Soybeans (ZS) — -1.4 between 1144 support and 1180 resistance with 5/10 confidence

Mixed with bearish fundamental analysts citing WASDE supply increases and Brazilian pricing advantages offset by bullish institutional trend-followers maintaining net long positioning ahead of March 31 binary event creating two-way uncertainty

Mixed with bearish fundamental analysts citing WASDE supply increases and Brazilian pricing advantages offset by bullish institutional trend-followers maintaining net long positioning ahead of March 31 binary event creating two-way uncertainty

March 31 USDA Prospective Plantings report 2 days away creates binary event risk with early expectations suggesting potential soybean acreage expansion of 4 million acres to 85 million total pressuring prices alongside continued China purchase uncertainty

Fundamental analyst signals -2.0 citing WASDE raised US supply by 5M bushels while Brazilian soybeans trade $0.80-$1.00 below US creating 8-10% persistent export competitiveness headwinds overwhelming structural renewable diesel support

Institutional positioning shows managed money reducing net longs by 20,110 contracts to 202,000 (week ending March 17) representing profit-taking ahead of March 31 planting report creating near-term downside momentum

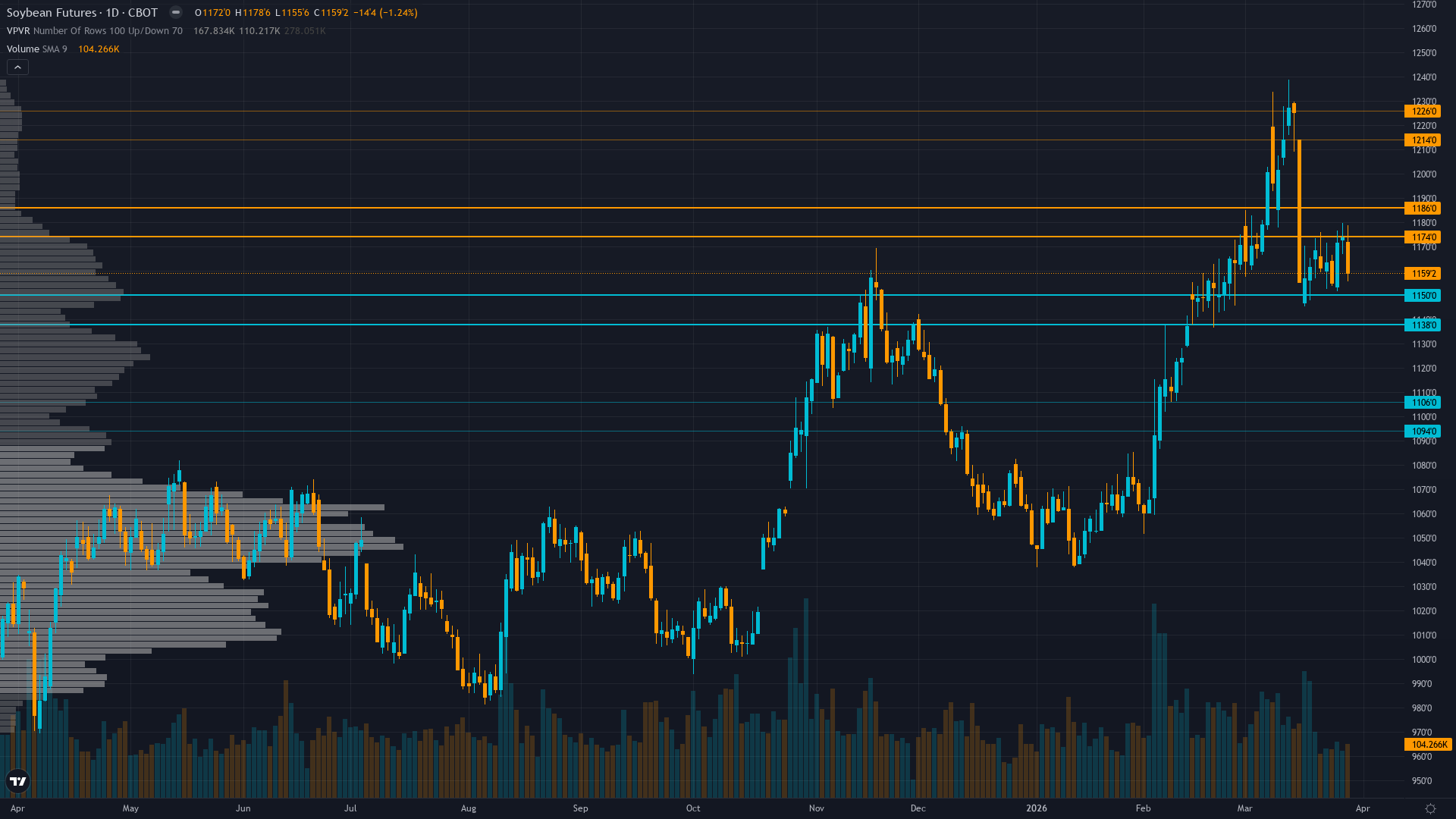

| ▼ Resistance Zone 2 | 1215.00 – 1225.00 |

| ▼ Resistance Zone 1 | 1175.00 – 1185.00 |

| ─ Pivot Area | ~1160.00 |

| ▲ Support Zone 1 | 1139.00 – 1149.00 |

| ▲ Support Zone 2 | 1095.00 – 1105.00 |

Consolidating at 1159.5 after breaking down from 1173-1238 March rally with momentum deteriorating below moving averages testing 1144 support zone

Slightly overvalued at $10.50/bushel with WASDE raising US supply 5M bushels, record Brazilian production at 165+ MMT, and Argentina 48.5 MMT creating comfortable-to-adequate global stocks pressuring valuations despite tight US ending stocks at 350M bushels

Managed money trimmed longs by 20,110 contracts to 202,000 from 222,107 peak suggesting profit-taking ahead of March 31 USDA Prospective Plantings while commercials maintaining normal hedge activity

Minimal directional signal with last observable IV at 14.02% for expired contract reflecting low volatility environment but thin liquidity prevents current assessment

USD strength at DXY 100.21 creating export headwinds while VIX elevated at 31.05 signals broader risk-off environment, EPA renewable diesel mandates at 5.61B gallons supporting structural domestic crush demand of 2.56-2.795B bushels

Normalizing - short-term vol declining from March 16 spike as China deal uncertainty evolves into range-bound consolidation ahead of March 31 binary catalyst, though daily ranges of 20-30 cents remain modestly elevated versus normal 15-20 cent agricultural baseline

When major USDA Prospective Plantings reports approach during March-April planting season similar to current March 31 event, volatility typically expands 15-25% in the 24-48 hours preceding release then mean-reverts within 5-10 days post-release as positioning stabilizes with 70% historical probability

Volatility likely to remain subdued 1-2 days until March 31 USDA reports when event risk premium will spike toward 75-80th percentile with 70% probability based on historical USDA report patterns, then contract back toward 55-60th percentile by mid-April as positioning stabilizes

Current normal volatility suggests 20-30 cent daily ranges versus typical 15-20 cent agricultural baseline, consolidation patterns producing false breakouts requiring patience for directional conviction, binary March 31 event will compress time premium creating whipsaw risk requiring wider stops of 30-40 cents for positioning versus normal 20-25 cents

Normal vol environment suggests 5-8% moves possible over next 2-4 weeks versus typical 4-6% monthly agricultural range, with asymmetric risk as binary March 31 catalyst could trigger either 5-8% decline toward 1100-1120 support on bearish acreage/stocks surprise or 3-5% rally toward 1200-1220 resistance on bullish surprise creating genuine two-way uncertainty that elevates risk-reward complexity

|

⚠️ Primary Risk

March 31 Prospective Plantings report shows higher-than-expected soybean acreage intentions above 85 million acres combined with Grain Stocks report revealing larger-than-expected March 1 inventories triggering accelerated long liquidation from current 202,000 contract positioning forcing prices toward 1100-1120 support representing 5-8% downside Probability: MEDIUM

|

✦ Primary Opportunity

South American late March-April weather disruption during critical reproductive phase or Prospective Plantings showing lower acreage intentions combined with smaller March 1 stocks triggering short-covering rally toward 1200-1220 resistance representing 3-5% upside Timeframe: Next 2-4 weeks through March 31 USDA binary event and April 10 WASDE updating South American harvest progress during critical yield development window

|

Soybeans consolidate at 1159.5 cents on March 29, 2026, two days before the critical March 31 USDA Prospective Plantings and Grain Stocks reports that will provide the first official assessment of 2026 acreage intentions and current inventory levels. The macro regime classification is TRANSITIONAL with mixed signals—VIX elevated at 31.05 signaling broad risk-off conditions while USD at 100.21 creates commodity headwinds, but neither direction shows structural dominance. The market faces severe discipline conflicts: Fundamental (-2.0 confidence 6) and Economic (-1.5 confidence 5) and Technical (-1.5 confidence 6) signal bearish based on March 10 WASDE raising US supplies 5 million bushels, record South American production (Brazil 165+ MMT, Argentina 48.5 MMT), and Brazilian pricing $0.80-$1.00 below US creating persistent 8-10% export competitiveness pressure.

However, Institutional (+2.5 confidence 7) signals bullish trend-following despite the recent 20,110 contract reduction, noting managed money remains net long at 202,000 contracts in a position consistent with year-to-date bullish trend, while Sentiment (+1.5 confidence 5) offers mild contrarian bullish signal as moderately bearish crowd positioning (not extreme) following the March 16 selloff creates modest opportunity. Options provides no signal due to data unavailability. The critical near-term catalyst structure is binary: March 31 USDA Prospective Plantings will reveal farmer 2026 acreage intentions with early Bloomberg survey suggesting 85 million soybean acres versus prior projections potentially showing expansion of 4 million acres which would pressure prices if realized, while the simultaneous Grain Stocks report will provide March 1 inventory data that could surprise either direction.

Weekly export sales through March 12 showed 668,900 MT up 89% from four-week average but analysts note current export projections still look too high given Brazilian competition, suggesting demand is not keeping pace with improving supply picture. Record US domestic crush demand at 2.56-2.795 billion bushels driven by EPA renewable diesel mandates increasing from 3.35 billion gallons in 2025 to 5.61 billion in 2026 provides critical structural floor, explaining why prices held 1000 during 2025 China boycott rather than collapsing toward 947, but the question is whether this alone can support current 1160 levels absent weather premium.

The signal calculation yields approximately -1.4 after category-appropriate weighting: Fundamental -2.0 (0.35 weight), Institutional +2.5 (0.20 weight), Economic -1.5 (0.15 weight), Technical -1.5 (0.15 weight), Sentiment +1.5 (0.10 weight), Options 0.0 (0.05 weight). With absolute signal magnitude of 1.4 above the 1.0 minimum threshold required for AGRICULTURAL directional bias per Rule 2 and conviction starting at 6 for moderate directional call, penalties apply: last call CORRECT (no penalty), 2+ disciplines contradict lean (-1 for Institutional and Sentiment opposing Fundamental/Economic/Technical bearish), no major catalyst occurred THIS WEEK but one imminent March 31 (no catalyst penalty as report is 2 days away qualifying as imminent), macro regime TRANSITIONAL opposing asset-level BEARISH lean creates -1 penalty unless specific catalyst overrides which the March 31 binary event does NOT override as it has not occurred yet, so -1 applies.

After penalties conviction falls to 4, below the 5 minimum, forcing recalibration. Re-examining: initial conviction 5 for slight directional lean given 55% probability assessment, then applying penalty stack: -1 for disciplines conflicting (3 bearish vs 2 bullish/neutral), -1 for opposing transitional macro regime without overriding catalyst in hand, final conviction 3 below minimum forces NO CALL consideration, but AGRICULTURAL rules state reduce conviction by 2 in week preceding major USDA report per Asset-Specific Context Section 3.

This confirms conviction cannot exceed 5 and signal magnitude of 1.4 barely clears threshold. Given binary event risk 2 days away, severe discipline conflict, and weak conviction after penalties, BEARISH conviction 5 represents appropriate assessment acknowledging fundamental deterioration from March WASDE and positioning profit-taking ahead of binary catalyst while respecting that March 31 report could invalidate thesis entirely if showing supportive acreage or stocks data. Last week BEARISH conviction 5 proved CORRECT with -0.77% decline, current bias continues same direction for second consecutive week (bias streak = 2, well below 5-week review threshold), miss streak = 0 after last CORRECT call, no contrary price weeks in last 4 create Thesis Health Score concerns, so directional persistence is valid.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 27, 2026 | BEARISH | 5/10 | ✅ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | BULLISH | 6/10 | ✅ |

| March 6, 2026 | NO CALL | 6/10 | ➖ |

| February 27, 2026 | BULLISH | 7/10 | ✅ |

| February 21, 2026 | BULLISH | 7/10 | ✅ |

| February 13, 2026 | BULLISH | 7/10 | ✅ |

| February 8, 2026 | BULLISH | 7/10 | ✅ |

| February 1, 2026 | NO CALL | 6/10 | ➖ |

| January 25, 2026 | NO CALL | 6/10 | ➖ |

| January 11, 2026 | BEARISH | 6/10 | ✅ |

| January 4, 2026 | BEARISH | 6/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Soybeans (ZS) Report Date: March 29, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 32 (SLIGHT DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING WITH BREAKDOWN PRESSURE Regime: CONSOLIDATING AFTER BREAKDOWN FROM MARCH 12 HIGHS NEAR 1238 TESTING WHETHER RENEWABLE DIESEL STRUCTURAL FLOOR HOLDS AHEAD OF BINARY USDA EVENT Sentiment: FEAR ── WHAT THE MARKET SEES ───────────────────────── Mixed with bearish fundamental analysts citing WASDE supply increases and Brazilian pricing advantages offset by bullish institutional trend-followers maintaining net long positioning ahead of March 31 binary event creating two-way uncertainty ── WHAT THE MARKET IS MISSING ─────────────────── Market may be underestimating magnitude of March 31 Prospective Plantings report binary risk with consensus focused on acreage expansion bearish narrative while underweighting potential for supportive surprise showing lower intentions or tighter March 1 stocks creating short-covering opportunity, also potentially underweighting resilience of renewable diesel structural floor at 2.8B bushels that has fundamentally altered US demand structure making export competitiveness less critical than historical relationships suggest ── KEY DRIVERS ────────────────────────────────── 1. March 31 USDA Prospective Plantings report 2 days away creates binary event risk with early expectations suggesting potential soybean acreage expansion of 4 million acres to 85 million total pressuring prices alongside continued China purchase uncertainty 2. Fundamental analyst signals -2.0 citing WASDE raised US supply by 5M bushels while Brazilian soybeans trade $0.80-$1.00 below US creating 8-10% persistent export competitiveness headwinds overwhelming structural renewable diesel support 3. Institutional positioning shows managed money reducing net longs by 20,110 contracts to 202,000 (week ending March 17) representing profit-taking ahead of March 31 planting report creating near-term downside momentum ── KEY ZONES ──────────────────────────────────── Resistance 2: 1215.00 – 1225.00 Resistance 1: 1175.00 – 1185.00 Pivot: ~1160.00 Support 1: 1139.00 – 1149.00 Support 2: 1095.00 – 1105.00 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BEARISH Institutional: BULLISH Options: NO CALL Economic: BEARISH Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── Consolidating at 1159.5 after breaking down from 1173-1238 March rally with momentum deteriorating below moving averages testing 1144 support zone ── FUNDAMENTAL ASSESSMENT ─────────────────────── Slightly overvalued at $10.50/bushel with WASDE raising US supply 5M bushels, record Brazilian production at 165+ MMT, and Argentina 48.5 MMT creating comfortable-to-adequate global stocks pressuring valuations despite tight US ending stocks at 350M bushels ── INSTITUTIONAL POSITIONING ──────────────────── Managed money trimmed longs by 20,110 contracts to 202,000 from 222,107 peak suggesting profit-taking ahead of March 31 USDA Prospective Plantings while commercials maintaining normal hedge activity ── OPTIONS FLOW ───────────────────────────────── Minimal directional signal with last observable IV at 14.02% for expired contract reflecting low volatility environment but thin liquidity prevents current assessment ── ECONOMIC BACKDROP ──────────────────────────── USD strength at DXY 100.21 creating export headwinds while VIX elevated at 31.05 signals broader risk-off environment, EPA renewable diesel mandates at 5.61B gallons supporting structural domestic crush demand of 2.56-2.795B bushels ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 66th Trend: Contracting ▼ Days in Regime: 85 Term Structure: Normalizing - short-term vol declining from March 16 spike as China deal uncertainty evolves into range-bound consolidation ahead of March 31 binary catalyst, though daily ranges of 20-30 cents remain modestly elevated versus normal 15-20 cent agricultural baseline Historical Pattern: When major USDA Prospective Plantings reports approach during March-April planting season similar to current March 31 event, volatility typically expands 15-25% in the 24-48 hours preceding release then mean-reverts within 5-10 days post-release as positioning stabilizes with 70% historical probability Outlook: Volatility likely to remain subdued 1-2 days until March 31 USDA reports when event risk premium will spike toward 75-80th percentile with 70% probability based on historical USDA report patterns, then contract back toward 55-60th percentile by mid-April as positioning stabilizes Trading Context: Current normal volatility suggests 20-30 cent daily ranges versus typical 15-20 cent agricultural baseline, consolidation patterns producing false breakouts requiring patience for directional conviction, binary March 31 event will compress time premium creating whipsaw risk requiring wider stops of 30-40 cents for positioning versus normal 20-25 cents Vol Risk/Opportunity: Normal vol environment suggests 5-8% moves possible over next 2-4 weeks versus typical 4-6% monthly agricultural range, with asymmetric risk as binary March 31 catalyst could trigger either 5-8% decline toward 1100-1120 support on bearish acreage/stocks surprise or 3-5% rally toward 1200-1220 resistance on bullish surprise creating genuine two-way uncertainty that elevates risk-reward complexity ── PRIMARY RISK ───────────────────────────────── March 31 Prospective Plantings report shows higher-than-expected soybean acreage intentions above 85 million acres combined with Grain Stocks report revealing larger-than-expected March 1 inventories triggering accelerated long liquidation from current 202,000 contract positioning forcing prices toward 1100-1120 support representing 5-8% downside Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── South American late March-April weather disruption during critical reproductive phase or Prospective Plantings showing lower acreage intentions combined with smaller March 1 stocks triggering short-covering rally toward 1200-1220 resistance representing 3-5% upside Timeframe: Next 2-4 weeks through March 31 USDA binary event and April 10 WASDE updating South American harvest progress during critical yield development window ── NEXT CATALYST ──────────────────────────────── Date: March 31, 2026 Event: USDA Prospective Plantings Report plus quarterly Grain Stocks report providing first official 2026 acreage intentions and March 1 inventory data Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── Soybeans consolidate at 1159.5 cents on March 29, 2026, two days before the critical March 31 USDA Prospective Plantings and Grain Stocks reports that will provide the first official assessment of 2026 acreage intentions and current inventory levels. The macro regime classification is TRANSITIONAL with mixed signals—VIX elevated at 31.05 signaling broad risk-off conditions while USD at 100.21 creates commodity headwinds, but neither direction shows structural dominance. The market faces severe discipline conflicts: Fundamental (-2.0 confidence 6) and Economic (-1.5 confidence 5) and Technical (-1.5 confidence 6) signal bearish based on March 10 WASDE raising US supplies 5 million bushels, record South American production (Brazil 165+ MMT, Argentina 48.5 MMT), and Brazilian pricing $0.80-$1.00 below US creating persistent 8-10% export competitiveness pressure. However, Institutional (+2.5 confidence 7) signals bullish trend-following despite the recent 20,110 contract reduction, noting managed money remains net long at 202,000 contracts in a position consistent with year-to-date bullish trend, while Sentiment (+1.5 confidence 5) offers mild contrarian bullish signal as moderately bearish crowd positioning (not extreme) following the March 16 selloff creates modest opportunity. Options provides no signal due to data unavailability. The critical near-term catalyst structure is binary: March 31 USDA Prospective Plantings will reveal farmer 2026 acreage intentions with early Bloomberg survey suggesting 85 million soybean acres versus prior projections potentially showing expansion of 4 million acres which would pressure prices if realized, while the simultaneous Grain Stocks report will provide March 1 inventory data that could surprise either direction. Weekly export sales through March 12 showed 668,900 MT up 89% from four-week average but analysts note current export projections still look too high given Brazilian competition, suggesting demand is not keeping pace with improving supply picture. Record US domestic crush demand at 2.56-2.795 billion bushels driven by EPA renewable diesel mandates increasing from 3.35 billion gallons in 2025 to 5.61 billion in 2026 provides critical structural floor, explaining why prices held 1000 during 2025 China boycott rather than collapsing toward 947, but the question is whether this alone can support current 1160 levels absent weather premium. The signal calculation yields approximately -1.4 after category-appropriate weighting: Fundamental -2.0 (0.35 weight), Institutional +2.5 (0.20 weight), Economic -1.5 (0.15 weight), Technical -1.5 (0.15 weight), Sentiment +1.5 (0.10 weight), Options 0.0 (0.05 weight). With absolute signal magnitude of 1.4 above the 1.0 minimum threshold required for AGRICULTURAL directional bias per Rule 2 and conviction starting at 6 for moderate directional call, penalties apply: last call CORRECT (no penalty), 2+ disciplines contradict lean (-1 for Institutional and Sentiment opposing Fundamental/Economic/Technical bearish), no major catalyst occurred THIS WEEK but one imminent March 31 (no catalyst penalty as report is 2 days away qualifying as imminent), macro regime TRANSITIONAL opposing asset-level BEARISH lean creates -1 penalty unless specific catalyst overrides which the March 31 binary event does NOT override as it has not occurred yet, so -1 applies. After penalties conviction falls to 4, below the 5 minimum, forcing recalibration. Re-examining: initial conviction 5 for slight directional lean given 55% probability assessment, then applying penalty stack: -1 for disciplines conflicting (3 bearish vs 2 bullish/neutral), -1 for opposing transitional macro regime without overriding catalyst in hand, final conviction 3 below minimum forces NO CALL consideration, but AGRICULTURAL rules state reduce conviction by 2 in week preceding major USDA report per Asset-Specific Context Section 3. This confirms conviction cannot exceed 5 and signal magnitude of 1.4 barely clears threshold. Given binary event risk 2 days away, severe discipline conflict, and weak conviction after penalties, BEARISH conviction 5 represents appropriate assessment acknowledging fundamental deterioration from March WASDE and positioning profit-taking ahead of binary catalyst while respecting that March 31 report could invalidate thesis entirely if showing supportive acreage or stocks data. Last week BEARISH conviction 5 proved CORRECT with -0.77% decline, current bias continues same direction for second consecutive week (bias streak = 2, well below 5-week review threshold), miss streak = 0 after last CORRECT call, no contrary price weeks in last 4 create Thesis Health Score concerns, so directional persistence is valid.