30-Year Treasury Forecast This Week — Outlook, Drivers & Key Levels

This week's 30-Year Treasury outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

This Week's Starting Point

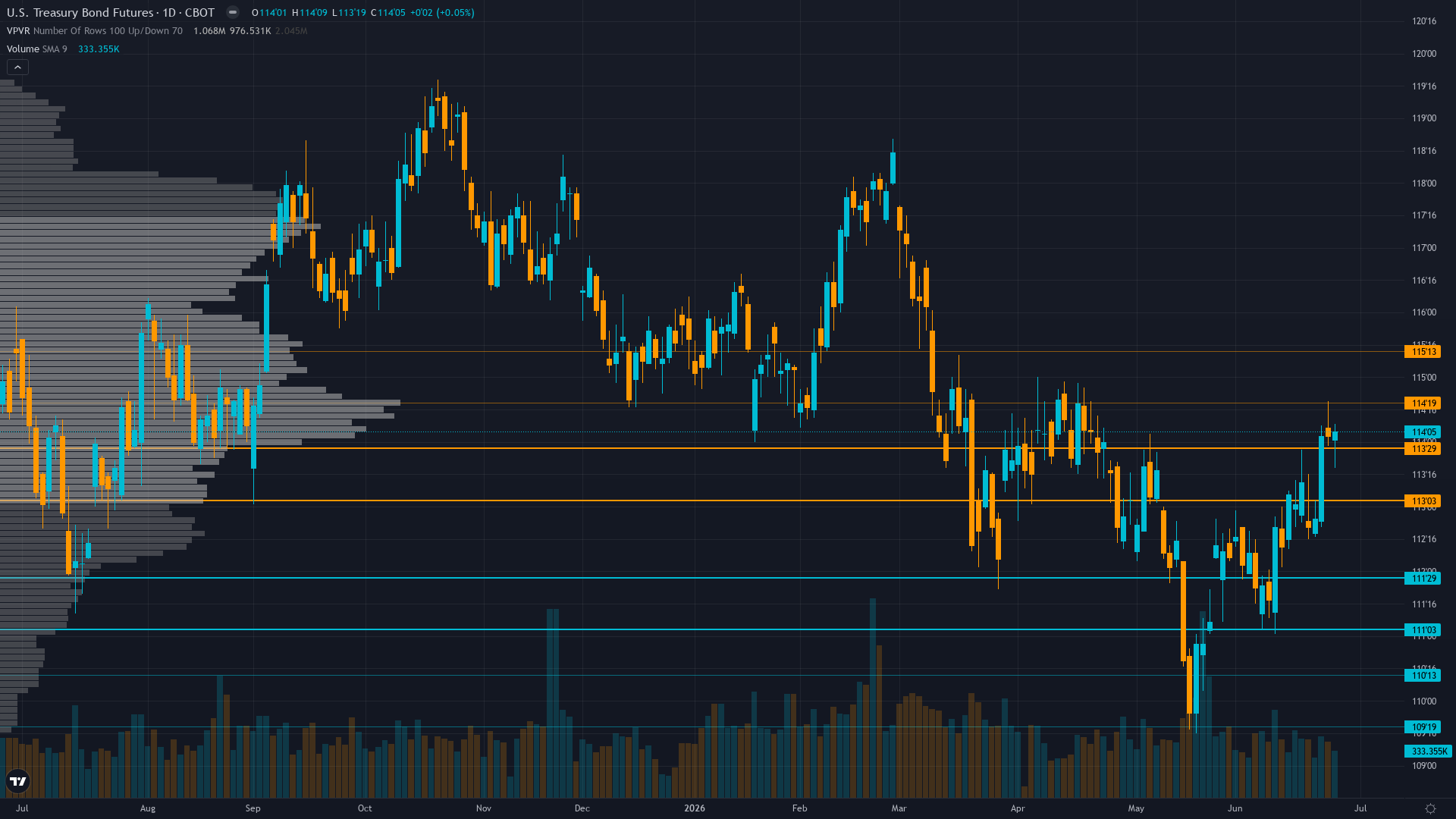

30-year Treasury holds at 114.03, up a marginal 0.08% as the market grinds forward. Treasury bond futures is in a consolidating within narrow range market state, requiring careful assessment of current conditions.

Market pricing Fed on hold at July 30-31 FOMC maintaining 3.50-3.75% range with <10% cut probability 2026 per June 19 analysis; bonds consolidating 112-116 awaiting July 14 CPI clarity on whether Warsh June 17 hawkish shift validated by data

Forces in Play

Primary driver: June 17 FOMC hawkish pivot removing easing bias and raising dot plot to 3.6-4.1% combined with May CPI 4.17% acceleration creating structural bearish repricing environment yet consecutive miss streak at 2 requiring heightened caution on directional positioning

Secondary factor: Cross-discipline conflict with Economic -3.5 (hawkish Fed shift) heavily bearish versus Fundamental/Options/Institutional/Technical/Sentiment all mildly bullish creating 1v5 split reducing directional clarity despite Economic discipline carrying 0.35 weight

Additional influence: MOVE volatility at 67.10 down 13.37% monthly from elevated regime signals extreme complacency creating dangerous calm yet current depressed levels provide no catalyst for directional conviction until July 14 CPI forces resolution

Economic backdrop: Post-input development identified: Kevin Warsh's June 17 FOMC held at 3.50-3.75% as expected but removed dovish easing bias language and raised year-end dot plot to 3.6-4.1% with market now pricing <10% cut probability 2026; May CPI 4.17% YoY with 3-month annualized pace at 8.20% shows sticky inflation above Fed 2% target; no major data until July 14 CPI creating 16-day low-information void

Fundamental assessment: Fed at 3.50-3.75% with June 17 FOMC removing easing bias and raising year-end dot plot to 3.6-4.1% representing material hawkish shift yet market pricing <10% cut probability 2026 already reflects this; FY2026 deficit $1.25T through May tracking 2% below prior year improving trajectory; term premium compressed at 0.67% versus historical ~1.0% norm

Technical Landscape

Consolidating 113.20-115.00 range after last week rally to 114.09; current 114.03 in middle of range with stalled momentum and declining open interest at 2.00M suggesting participant deleveraging; former downtrend structure from April 7 peak at 114.75 remains intact but recent rallies challenge bearish thesis

Trend strength is low at 3/10, indicating weak directional conviction and potential for range-bound behaviour.

Risk-Reward Assessment

Primary risk: July 14 CPI shows inflation persistence above 0.3% MoM core validating May 4.17% acceleration forcing market to reprice Fed terminal rate higher sending ZB below 113.2 support toward 112 major support with cascade potential representing 1.5-2% decline from current 114.03 levels (Probability: medium)

Primary opportunity: June employment July 5 or CPI July 14 data shows material deterioration contradicting May inflation spike forcing Fed to acknowledge Warsh hawkish pivot was premature triggering violent short covering rally above 115.0 resistance toward 116.5-118 zone from current compressed MOVE levels at 67.10 (Timeframe: Next 2-3 weeks through July 5 employment and July 14 CPI if data deteriorates significantly creating 15-20% MOVE expansion from current 67.10 toward 80-85 range)

This week's edge: Market potentially underpricing magnitude of hawkish shift from Warsh's June 17 removal of easing bias combined with May CPI 4.17% yet consecutive miss streak at 2 and cross-discipline 1v5 conflict suggests this desk's bearish thesis may be stale or incorrectly timed; alternatively market may be overpricing resilience from improving deficit trajectory and quarter-end flows creating false stability before July catalysts force resolution; probable weekly move 0.5-0.6% marginally above 0.50% Noise Floor with 16-day void until July 14 CPI limiting conviction to minimum threshold

Risk Environment

With vol compressed to the 25th percentile, T-bond futures is in the kind of quiet period that tends to end abruptly when a catalyst arrives. Volatility is contracting, with realised vol declining across timeframes. Compressed volatility often precedes sharp directional moves as energy builds.

Volatility compression creating false calm environment; daily ranges compressing from 1.0-1.5 handles during May breakdown toward current 0.4-0.6 handles as MOVE declines to multi-year lows; current 114.03 price in middle of 113.2-115.0 consolidation with July 14 CPI creating near-term binary catalyst that could force violent breakout in either direction with expected 1.5-2.0 handle daily swings post-decision

Looking Forward

All eyes turn to June CPI release at 8:30 AM ET critical for validating whether May's 4.17% inflation persistence continues; if June exceeds 0.3% MoM core would cement Fed hawkish hold through Q3-Q4 2026 pressuring duration; precedes July 30-31 FOMC decision which will incorporate this data on Tuesday 14 July, which carries enough weight to force a decisive directional move.

The week ahead for Treasury bond futures hinges on whether the prevailing consolidating within narrow range regime can absorb the scheduled catalysts without a regime shift.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime