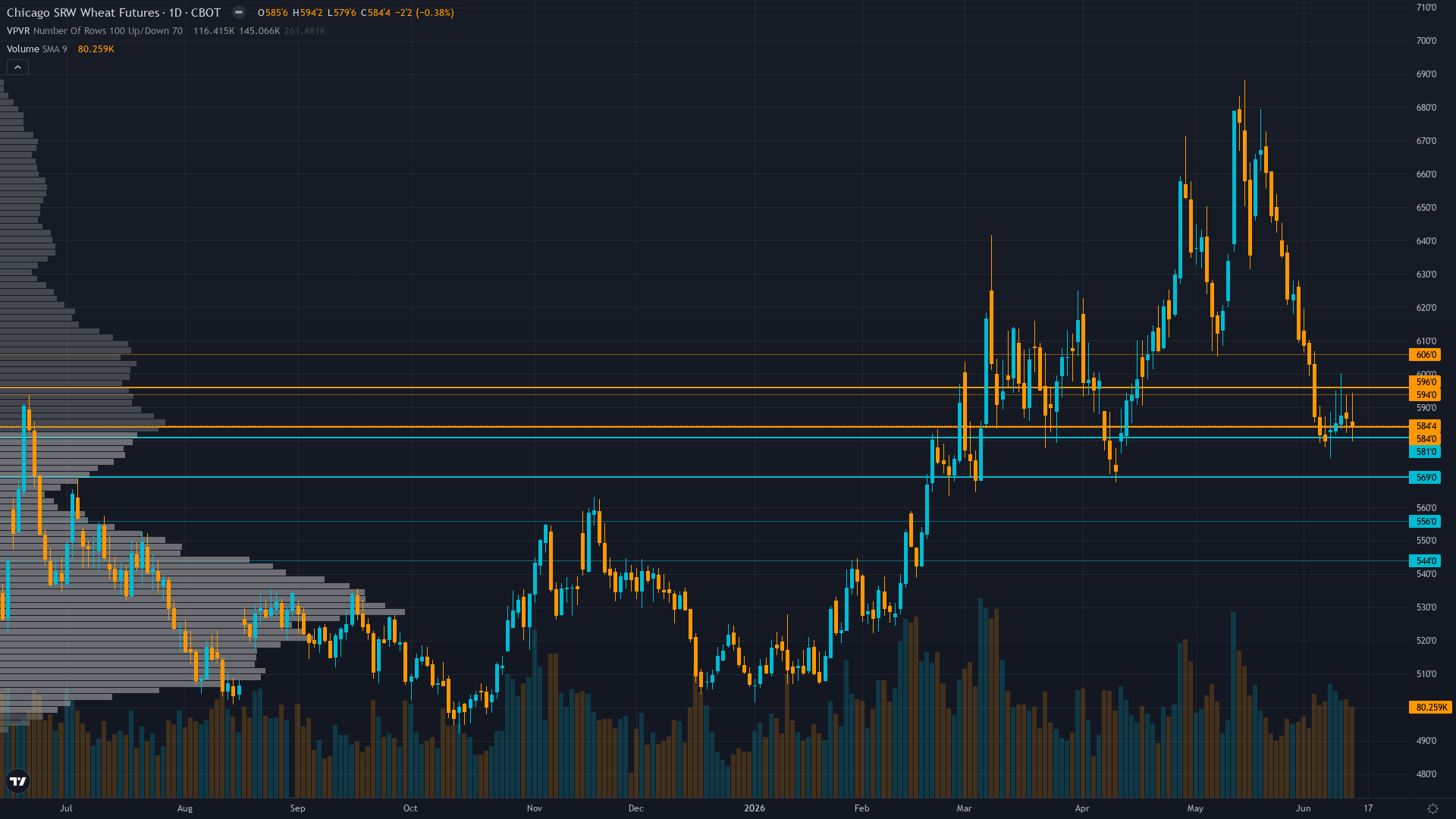

This week's Wheat outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

This week's 30-Year Treasury outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Russell 2000 (RTY): Market consensus may be underpricing the magnitude of reconstitution-driven flows in 12-day window while overweighting sentiment bearishness (AAII 47.7% bears) as contrarian opportunity, desk sees tactical bullish setup with calendar catalyst providing high-probability support ve

Core

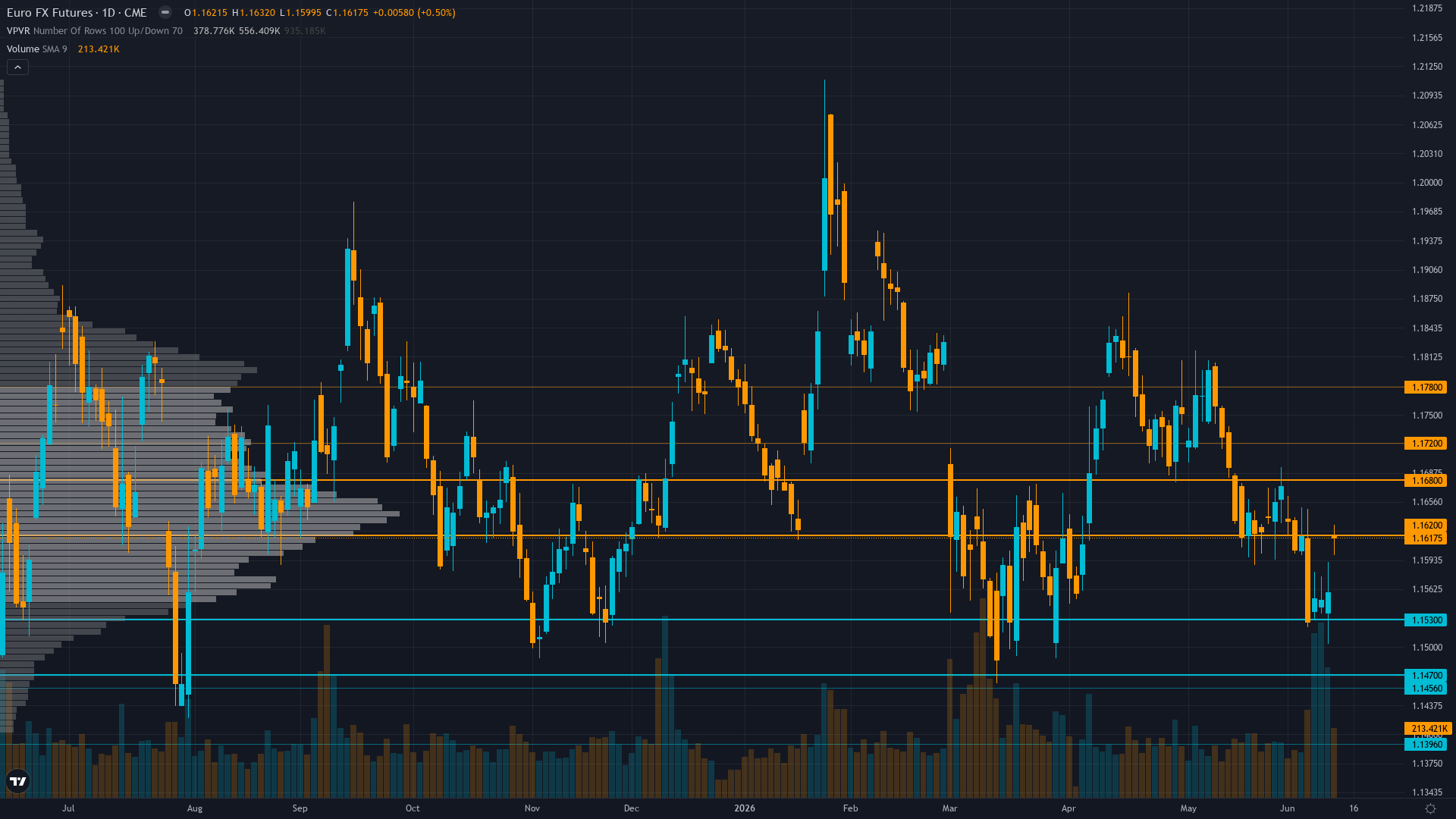

EUR consolidation in 1.15-1.18 range through June with neutral bias after ECB June 11 delivered expected 25bp hike, year-end consensus targets 1.20-1.22 dependent on Fed easing timeline and eurozone demand recovery materializing

Core

Cautiously positioned ahead of June 17 FOMC with strategists acknowledging June 22 rebalancing flows provide structural support but defensive given expected removal of Fed easing bias and elevated valuations requiring execution

Core

Mixed with institutional year-end targets remaining at $5,000-5,400 maintaining structural bull case but near-term positioning increasingly defensive following 25% correction from January peaks and 9 consecutive weeks of directional analytical failures creating elevated tactical caution ahead of Jun

Core

Tactically bearish on geopolitical premium fade with market pricing 60-92% probability of sub-$85 by month-end per Polymarket; structural oversupply consensus (J.P. Morgan $60 Brent, EIA $88 Q4, IEA 2.5 mb/d surplus 2H26) implies modest remaining downside from current $84.88 as mean reversion 90-95%