GBP/USD COT & Institutional Positioning — Smart Money Analysis

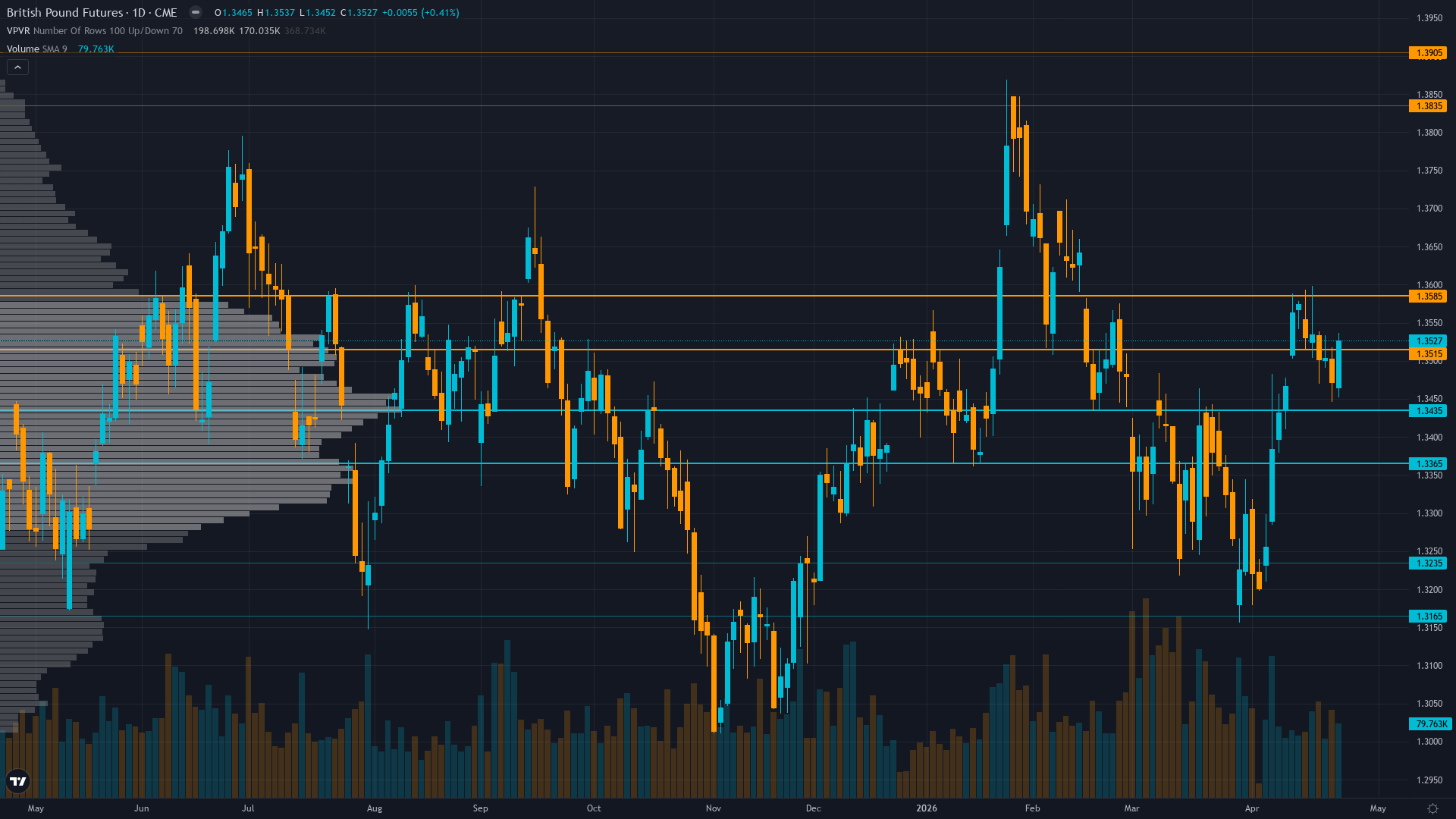

GBP/USD institutional positioning: COT data, sentiment analysis and smart money flow assessment.

GBP/USD institutional positioning: COT data, sentiment analysis and smart money flow assessment.

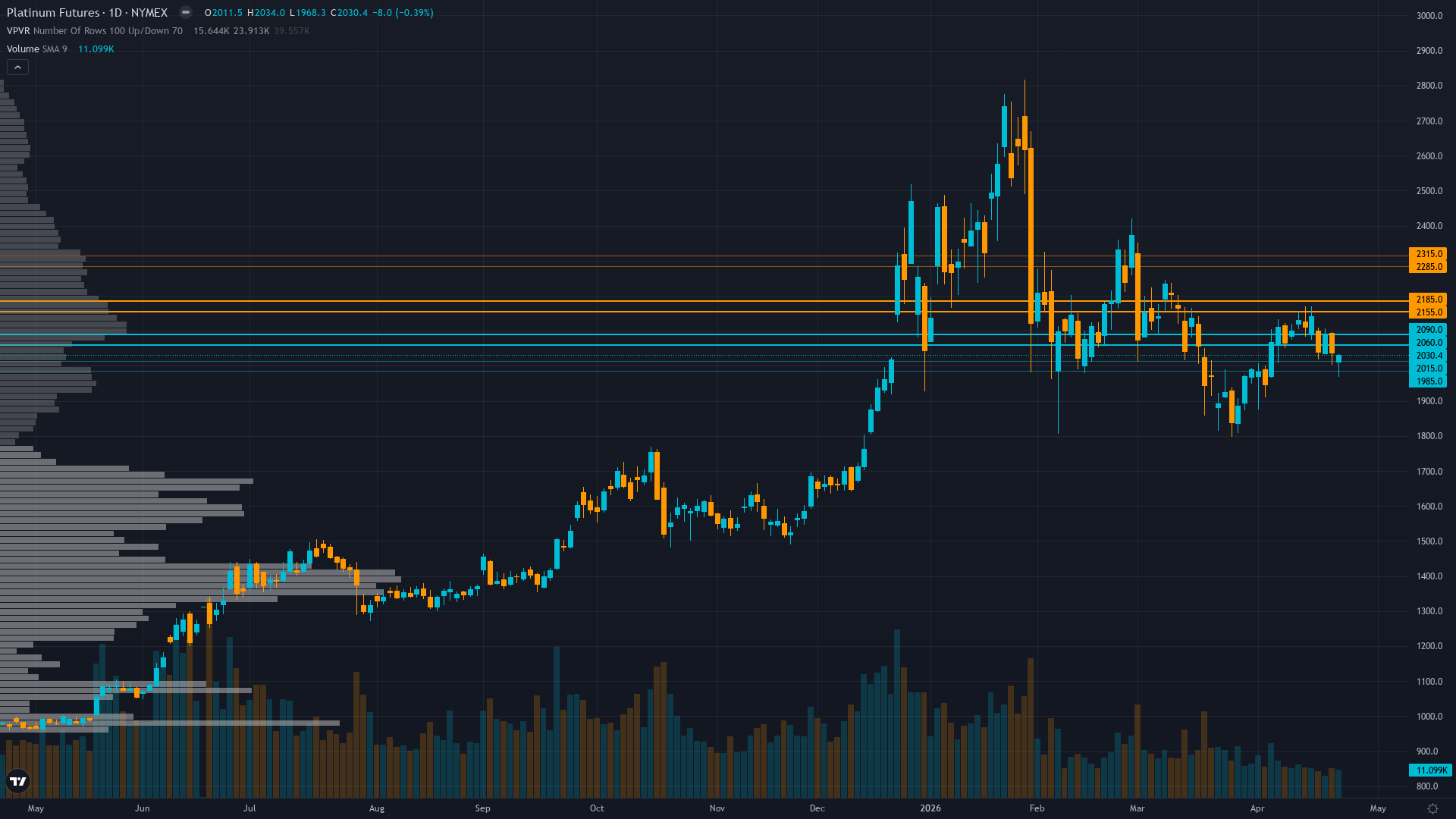

Platinum key levels breakdown: support zones, resistance zones, confluence and price structure.

Gold institutional positioning: COT data, sentiment analysis and smart money flow assessment.

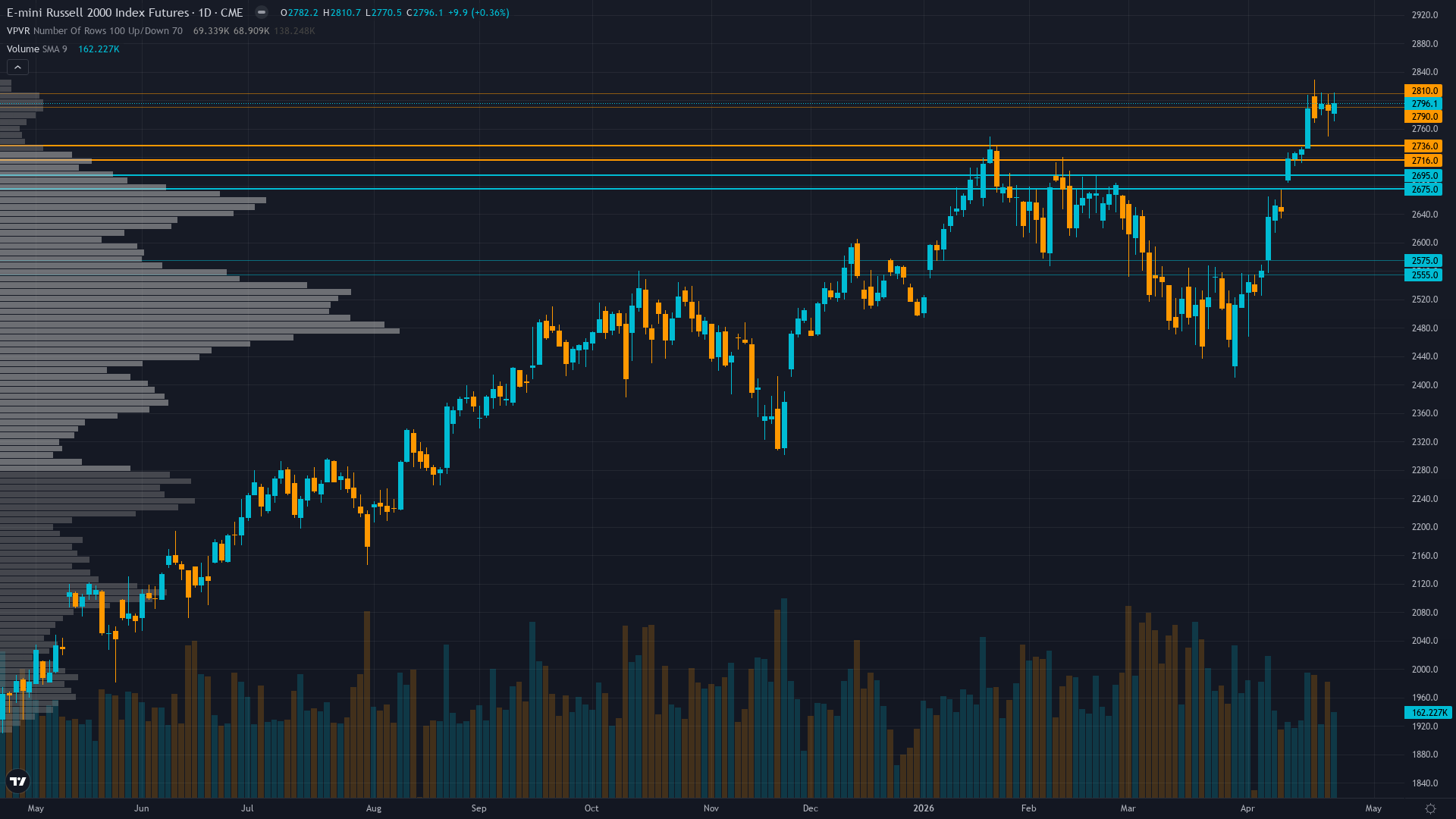

Russell 2000 institutional positioning: COT data, sentiment analysis and smart money flow assessment.

This week's Crude Oil outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Silver key levels breakdown: support zones, resistance zones, confluence and price structure.

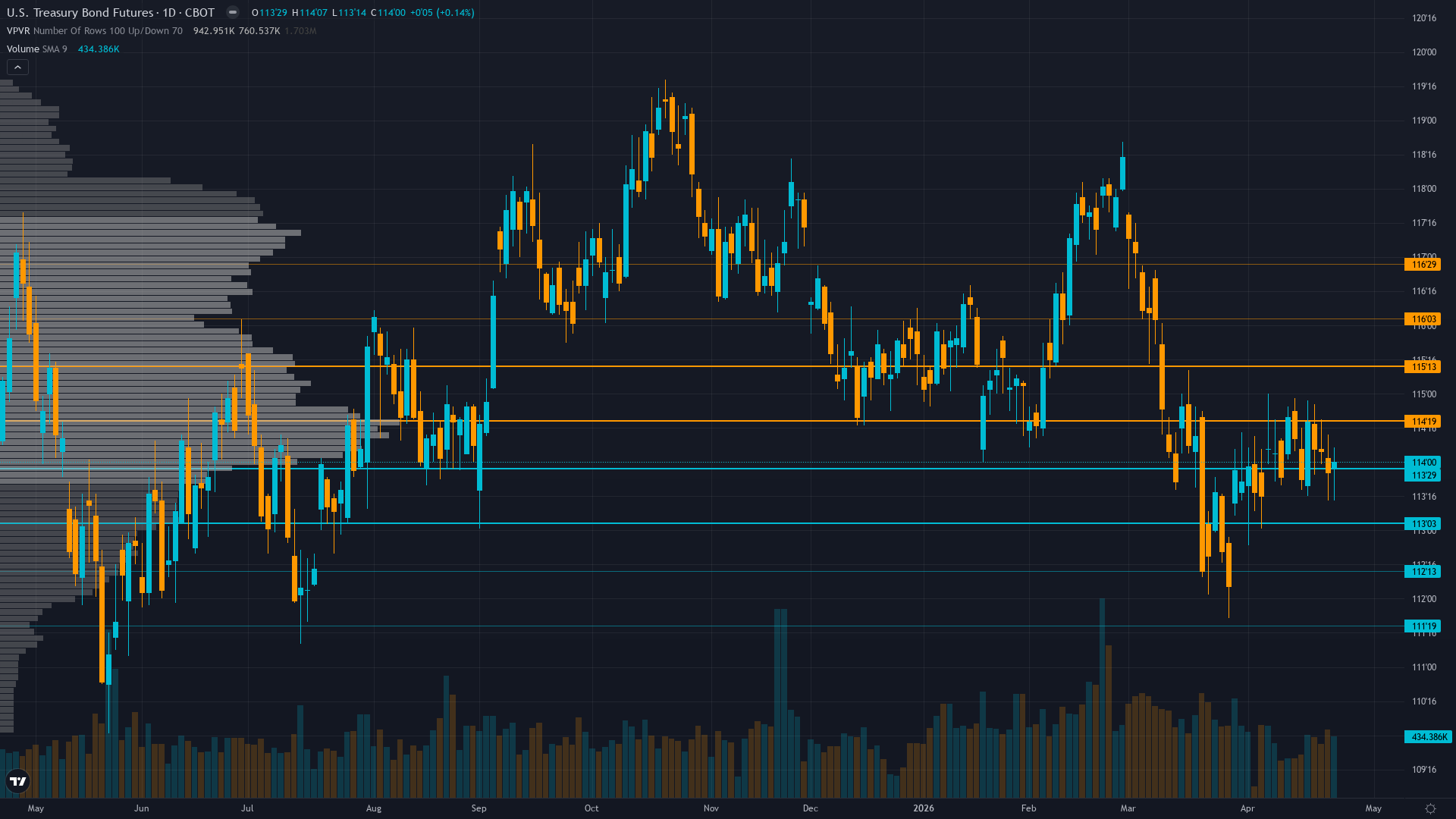

30-Year Treasury key levels breakdown: support zones, resistance zones, confluence and price structure.

This week's EUR/USD outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

USD/JPY key levels breakdown: support zones, resistance zones, confluence and price structure.

AUD/USD institutional positioning: COT data, sentiment analysis and smart money flow assessment.

This week's GBP/USD outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

AUD/USD key levels breakdown: support zones, resistance zones, confluence and price structure.