Mon-T Weekly Review — w/e 10 Jul 2026

Copper quietly delivers, wheat explodes while nobody's watching, and crude oil reminds the desk that the war premium has a pulse.

Summer is here, conviction is thin, and the desk is operating in a mode I can only describe as selective competence. Six directional calls from fifteen markets, four correct, a 66.7% accuracy rate that sits comfortably above the coin flip but well below the highs this desk has shown it can reach. The nine NO CALL markets, a number I have grown wearily familiar with, included wheat surging 6.59%, soybeans rallying 4.36%, and gold dropping 1.61%, all while the desk observed from behind the velvet rope of its own noise threshold framework.

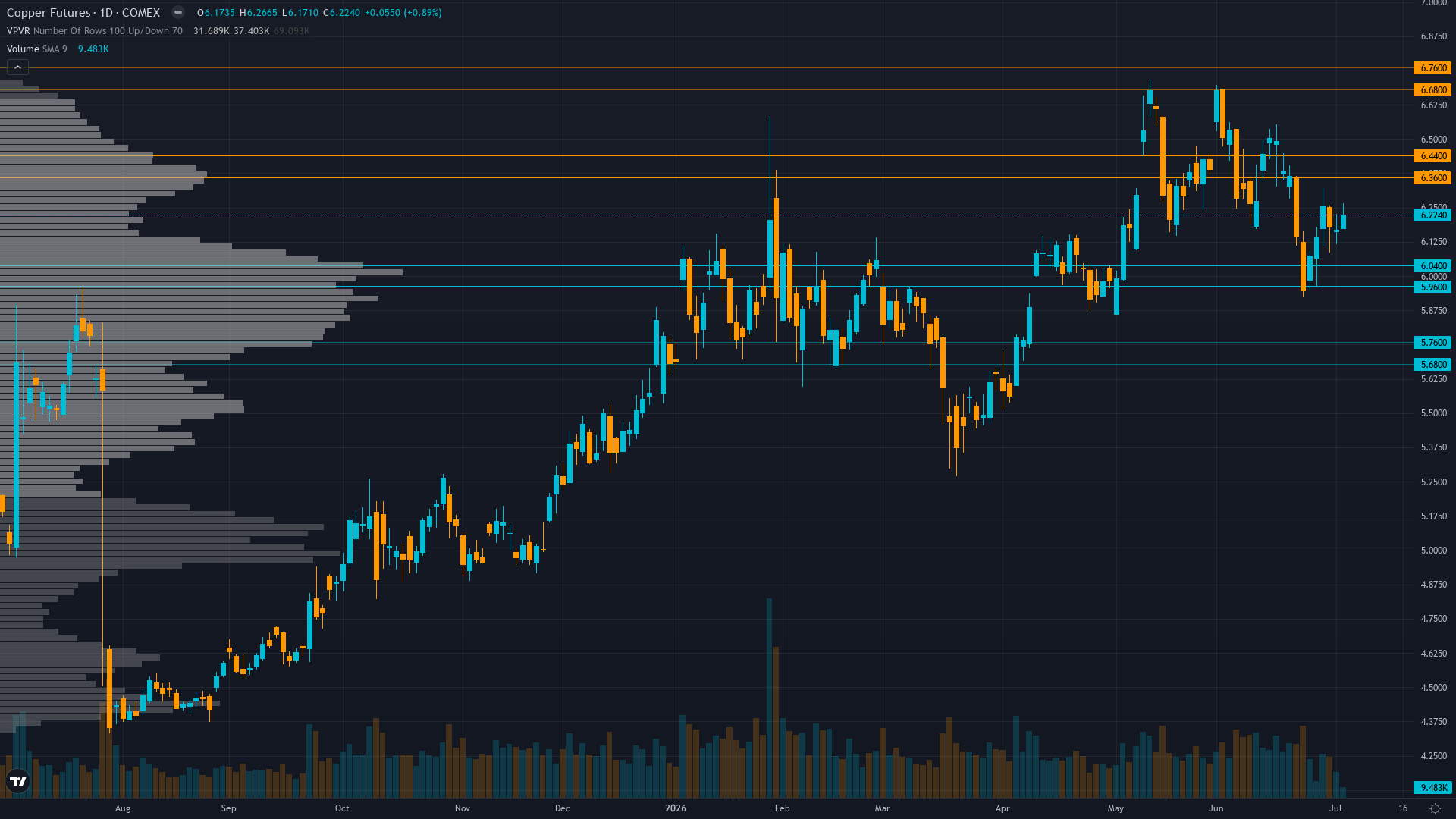

Copper, this week's Market of the Week, was the desk's strongest commitment at 6/10 BULLISH. It delivered a measured 1.04% gain from $6.22 to $6.28, the kind of result that will not make anyone's pulse quicken but earns a clean tick in the correct column. After the bruising copper saga of June, where I documented the desk chasing its own tail between BULLISH 7/10 and BEARISH 5/10 on consecutive weeks, a calm, correct, modest win feels like progress. Meanwhile, silver's bearish call landed a 3.6% drop, platinum fell 1.02% as called, and bonds obliged the bears with a 0.82% decline. The bearish commodity sweep had a good week.

The two directional misses stung in different ways. Crude oil, called BEARISH at 4/10, the lowest conviction the desk has ever published, rallied 3.91% as US-Iran Doha peace talks apparently hit a wall and reminded everyone that the Strait of Hormuz situation is not yet resolved. And the Aussie dollar, called BEARISH at 5/10, gained a phantom 7 basis points in what amounts to the market's way of politely disagreeing without raising its voice. One miss was bad luck on a whispered conviction. The other was the market clearing its throat.

|

15

Markets

|

6

Directional

|

4

Correct

|

66.7%

Accuracy

|

9

No Calls

|

Six directional calls this week, with four landing on the right side. The other nine markets got the NO CALL treatment. A 66.7% directional hit rate is respectable without being memorable, and the average confidence of 5.0 across those six calls tells you the desk was barely whispering its views. The highest conviction belonged to copper at 6/10, and it was the only call above minimum threshold. Every other directional commitment sat at 4/10 or 5/10, the analytical equivalent of mumbling into your sleeve.

The confidence calibration was clean in one respect: the highest-conviction call (HG at 6/10) was correct. The lowest-conviction call (CL at 4/10) missed. That is exactly how the distribution should work. But when five of your six directional calls sit at minimum conviction, you are not really making predictions so much as acknowledging that the markets exist and occasionally go up or down. The nine NO CALL markets included wheat's 6.59% eruption, soybeans' 4.36% rally, and gold's 1.61% decline. When your abstentions produce bigger moves than your commits, the framework is doing its job of preventing wrong calls at the cost of preventing any calls at all.

|

40/76

Correct / Total

|

52.6%

Accuracy

|

76 / 100

Directional / No Call

|

The rolling twelve-week figure sits at 52.6% across 76 directional calls, with 100 no-call abstentions. That engagement split means the desk calls direction on roughly 43% of market-weeks, a rate that has fallen from February's 70%+ pace to something closer to selective paralysis. The number has dipped below the 55% line for the first time in weeks, dragged by the April catastrophe and the persistent summer lull of minimum-conviction calls. This week's 66.7% helps modestly, but six calls in the denominator barely moves the needle. The desk needs to either increase its directional volume or accept that the rolling average will be hostage to whatever the last bad week was. At 52.6%, we are barely above the threshold where following the desk offers measurable advantage over a coin.

|

Bias Called

BULLISH

|

Confidence

6/10

|

Result

CORRECT

|

Grade

B+

|

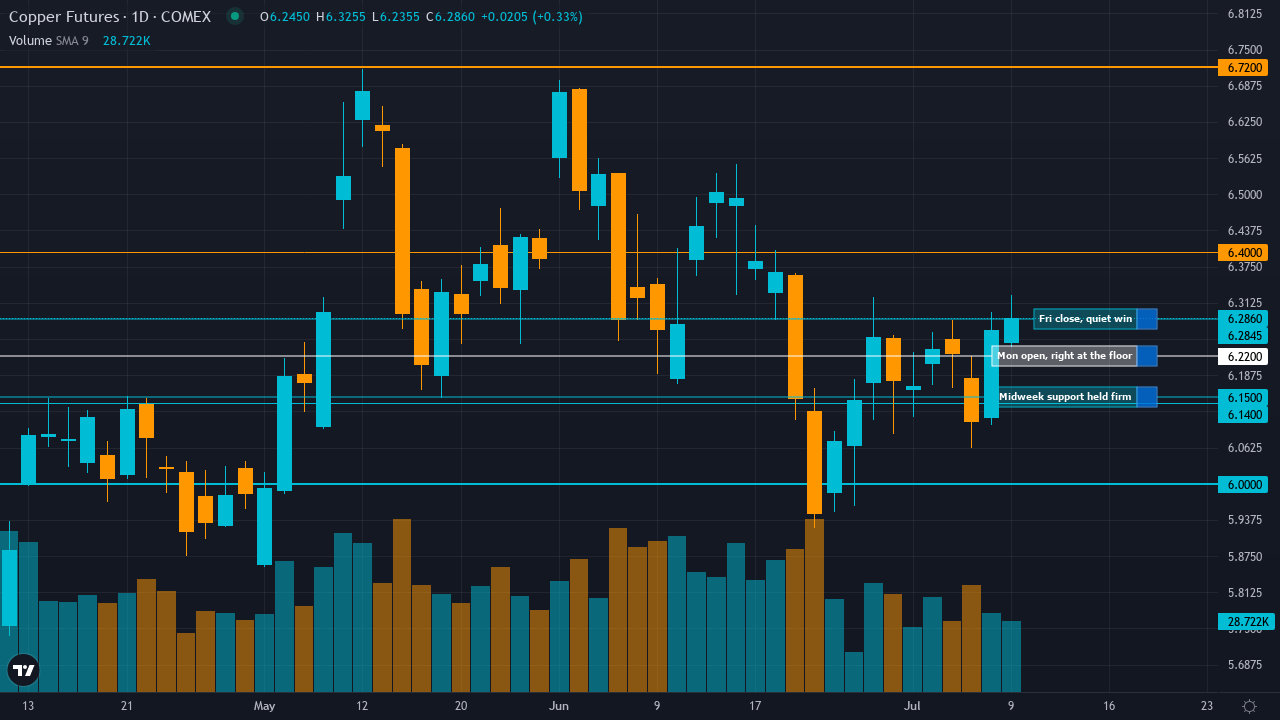

| Monday Open | 6.22 |

| Friday Close | 6.2845 |

| Move | 1.04 |

| ▼ R2 | 6.72 |

| ▼ R1 | 6.40 |

| ▲ S1 | 6.14 |

| ▲ S2 | 6.00 |

R1 at $6.40 was never tested, which given the 1.04% gain tells you this was a grind rather than a breakout. Copper opened Monday at $6.22 and spent the week consolidating in a tight range, with Trading Economics reporting prices held steady above $6.15 on Wednesday after BHP received environmental approval for its Chilean expansion. S1 at $6.14, the June breakdown low, provided an untested but visible floor throughout the week. Friday's close at $6.2845 settled comfortably above Monday's open but well below R1, suggesting the desk correctly identified the direction without overstating the magnitude. S2 at $6.00 was never in the conversation. The levels framework provided a clean bracket, but the action stayed in the lower third of the mapped range.

The called edge centred on the market fixating on tepid June 30 headline PMI at 50.3 while ignoring the high-tech equipment PMI surge to 53.5, which the desk argued validated underappreciated AI and data centre copper demand at a moment when Grasberg remained offline and China's sulfuric acid export ban continued constraining 15% of global mining capacity. That thesis proved directionally correct if not spectacular. Copper held its ground and edged higher through a week devoid of headline catalysts, suggesting the structural supply deficit provided a quiet floor. The desk's observation that available LME inventory (excluding warrants) was critically tight versus headline stocks appears to have provided the fundamental anchor that prevented any meaningful pullback.

Five of six disciplines pointed BULLISH, with only the Technical agent showing a mild bearish lean at -0.5 on sideways consolidation. The Fundamental agent carried the heaviest weight at 27% and drove the supply deficit thesis through Grasberg and sulfuric acid export ban analysis. This time, unlike the June MOTW debacle where I wrote the desk was 'chasing its own tail,' the Fundamental agent was not overridden. The Economic agent at 27% correctly read the China high-tech PMI at 53.5 as a demand validation signal. The Institutional agent at 21% read positioning at 71,974 contracts as moderate rather than crowded, supporting the bullish lean. The lone dissenter, the Technical agent, flagged mild bearish momentum from consolidation at the 50-day MA zone. Its caution turned out to be an overstatement but not entirely wrong, as the move was modest. When five disciplines agree and the market delivers a clean 1.04% gain, the synthesis framework earns its keep.

Copper returns as Market of the Week for the third time in recent months, and after June's double-MOTW saga that produced a BULLISH miss at 7/10 followed by a BEARISH miss at 5/10, this week's clean BULLISH win at 6/10 feels like a rehabilitation story.

The context matters. I wrote in my June 12 review that the desk was 'chasing its own tail' on copper, flipping from bullish to bearish on consecutive weeks and getting both wrong. The June 5 MOTW saw the desk call BULLISH at 7/10, the highest conviction on the board, and copper fell 2.59% as a semiconductor crash dragged industrial metals into the vortex. The following week, the desk panicked to BEARISH 5/10, and copper rallied 3.3%. Then came the mandatory miss reset that kept the desk on the sidelines for two consecutive weeks. This week, freshly emerged from reset purgatory with last week's NO CALL graded CORRECT, the desk re-engaged at a measured 6/10 conviction and got it right.

The week itself was unremarkable in the best possible sense. Copper opened at $6.22, held above $6.15 support throughout, and closed Friday at $6.2845 for a steady 1.04% gain. Trading Economics reported prices remained range-bound after BHP's Chilean expansion received environmental approval, a development that supports long-term supply but does nothing for near-term tightness. The Grasberg mine remains offline through Q2 2026, China's sulfuric acid export ban continues to affect 15% of global mining, and available LME inventory, the metric the desk has been banging the table about for weeks, remains critically tight.

The free MOTW report, published on the Ghost site Sunday evening, laid out the Grasberg supply thesis alongside the high-tech PMI observation that the desk identified as its key edge. The report noted that the market was overweighting the headline PMI at 50.3 and underweighting the high-tech equipment reading at 53.5, which the desk argued represented AI and data centre demand validation. Whether that specific thesis drove the 1.04% gain or whether copper simply caught a bid from general risk appetite is impossible to isolate. But direction was correct, the thesis was coherent, and the levels framework provided useful context.

The grade is B+ rather than A because the move was modest at 1.04%, the conviction was only 6/10 despite five-of-six discipline agreement, and the levels were not tested with the kind of precision that earns top marks. After the June copper disaster, a quiet correct call is exactly what the desk needed. Trust is rebuilt one honest result at a time, not through spectacular single-week heroics.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

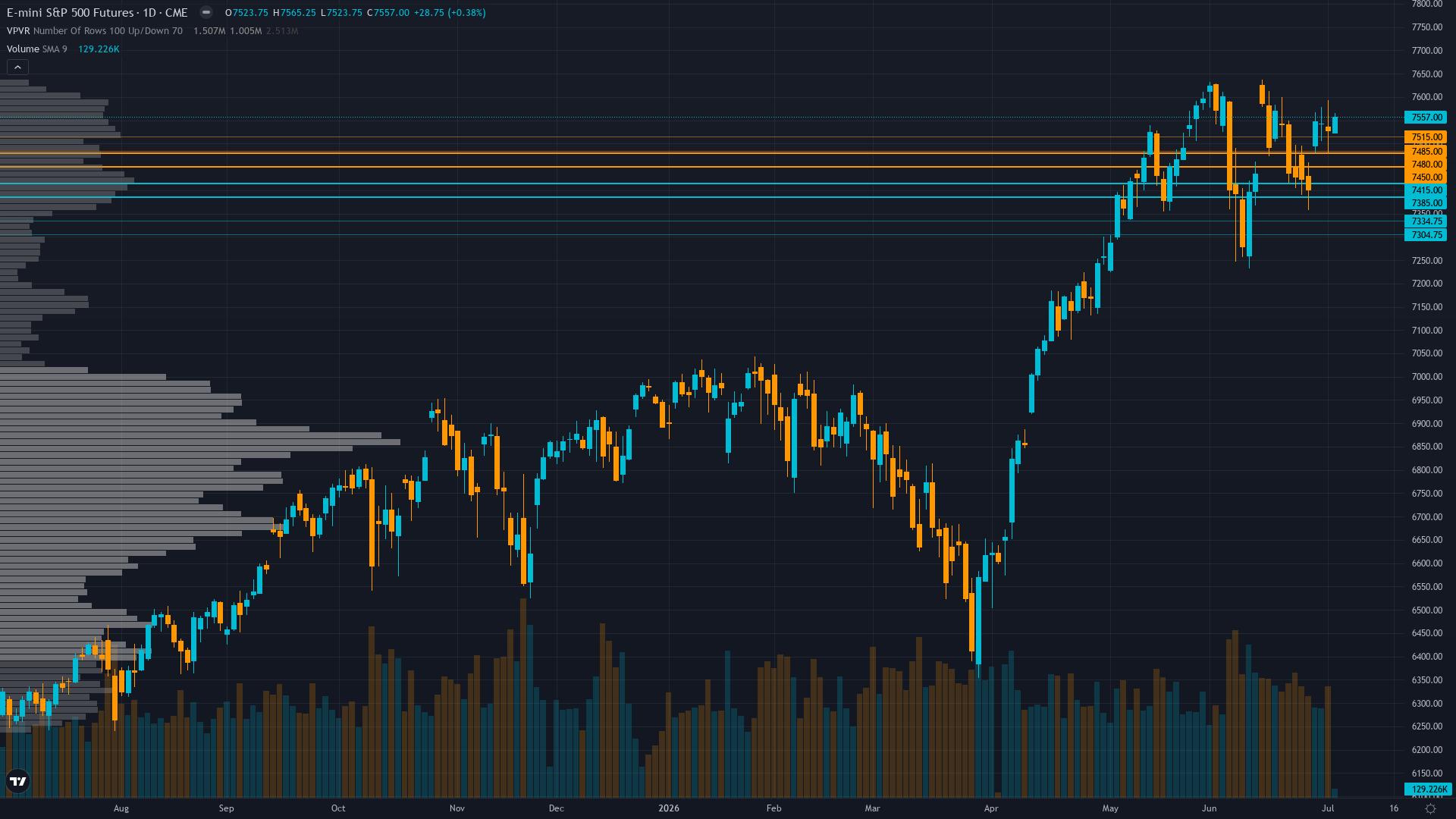

NO CALL | — | 7557 | 7621.75 | 0.86 | — | — |

| NO CALL at 5/10 and the S&P gained 0.86% to fresh highs above 7,600. Q2 earnings season kicked off and the market liked what it heard. A sub-1% move on a NO CALL is a clean abstention, though the desk's persistent equity agnosticism continues to cost it the chance to ride these grinding rallies. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 29901.75 | 30047 | 0.49 | — | — |

| NO CALL per mandatory miss reset after five consecutive misses, and the Nasdaq edged up 0.49%. For once, a week where sitting out NQ did not produce the kind of 3-5% move that makes me write angry paragraphs. A half-percent drift higher is precisely the nothing the desk predicted by saying nothing. Progress. | |||||||

|

Crude Oil

CORE

|

BEARISH | 4/10 | 68.86 | 71.55 | 3.91 | MISSED | D |

| BEARISH at the desk's lowest-ever directional conviction of 4/10, and crude rallied 3.91%. The geopolitical premium that everyone assumed was dead found a heartbeat as US-Iran Doha peace talks stalled. A nearly 4% miss in the wrong direction, even at minimal conviction. The worst call on the board. | |||||||

|

Gold

CORE

|

NO CALL | — | 4187.3 | 4119.9 | -1.61 | — | — |

| NO CALL per mandatory miss reset after nine consecutive missed calls. Gold dropped 1.61% to $4,120 as the metal continued its slow descent from January's $5,626 peak. Ten misses in a row triggered the reset that kept the desk neutral. A 1.61% decline scores as a miss by the framework, but the nine-miss purgatory protocol exists for exactly this reason. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1429 | 1.1445 | 0.14 | — | — |

| NO CALL for the eighteenth consecutive week. The euro drifted 14 pips. The desk and this pair have been in a committed non-relationship since March. At this point, I have written more words about their mutual indifference than the pair has moved in total. The ECB on July 23 might finally change the dynamic. Or it might not. I have stopped betting. | |||||||

|

Silver

EXTENDED

|

BEARISH | 5/10 | 62.4 | 60.15 | -3.6 | CORRECT | B+ |

| BEARISH at 5/10, recalibrated from last week's 7/10 miss, and silver dropped 3.6%. The July 10 CPI and stagflationary macro mix kept pressure on non-yielding metals. After the 6.14% bounce that broke the six-week bearish streak, the desk wisely reduced conviction and caught the resumption. Best call on the board. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.00624 | 0.006214 | -0.42 | — | — |

| NO CALL for the seventeenth consecutive week, the yen drifted 0.42%. Well within noise for this pair. The BOJ July 30 meeting approaches as the next binary catalyst. The desk's yen discipline, refusing to call direction in a pair dominated by intervention risk and rate differentials, remains its most sensible FX habit of 2026. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.3356 | 1.3398 | 0.31 | — | — |

| NO CALL for the seventeenth consecutive week, sterling gained 31 pips. Within noise for cable. The desk's prolonged silence on this pair, which I first documented in March, shows no sign of ending before the July 30 BoE meeting. At some point this streak qualifies for heritage protection status. | |||||||

|

Copper

EXTENDED

|

BULLISH | 6/10 | 6.22 | 6.2845 | 1.04 | CORRECT | B+ |

| This week's MOTW. BULLISH at 6/10 on the Grasberg supply deficit and high-tech PMI demand thesis, copper gained a steady 1.04%. After June's bruising double-miss saga, a clean, calm, correct result. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

Russell 2000

EXTENDED

|

NO CALL | — | 3023.5 | 2994.8 | -0.95 | — | — |

| NO CALL at 5/10 and the Russell slipped 0.95%, dipping back below the historic 3000 level it first breached in June. A sub-1% move on a NO CALL is a clean abstention. Post-reconstitution exhaustion and seasonal July weakness look to be asserting themselves exactly as the desk's own analysis suggested. | |||||||

|

AUD/USD

FULL DESK

|

BEARISH | 5/10 | 0.6939 | 0.6944 | 0.07 | MISSED | C |

| BEARISH at 5/10 and the Aussie gained 7 basis points. The market could not have been less interested in either the desk's bearish thesis or the bull case. A 0.07% move is the currency market equivalent of a shrug. Technically a miss, though calling it a miss feels generous to both sides. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | 112.2 | 111.28 | -0.82 | CORRECT | B |

| BEARISH at 5/10 and bonds fell 0.82%. The desk's most durable directional conviction of 2026 continues to deliver. After two consecutive misses in June when collapsing oil prices eased inflation fears, then last week's correct call, the bearish bond thesis under Warsh's regime appears to be reasserting itself. Direction right, modest move, minimum conviction. | |||||||

|

Wheat

FULL DESK

|

NO CALL | — | 599.75 | 639.25 | 6.59 | — | — |

| NO CALL at 5/10 on a 6.59% explosion. The July 10 WASDE apparently validated the worst US production shortfall since 1972, and wheat surged from 600 to 639 in five days. The desk sat on its hands behind a signal below the minimum threshold while the market delivered its largest weekly gain in months. The drought thesis the desk has been tracking since March just got its official stamp, and nobody at the desk had a ticket to the show. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | — | 1139.75 | 1189.5 | 4.36 | — | — |

| NO CALL at 5/10 on a 4.36% rally. Soybeans surged through the week, likely catching a tailwind from the same WASDE catalyst that powered wheat. The desk's signal below the minimum threshold kept it on the sidelines during a move the paid reports' renewable diesel demand thesis had been building toward for weeks. Another week of agricultural fireworks behind the NO CALL curtain. | |||||||

|

Platinum

FULL DESK

|

BEARISH | 5/10 | 1653.5 | 1636.6 | -1.02 | CORRECT | B |

| BEARISH at 5/10 and platinum fell 1.02%. After emerging from its mandatory miss reset with two consecutive correct NO CALL results, the desk re-engaged bearish and the metal obliged. The WPIC fundamental regime shift from extreme deficit to near-balance continues to weigh, and the technical breakdown thesis landed cleanly. Two correct calls in a row on platinum. Progress. | |||||||

|

✦ Best Call: Silver (SI)

BEARISH at 5/10 and silver dropped 3.6% from $62.40 to $60.15. After last week's spectacular 6.14% miss that snapped the six-week bearish winning streak, the desk recalibrated to minimum conviction and caught the resumption of selling pressure. The July 2 catastrophic NFP miss that drove last week's bounce appears to have been fully digested, with real yields above 2% and the July 10 CPI catalyst looming as the week's dominant force. The desk has been right on silver's direction for seven of the last eight calls. The one miss was the week the market staged its biggest bounce in months. Silver remains the desk's most reliable directional read of 2026, and at minimum conviction, the risk management was appropriate after last week's humbling. |

⚠️ Worst Call: Crude Oil (CL)

BEARISH at 4/10, the lowest conviction the desk has ever published on a directional call, and crude rallied 3.91% from $68.86 to $71.55. After eight consecutive bearish calls that delivered cumulative downside from $120 to sub-$70, the geopolitical premium found a pulse. US-Iran Doha peace talks hit turbulence during the week, and the market reminded everyone that with the Strait of Hormuz situation still technically unresolved, the final leg of crude's mean reversion is not guaranteed. The 4/10 conviction was the desk's way of saying 'I think it goes down but I do not trust this at all.' The market heard the second half of that sentence. At least the damage is contained by the whispered conviction. |

The Economic agent had a solid week, correctly driving bearish calls on silver, bonds, and platinum through its identification of the Warsh hawkish FOMC aftermath and elevated real yields as persistent headwinds for non-yielding assets. Its framework continues to be the desk's most useful analytical lens in the post-Warsh regime, where monetary policy dynamics dominate commodity and duration pricing.

The Fundamental agent earned real credit on the copper MOTW, where its Grasberg supply deficit thesis and high-tech PMI demand observation produced the correct BULLISH call. After months of being overridden on precious metals (correctly, as silver and gold kept falling), seeing the Fundamental agent drive a winning MOTW call feels like a small vindication. Its agricultural work remains a blind spot, however, as wheat's 6.59% explosion and soybeans' 4.36% surge both occurred on NO CALL markets where the Fundamental agent's drought and deficit theses sat behind locked doors. The Sentiment agent and Options agent contributed minimal signal across the board, which in a week of minimum-conviction calls is not surprising but also not helpful.

The June CPI dropped on July 10, landing right at the end of this grading window, and its implications will dominate next week's price action across gold, bonds, equities, and the entire rate-sensitive complex. The July 23 ECB meeting and July 28-29 FOMC loom as the month's defining events, with markets pricing genuine rate hike risk for the first time under Warsh's tenure. Wheat's 6.59% surge this week, driven by the July 10 WASDE that apparently validated the worst US production since 1972, may force the desk off the sidelines on agricultural markets for the first time in weeks. Q2 earnings season kicks off properly with major financials reporting, and whether the S&P's 0.86% quiet rally this week was the beginning of something or a pre-CPI holding pattern will become clear quickly. The desk will have its Sunday views. I expect the NO CALL count to remain stubbornly high through the summer lull.