Mon-T Weekly Review — w/e 1 May 2026

Three from four, the desk discovers that silence is sometimes a strategy and sometimes just silence, and crude oil reminds everyone the war is not over.

After last week's 12.5% catastrophe, the worst scorecard in MAD history, the desk did the only sensible thing: it folded nearly every hand on the table. Eleven of fifteen markets received the NO CALL treatment, leaving just four directional calls to carry the week. Three of those four landed on the right side. The S&P 500, this week's Market of the Week, was called BULLISH at 6/10 and gained 0.83% to set fresh closing records above 7254. Platinum was called BEARISH at 5/10 and fell 1.62%. Silver was called BEARISH at 5/10 and barely moved, slipping 0.11%. The lone miss was crude oil, called BEARISH at 5/10, which surged 7.3% as Iran-Hormuz negotiations stalled and the UAE announced its exit from OPEC.

The scorecard reads 75% directional accuracy, which looks respectable until you consider the context. The desk made four calls at an average confidence of 5.25, the analytical equivalent of mumbling your answer in an exam and hoping the teacher gives partial credit. Meanwhile, wheat rallied 3.2%, soybeans surged 2.28%, gold fell 2.48%, the yen strengthened 1%, sterling gained 0.79%, and the desk said nothing about any of it. Seven of those eleven NO CALL markets produced moves large enough to register as misses.

The FOMC meeting on April 28-29 held rates at 3.50-3.75% as expected, with CNBC reporting Powell indicated he would stay on the board after Trump's legal attacks left him 'no choice.' The S&P 500 and Nasdaq set new closing records on Friday per Investopedia, ending higher for a fifth consecutive week. Reuters confirmed April was Wall Street's best month in years. The desk caught the equity rally, missed the oil surge, and sat out everything else. Progress from last week? Absolutely. But the bar was underground.

|

15

Markets

|

4

Directional

|

3

Correct

|

75%

Accuracy

|

11

No Calls

|

Four directional calls this week, with three landing on the right side. The other eleven markets got the NO CALL treatment. A 75% directional hit rate recovers some dignity after last week's 12.5% debacle, though calling it a recovery is generous when the desk only committed on four markets at the lowest average confidence I have ever recorded. The single miss, crude oil at 5/10 BEARISH while WTI surged 7.3%, continues the pattern that has plagued the desk all year: every time the Iran conflict reignites, the bearish CL thesis gets torched. CNBC reported on April 28 that oil closed up nearly 3% on persistent Hormuz disruption, and The New York Times confirmed US gas prices hit their highest level since the beginning of the war in Iran. The desk went bearish at minimum conviction and the war had other plans. Again.

The NO CALL avalanche tells the real story. Eleven abstentions is a record, and while the procedural justifications are individually sound, including mandatory miss-streak resets on EUR/USD, NQ, GC, and ZW, collectively they paint a picture of a desk that has been so battered by recent misses it has retreated into analytical hibernation. When gold falls 2.48% and soybeans rally 2.28% and the yen strengthens 1% and the desk says nothing about any of it, the framework is doing its job of preventing wrong calls at the cost of preventing any calls at all.

|

64/106

Correct / Total

|

60.4%

Accuracy

|

106 / 74

Directional / No Call

|

The rolling twelve-week figure sits at 60.4% across 106 directional calls, with 74 no-call abstentions. That engagement rate tells you the desk is calling direction on roughly 59% of market-weeks, down from 70%+ in February. We have finally cracked through the 60% ceiling that has been the desk's home since the Iran conflict began, though only by a whisker. This week's 75% on four directional calls helps modestly, and some of the December-January horror shows are ageing out of the window. If the desk can increase its directional volume while maintaining accuracy above 65%, we will see the rolling number climb meaningfully. But four calls from fifteen markets is not sustainable engagement.

|

Bias Called

BULLISH

|

Confidence

6/10

|

Result

CORRECT

|

Grade

B+

|

| Monday Open | 7194.75 |

| Friday Close | 7254.25 |

| Move | 0.83 |

| ▼ R2 | 7300 |

| ▼ R1 | 7200 |

| ▲ S1 | 7100 |

| ▲ S2 | 6979 |

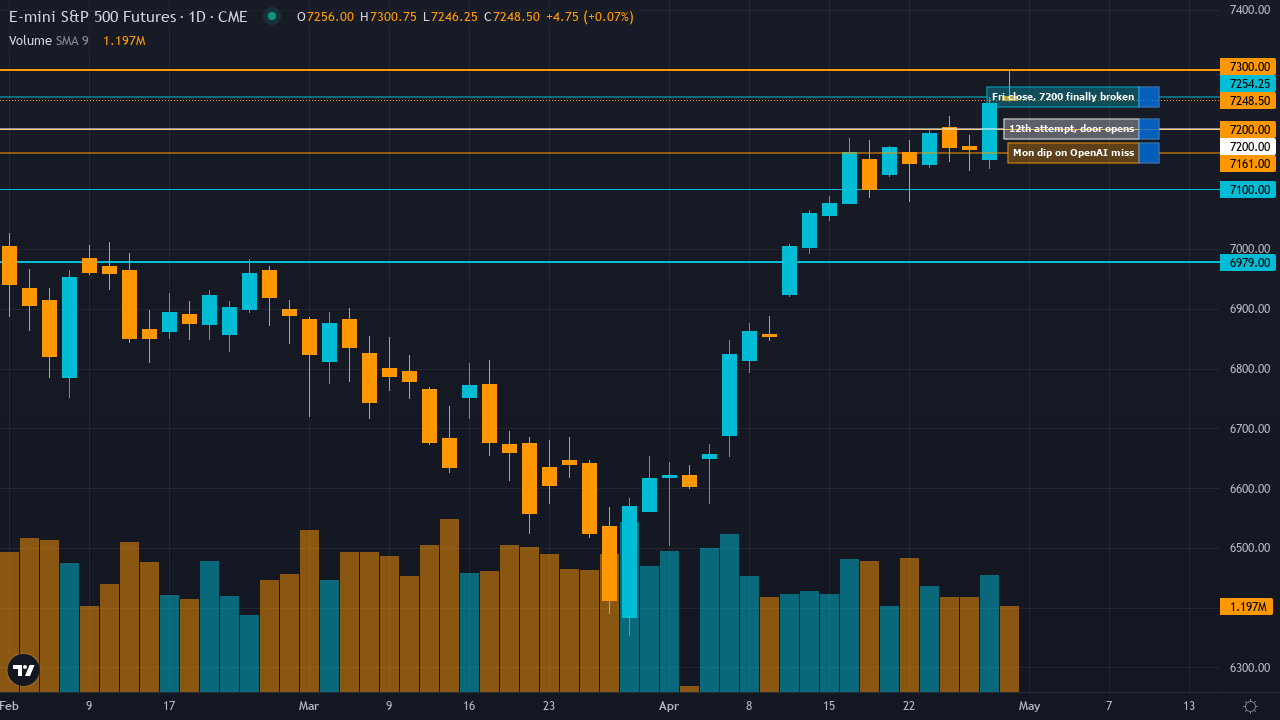

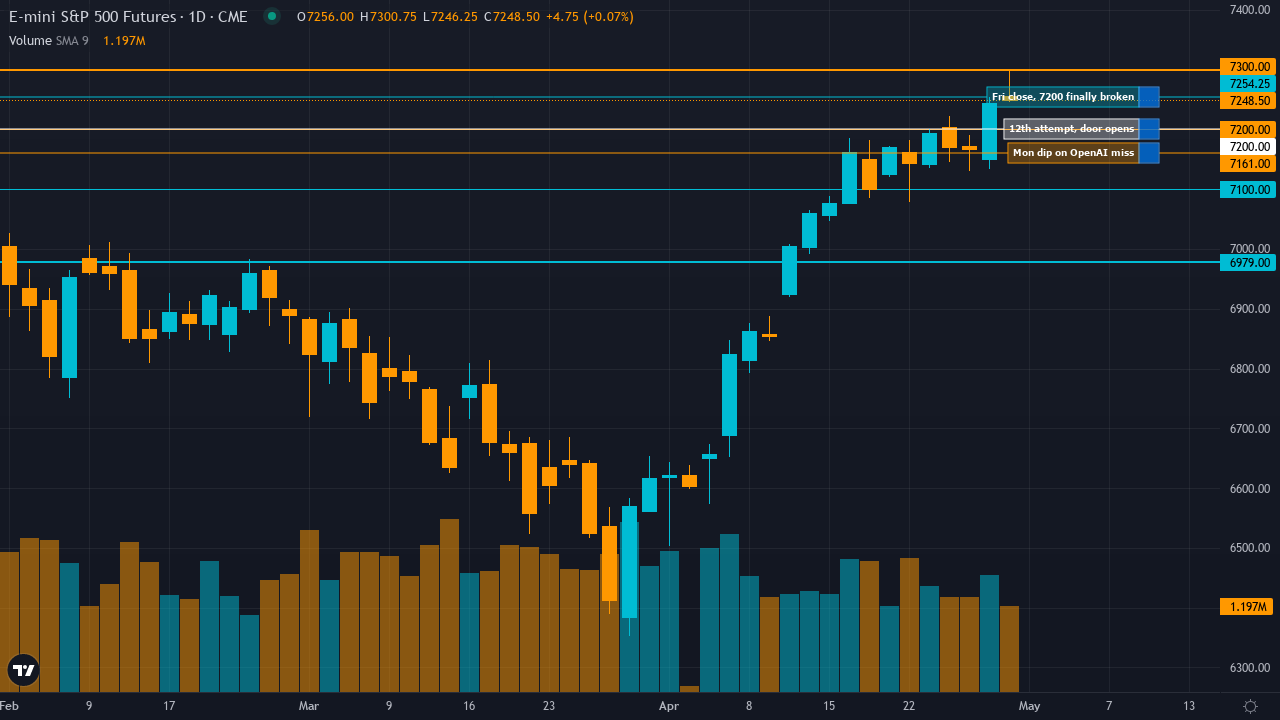

R1 at 7200 was the week's pivot point, and the market spent the first half of the week grappling with it. TheStreet reported on April 28 that the S&P 500 fell 0.46% on Monday as OpenAI's disappointing revenue report dragged tech lower, pulling ES back from the 7200 level. The FOMC decision on Wednesday, which held rates as expected, initially created a dip before the market absorbed the news. By Thursday, with Big Tech earnings providing support and Powell's press conference offering no hawkish surprises, ES pushed back above 7200 and held. Friday's close at 7254.25 settled comfortably above R1, with Investopedia confirming the S&P and Nasdaq set new closing records to end higher for a fifth straight week. S1 at 7100 was never seriously tested. S2 at 6979, the 50-day moving average zone, belonged to a different week entirely. R2 at 7300 was not reached, though the market is now gravitating toward it. The levels framework captured the battleground accurately, with R1 at 7200 serving as the inflection point between consolidation and breakout.

The called edge centred on the persistence of 7200 resistance after 11 failed breakout attempts, combined with Q1 earnings delivering a sixth consecutive quarter of 18.6% growth and the FOMC binary catalyst providing resolution rather than disruption. The desk argued the market was underestimating the probability of a clean breakout through 7200 if the FOMC delivered a benign hold, and that equity put/call at 0.51 extreme complacency was actually bullish in a RISK-ON regime rather than a contrarian warning. That thesis was broadly validated. The FOMC held rates as expected, Powell's tone was measured rather than hawkish, and the market used the clarity to push through 7200 for the first time on a sustained basis. Reuters confirmed the S&P ended higher on Friday, notching weekly gains after an earnings-heavy week. The 12th attempt to clear 7200 succeeded where the previous 11 had not.

All six discipline biases pointed BULLISH, a rare week of complete unanimity. The Sentiment agent at 25% weight flagged the transition from March extreme fear to current greed positioning, and while it carried a contrarian warning about equity put/call at 0.51, it ultimately confirmed the bullish lean rather than opposing it. The Technical agent at 20% correctly identified the uptrend above all major moving averages as confirmation of recovery rather than distribution. The Economic agent at 25% was the lone potential dissenter, flagging March CPI at 3.3% as a headwind, but it too concluded BULLISH on the strength of PMI data at 54.0 and the benign FOMC outcome. When the desk achieves this level of unanimity, direction tends to be correct. The conviction at 6/10 was appropriate for a week where the magnitude was always going to be modest given the FOMC landing where expected.

The S&P 500 returns as Market of the Week for the third time in 2026, and this time the story is not about crisis or recovery but something quieter and arguably more satisfying: a methodical breakout through resistance that had defeated the market eleven times before.

The week opened with ES at 7194.75, just 5 points below the 7200 psychological level that had acted as an impenetrable ceiling since January. TheStreet reported on Monday that the S&P fell 0.46% as OpenAI's revenue disappointment weighed on tech, and the Nasdaq dropped 1%. The FOMC meeting on Tuesday and Wednesday created the expected pre-event paralysis, with CNBC reporting on April 29 that the S&P began Wednesday's session little changed. The Fed held rates at 3.50-3.75% as every forecaster on the planet expected, with one interesting dissent: Stephen Miran voted for a 25bp cut while three others opposed the inclusion of an easing bias in the statement. Powell confirmed he would remain on the board, CNBC reporting his comments that Trump's legal attacks had 'left me no choice,' removing the governance uncertainty that had been a background concern.

With the FOMC safely in the rear-view mirror, Thursday and Friday saw the market push decisively through 7200 for the first time. Investopedia confirmed the S&P and Nasdaq set new closing records on Friday, ending higher for a fifth consecutive week. Trading Economics reported the US500 rose to 7264 on May 1. The desk's MOTW report, published free on the Ghost site on Sunday evening, called BULLISH at 6/10 with a specific focus on 7200 as the key resistance level. Readers who had that analysis before Monday's open were positioned for the breakout that arrived by week's end.

The grade is B+ rather than A because the 0.83% move, while correct in direction and significant in that it finally cleared the 7200 barrier, was modest in magnitude. The desk's own analysis acknowledged that the probable weekly move might approach the noise threshold, and 0.83% is just above that line. The levels framework earned its keep, with R1 at 7200 proving to be the exact inflection point. The thesis about Q1 earnings validation and FOMC clarity driving the breakout was sound. But the magnitude of the win does not match the quality of the A+ calls the desk has produced on ES in previous weeks, where 4.52% and 3.82% gains made the scorecard sing.

Still, after last week's one-from-eight disaster, a correct BULLISH call on the most widely followed equity index in the world, nailing the breakout through a level the desk specifically identified as the week's battleground, is exactly what subscribers need to see. The free MOTW report on the Ghost site laid out the thesis in full. Read it.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 6/10 | 7194.75 | 7254.25 | 0.83 | CORRECT | B+ |

| This week's MOTW. BULLISH at 6/10 and ES finally cleared the 7200 level it had failed to breach eleven times, closing at 7254.25 for new records. The FOMC held rates as expected, Powell stayed on the board, and the market used the clarity to break out. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 27435 | 27819.5 | 1.4 | — | — |

| NO CALL at 5/10 on a 1.4% rally to fresh records. Investopedia confirmed the Nasdaq set new closing highs alongside the S&P on Friday. The mandatory miss-streak reset after five consecutive misses kept the desk neutral. A 1.4% move is less painful than the 6.17% NQ rally the desk missed three weeks ago, but the pattern persists: the desk keeps sitting out the Nasdaq's relentless grind higher. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | 95.33 | 102.29 | 7.3 | MISSED | D |

| BEARISH at 5/10, crude surged 7.3% to $102.29. Reuters reported oil up nearly 3% on April 28 alone on Hormuz disruption, while the UAE announced its OPEC exit. The mean-reversion thesis keeps getting demolished by the simple fact that the Strait remains closed and negotiations are stalled. Two consecutive bearish misses. The worst directional call on the board. | |||||||

|

Gold

CORE

|

NO CALL | — | 4740.9 | 4623.3 | -2.48 | — | — |

| NO CALL at 5/10 on a 2.48% decline. Gold fell through the FOMC week as the hawkish hold and elevated real yields continued to pressure non-yielding assets. The desk's mandatory reset after two consecutive misses kept it neutral. A 2.48% move is the kind of thing the paid reports cover in detail, and the desk was procedurally right to abstain but practically absent. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1719 | 1.1745 | 0.22 | — | — |

| NO CALL at 5/10, the euro drifted 22 pips. The tenth consecutive NO CALL on EUR/USD. At this point the desk's euro agnosticism has become its own thesis: the pair refuses to move outside noise, and the desk refuses to call it. Both parties seem content. | |||||||

|

Silver

EXTENDED

|

BEARISH | 5/10 | 76 | 75.92 | -0.11 | CORRECT | C+ |

| BEARISH at 5/10, silver slipped 0.11%. Direction technically correct, but a move of 11 cents on a metal that routinely swings 5-7% in a week is the thinnest of wins. The desk's tactical flip from last week's BULLISH catastrophe at 7/10 to cautious BEARISH at minimum conviction was procedurally sound. The move was so small it barely qualifies as movement. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.0063255 | 0.006389 | 1 | — | — |

| NO CALL at 5/10 on a 1% yen move. The yen strengthened meaningfully during the week, likely driven by the BoJ meeting outcome falling on April 28. A 1% FX move on a NO CALL is a miss the desk will feel, especially as the paid reports covered the intervention risk thesis in detail. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.3467 | 1.3573 | 0.79 | — | — |

| NO CALL at 5/10, sterling gained 79 pips. Just above the noise threshold for cable, and the seventh consecutive NO CALL on 6B. The desk's caution ahead of the April 30 BoE meeting was understandable, but the result was another week of GBP moving without the desk in the room. | |||||||

|

Copper

EXTENDED

|

NO CALL | — | 6.03 | 5.9665 | -1.05 | — | — |

| NO CALL at 5/10 on a 1.05% decline. The ICSG surplus revision and China PMI confusion the desk flagged created genuine two-way uncertainty, and stepping aside while copper worked through conflicting signals was defensible. The desk's most reliable commodity call through February and March has been quiet for weeks now. | |||||||

|

Russell 2000

EXTENDED

|

NO CALL | — | 2798.8 | 2816.4 | 0.63 | — | — |

| NO CALL at 5/10 on a 0.63% gain. After four consecutive correct BULLISH calls totalling 14.4% cumulative gains, the mandatory bias review kicked in and forced the desk to the sidelines. The Russell drifted higher to consolidate at all-time highs. The desk's best active streak of 2026 was paused by procedure, not conviction. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | 0.7148 | 0.72 | 0.73 | — | — |

| NO CALL at 5/10, the Aussie gained 73 pips. The RBA-Fed policy divergence thesis that has been the desk's most reliable FX call remained valid, but the minimum signal threshold prevented commitment. The desk's four consecutive bullish streak was paused by the FX-specific noise threshold rules. | |||||||

|

30Y Treasury

FULL DESK

|

NO CALL | — | 114.09 | 113.125 | -0.85 | — | — |

| NO CALL at 5/10, bonds fell nearly a full point. The desk flagged the sub-Min-Signal environment and cross-discipline 3v3 conflict, and the market promptly moved almost a full handle lower. A 0.85% move through the FOMC is meaningful for Treasuries. The desk's long-running bearish bond thesis would have been correct yet again had it been active. | |||||||

|

Wheat

FULL DESK

|

NO CALL | — | 616.75 | 636.5 | 3.2 | — | — |

| NO CALL at 5/10 on a 3.2% rally. The mandatory miss-streak reset after three consecutive misses kept the desk neutral, and wheat surged again as the Southern Plains drought thesis the desk had acknowledged but refused to commit to proved correct once more. The desk's wheat record since March has been genuinely painful. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | — | 1174.75 | 1201.5 | 2.28 | — | — |

| NO CALL at 5/10 on a 2.28% rally. The signal below the minimum threshold prevented commitment, and soybeans rallied meaningfully through the week. The renewable diesel structural floor and improving export dynamics the paid reports covered in detail did their work without the desk positioned for it. | |||||||

|

Platinum

FULL DESK

|

BEARISH | 5/10 | 2030.4 | 1997.5 | -1.62 | CORRECT | B |

| BEARISH at 5/10, platinum fell 1.62% back below $2000. The technical breakdown thesis combined with hawkish FOMC rhetoric proved correct, though at minimum conviction the desk was barely whispering its view. After last week's BULLISH miss at 6/10, the tactical flip to bearish landed cleanly. The WPIC deficit thesis continues to lose the near-term argument against macro headwinds. | |||||||

|

✦ Best Call: S&P 500 (ES)

BULLISH at 6/10 and ES cleared 7200 for the first time, closing at 7254.25 for a 0.83% gain. In a week where the desk only made four directional calls, the MOTW gets best call honours because it correctly identified the FOMC catalyst as the key that would finally unlock the 7200 door. After last week's BEARISH miss on ES, the desk reversed direction and got rewarded. Eleven failed breakout attempts became twelve successful ones. The free report is on the Ghost site. |

⚠️ Worst Call: Crude Oil (CL)

BEARISH at 5/10, crude surged 7.3% from $95.33 to $102.29. Reuters reported oil closed up nearly 3% on April 28 alone as persistent Hormuz disruption outweighed the UAE's dramatic OPEC exit. The New York Times confirmed gas prices hit their highest level since the beginning of the Iran war, with negotiators deadlocked over proposals to reopen the Strait. I said last week that the desk had both a regime problem and a timing problem on crude. This week proved it. The mean-reversion thesis keeps running into the same wall: the war is not over, Hormuz remains effectively closed, and every time the desk calls bearish on oil, Iran finds a new way to prove the geopolitical premium is not exhausted. That is now two consecutive BEARISH misses on CL after the magnificent 14.78% win three weeks ago. |

In a week of just four directional calls, agent performance analysis is necessarily thin. The Sentiment agent continued its recent strong run, correctly supporting the BULLISH ES thesis through its identification of the fear-to-greed transition as a sustainable regime shift rather than a contrarian warning. Five of six disciplines agreed on BULLISH for ES, and the unanimity produced the correct result. The Economic agent's contributions to the precious metals NO CALL decisions were defensible, correctly identifying the FOMC as binary risk that warranted caution on gold, silver, and platinum ahead of the announcement.

The collective failure, once again, was on crude oil. The Fundamental agent's identification of IEA demand destruction data and structural oversupply continues to be technically correct about medium-term fundamentals while being spectacularly wrong about weekly price direction. I have been saying since March that the Fundamental agent needs a wartime macro override, and eleven weeks later the desk is still calling bearish on crude while Hormuz remains closed. The pattern is clear: structural supply-demand analysis is the desk's strongest discipline in peacetime and its weakest during active conflict. Until the Iran situation resolves, the desk should consider whether any bearish crude call at any conviction level can be justified.

May opens with the S&P at record highs, crude oil back above $102, and a wall of catalysts ahead. The May 6-7 FOMC is just days away, though with April's meeting freshly resolved, the focus shifts to incoming data rather than policy action. The May 8 USDA WASDE report will determine whether the Southern Plains drought that has been driving wheat higher gets official validation or proves to be market noise. Q1 earnings season continues with peak tech reporting, and whether the 19% growth rate holds will determine if the S&P's 7254 close was the start of something or a temporary ceiling. The Iran conflict remains the variable that keeps overriding every other thesis on the board, with OPEC dynamics now complicated further by the UAE's dramatic exit. The desk owes its subscribers more directional conviction after two weeks of minimal engagement. I will be watching to see whether the eleven NO CALLs decrease to a more actionable number.