GBP/USD Forecast This Week — Outlook, Drivers & Key Levels

This week's GBP/USD outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

This Week's Starting Point

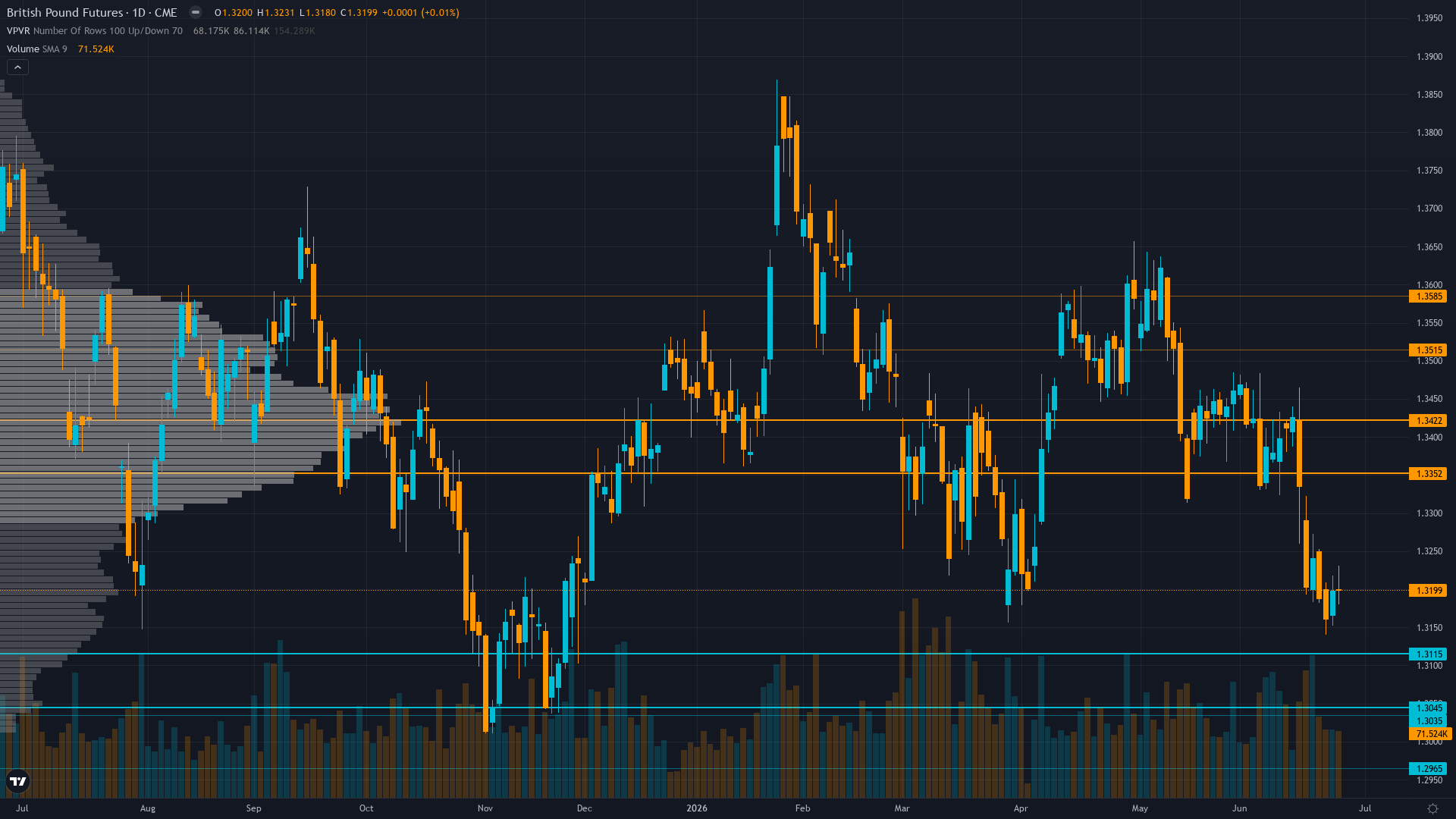

Trading at 1.32 with a 0.10% uptick, GBP/USD is drifting higher without strong conviction. Price action in cable has compressed into a consolidation pattern, typically a precursor to a directional breakout.

Neutral consolidation expected with defensive positioning as markets digest dual central bank outcomes from 11 days ago with Fed June 17 hawkish pivot and BoE June 18 hold at 3.75% on 7-2 vote showing increased hawkish dissent, rate differential at parity eliminating carry advantage while 32-day gap to next catalysts creates low-information-edge environment

Forces in Play

Primary driver: SIXTEENTH consecutive week of NO CALL bias maintaining disciplined noise-threshold stance as 6B consolidates at 1.32 in extended 32-day pre-catalyst window ahead of July 30 BoE meeting following dual central bank outcomes now 11 days past and fully priced

Secondary factor: Post-input development confirmed via mandatory news scan: BoE June 18 held 3.75% on 7-2 vote (versus prior 8-1) with two members voting for hike to 4.0%, increased hawkish dissent NOT fully reflected in discipline inputs suggesting market still digesting policy trajectory uncertainty

Additional influence: FX_MAJOR 0.50% noise floor with probable weekly move uncertain in post-dual-central-bank consolidation phase as Fed June 17 hawkish pivot and BoE June 18 hold create rate differential parity (both 3.75%) eliminating prior Sterling carry advantage while Technical RSI 33.99 oversold creates mean-reversion bounce risk

Economic backdrop: MACRO REGIME: TRANSITIONAL with VIX at 16.41 below 20 threshold indicating calm risk appetite but Fear & Greed at 25 (Fear territory) showing cautious undertones, Fed June 17 removed dovish bias signaling possible hikes while BoE June 18 held 3.75% on 7-2 vote (increased dissent from prior 8-1), rate differential at parity creates no structural advantage for Sterling

Fundamental assessment: GBP materially overvalued at 1.32 versus PPP ~1.12, UK current account deficit 1.1% GDP with fiscal deficit deteriorating (PSNFL 84.7%), rate differential eliminated at parity (BoE 3.75%, Fed 3.75%) removing carry support pillar that previously sustained Sterling

Technical Landscape

Downtrend confirmed with price at 1.32 below 50-day MA at 1.3376, all 12 moving averages in sell mode, RSI 33.99 oversold creating acute mean-reversion bounce risk typical of FX_MAJOR pairs but insufficient to override bearish structure

Trend strength is low at 3/10, indicating weak directional conviction and potential for range-bound behaviour.

Risk-Reward Assessment

Primary risk: Further GBP breakdown below 1.3182 support toward 1.30 major support if Fed maintains hawkish trajectory at July 29 meeting or delivers additional hawkish communications before then while BoE July 30 disappoints with dovish hold contrary to June 18 increased hawkish dissent, accelerating USD strength on widening policy divergence (Probability: medium)

Primary opportunity: GBP mean reversion bounce toward 1.3376-1.3474 resistance from current oversold RSI 33.99 if July 30 BoE delivers hawkish hold with forward guidance signaling potential hikes by August as UK services inflation 3.7% validates policy restraint case, triggering short-covering from defensive positioning or if Fed July 29 provides dovish clarification softening June 17 hawkish shift (Timeframe: 32 days through July 30 BoE meeting with near-term 1-2 week window for technical mean reversion from oversold conditions before extended positioning window ahead of late July dual central bank meetings)

This week's edge: No material information edge in current environment—dual central bank meetings are 10-11 days past and fully priced, next catalysts are Fed July 29 and BoE July 30 meetings creating extended 32-day low-catalyst window, FX_MAJOR noise floor of 0.50% with sixteen consecutive weeks of NO CALL bias exceeding 4-week review threshold by 300% indicating extreme persistence but appropriate given Section 3 guidance that default assumption is range-bound absent specific catalyst, mandatory news scan revealed BoE June 18 increased hawkish dissent (7-2 vote with two hike votes versus prior 8-1) already reflected in current 1.32 consolidation and market positioning, last week's CORRECT NO CALL (-0.2% move) demonstrates appropriate noise-threshold discipline, maintaining NEUTRAL stance consistent with measured calibration showing 40% weekly direction accuracy and -0.75R average requiring defensive positioning when catalyst clarity absent

Risk Environment

With vol compressed to the 39th percentile, GBPUSD is in the kind of quiet period that tends to end abruptly when a catalyst arrives. Volatility is stable, with realised vol holding steady across timeframes. This equilibrium can persist but eventually resolves into expansion or contraction.

Normal volatility environment allows standard risk management with 1.0-1.5% daily ranges expected in current consolidation, potential for 1.5-2% moves around July 29-30 Fed/BoE meetings given policy trajectory uncertainty with wider stops advised around event windows particularly if Fed delivers additional hawkish repricing or BoE surprises contrary to extended-hold-through-2027 expectations

Looking Forward

All eyes turn to Bank of England July 2026 MPC meeting following June 18 hold at 3.75% on 7-2 vote with two members voting for hike to 4.0%, market pricing extended hold through rest of 2026 but increased hawkish dissent creates policy trajectory uncertainty as UK services inflation at 3.7% remains elevated on Thursday 30 July, which carries enough weight to force a decisive directional move.

The week ahead for cable hinges on whether the prevailing consolidating regime can absorb the scheduled catalysts without a regime shift.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime