Wheat (ZW) — Resetting after 3 consecutive misses - thesis under review

Mixed to cautiously bullish on technical breakout above moving averages and March 27 drought reports yet skeptical about sustainability given March 10 WASDE showing minimal changes and structural oversupply at record global stocks

Mixed to cautiously bullish on technical breakout above moving averages and March 27 drought reports yet skeptical about sustainability given March 10 WASDE showing minimal changes and structural oversupply at record global stocks

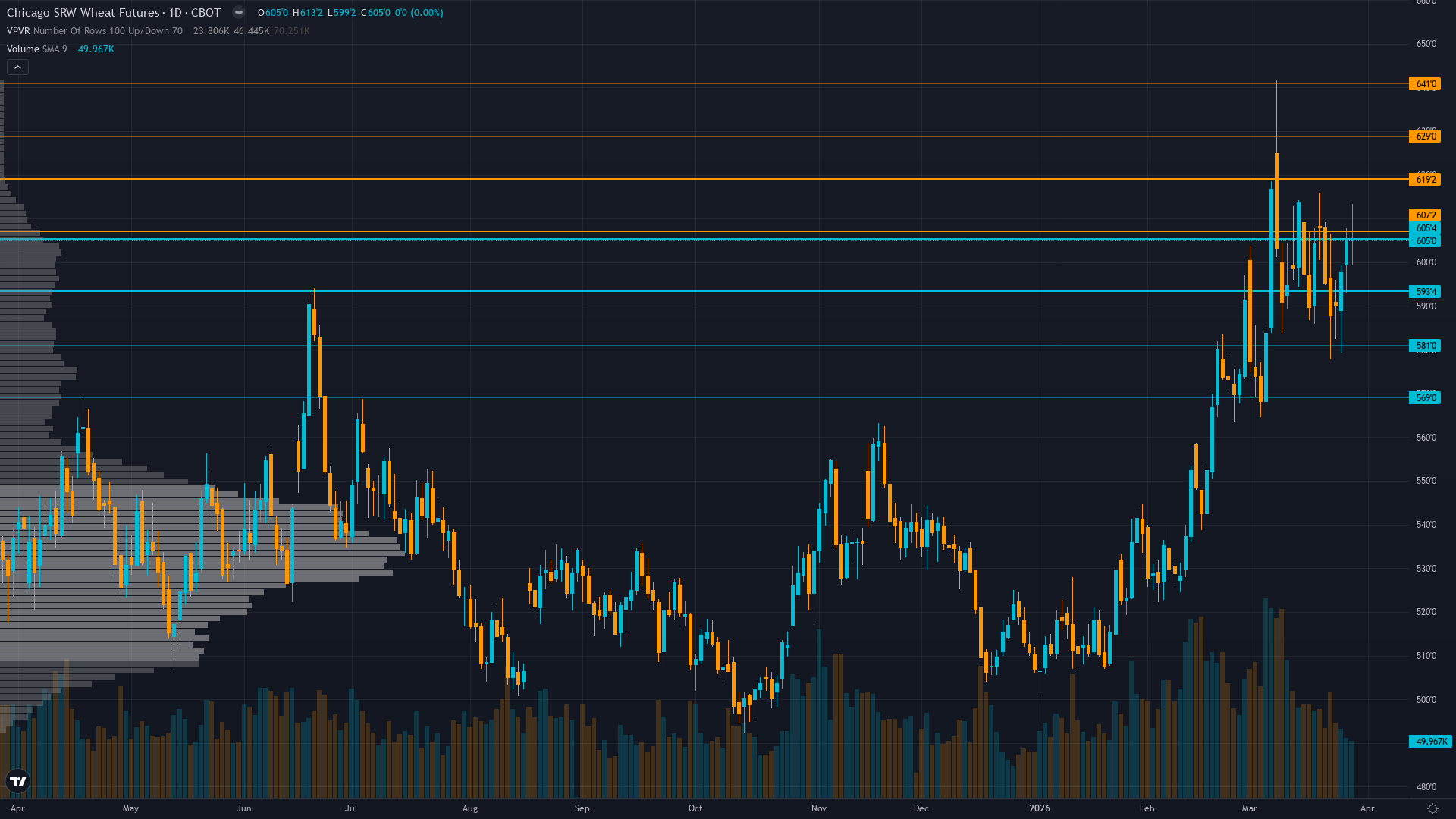

Resetting after 3 consecutive missed directional calls - wheat at 605 cents following fresh drought intensification news showing 18% harvest forecast plummet but miss streak requiring mandatory neutral period

March 10 WASDE held US wheat stocks steady yet March 27 FinancialContent reports global harvest forecast down 18% amid historic Plains drought with heat dome 20-25F above normal creating fundamental uncertainty

Technical structure remains bullish above 50-day and 200-day moving averages per March 27 OneUpTrader analysis yet spec positioning shifted from net short 3,247 contracts creating two-way risk without clear edge

| ▼ Resistance Zone 2 | 630.00 – 640.00 |

| ▼ Resistance Zone 1 | 608.13 – 618.13 |

| ─ Pivot Area | ~605.00 |

| ▲ Support Zone 1 | 594.38 – 604.38 |

| ▲ Support Zone 2 | 570.00 – 580.00 |

Price holding above both 50-day and 200-day moving averages for first time in months per March 27 analysis with strong buy signals yet daily range 599-613 shows consolidation after rally from 492 lows

Conflicting signals with March 10 WASDE showing minimal changes to 931 million bushel US stocks yet March 27 drought reports showing 18% global harvest forecast reduction creating fundamental uncertainty requiring data resolution

Spec positioning marginally net long 3,247 contracts as of March 17 representing bullish shift from prior week yet mid-range positioning creates balanced two-way risk without positioning extreme to exploit

Implied volatility data unavailable for current contracts with March contract showing minimal open interest of 92 contracts indicating liquidity rolled to May limiting options market directional insight

TRANSITIONAL macro regime with VIX at 25-31 indicating elevated fear USD strength at 99-100 creating export headwinds and crude oil at 92/bbl following Iran conflict raising input costs offsetting stable demand

Slightly inverted - short-term volatility elevated at 28.5% versus medium-term 26.5% following February-March rally and WASDE event risk with term structure suggesting elevated two-way action persists but expansion phase may be maturing

Weather-driven rallies from extreme short positioning historically produce 50-80% volatility expansion over 4-6 weeks with current expansion from 24% to 32% consistent with mature stages suggesting peak volatility likely achieved unless fresh catalyst emerges from April WASDE or late March freeze event

Volatility expanded from January-February consolidation following Arctic blast and WASDE events now stabilizing in high regime with potential for 15-20% compression if market enters sustained consolidation without fresh weather catalyst or modest additional expansion if directional breakout occurs

Daily ranges expanded from compressed 10-16 cents during late 2025 consolidation to current 15-25 cent action requiring wider stops with breakdown below 594 or recovery above 608 triggering accelerated moves given failed breakout structure and elevated volatility environment

Elevated volatility in high regime creates balanced two-way risk where fresh bullish catalyst from intensifying drought or April WASDE production downgrades could drive 5-8% rally toward 630-650 while downside to 575-590 appears possible if drought fears prove overblown with stable high volatility suggesting ranging behavior most likely near-term between 575-610 boundaries

|

⚠️ Primary Risk

April WASDE confirms March drought damage overblown with adequate moisture arriving in time to prevent material production losses sending market back toward 575-590 support as structural oversupply narrative reasserts dominance Probability: MEDIUM

|

✦ Primary Opportunity

Continued drought deterioration through April combined with late-season freeze risk from early dormancy break triggers additional production downgrades driving explosive rally toward 635-650 range on renewed weather premium Timeframe: Next 2-4 weeks through April 9 WASDE and critical March-April weather window for 2026 crop

|

ZW wheat futures stand at 605.00 cents per bushel on March 29, 2026, requiring a mandatory NEUTRAL call following three consecutive missed directional forecasts per Rule 5 miss streak reset protocol. This reset occurs at a critical juncture as conflicting fundamental signals create genuine analytical uncertainty. Current macro regime classification: TRANSITIONAL with mixed signals showing VIX elevated at 25-31 (above 25 fear threshold) indicating heightened investor nervousness, USD strengthening to 99-100 DXY following geopolitical safe-haven flows from Iran-Hormuz conflict, and crude oil at 92/bbl creating input cost pressures.

For agricultural commodities, the dominant headwind is USD strength which directly impairs US wheat export competitiveness versus Argentina, Russia, and Black Sea suppliers. Post-input development identified: March 27, 2026 FinancialContent reported global breadbasket under siege with wheat harvest forecast plummeting 18% amid historic droughts, with heat dome temperatures in the West and Plains reaching 20-25 degrees Fahrenheit above normal and shattering early-season records. This represents a material new development NOT reflected in the March 10 WASDE report which held US corn, soybean, and wheat ending stocks steady at approximately 931 million bushels with 32% stocks-to-use ratio.

The High Plains Journal confirmed on March 26 that extreme weather added drought pressure with persistent heat dome driving temperatures 20-25F above normal and significantly increasing evaporative demand. However, the February 25 FinancialContent report noted a 'wet trend' for Southern Plains with 35-90% chance of heavy rain and thunderstorms expected between March 1-7, creating conflicting weather narratives that require April WASDE resolution. Technical structure per March 27 OneUpTrader analysis shows price now holding above both the 50-day moving average and 200-day moving average for the first time in months following rally from 500 lows, with current price at 605 testing the 560-613 breakout zone.

Positioning dynamics show spec shorts reduced to 3,247 contracts marginally net long as of March 17, representing a bullish shift from prior week yet positioning remains in mid-range (45th-55th percentile) creating balanced two-way risk without the positioning extreme required for asymmetric squeeze potential. The fundamental backdrop remains dominated by structural oversupply with global stocks at record 925.5 million tonnes (FAO March 2026) and 276.2 million tons per WASDE, yet the emerging March 27 drought narrative showing 18% harvest forecast reduction creates fundamental uncertainty that cannot be resolved without additional data.

The miss streak requiring this reset stemmed from attempting to call direction in a market transitioning between oversupply dominance and emerging weather premium without sufficient edge to overcome the 0.75% noise threshold for agricultural assets. Current price sits in the middle of the 52-week range spanning 492-635, up 14.53% year-over-year, suggesting the market has priced in US supply tightness but not adequately discounting either the global surplus OR the emerging March drought developments.

Volatility intelligence suggests elevated two-way action with daily ranges expanding from compressed consolidation, yet without clear directional catalyst before April 9 WASDE the probable weekly move may approach the 0.75% noise threshold. The combination of mandatory miss reset, conflicting fundamental signals between WASDE oversupply and March 27 drought reports, mid-range positioning without extreme, and absence of fresh catalyst before April 9 creates setup where NEUTRAL is the only appropriate call.

This desk acknowledges it lacks sufficient edge to overcome noise threshold and positioning uncertainty until April WASDE provides weather-adjusted production clarity.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 27, 2026 | BEARISH | 5/10 | ❌ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | BULLISH | 8/10 | ❌ |

| March 6, 2026 | BULLISH | 8/10 | ✅ |

| February 27, 2026 | BULLISH | 8/10 | ✅ |

| February 21, 2026 | NO CALL | 7/10 | ➖ |

| February 13, 2026 | NO CALL | 7/10 | ➖ |

| February 8, 2026 | NO CALL | 7/10 | ➖ |

| February 1, 2026 | NO CALL | 7/10 | ➖ |

| January 25, 2026 | NO CALL | 7/10 | ➖ |

| January 11, 2026 | NO CALL | 7/10 | ➖ |

| January 4, 2026 | BEARISH | 7/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Wheat (ZW) Report Date: March 29, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 18 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: CONSOLIDATING IN RANGE Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Mixed to cautiously bullish on technical breakout above moving averages and March 27 drought reports yet skeptical about sustainability given March 10 WASDE showing minimal changes and structural oversupply at record global stocks ── WHAT THE MARKET IS MISSING ─────────────────── Resetting after 3 consecutive misses - thesis under review. Market faces conflicting fundamental signals between March 10 WASDE minimal changes and March 27 reports of 18% harvest forecast reduction requiring April 9 WASDE resolution before establishing directional edge. ── KEY DRIVERS ────────────────────────────────── 1. Resetting after 3 consecutive missed directional calls - wheat at 605 cents following fresh drought intensification news showing 18% harvest forecast plummet but miss streak requiring mandatory neutral period 2. March 10 WASDE held US wheat stocks steady yet March 27 FinancialContent reports global harvest forecast down 18% amid historic Plains drought with heat dome 20-25F above normal creating fundamental uncertainty 3. Technical structure remains bullish above 50-day and 200-day moving averages per March 27 OneUpTrader analysis yet spec positioning shifted from net short 3,247 contracts creating two-way risk without clear edge ── KEY ZONES ──────────────────────────────────── Resistance 2: 630.00 – 640.00 Resistance 1: 608.13 – 618.13 Pivot: ~605.00 Support 1: 594.38 – 604.38 Support 2: 570.00 – 580.00 ── DISCIPLINE BIASES ──────────────────────────── Technical: BULLISH Fundamental: NO CALL Institutional: NO CALL Options: NO CALL Economic: BEARISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Price holding above both 50-day and 200-day moving averages for first time in months per March 27 analysis with strong buy signals yet daily range 599-613 shows consolidation after rally from 492 lows ── FUNDAMENTAL ASSESSMENT ─────────────────────── Conflicting signals with March 10 WASDE showing minimal changes to 931 million bushel US stocks yet March 27 drought reports showing 18% global harvest forecast reduction creating fundamental uncertainty requiring data resolution ── INSTITUTIONAL POSITIONING ──────────────────── Spec positioning marginally net long 3,247 contracts as of March 17 representing bullish shift from prior week yet mid-range positioning creates balanced two-way risk without positioning extreme to exploit ── OPTIONS FLOW ───────────────────────────────── Implied volatility data unavailable for current contracts with March contract showing minimal open interest of 92 contracts indicating liquidity rolled to May limiting options market directional insight ── ECONOMIC BACKDROP ──────────────────────────── TRANSITIONAL macro regime with VIX at 25-31 indicating elevated fear USD strength at 99-100 creating export headwinds and crude oil at 92/bbl following Iran conflict raising input costs offsetting stable demand ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 68th Trend: Stable — Days in Regime: 14 Term Structure: slightly inverted - short-term volatility elevated at 28.5% versus medium-term 26.5% following February-March rally and WASDE event risk with term structure suggesting elevated two-way action persists but expansion phase may be maturing Historical Pattern: Weather-driven rallies from extreme short positioning historically produce 50-80% volatility expansion over 4-6 weeks with current expansion from 24% to 32% consistent with mature stages suggesting peak volatility likely achieved unless fresh catalyst emerges from April WASDE or late March freeze event Outlook: Volatility expanded from January-February consolidation following Arctic blast and WASDE events now stabilizing in high regime with potential for 15-20% compression if market enters sustained consolidation without fresh weather catalyst or modest additional expansion if directional breakout occurs Trading Context: Daily ranges expanded from compressed 10-16 cents during late 2025 consolidation to current 15-25 cent action requiring wider stops with breakdown below 594 or recovery above 608 triggering accelerated moves given failed breakout structure and elevated volatility environment Vol Risk/Opportunity: Elevated volatility in high regime creates balanced two-way risk where fresh bullish catalyst from intensifying drought or April WASDE production downgrades could drive 5-8% rally toward 630-650 while downside to 575-590 appears possible if drought fears prove overblown with stable high volatility suggesting ranging behavior most likely near-term between 575-610 boundaries ── PRIMARY RISK ───────────────────────────────── April WASDE confirms March drought damage overblown with adequate moisture arriving in time to prevent material production losses sending market back toward 575-590 support as structural oversupply narrative reasserts dominance Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Continued drought deterioration through April combined with late-season freeze risk from early dormancy break triggers additional production downgrades driving explosive rally toward 635-650 range on renewed weather premium Timeframe: Next 2-4 weeks through April 9 WASDE and critical March-April weather window for 2026 crop ── NEXT CATALYST ──────────────────────────────── Date: April 9, 2026 Event: USDA April 2026 WASDE Report with winter wheat acreage estimates production forecasts and condition assessments incorporating weather-adjusted outlook following March drought intensification Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ZW wheat futures stand at 605.00 cents per bushel on March 29, 2026, requiring a mandatory NEUTRAL call following three consecutive missed directional forecasts per Rule 5 miss streak reset protocol. This reset occurs at a critical juncture as conflicting fundamental signals create genuine analytical uncertainty. Current macro regime classification: TRANSITIONAL with mixed signals showing VIX elevated at 25-31 (above 25 fear threshold) indicating heightened investor nervousness, USD strengthening to 99-100 DXY following geopolitical safe-haven flows from Iran-Hormuz conflict, and crude oil at 92/bbl creating input cost pressures. For agricultural commodities, the dominant headwind is USD strength which directly impairs US wheat export competitiveness versus Argentina, Russia, and Black Sea suppliers. Post-input development identified: March 27, 2026 FinancialContent reported global breadbasket under siege with wheat harvest forecast plummeting 18% amid historic droughts, with heat dome temperatures in the West and Plains reaching 20-25 degrees Fahrenheit above normal and shattering early-season records. This represents a material new development NOT reflected in the March 10 WASDE report which held US corn, soybean, and wheat ending stocks steady at approximately 931 million bushels with 32% stocks-to-use ratio. The High Plains Journal confirmed on March 26 that extreme weather added drought pressure with persistent heat dome driving temperatures 20-25F above normal and significantly increasing evaporative demand. However, the February 25 FinancialContent report noted a 'wet trend' for Southern Plains with 35-90% chance of heavy rain and thunderstorms expected between March 1-7, creating conflicting weather narratives that require April WASDE resolution. Technical structure per March 27 OneUpTrader analysis shows price now holding above both the 50-day moving average and 200-day moving average for the first time in months following rally from 500 lows, with current price at 605 testing the 560-613 breakout zone. Positioning dynamics show spec shorts reduced to 3,247 contracts marginally net long as of March 17, representing a bullish shift from prior week yet positioning remains in mid-range (45th-55th percentile) creating balanced two-way risk without the positioning extreme required for asymmetric squeeze potential. The fundamental backdrop remains dominated by structural oversupply with global stocks at record 925.5 million tonnes (FAO March 2026) and 276.2 million tons per WASDE, yet the emerging March 27 drought narrative showing 18% harvest forecast reduction creates fundamental uncertainty that cannot be resolved without additional data. The miss streak requiring this reset stemmed from attempting to call direction in a market transitioning between oversupply dominance and emerging weather premium without sufficient edge to overcome the 0.75% noise threshold for agricultural assets. Current price sits in the middle of the 52-week range spanning 492-635, up 14.53% year-over-year, suggesting the market has priced in US supply tightness but not adequately discounting either the global surplus OR the emerging March drought developments. Volatility intelligence suggests elevated two-way action with daily ranges expanding from compressed consolidation, yet without clear directional catalyst before April 9 WASDE the probable weekly move may approach the 0.75% noise threshold. The combination of mandatory miss reset, conflicting fundamental signals between WASDE oversupply and March 27 drought reports, mid-range positioning without extreme, and absence of fresh catalyst before April 9 creates setup where NEUTRAL is the only appropriate call. This desk acknowledges it lacks sufficient edge to overcome noise threshold and positioning uncertainty until April WASDE provides weather-adjusted production clarity.