Wheat (ZW) — Black Sea winter weather disruptions creating first supply-side risk premium in…

Bearish consensus has complete dominance expecting continued weakness with January WASDE confirming oversupply trajectory yet acknowledging potential for tactical bounces from extreme positioning and emerging Black Sea weather concerns

Bearish consensus has complete dominance expecting continued weakness with January WASDE confirming oversupply trajectory yet acknowledging potential for tactical bounces from extreme positioning and emerging Black Sea weather concerns

Black Sea winter weather disruptions creating first supply-side risk premium in six months as extreme cold shots in late January-early February 2026 trigger widespread wheat winterkill concerns in Ukraine and Southern Russia

Extreme oversold positioning with market trading just 7.6% above October 2025 capitulation lows at 492.25 following catastrophic failure of November-December seasonal strength patterns

February historically strong seasonal period testing whether calendar effects can finally assert themselves after 2025 structural oversupply overwhelmed multi-decade patterns

| ▲ Resistance Zone 2 | 575.00 – 585.00 |

| ▲ Resistance Zone 1 | 540.00 – 550.00 |

| ─ Pivot Area | ~530.00 |

| ▼ Support Zone 1 | 510.00 – 520.00 |

| ▼ Support Zone 2 | 487.25 – 497.25 |

Trading at 529.75 just 7.6% above October 2025 capitulation floor at 492.25 in lower 30th percentile of 52-week range 492-622 attempting stabilization after complete November-December seasonal pattern failure

Overwhelmingly bearish with January 2026 WASDE confirming global stocks at 276.2 million tons and record production yet strong US export pace at 900 million bushels highest since 2020-21 provides tangible floor around 500-515

Net short 109,483 contracts as of January 7 2026 representing largest bearish position since October 2025 creating asymmetric short-covering vulnerability at multi-year lows

Implied volatility normalizing around 23-24% annualized after October 2025 breakdown expansion reflecting market acceptance of oversupply narrative yet readings remain elevated versus prior 18% compression suggesting continued two-way risk

Stable agricultural demand environment unable to absorb record global wheat supply with USD strength creating export headwinds offset by US competitive positioning maintaining 11% global market share

Normalizing - short-term volatility stable around medium-term following October 2025 breakdown and January 2026 WASDE confirmation with term structure flattening as market finds equilibrium

Post-breakdown volatility typically remains elevated 10-12 weeks before normalizing - current 16-week period since October 2025 capitulation suggests volatility normalization underway unless fresh Black Sea weather catalyst triggers new expansion phase

Volatility expanded from October 2025 breakdown through December consolidation now stabilizing around normal range suggesting market acceptance of new lower price equilibrium around 500-530 level with potential for spike if Black Sea weather concerns accelerate or breakdown extends below 500

Daily ranges stable around 10-16 cents suggesting reduced directional conviction near multi-year lows - breakout above 545 or breakdown below 515 would trigger expansion with Black Sea weather developments representing high-impact catalyst for potential volatility spike in either direction

Stable volatility near 52-week lows creates asymmetric setup where unexpected bullish catalyst from Black Sea port disruptions severe Russian-Ukrainian winter weather or February WASDE surprises could trigger explosive 10-15% short-covering rally toward 560-580 while downside appears increasingly limited to 492-515 zone by export floor and extreme oversold conditions from October

|

⚠️ Primary Risk

February WASDE confirms continued global oversupply trajectory sending market below 500 psychological support toward retesting October 492 lows as Black Sea weather premium dissipates and structural bear market extends Probability: MEDIUM

|

✦ Primary Opportunity

Black Sea winter weather disruptions intensify winterkill damage combining with February seasonal tailwinds and extreme short positioning at 109,483 contracts to trigger explosive 10-15% short-covering rally toward 580-600 range as first genuine supply-side catalyst in six months materializes Timeframe: Next 2-6 weeks through February WASDE and peak winter weather assessment period for 2026 Black Sea crop

|

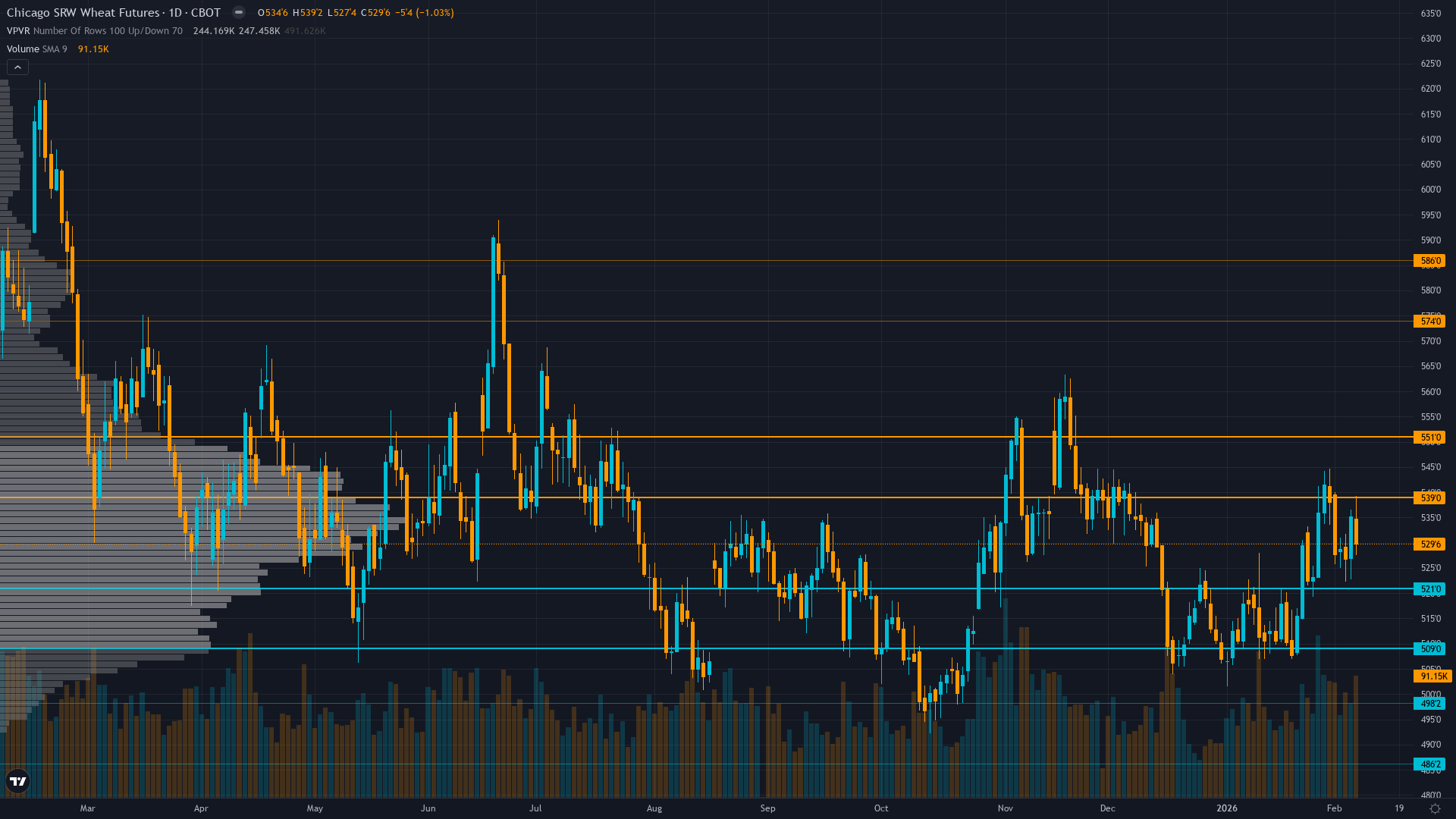

ZW wheat futures stand at one of the most critical inflection points in modern commodity market history on February 8, 2026, trading at 529.75 cents per bushel after experiencing the most spectacular failure of seasonal patterns on record during November-December 2025 where record 1,097.8 million ton global oversupply completely overwhelmed multi-decade calendar effects. The market enters February 2026 having surrendered nearly all gains from the November bounce that peaked near 541, trading just 7.6% above the October capitulation lows at 492.25 that marked 52-week extremes.

However, late January and early February 2026 bring the first genuine bullish catalyst in six months: extreme cold shots in the Black Sea region, particularly Ukraine and Southern Russia, are triggering widespread wheat winterkill concerns as severe winter weather threatens dormant winter wheat crops with frozen ports disrupting export flows. Current positioning shows spec shorts at 109,483 contracts as of January 7—the largest bearish position since October 2025—reflecting entrenched oversupply consensus yet creating maximum vulnerability to squeeze dynamics at multi-year lows.

February historically represents continuation of autumn-winter seasonal recovery patterns, and the question for 2026 is whether Black Sea weather concerns can provide the catalyst to break the oversupply narrative that has dominated since summer 2025. The fundamental backdrop remains dominated by structural oversupply with normalized Black Sea exports throughout 2025 eliminating geopolitical risk premiums, yet robust US export competitiveness at 900 million bushels forecast provides tangible support around 500-515.

The February 10 WASDE emerges as critical catalyst determining whether Black Sea weather disruptions are material enough to alter supply projections or whether structural oversupply narrative extends. Current price essentially reflects worst-case scenarios fully discounted creating asymmetric setup where unexpected bullish catalysts from intensifying Black Sea winterkill, stronger export demand, or February WASDE production downgrades could trigger explosive 10-15% short-covering rallies toward 560-580 given the 109,483 contract net short position and expanding volatility environment, while downside appears increasingly limited by psychological 500 support and strong export fundamentals providing floor.

Volatility has normalized from October breakdown expansion to 52nd percentile suggesting market acceptance of new equilibrium yet readings remain elevated versus the 62-day low regime compression of August-October 2025 at 32nd percentile. The combination of extreme oversold technical conditions at 52-week lows, historically crowded short positioning, emerging Black Sea weather catalyst, potential February seasonal tailwinds attempting to reassert after spectacular 2025 failure, and the 900 million bushel export floor creates setup where 2026 could mark either extension of generational oversupply bear market or the beginning of mean reversion as weather concerns and positioning dynamics overwhelm fundamental headwinds.

| Week | Bias | Confidence |

|---|---|---|

| February 8, 2026 | NEUTRAL | 7/10 |

| February 1, 2026 | NEUTRAL | 7/10 |

| January 25, 2026 | NEUTRAL | 7/10 |

| January 18, 2026 | NEUTRAL | 7/10 |

| January 11, 2026 | NEUTRAL | 7/10 |

| January 4, 2026 | BEARISH | 7/10 |

| December 28, 2025 | BEARISH | 7/10 |

| December 21, 2025 | BEARISH | 8/10 |

| December 14, 2025 | NEUTRAL | 7/10 |

| December 7, 2025 | NEUTRAL | 7/10 |

| November 30, 2025 | NEUTRAL | 7/10 |

| November 23, 2025 | NEUTRAL | 7/10 |