GBP/USD Forecast This Week — Outlook, Drivers & Key Levels

This week's GBP/USD outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

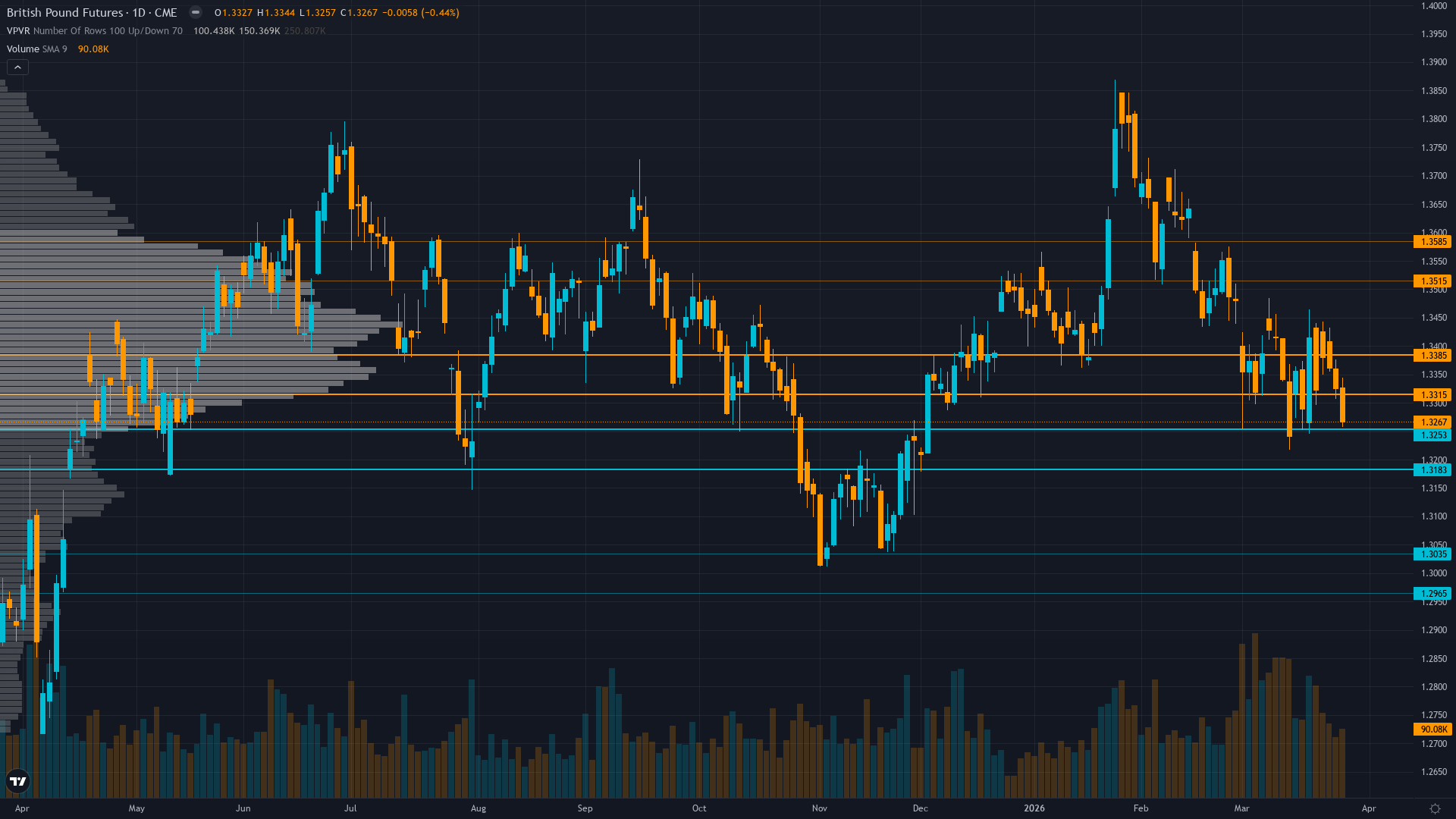

Current Market Picture

GBP/USD is trading at 1.3317, down 0.11% in a measured pullback. The range-bound condition in cable persists, with each test of the boundaries met by opposing force.

Neutral to mildly bearish consolidation expected with defensive positioning as markets digest BoE's hawkish inflation revision to 3.0-3.5% range following Iran conflict energy shock creating stagflationary policy dilemma

Key Drivers This Week

Primary driver: BoE March 19 hawkish hold at 3.75% with inflation forecasts revised HIGHER to 3.0-3.5% due to Iran war energy shock creating stagflationary headwinds that override near-term directional thesis for FX_MAJOR asset with smallest signal-to-noise ratio

Secondary factor: Speculative short covering accelerated from -84.2K to -65.5K contracts (22% reduction) creating modest positioning tailwind but insufficient to overcome fundamental uncertainty and elevated VIX at 31.05 indicating risk-off environment

Additional influence: Technical breakdown below 1.33 psychological support with 10-week downtrend intact trading near March low at 1.3218 while compressed implied volatility at 10.4% (IV Rank 19.9) signals market complacency despite elevated fundamental risks

Economic backdrop: MACRO REGIME: TRANSITIONAL with VIX at 31.05 indicating elevated fear above 25 threshold but no clear directional dominance, BoE held rates March 19 at 3.75% unanimously with inflation forecasts revised higher to 3.0-3.5% due to Iran conflict energy shock while Fed dot plot showed 7 of 19 members expect NO cuts in 2026 widening forward rate differential trajectory against GBP

Fundamental assessment: UK current account improved to 1.4% GDP in Q3 2025 and trade deficit narrowed to £6.0 billion but fiscal deterioration with February deficit £14.3bn versus £8.8bn forecast and BoE inflation revision to 3.0-3.5% range create stagflationary headwinds offsetting carry attractiveness

Price Structure

Downtrend intact trading at 1.3317 below 50-day MA at 1.3375 and 200-day MA at 1.3400 with RSI at 39.05 showing bearish momentum, 10-week decline from 1.3870 January peak with lower highs and lower lows pattern established

Trend strength at 4/10 paints a picture of a market with some direction but lacking strong conviction.

Upside & Downside

Primary risk: Further deterioration in UK fiscal position or sustained energy price elevation from Iran conflict causing BoE to maintain higher inflation forecasts triggering GBP breakdown below critical 1.3218 support toward 1.30 major support zone as real yield advantage erodes and stagflation fears intensify (Probability: medium)

Primary opportunity: GBP stabilization or recovery toward 1.335-1.355 resistance if Iran conflict de-escalates rapidly causing energy price collapse and allowing BoE to resume dovish trajectory while USD weakness from Fed easing expectations provides cross-current support (Timeframe: 2-4 weeks contingent on geopolitical developments and April US employment and inflation data releases determining policy trajectory divergence)

This week's edge: No material information edge in current environment—BoE March 19 hawkish inflation revision is now public and priced, April 3 US employment catalyst is 5 days away creating defensive pre-event positioning window, FX_MAJOR noise floor of 0.50% with probable weekly move near threshold argues against directional call, maintaining disciplined NO CALL stance after last week's CORRECT no-bias assessment

Volatility Context

At the 39th percentile, GBPUSD volatility is unusually subdued, creating conditions that historically precede sharp directional moves. Realised vol is holding its current level, suggesting the market has found a temporary equilibrium in its risk pricing.

Normal volatility environment allows standard risk management with 1.0-1.5% daily ranges expected in current consolidation, potential for 2-3% moves around April 3 US employment or April 10 CPI releases given inflation trajectory uncertainty with wider stops advised around event windows particularly if geopolitical developments escalate

Week Ahead Outlook

The next major catalyst is US Employment Situation Report for March 2026 followed by UK monthly trade data mid-April and US CPI April 10 providing critical inflation trajectory confirmation for both central banks on Friday 3 April — a high-impact event that could materially shift the directional picture.

For pound futures, the balance between existing momentum and scheduled risk events sets the stage for the week ahead.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime