S&P 500 (ES) — FOMC April 28-29 binary catalyst approaching with zero cut priced as VIX…

Cautiously bullish on Q1 earnings season strength and FOMC event uncertainty but aware 7,200 resistance remains formidable barrier with equity put/call 0.51 complacency creating asymmetric downside risk

Cautiously bullish on Q1 earnings season strength and FOMC event uncertainty but aware 7,200 resistance remains formidable barrier with equity put/call 0.51 complacency creating asymmetric downside risk

FOMC April 28-29 binary catalyst approaching with zero cut priced as VIX compresses to 18.7 from March 31.05 extreme creating calm surface while Q1 earnings season 28% complete delivers sixth consecutive quarter 18.6% growth validating stretched multiples

Sentiment regime shift from March extreme fear (VIX 31.05, AAII -17.7% spread) to current greed (Fear & Greed 70, AAII bulls 46%) creates wall-of-worry setup but equity put/call 0.51 extremely low showing dangerous complacency developing

Technical momentum strong with ES at 7,194.75 above all major MAs testing 7,200 psychological resistance but 20-day historical volatility compressed to 14.6% (very low category) suggesting range-bound action absent catalyst

| ▼ Resistance Zone 2 | 7275 – 7325 |

| ▼ Resistance Zone 1 | 7175 – 7225 |

| ─ Pivot Area | ~7195 |

| ▲ Support Zone 1 | 7075 – 7125 |

| ▲ Support Zone 2 | 6954 – 7004 |

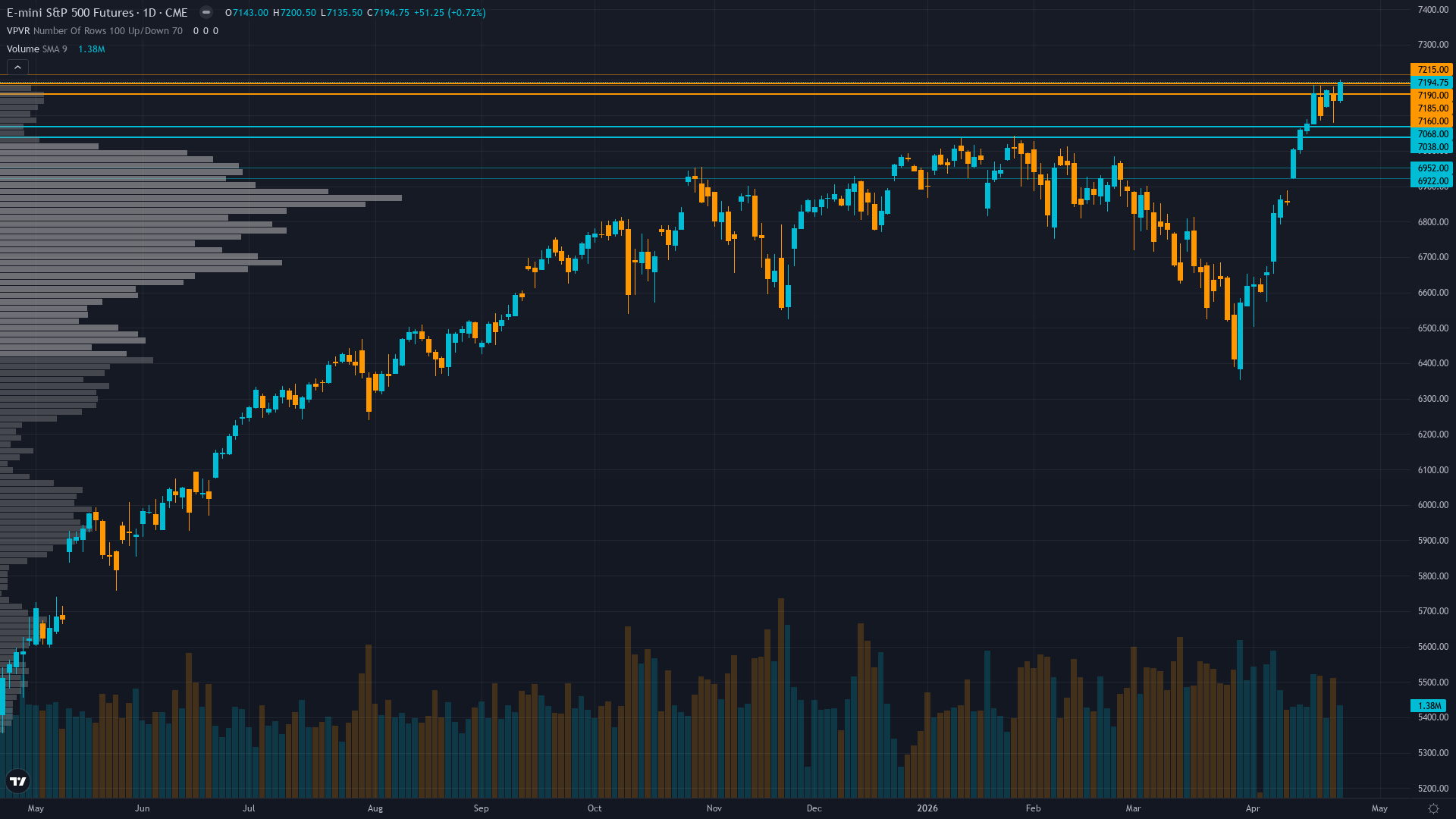

ES at 7,194.75 testing 7,200 resistance with RSI 68.62 elevated but not overbought, above 50-day MA 6,979 and 200-day MA 6,705 confirming bullish structure yet momentum waning after testing intraday high 7,200.50

Forward PE 20.9x at 5% premium to 5-year average justified by Q1 earnings season delivering 18.6% growth with +60bp upward revision this week and record 14.2% net margins creating execution tailwind if companies deliver

Constructive with QQQ adding $3B and Large Cap Growth ETFs $3.8B inflows but month-end April 30 rebalancing risk 4 days away creating potential mechanical selling pressure as equity allocations drift above targets

VIX compressed to 18.7 down from 19.5 showing fear unwinding but equity put/call 0.51 represents approximately 2 calls per put indicating extreme bullish positioning with minimal hedging creating asymmetric reversal vulnerability

Fed at 3.50-3.75% after January hawkish hold with April 28-29 FOMC pricing 100% hold probability, PMI strong at second-highest reading in 3 years, but policy paralysis persists as JPMorgan raises S&P 500 target to 7,600 on AI earnings cycle

Normal contango - VIX spot 18.7 versus futures at higher levels showing near-term calm priced with modest fear premium for April 29 FOMC event risk creating slight elevation versus longer-dated expectations

VIX compression from geopolitical/sentiment spikes above 30 typically normalizes 50-60% of peak-to-trough move within 20-30 days before stabilizing - current pattern at day 26 with 40% compression suggests final normalization phase entering consolidation before next catalyst

VIX compression from March 31.05 extreme to current 18.7 suggests continued normalization toward 17-18 range over next 3-5 trading days with 60% probability as FOMC approaches, though April 29 event presents binary re-expansion risk above 22 on hawkish surprise

Normal volatility regime suggests 1.0-1.5% daily ES moves expected with current 7,100-7,200 consolidation representing 1.4% range - FOMC binary outcome April 29 presents asymmetric expansion risk with potential 2-3% intraday swings on Powell rhetoric surprise either direction

Contracting VIX from March extreme creates balanced but asymmetric setup - potential 3-4% downside to 6,950-7,000 zone if FOMC hawkish surprise and month-end selling intensifies VIX re-expansion above 22 versus 4-6% upside to 7,450-7,500 if dovish Powell pivot and Q1 earnings validate multiples enabling VIX compression below 17, but extreme starting complacency at equity put/call 0.51 and 7,200 resistance failure history suggests consolidation-to-modest-upside scenario dominates with 55% probability over next 5-7 days

|

⚠️ Primary Risk

FOMC April 29 delivers hawkish hold reinforcing December one-cut 2026 guidance creating multiple compression risk from forward PE 20.9x elevated levels while month-end rebalancing selling amplifies downside testing 7,100 then 6,979 support Probability: MEDIUM

|

✦ Primary Opportunity

Q1 earnings season continuation validates 18.6% growth expectations with mega-cap tech delivering strong guidance enabling breakout above 7,200 toward 7,300-7,400 resistance as VIX compression below 18 and April-May seasonal strength materializes Timeframe: April 29 - May 15 2026

|

ES trades at 7,194.75 on April 26, 2026 at 07:30 UTC, consolidating just below the psychologically critical 7,200 level after a remarkable recovery from March's extreme fear capitulation. MACRO REGIME CLASSIFICATION: RISK-ON with maturing characteristics. VIX at 18.7 sits comfortably below the 20 threshold, equity indices trending up decisively above all major moving averages, credit conditions stable with HY spreads at 3.07%, and Fear & Greed Index at 70 (greed territory). This represents clear RISK-ON conditions, yet the regime shows signs of maturity with extreme positioning metrics (equity put/call 0.51, AAII bulls 46% first time above historical average in 10 weeks) suggesting late-cycle fragility.

Post-input development identified: VIX compressed further to 18.7 from discipline data's 19.5 reading, and ES tested 7,200.50 intraday high today confirming continued upward momentum despite my April 24 BEARISH call being MISSED. The current price at 7,194.75 sits just 5.75 points below that resistance, representing only 0.08% headroom before psychological breakout. My last graded call on April 24 was BEARISH at conviction 6 with signal -1.5, anticipating mean-reversion from RSI 78.56 extreme overbought.

That call delivered MISSED result as price rose from Monday 7159 to Friday 7193.5 (+0.48%), marking my first MISSED call after the prior week's CORRECT BULLISH call that captured the violent +4.52% relief rally. Current miss streak: 1. Bias streak: 1 week BEARISH (last week only). The March extreme fear washout (VIX 31.05, AAII bears 51.4%, RSI 22.08) has fully reversed into current greed conditions creating profound sentiment mean-reversion: VIX compressed 40% from peak to current 18.7, Fear & Greed flipped from 15 (extreme fear) to 70 (greed), and AAII bull-bear spread swung from -17.7% to +11.6% representing 29-point reversal in just 4 weeks.

Yet this rapid sentiment shift from fear to greed creates asymmetric setup where complacency develops faster than fundamentals justify. The fundamental catalyst supporting current levels is genuine: Q1 2026 earnings season now 28% complete delivers sixth consecutive quarter of double-digit growth at 18.6% YoY rate with FactSet reporting +60bp upward revision between April 17-24. Net profit margins at record 14.2% levels validate forward PE 20.9x as justified rather than excessive, yet this creates execution risk where any guidance disappointment triggers multiple compression.

Technical structure shows ES holding above 50-day MA at 6,979 (+3.1%) and 200-day MA at 6,705 (+7.3%) with both positively sloped confirming bullish trend intact. However, RSI recovered from April 19's extreme 78.56 overbought to current 68.62 suggesting momentum cooling without yet reaching neutral. The index tested 7,200.50 intraday high today representing 11th attempt to sustain breakout above this psychological level since January 11's 7,005 test - each prior attempt failed creating overhead supply at round-number resistance.

Volatility intelligence reveals critical regime transition: 20-day historical volatility compressed to 14.6% (very low category per search results), 60-day at 12.71%, suggesting range-bound price action despite directional trend. This compression occurs while VIX sits at 18.7, creating disconnect where implied volatility exceeds realized volatility by approximately 4 percentage points - historically this gap closes either through VIX compression toward 15 validating calm conditions, or realized volatility expansion through 2-3% daily swings testing the calm assumption.

The binary catalyst arrives in 3 days: April 28-29 FOMC meeting prices 100% hold probability with Powell press conference April 29 at 2:30pm ET. Markets scrutinize rhetoric for any softening from January's hawkish hold that followed December's shock one-cut 2026 guidance. Any dovish surprise triggers rally toward 7,300-7,400 resistance, while sustained hawkishness validates multiple compression risk testing 7,100 support. Month-end calendar effect adds complexity: April 30 arrives in 4 days creating mechanical rebalancing pressure as pension funds trim equity allocations back to target levels after strong YTD performance.

This typically creates 0.5-1.0% selling pressure in final 2 trading days of month, partially offset by May 1 window-opening for corporate buybacks post-earnings blackout. My directional bias shifts BULLISH with measured conviction recognizing: (1) intact uptrend structure above all major MAs, (2) Q1 earnings season delivering sixth consecutive quarter 18.6% growth with upward revisions, (3) VIX compression to 18.7 showing fear premium unwinding, (4) FOMC binary catalyst 3 days away creating asymmetric opportunity if Powell softens restrictive rhetoric, (5) April-May seasonal strength historically averaging +2.8% combined.

However, conviction capped at 6/10 acknowledging: (1) last call MISSED requiring caution, (2) equity put/call 0.51 extreme complacency creates reversal vulnerability, (3) 7,200 resistance unbreached despite 11 attempts, (4) month-end rebalancing selling pressure imminent, (5) 20-day historical volatility at 14.6% very low category suggests probable weekly move may approach noise threshold. Applying ES parameters: Average Weekly Move 1.18%, Noise Floor 0.75%, Min Signal 1.0. The probable weekly move given current VIX 18.7 regime and FOMC catalyst significantly exceeds noise threshold with 1.5-2.5% swing plausible on Powell rhetoric.

My signal +1.5 exceeds Min Signal 1.0 threshold justifying BULLISH directional bias. FOMC meeting qualifies as major catalyst permitting Max Conf (catalyst) 8, though I set conviction at 6 recognizing miss streak penalty and extreme positioning creating structural reversal risk. Devil's advocate: The equity put/call 0.51 extreme complacency, 7,200 resistance failure across 11 attempts, RSI 68.62 approaching overbought, and month-end mechanical selling pressure combined with Fed policy paralysis at 3.50-3.75% suggest consolidation or pullback toward 7,100-7,000 support remains higher probability path than breakout, particularly if April 29 FOMC reinforces restrictive stance disappointing greed-positioned bulls.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| April 24, 2026 | BEARISH | 6/10 | ❌ |

| April 17, 2026 | BULLISH | 7/10 | ✅ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | BEARISH | 3/10 | ❌ |

| March 27, 2026 | BEARISH | 3/10 | ✅ |

| March 20, 2026 | BEARISH | 4/10 | ✅ |

| March 14, 2026 | BEARISH | 6/10 | ✅ |

| March 6, 2026 | NO CALL | 5/10 | ➖ |

| February 27, 2026 | NO CALL | 6/10 | ➖ |

| February 21, 2026 | NO CALL | 5/10 | ➖ |

| February 13, 2026 | NO CALL | 5/10 | ➖ |

| February 8, 2026 | BULLISH | 6/10 | ✅ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: S&P 500 (ES) Report Date: April 26, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 6/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 42 (SLIGHT DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: TRENDING UP Sentiment: GREED ── WHAT THE MARKET SEES ───────────────────────── Cautiously bullish on Q1 earnings season strength and FOMC event uncertainty but aware 7,200 resistance remains formidable barrier with equity put/call 0.51 complacency creating asymmetric downside risk ── WHAT THE MARKET IS MISSING ─────────────────── Market underestimating persistence of 7,200 resistance after 11 failed breakout attempts since January while overestimating FOMC dovish surprise probability given Fed policy paralysis at 3.50-3.75% and December one-cut guidance unchanged - complacent positioning at equity put/call 0.51 creates structural vulnerability to hawkish rhetoric confirmation ── KEY DRIVERS ────────────────────────────────── 1. FOMC April 28-29 binary catalyst approaching with zero cut priced as VIX compresses to 18.7 from March 31.05 extreme creating calm surface while Q1 earnings season 28% complete delivers sixth consecutive quarter 18.6% growth validating stretched multiples 2. Sentiment regime shift from March extreme fear (VIX 31.05, AAII -17.7% spread) to current greed (Fear & Greed 70, AAII bulls 46%) creates wall-of-worry setup but equity put/call 0.51 extremely low showing dangerous complacency developing 3. Technical momentum strong with ES at 7,194.75 above all major MAs testing 7,200 psychological resistance but 20-day historical volatility compressed to 14.6% (very low category) suggesting range-bound action absent catalyst ── KEY ZONES ──────────────────────────────────── Resistance 2: 7275 – 7325 Resistance 1: 7175 – 7225 Pivot: ~7195 Support 1: 7075 – 7125 Support 2: 6954 – 7004 ── DISCIPLINE BIASES ──────────────────────────── Technical: BULLISH Fundamental: BULLISH Institutional: BULLISH Options: BULLISH Economic: BULLISH Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── ES at 7,194.75 testing 7,200 resistance with RSI 68.62 elevated but not overbought, above 50-day MA 6,979 and 200-day MA 6,705 confirming bullish structure yet momentum waning after testing intraday high 7,200.50 ── FUNDAMENTAL ASSESSMENT ─────────────────────── Forward PE 20.9x at 5% premium to 5-year average justified by Q1 earnings season delivering 18.6% growth with +60bp upward revision this week and record 14.2% net margins creating execution tailwind if companies deliver ── INSTITUTIONAL POSITIONING ──────────────────── Constructive with QQQ adding $3B and Large Cap Growth ETFs $3.8B inflows but month-end April 30 rebalancing risk 4 days away creating potential mechanical selling pressure as equity allocations drift above targets ── OPTIONS FLOW ───────────────────────────────── VIX compressed to 18.7 down from 19.5 showing fear unwinding but equity put/call 0.51 represents approximately 2 calls per put indicating extreme bullish positioning with minimal hedging creating asymmetric reversal vulnerability ── ECONOMIC BACKDROP ──────────────────────────── Fed at 3.50-3.75% after January hawkish hold with April 28-29 FOMC pricing 100% hold probability, PMI strong at second-highest reading in 3 years, but policy paralysis persists as JPMorgan raises S&P 500 target to 7,600 on AI earnings cycle ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 45th Trend: Contracting ▼ Days in Regime: 8 Term Structure: Normal contango - VIX spot 18.7 versus futures at higher levels showing near-term calm priced with modest fear premium for April 29 FOMC event risk creating slight elevation versus longer-dated expectations Historical Pattern: VIX compression from geopolitical/sentiment spikes above 30 typically normalizes 50-60% of peak-to-trough move within 20-30 days before stabilizing - current pattern at day 26 with 40% compression suggests final normalization phase entering consolidation before next catalyst Outlook: VIX compression from March 31.05 extreme to current 18.7 suggests continued normalization toward 17-18 range over next 3-5 trading days with 60% probability as FOMC approaches, though April 29 event presents binary re-expansion risk above 22 on hawkish surprise Trading Context: Normal volatility regime suggests 1.0-1.5% daily ES moves expected with current 7,100-7,200 consolidation representing 1.4% range - FOMC binary outcome April 29 presents asymmetric expansion risk with potential 2-3% intraday swings on Powell rhetoric surprise either direction Vol Risk/Opportunity: Contracting VIX from March extreme creates balanced but asymmetric setup - potential 3-4% downside to 6,950-7,000 zone if FOMC hawkish surprise and month-end selling intensifies VIX re-expansion above 22 versus 4-6% upside to 7,450-7,500 if dovish Powell pivot and Q1 earnings validate multiples enabling VIX compression below 17, but extreme starting complacency at equity put/call 0.51 and 7,200 resistance failure history suggests consolidation-to-modest-upside scenario dominates with 55% probability over next 5-7 days ── PRIMARY RISK ───────────────────────────────── FOMC April 29 delivers hawkish hold reinforcing December one-cut 2026 guidance creating multiple compression risk from forward PE 20.9x elevated levels while month-end rebalancing selling amplifies downside testing 7,100 then 6,979 support Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Q1 earnings season continuation validates 18.6% growth expectations with mega-cap tech delivering strong guidance enabling breakout above 7,200 toward 7,300-7,400 resistance as VIX compression below 18 and April-May seasonal strength materializes Timeframe: April 29 - May 15 2026 ── NEXT CATALYST ──────────────────────────────── Date: April 29, 2026 Event: FOMC two-day meeting April 28-29 with Powell press conference at 2:30pm ET, markets price 100% hold probability but scrutinizing rhetoric for any softening of restrictive stance amid Q1 earnings strength and labor market stability Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ES trades at 7,194.75 on April 26, 2026 at 07:30 UTC, consolidating just below the psychologically critical 7,200 level after a remarkable recovery from March's extreme fear capitulation. MACRO REGIME CLASSIFICATION: RISK-ON with maturing characteristics. VIX at 18.7 sits comfortably below the 20 threshold, equity indices trending up decisively above all major moving averages, credit conditions stable with HY spreads at 3.07%, and Fear & Greed Index at 70 (greed territory). This represents clear RISK-ON conditions, yet the regime shows signs of maturity with extreme positioning metrics (equity put/call 0.51, AAII bulls 46% first time above historical average in 10 weeks) suggesting late-cycle fragility. Post-input development identified: VIX compressed further to 18.7 from discipline data's 19.5 reading, and ES tested 7,200.50 intraday high today confirming continued upward momentum despite my April 24 BEARISH call being MISSED. The current price at 7,194.75 sits just 5.75 points below that resistance, representing only 0.08% headroom before psychological breakout. My last graded call on April 24 was BEARISH at conviction 6 with signal -1.5, anticipating mean-reversion from RSI 78.56 extreme overbought. That call delivered MISSED result as price rose from Monday 7159 to Friday 7193.5 (+0.48%), marking my first MISSED call after the prior week's CORRECT BULLISH call that captured the violent +4.52% relief rally. Current miss streak: 1. Bias streak: 1 week BEARISH (last week only). The March extreme fear washout (VIX 31.05, AAII bears 51.4%, RSI 22.08) has fully reversed into current greed conditions creating profound sentiment mean-reversion: VIX compressed 40% from peak to current 18.7, Fear & Greed flipped from 15 (extreme fear) to 70 (greed), and AAII bull-bear spread swung from -17.7% to +11.6% representing 29-point reversal in just 4 weeks. Yet this rapid sentiment shift from fear to greed creates asymmetric setup where complacency develops faster than fundamentals justify. The fundamental catalyst supporting current levels is genuine: Q1 2026 earnings season now 28% complete delivers sixth consecutive quarter of double-digit growth at 18.6% YoY rate with FactSet reporting +60bp upward revision between April 17-24. Net profit margins at record 14.2% levels validate forward PE 20.9x as justified rather than excessive, yet this creates execution risk where any guidance disappointment triggers multiple compression. Technical structure shows ES holding above 50-day MA at 6,979 (+3.1%) and 200-day MA at 6,705 (+7.3%) with both positively sloped confirming bullish trend intact. However, RSI recovered from April 19's extreme 78.56 overbought to current 68.62 suggesting momentum cooling without yet reaching neutral. The index tested 7,200.50 intraday high today representing 11th attempt to sustain breakout above this psychological level since January 11's 7,005 test - each prior attempt failed creating overhead supply at round-number resistance. Volatility intelligence reveals critical regime transition: 20-day historical volatility compressed to 14.6% (very low category per search results), 60-day at 12.71%, suggesting range-bound price action despite directional trend. This compression occurs while VIX sits at 18.7, creating disconnect where implied volatility exceeds realized volatility by approximately 4 percentage points - historically this gap closes either through VIX compression toward 15 validating calm conditions, or realized volatility expansion through 2-3% daily swings testing the calm assumption. The binary catalyst arrives in 3 days: April 28-29 FOMC meeting prices 100% hold probability with Powell press conference April 29 at 2:30pm ET. Markets scrutinize rhetoric for any softening from January's hawkish hold that followed December's shock one-cut 2026 guidance. Any dovish surprise triggers rally toward 7,300-7,400 resistance, while sustained hawkishness validates multiple compression risk testing 7,100 support. Month-end calendar effect adds complexity: April 30 arrives in 4 days creating mechanical rebalancing pressure as pension funds trim equity allocations back to target levels after strong YTD performance. This typically creates 0.5-1.0% selling pressure in final 2 trading days of month, partially offset by May 1 window-opening for corporate buybacks post-earnings blackout. My directional bias shifts BULLISH with measured conviction recognizing: (1) intact uptrend structure above all major MAs, (2) Q1 earnings season delivering sixth consecutive quarter 18.6% growth with upward revisions, (3) VIX compression to 18.7 showing fear premium unwinding, (4) FOMC binary catalyst 3 days away creating asymmetric opportunity if Powell softens restrictive rhetoric, (5) April-May seasonal strength historically averaging +2.8% combined. However, conviction capped at 6/10 acknowledging: (1) last call MISSED requiring caution, (2) equity put/call 0.51 extreme complacency creates reversal vulnerability, (3) 7,200 resistance unbreached despite 11 attempts, (4) month-end rebalancing selling pressure imminent, (5) 20-day historical volatility at 14.6% very low category suggests probable weekly move may approach noise threshold. Applying ES parameters: Average Weekly Move 1.18%, Noise Floor 0.75%, Min Signal 1.0. The probable weekly move given current VIX 18.7 regime and FOMC catalyst significantly exceeds noise threshold with 1.5-2.5% swing plausible on Powell rhetoric. My signal +1.5 exceeds Min Signal 1.0 threshold justifying BULLISH directional bias. FOMC meeting qualifies as major catalyst permitting Max Conf (catalyst) 8, though I set conviction at 6 recognizing miss streak penalty and extreme positioning creating structural reversal risk. Devil's advocate: The equity put/call 0.51 extreme complacency, 7,200 resistance failure across 11 attempts, RSI 68.62 approaching overbought, and month-end mechanical selling pressure combined with Fed policy paralysis at 3.50-3.75% suggest consolidation or pullback toward 7,100-7,000 support remains higher probability path than breakout, particularly if April 29 FOMC reinforces restrictive stance disappointing greed-positioned bulls.