Mon-T Weekly Review — w/e 22 May 2026

Six from eight, crude oil finally cooperates, and platinum reminds the desk that WPIC reports do not constitute a floor.

There is a version of this week where I open by celebrating the desk's best crude oil call in months. There is another version where I linger on platinum's 6.7% collapse against a bullish call, or gold dropping 4.7% while the desk sat on its hands with a NO CALL. I am going to try to do all three, because that is what happened, and the honest scorecard contains all of it.

Six of eight directional calls correct, a 75% hit rate that matches the prior week's ungraded estimate and represents the desk's most consistent recent stretch. Eight directional calls at an average confidence of 6 shows measured commitment rather than the whispered 5.25 of the May 1 hibernation period, and seven NO CALL markets demonstrate the agents still know when to fold their arms. Crude oil, the desk's longest-running headache since the Iran war began in February, was called BEARISH at 5/10 and dropped 6.84%. After months of bearish calls getting torched by Hormuz headlines, the ceasefire timeline finally bent in the desk's favour. That single call was worth the price of admission.

But the misses cut deep. Platinum was called BULLISH at 6/10 ahead of the WPIC Platinum Quarterly report on May 18, and the metal promptly fell 6.7% from $2,068 to $1,930. The Russell 2000, after weeks of bullish glory that I praised in every review, was called BEARISH at 6/10 and rallied 2.54% to prove the desk's bearish pivot was premature. And gold, where the desk issued NO CALL despite a mild bullish lean in the synthesis, crashed 4.68%. I said last week that the CPI-driven gold thesis needed resolution. It resolved, and the desk was not in the room.

|

15

Markets

|

8

Directional

|

6

Correct

|

75%

Accuracy

|

7

No Calls

|

Eight directional calls this week, with six landing on the right side. The other seven markets got the NO CALL treatment. A 75% directional hit rate is solid, and the confidence calibration was clean: the two highest-conviction calls at 7/10 were Wheat BULLISH (+1.77%, correct) and Soybeans BULLISH (+0.36%, correct). The two misses came from 6/10 calls, Platinum BULLISH and Russell 2000 BEARISH, which is exactly how you want the distribution to work. Your high-conviction calls should outperform your moderate ones, and this week they did.

The NO CALL markets tell a more complicated story. Gold dropped 4.68% on a NO CALL, which the desk will feel given its own synthesis showed a mild bullish lean. Sterling rallied 0.91% and the yen weakened 0.70%, both misses by the NO CALL scoring framework. Copper bounced 1.93% after a brutal breakdown the desk correctly identified but chose not to trade. When four of seven NO CALL markets produce moves above the noise threshold, the framework is protecting the accuracy percentage at the cost of opportunity. That trade-off is defensible. It is not always comfortable.

|

57/99

Correct / Total

|

57.6%

Accuracy

|

99 / 96

Directional / No Call

|

The rolling twelve-week figure sits at 57.6% across 99 directional calls, with 96 no-call abstentions. That engagement split tells you the desk is calling direction on roughly half of all market-weeks, a rate that has fallen steadily since the 70%+ pace of February when the precious metals thesis was printing money. This week's 75% accuracy on eight calls nudges the number in the right direction, and the December-January catastrophes have now fully aged out of the window. If the desk can maintain 70%+ accuracy while increasing its directional volume to ten or twelve calls per week, we should finally see the rolling figure crack through 60% on a sustained basis. The 57-58% range has been home for too long.

|

Bias Called

BEARISH

|

Confidence

6/10

|

Result

CORRECT

|

Grade

B+

|

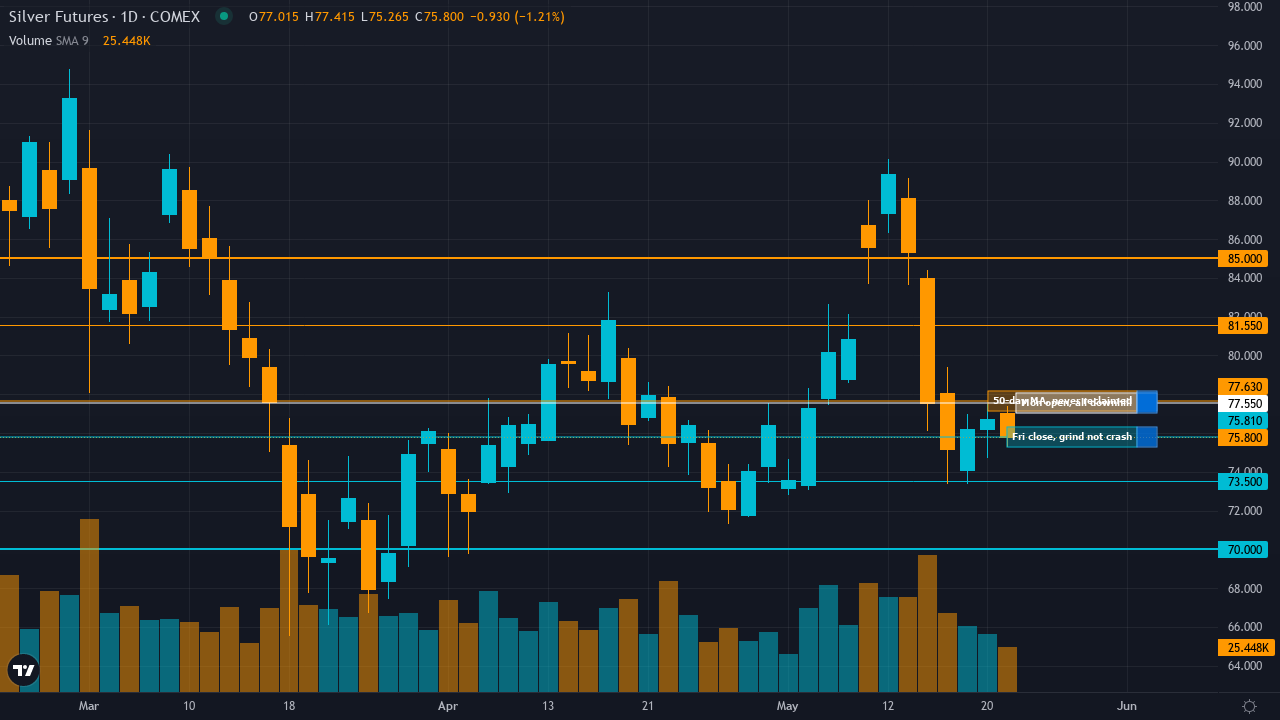

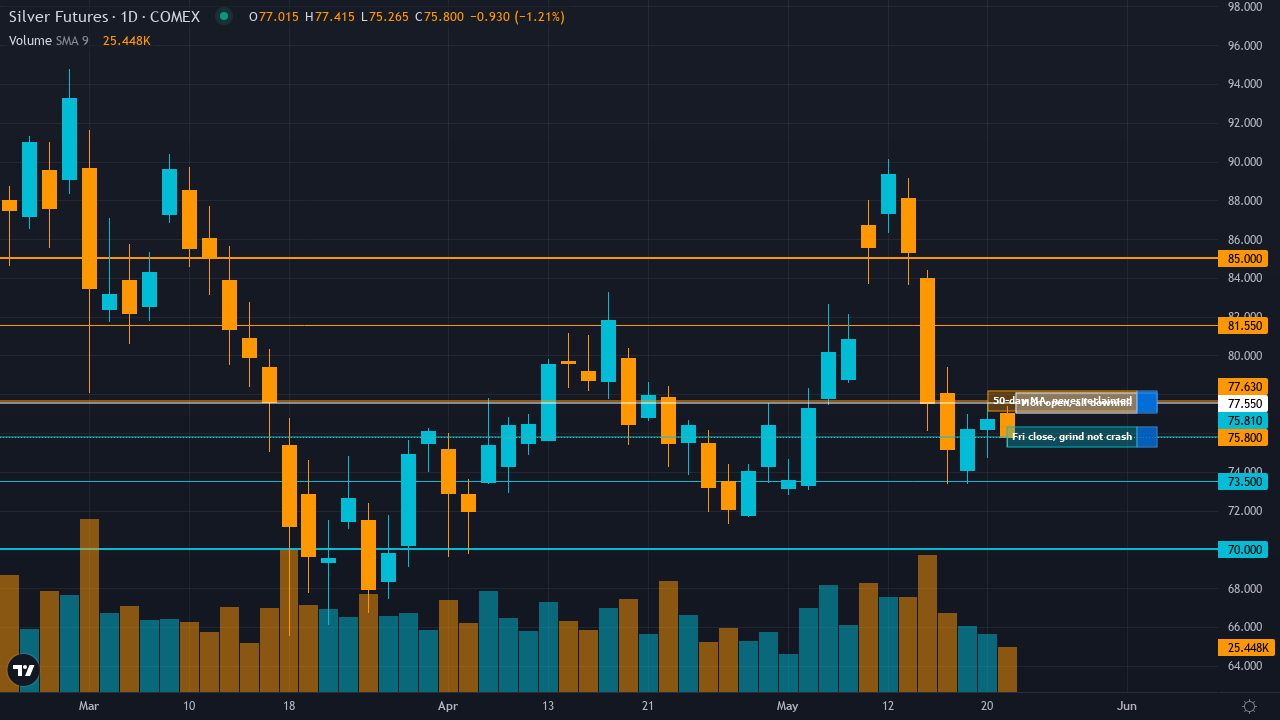

| Monday Open | 77.55 |

| Friday Close | 75.805 |

| Move | -2.25 |

| ▼ R2 | 85.00 |

| ▼ R1 | 81.55 |

| ▲ S1 | 73.50 |

| ▲ S2 | 70.00 |

S1 at $73.50 was never seriously tested, with Friday's close at $75.81 settling roughly $2.30 above that support level. The market drifted lower through the week without the kind of violent cascade the desk's synthesis warned about from extreme retail long positioning at 90%. R1 at $81.55 was never remotely threatened. The prior week's -9.18% single-session crash on May 15 had already done the heavy lifting, and this week's price action was more of a controlled descent than a capitulation. Trading Economics confirmed silver held below $4,700 equivalent gold levels and surrendered gains from earlier in May. Yahoo Finance reported silver July futures opened Friday at $77.01 and drifted lower to $76.11 in early trading, confirming the bearish grind the desk anticipated. The levels framework bracketed the action adequately, with S1 providing downside context that was not needed and R1 marking an overhead ceiling that was never approached.

The called edge identified the May 15 cross-asset selloff as a Fed-driven cyclical liquidation within an intact secular bull structure, not a secular trend change. The desk argued that the UBS May 14 deficit-narrowing revision to 60-70 million ounces from prior estimates introduced fresh demand elasticity headwinds at elevated prices, while extreme 90% retail long positioning faced forced liquidation risk as price broke below $77-78 support. That thesis was directionally correct: silver continued lower through the week as the inflation narrative and Fed higher-for-longer stance kept pressure on non-yielding assets. GoldSilver's May 14 outlook noted the bear case centred on a June dot plot signalling no cuts and sticky inflation through Q3, which is precisely the macro backdrop the desk identified. The edge call earned its keep, though the magnitude of the move at 2.25% was modest compared to the 5-7% daily swings this metal has produced in 2026.

The Technical agent and Economic agent were the week's correct voices. The Technical agent, weighted at 20%, called BEARISH on the breakdown below the 50-day MA at $77.63, and price never reclaimed that level. The Economic agent at 30% weight correctly identified the cross-asset inflation selloff and Fed hawkish stance as structural headwinds. The Fundamental agent at 25% weight called BULLISH on the sixth-year structural deficit, and it was wrong for the near term, though the desk wisely overrode its signal given the technical breakdown. The Sentiment agent at 10% called BEARISH on fear-driven retail positioning, and its contrarian instinct proved correct. The Institutional agent at 15% called BULLISH on washed-out managed money, which was the wrong read this week as the positioning story took a back seat to macro pressure. When the desk correctly overrode its highest-weighted bullish discipline to follow the Technical and Economic agents, that is the synthesis framework doing exactly what it should.

Silver returns as Market of the Week for what must be the seventh or eighth time in 2026, and for the first time in a while, it comes back in control rather than chaos. The desk called BEARISH at 6/10, a complete reversal from the prior week's BULLISH call at 6/10 that was missed, and silver drifted lower from Monday's open at $77.55 to Friday's close at $75.81 for a measured 2.25% decline.

The backstory matters. The prior week saw silver crash 9.18% in a single session on May 15, the most violent one-day decline in months, driven by what CNBC characterised as mounting inflation fears creating simultaneous pressure on bonds, stocks, and precious metals. The desk's MOTW selection for this week identified that crash as the catalyst for a bearish continuation thesis, arguing that the May 15 breakdown below the 50-day MA at $77.63 confirmed near-term bearish momentum despite the sixth-year structural deficit remaining intact. That thesis proved correct. Silver never reclaimed $78 during the week and settled near the lower end of the $73-78 range the desk mapped.

The free MOTW report, published on the Ghost site Sunday evening, laid out the full thesis with the UBS May 14 deficit revision as a fresh headwind and the 90% retail long positioning as liquidation fuel. Yahoo Finance confirmed silver prices 'hardly moved all week' with July futures opening Friday at $77.01 before drifting to $76.11, consistent with the grinding lower pattern the desk predicted. Trading Economics noted silver had 'surrendered gains recorded earlier this month that were fueled by optimism surrounding AI-related stocks.'

The grade is B+ rather than A because while direction was correct and the thesis was sound, the 2.25% move was modest for a metal that routinely produces 5-7% weekly swings. The desk correctly identified the direction and the drivers, but the magnitude did not reward the thesis with the kind of price action that earns top marks. For a market where the desk's February glory days produced 9% weekly gains on BULLISH calls, this was a quieter, more professional kind of correct. Sometimes the best calls are not the loudest.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 6/10 | 7432 | 7492.25 | 0.81 | CORRECT | B |

| BULLISH at 6/10 and the S&P gained 0.81% to fresh closing highs above 7490. The desk's thesis about Q1 earnings validation and intact uptrend structure above the 50-day MA proved correct, though the move was modest. Direction right, conviction appropriate, magnitude just above the noise floor. The seventh consecutive week of gains for the broader market. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 29231.75 | 29557 | 1.11 | — | — |

| NO CALL at 5/10 on a 1.11% rally. The Nasdaq ground higher while the desk sat this one out with a mild bearish lean in the synthesis that did not meet the signal threshold. A 1.11% move is right at the boundary of meaningful, and the desk's caution was defensible if unglamorous. At least it was not another 6% NQ miss. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | 103.5 | 96.42 | -6.84 | CORRECT | A |

| BEARISH at 5/10 and crude collapsed 6.84%. The OPEC May 13 demand downgrade and IEA contraction forecast the desk identified as fresh catalysts finally overwhelmed the geopolitical premium. After months of bearish frustration, the ceasefire timeline bent in the desk's favour. Best call on the board this week. | |||||||

|

Gold

CORE

|

NO CALL | — | 4730 | 4508.6 | -4.68 | — | — |

| NO CALL at 5/10 on a 4.68% crash. Gold fell from $4,730 to $4,509 as the Warsh Fed transition and elevated real yields continued to pressure the metal. The desk's synthesis showed a mild bullish lean but the signal did not clear the threshold. A 4.68% move on a NO CALL is the kind of miss that keeps you up at night, even if the procedure was followed correctly. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1623 | 1.1617 | -0.05 | — | — |

| NO CALL at 5/10 on a 5-pip move. The euro went absolutely nowhere, and the desk's twelfth consecutive NO CALL on this pair was vindicated by the platonic ideal of currency immobility. At this point, EUR/USD and the desk have a non-aggression pact. The ECB on June 5 might finally break the stalemate. | |||||||

|

Silver

EXTENDED

|

BEARISH | 6/10 | 77.55 | 75.805 | -2.25 | CORRECT | B+ |

| This week's MOTW. BEARISH at 6/10 on the May 15 breakdown continuation thesis, and silver drifted lower by 2.25%. The UBS deficit revision and extreme retail positioning headwinds drove the call. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.0063385 | 0.006294 | -0.7 | — | — |

| NO CALL at 5/10, the yen weakened 0.70%. The eighth consecutive NO CALL on this pair, and this one scored as a miss. The desk's intervention-risk thesis kept it on the sidelines while the yen drifted through the 158-159 range. A 0.70% move for FX_MAJOR clears the noise threshold narrowly. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.332 | 1.3441 | 0.91 | — | — |

| NO CALL at 5/10, sterling rallied 0.91%. The tenth consecutive NO CALL on cable, and this one was a clear miss with nearly a full percent of upside the desk left on the table. The June 18 BoE is now 27 days away, and at some point the agents need to form a view on this pair. | |||||||

|

Copper

EXTENDED

|

NO CALL | — | 6.27 | 6.391 | 1.93 | — | — |

| NO CALL at 5/10, copper bounced 1.93% from the May 15 breakdown low. The desk correctly identified the fundamental-technical schism but chose to step aside rather than pick a direction. The Grasberg supply deficit thesis won the week, and the desk watched from the cheap seats. | |||||||

|

Russell 2000

EXTENDED

|

BEARISH | 6/10 | 2799.6 | 2870.8 | 2.54 | MISSED | D |

| BEARISH at 6/10 and the Russell rallied 2.54%. After four consecutive correct BULLISH calls earlier this spring, the desk flipped bearish following the May 15 breakdown and immediately got punished. The oversold RSI at 33.73 that the desk identified as 'without bullish divergence' turned out to be a classic bounce setup. When your own analysis flags the contrarian case and then dismisses it, that is a process failure worth examining. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | 0.714 | 0.71285 | -0.16 | — | — |

| NO CALL at 5/10 on a 16-pip decline. The Aussie went effectively nowhere while the desk sat out the RBA-Fed policy divergence thesis that has been its most reliable FX view of 2026. A tiny move validates the abstention. The June 3-4 RBA meeting should force a view. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | 112.31 | 111.53 | -0.69 | CORRECT | B |

| BEARISH at 5/10, bonds fell 0.69%. The desk's longest-running bearish thesis continues its remarkably consistent run, with the April CPI shock and fiscal deficit deterioration providing the backdrop. Direction correct, modest move, minimum conviction. The bearish bond call remains the desk's most reliable single-market view across 2026. | |||||||

|

Wheat

FULL DESK

|

BULLISH | 7/10 | 635.75 | 647 | 1.77 | CORRECT | B+ |

| BULLISH at 7/10 and wheat rallied 1.77%. The May 12 WASDE production shortfall thesis, the worst since 1972, continued to support prices despite the pullback from the 688 highs. The desk's first directional call on wheat since the mandatory miss-streak reset landed correctly. The drought narrative is winning the argument against global surplus data, and the desk caught it. | |||||||

|

Soybeans

FULL DESK

|

BULLISH | 7/10 | 1193 | 1197.25 | 0.36 | CORRECT | C+ |

| BULLISH at 7/10 and soybeans edged up 0.36%. Direction correct, but the move was thin enough to make you wonder whether the conviction was justified. The renewable diesel structural demand thesis and declining stocks-to-use ratio provided the floor, but the 3% profit-taking from the May 13 highs limited upside. A 7/10 call on a 0.36% move is the definition of right direction, wrong magnitude. | |||||||

|

Platinum

FULL DESK

|

BULLISH | 6/10 | 2068.1 | 1929.8 | -6.69 | MISSED | F |

| BULLISH at 6/10 and platinum cratered 6.69%. The desk positioned ahead of the May 18 WPIC Platinum Quarterly binary catalyst, arguing the technical base above $2,000 created asymmetric upside. The market disagreed violently, breaking $2,000 with authority and settling at $1,930. An F grade is warranted when a 6/10 call misses by 6.7% in the wrong direction on a binary event the desk explicitly identified as binary. The worst call on the board by a considerable margin. | |||||||

|

✦ Best Call: Crude Oil (CL)

BEARISH at 5/10 and crude dropped 6.84% from $103.50 to $96.42. After months of bearish calls being incinerated by Hormuz headlines, after the 21% moonshot in March that was the desk's greatest triumph and the 13% surge in April that was its most painful reversal, crude oil finally, mercifully, did what the structural oversupply thesis said it should. The ceasefire timeline the desk identified as the mean-reversion trigger appears to be approaching the resolution the EIA projected for late May. OPEC's May 13 demand downgrade and the IEA's demand contraction forecast were the fresh catalysts the desk flagged, and the market heard them. At minimum conviction, the desk was barely committing, which is appropriate humility after two consecutive bearish misses. But direction was emphatically right, and a 6.84% move on a commodity contract is real money. |

⚠️ Worst Call: Platinum (PL)

BULLISH at 6/10 and platinum collapsed 6.69% from $2,068 to $1,930. The desk positioned bullish ahead of the May 18 WPIC Platinum Quarterly report, arguing that the technical base formation above $2,000 support combined with the binary catalyst created asymmetric upside. Instead, the WPIC report either disappointed or was overwhelmed by broader precious metals weakness, and platinum crashed through $2,000 with the kind of authority that makes support-level analysis look decorative. I noted last week that the desk had been 'gun-shy on platinum conviction after January's catastrophic miss.' This week proves the gun-shyness was well-founded. The desk should have stayed at NO CALL until the WPIC data resolved rather than front-running the catalyst. When a binary event is genuinely binary, being positioned before the outcome is a coin flip dressed up as analysis. |

The Economic agent had the strongest week across the directional calls, correctly supporting the bearish crude oil thesis through demand destruction and OPEC downgrade frameworks, driving the bearish bond call that landed cleanly, and providing the macro backdrop for the silver bearish stance. Its identification of April CPI at 3.4% as a regime-shifting catalyst that removed Fed easing hopes proved to be the most useful analytical lens. The Fundamental agent had a mixed week: its agricultural work drove correct BULLISH calls on wheat and soybeans through the WASDE production shortfall and renewable diesel demand theses respectively, but its BULLISH conviction on platinum's structural deficit was overwhelmed by the very macro forces the Economic agent warned about.

The weakest collective performance came from the equity disciplines on the Russell 2000 bearish call, where four of six agents showed bearish leans following the May 15 breakdown but small caps promptly rallied 2.54% to prove the thesis premature. The desk's observation that RSI at 33.73 was 'oversold without bullish divergence' turned out to be exactly the kind of oversold condition that triggers bounces rather than continuations. After weeks of correctly riding the RTY rally, the desk flipped bearish at the worst possible moment. The Sentiment agent, which remained neutral on RTY this week, was the only voice not actively contributing to the wrong call.

June is catalyst season. The June 5 ECB meeting will determine whether the euro's twelve-week NO CALL hibernation finally ends with a directional view. The June 16-17 FOMC, Kevin Warsh's first as Chair, is the macro event of the quarter, with markets pricing zero cuts and the new dot plot potentially reshaping the rate trajectory that has dominated every asset class since March. The June 18 BoE follows immediately after. For commodities, the June 10 WASDE update on wheat will test whether the worst US production shortfall since 1972 gets worse or stabilises. Crude oil's ceasefire timeline per the EIA projects Strait normalisation in late May to early June, which means the geopolitical premium that has defined 2026 markets could finally collapse in the coming fortnight. The desk will have its Sunday views. I suspect the NO CALL count decreases as the catalyst density increases.