Crude Oil Forecast This Week — Outlook, Drivers & Key Levels

This week's Crude Oil outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

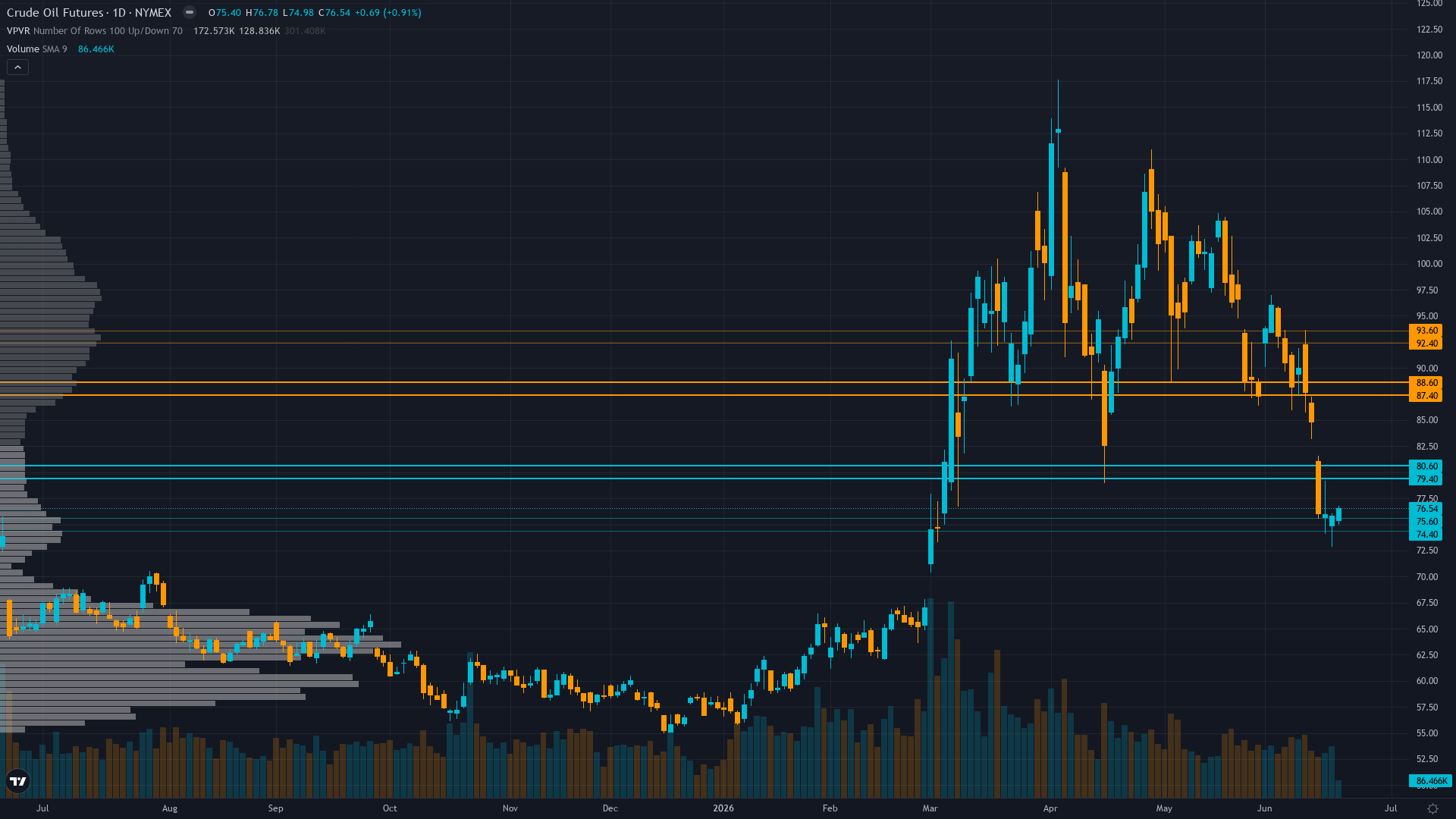

Current Market Picture

crude oil fell to 76.51 on a 1.06% decline, with selling pressure dominating price action. crude oil futures is in a breaking down market state, requiring careful assessment of current conditions.

Tactically bearish on geopolitical premium fade with structural oversupply consensus (IEA -1.1 mb/d demand contraction 2026, EIA Q4 $88 Brent, J.P. Morgan $60 Brent fair value) implying current $76.51 already at or below fundamental equilibrium as mean reversion 95%+ complete

Key Drivers This Week

Primary driver: Geopolitical premium complete collapse as WTI plunged 36% from March $120 peak to current $76.51 following Strait of Hormuz normalization, while IEA June 18 report delivers FRESH demand destruction bombshell downgrading 2026 global oil demand by 700 kb/d to -1.1 mb/d annual contraction versus prior month's forecast creating structural oversupply ceiling

Secondary factor: Technical breakdown acceleration with WTI at $76.51 breaking decisively below 200-day MA at $85.58 and 50-day MA at $86.89, RSI deeply oversold at 25.13 confirming distribution phase complete as 21% monthly decline represents one of sharpest mean reversions in years toward fundamental fair value

Additional influence: Managed money positioning undergoing forced liquidation from elevated levels built during Hormuz crisis while U.S. inventories at 424.4M barrels remain 4% below five-year average providing insufficient tactical tightness to justify premium as OPEC+ June production increase of 188k bpd signals cartel confidence in normalization trajectory

Economic backdrop: MACRO REGIME: TRANSITIONAL trending RISK-ON - VIX normalized to 16.78 (June 19, well below 20 calm threshold) indicating geopolitical risk successfully ring-fenced to energy sector; Fed on hold at 3.50-3.75%; CRITICAL FRESH CATALYST: IEA June 18 report (3 days old) downgraded 2026 demand by 700 kb/d creating net -1.1 mb/d contraction versus prior +0.2 mb/d growth expectation, most significant monthly revision validating demand destruction overwhelming supply normalization

Fundamental assessment: Crude modestly undervalued 0-5% versus normalized inventory levels $70-80 marginal cost but IEA June 18 demand destruction catalyst (global demand -1.1 mb/d contraction 2026, down 700 kb/d from prior month) creates structural ceiling; current $76.51 pricing already AT or below EIA Q4 forecast $88 Brent-equivalent suggesting mean reversion 95%+ complete

Price Structure

Confirmed downtrend with death cross complete, WTI at $76.51 broke and holding below critical 200-day MA $85.58 and 50-day MA $86.89, RSI 25.13 deeply oversold, 52-week high $117.63 now 54% overhead creating massive resistance wall

Trend strength registers just 3/10, which typically corresponds to choppy, directionless price action.

Upside & Downside

Primary risk: Strait of Hormuz normalization stalls or reverses with renewed military escalation forcing repricing back toward $85-90 range as residual supply disruption risk premium reasserts, invalidating mean reversion completion thesis despite U.S. policy commitment to normalization (Probability: low)

Primary opportunity: Complete Strait normalization validates EIA/IEA structural oversupply projections with geopolitical premium fully exhausted, triggering final leg toward J.P. Morgan $60/bbl Brent fair value ($58-60 WTI equivalent) as structural oversupply (IEA 2.5 mb/d surplus 2H26) and demand destruction (-1.1 mb/d contraction) overwhelm within 2-4 weeks (Timeframe: 2-4 weeks through early July as Strait flows normalize completely and Q3 structural oversupply reasserts full dominance over tactical factors)

This week's edge: Market may be underweighting IEA June 18 demand destruction magnitude (700 kb/d downgrade in ONE MONTH, largest monthly revision in years flipping to -1.1 mb/d annual contraction) while overweighting residual geopolitical tail risk; technical breakdown below 200-day MA with 9-week bearish vindication (36% decline) suggests LOW edge environment as consensus now aligned with desk thesis, yet deeply oversold RSI 25.13 and current price BELOW EIA Q4 forecast creates modest tactical support potential not fully priced in bearish positioning

Volatility Context

At the 88th percentile of its 90-day range, oil price volatility is running hot, creating both opportunity and risk for directional traders. Realised vol is holding its current level, suggesting the market has found a temporary equilibrium in its risk pricing.

High but contracting volatility requires moderately wide stops; expect 3-5% daily ranges currently versus 6-8% during peak conflict and 2-3% normal, as normalization removes binary catalyst creating more orderly price discovery; intraday volatility declining suggests market adapting to structural oversupply framework

Week Ahead Outlook

The next major catalyst is EIA Weekly Petroleum Status Report following week of catastrophic 9.83% collapse to 8-month low $76.51, providing inventory validation of Strait normalization trajectory versus structural oversupply fundamentals as demand destruction accelerates on Wednesday 24 June — a high-impact event that could materially shift the directional picture.

For CL futures, the balance between existing momentum and scheduled risk events sets the stage for the week ahead.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime