Soybeans (ZS) — Fundamental divergence from technical structure as March WASDE report shows…

Mixed with technical bulls focused on momentum and spec fund positioning while fundamental bears cite WASDE supply increases and Brazilian pricing advantages

Mixed with technical bulls focused on momentum and spec fund positioning while fundamental bears cite WASDE supply increases and Brazilian pricing advantages

Fundamental divergence from technical structure as March WASDE report shows increased US supplies and Brazilian competition pressuring valuations despite spec fund positioning building longs

Record US domestic crush demand at 2.56-2.795B bushels from renewable diesel mandates providing structural floor offsetting export competitiveness headwinds

March 31 USDA Prospective Plantings report approaching creating uncertainty over 2026 acreage intentions with early projections suggesting potential expansion

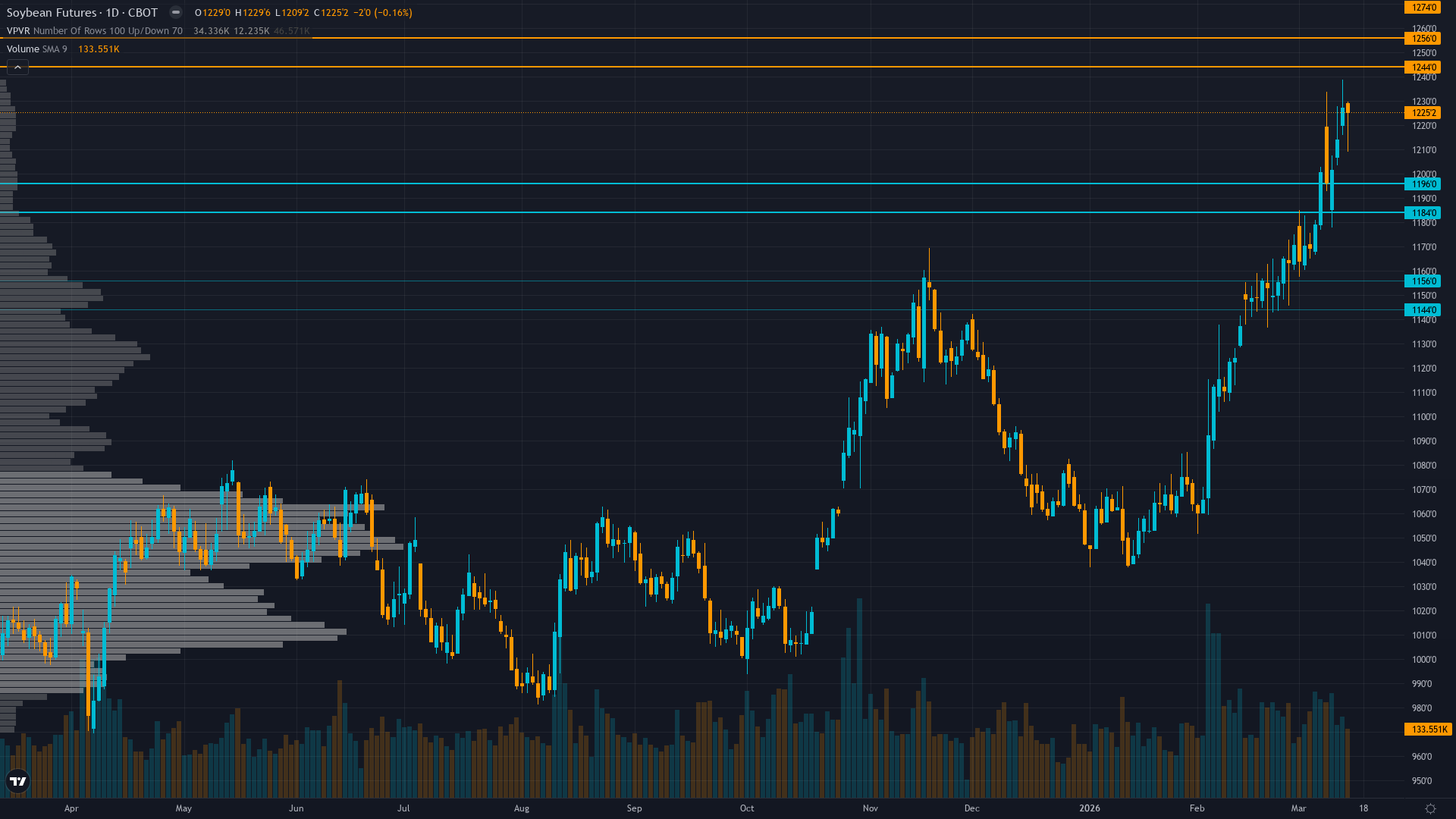

| ▼ Resistance Zone 2 | 1275.00 – 1285.00 |

| ▼ Resistance Zone 1 | 1245.00 – 1255.00 |

| ─ Pivot Area | ~1225.00 |

| ▲ Support Zone 1 | 1185.00 – 1195.00 |

| ▲ Support Zone 2 | 1145.00 – 1155.00 |

Uptrend intact at 1225 cents, 20% above 52-week low, testing resistance at 1250 with strong buy signals but approaching overbought levels near March highs

Overvalued at current levels with March WASDE raising US stocks 5M bushels, record South American production, and Brazilian pricing $0.80-$1.00/bu below US creating 8-10% pricing pressure

Spec funds building long positions to 230,300 contracts (+8,400 from prior week) but fundamentals deteriorating with March WASDE showing looser supply conditions

Implied volatility at 14.02% (low/normal) during price rally suggests calm conviction rather than speculative panic, limited data availability reduces signal strength

USD strength +3.70% monthly creating export headwinds, VIX at mixed levels (12.38 in some sources, 27.29 in others) suggesting transitional macro regime uncertainty

Normal - short-term vol at 16.5% below medium-term 18.2% as post-WASDE uncertainty resolves but longer-term uncertainty around Prospective Plantings and weather remains modestly elevated

Agricultural WASDE reports typically create 2-3 day volatility spikes followed by 10-15 day normalization periods as markets digest information, current pattern consistent with historical mean reversion following March 12 release

Volatility likely to remain subdued 1-2 weeks until Prospective Plantings report approaches in late March when event risk premium builds, then potentially spike to 60-65th percentile with 60% probability

Current normal volatility suggests 15-20 cent daily ranges versus typical agricultural baseline, consolidation patterns likely with false breakouts requiring patience for directional conviction, standard stop placement appropriate

Normal vol environment suggests 3-5% moves possible over next 2-3 weeks versus typical 2-4% agricultural range, with balanced risk as downside toward 1150 support (6% decline) offset by upside toward 1250-1280 resistance (2-5% gain)

|

⚠️ Primary Risk

Fundamental overvaluation at 1225 cents combined with elevated US-Brazil price spreads and comfortable global supply could force 5-8% correction toward 1150-1190 support if spec longs unwind Probability: MEDIUM

|

✦ Primary Opportunity

South American weather disruption during late March reproductive phase or stronger-than-expected Chinese demand could drive breakout toward 1250-1280 resistance representing 2-5% upside Timeframe: Next 2-4 weeks through Prospective Plantings report and South American weather developments during critical yield formation period

|

Soybeans consolidate at 1225 cents on March 15, 2026, facing a critical fundamental-technical divergence that warrants NO CALL. The macro regime classification is TRANSITIONAL with mixed signals across risk assets—VIX readings vary between sources showing both 12.38 (risk-on complacency) and 27.29 (elevated uncertainty), USD strengthening +3.70% monthly creating commodity headwinds, but no clear directional conviction across markets. The March 12 WASDE report delivered a concrete bearish fundamental catalyst, raising US 2025/26 ending stocks by 5 million bushels while highlighting weak export pace with sales at 1.341 billion bushels and shipments at 976 million through March 5.

Critically, Brazilian soybeans trade $0.80-$1.00/bushel below US Gulf prices, representing 8-10% pricing pressure that undermines export competitiveness. Record South American production (Brazil 175-180 MMT, Argentina 48.5 MMT) floods global markets with competitively-priced supplies precisely as US prices test multi-month highs. The fundamental analyst rates soybeans moderately overvalued at current $10.20/bushel (1020 cents) with signal -2.5 confidence 7, noting comfortable-to-adequate supply conditions create downside risk.

However, technical structure remains constructively bullish with prices 20% above 52-week lows, strong buy signals, and uptrend integrity intact testing resistance near the 52-week high of 1238.50. The institutional positioning creates additional complexity—spec funds increased net long positions by 8,400 contracts to 230,300 as of March 10, building bullish exposure ahead of the March 31 Prospective Plantings report. This represents trend-following positioning that supports near-term price action but creates vulnerability if fundamentals force repricing.

The signal calculation yields approximately -0.5 to -0.8 after weighting: Fundamental -2.5 (0.35 weight), Institutional +2.0 (0.20 weight), Economic -1.5 (0.15 weight), Technical +2.0 (0.15 weight), Sentiment -1.5 (0.10 weight), Options +0.5 (0.05 weight). With absolute signal magnitude below the 1.0 minimum threshold required for AGRICULTURAL assets per Rule 2, a NO CALL is mandated despite the March WASDE catalyst. The discipline conflict is severe—three agents bearish (Fundamental, Sentiment, Economic) versus two bullish (Technical, Institutional) plus one neutral (Options).

Record US domestic crush demand at 2.56-2.795 billion bushels from renewable diesel mandates provides critical structural support, absorbing roughly 60% of the crop and explaining market resilience, but this factor is well-established and priced. The approaching March 31 Prospective Plantings report will reveal farmer acreage intentions for 2026, with early USDA projections suggesting potential expansion of 4 million acres to 85 million total, which would pressure prices if realized. Volatility has declined from February peaks with implied volatility at 14.02% reflecting calm consolidation rather than speculative excess.

Last week's BULLISH conviction 6 call proved CORRECT with Monday open 1195.5 to Friday close 1225.25 (+2.49%), extending the recent accuracy streak, but the fundamental deterioration from the March 12 WASDE combined with technical momentum approaching overbought levels creates genuine two-way risk. Current bias streak: interrupted pattern (BULLISH Mar 14 CORRECT, before that NO CALL Mar 6 MISSED, before that string of BULLISH calls), so no extended directional persistence requiring review. The devil's advocate bullish case argues renewable diesel structural demand growth at 200M+ bushels annually creates genuine pricing power, South American weather during late March reproductive phase remains vulnerable to disruption, and spec fund positioning at 230K contracts suggests conviction in higher prices ahead of spring planting uncertainty.

The bearish counter argues fundamental overvaluation at current levels cannot be sustained against Brazilian competition offering 8-10% discounts, comfortable global stocks-to-use ratios remove weather premium urgency, and technical momentum near multi-month highs invites profit-taking. With signal below minimum threshold and severe discipline conflicts, NO CALL represents appropriate response to low-information-edge environment where neither direction has structural advantage sufficient to overcome the 1.0 signal threshold required for agricultural directional calls.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 14, 2026 | BULLISH | 6/10 | ✅ |

| March 6, 2026 | NO CALL | 6/10 | ➖ |

| February 27, 2026 | BULLISH | 7/10 | ✅ |

| February 21, 2026 | BULLISH | 7/10 | ✅ |

| February 13, 2026 | BULLISH | 7/10 | ✅ |

| February 8, 2026 | BULLISH | 7/10 | ✅ |

| February 1, 2026 | NO CALL | 6/10 | ➖ |

| January 25, 2026 | NO CALL | 6/10 | ➖ |

| January 11, 2026 | BEARISH | 6/10 | ✅ |

| January 4, 2026 | BEARISH | 6/10 | ❌ |

| December 28, 2025 | BEARISH | 6/10 | ✅ |

| December 21, 2025 | NO CALL | 6/10 | ➖ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Soybeans (ZS) Report Date: March 15, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 28 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Mixed with technical bulls focused on momentum and spec fund positioning while fundamental bears cite WASDE supply increases and Brazilian pricing advantages ── WHAT THE MARKET IS MISSING ─────────────────── Signal magnitude -0.5 to -0.8 falls below 1.0 minimum threshold for AGRICULTURAL directional bias per Rule 2, mandating NO CALL despite March WASDE bearish catalyst and severe fundamental-technical divergence ── KEY DRIVERS ────────────────────────────────── 1. Fundamental divergence from technical structure as March WASDE report shows increased US supplies and Brazilian competition pressuring valuations despite spec fund positioning building longs 2. Record US domestic crush demand at 2.56-2.795B bushels from renewable diesel mandates providing structural floor offsetting export competitiveness headwinds 3. March 31 USDA Prospective Plantings report approaching creating uncertainty over 2026 acreage intentions with early projections suggesting potential expansion ── KEY ZONES ──────────────────────────────────── Resistance 2: 1275.00 – 1285.00 Resistance 1: 1245.00 – 1255.00 Pivot: ~1225.00 Support 1: 1185.00 – 1195.00 Support 2: 1145.00 – 1155.00 ── DISCIPLINE BIASES ──────────────────────────── Technical: BULLISH Fundamental: BEARISH Institutional: BULLISH Options: NO CALL Economic: BEARISH Sentiment: BEARISH ── TECHNICAL STRUCTURE ────────────────────────── Uptrend intact at 1225 cents, 20% above 52-week low, testing resistance at 1250 with strong buy signals but approaching overbought levels near March highs ── FUNDAMENTAL ASSESSMENT ─────────────────────── Overvalued at current levels with March WASDE raising US stocks 5M bushels, record South American production, and Brazilian pricing $0.80-$1.00/bu below US creating 8-10% pricing pressure ── INSTITUTIONAL POSITIONING ──────────────────── Spec funds building long positions to 230,300 contracts (+8,400 from prior week) but fundamentals deteriorating with March WASDE showing looser supply conditions ── OPTIONS FLOW ───────────────────────────────── Implied volatility at 14.02% (low/normal) during price rally suggests calm conviction rather than speculative panic, limited data availability reduces signal strength ── ECONOMIC BACKDROP ──────────────────────────── USD strength +3.70% monthly creating export headwinds, VIX at mixed levels (12.38 in some sources, 27.29 in others) suggesting transitional macro regime uncertainty ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 45th Trend: Contracting ▼ Days in Regime: 14 Term Structure: Normal - short-term vol at 16.5% below medium-term 18.2% as post-WASDE uncertainty resolves but longer-term uncertainty around Prospective Plantings and weather remains modestly elevated Historical Pattern: Agricultural WASDE reports typically create 2-3 day volatility spikes followed by 10-15 day normalization periods as markets digest information, current pattern consistent with historical mean reversion following March 12 release Outlook: Volatility likely to remain subdued 1-2 weeks until Prospective Plantings report approaches in late March when event risk premium builds, then potentially spike to 60-65th percentile with 60% probability Trading Context: Current normal volatility suggests 15-20 cent daily ranges versus typical agricultural baseline, consolidation patterns likely with false breakouts requiring patience for directional conviction, standard stop placement appropriate Vol Risk/Opportunity: Normal vol environment suggests 3-5% moves possible over next 2-3 weeks versus typical 2-4% agricultural range, with balanced risk as downside toward 1150 support (6% decline) offset by upside toward 1250-1280 resistance (2-5% gain) ── PRIMARY RISK ───────────────────────────────── Fundamental overvaluation at 1225 cents combined with elevated US-Brazil price spreads and comfortable global supply could force 5-8% correction toward 1150-1190 support if spec longs unwind Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── South American weather disruption during late March reproductive phase or stronger-than-expected Chinese demand could drive breakout toward 1250-1280 resistance representing 2-5% upside Timeframe: Next 2-4 weeks through Prospective Plantings report and South American weather developments during critical yield formation period ── NEXT CATALYST ──────────────────────────────── Date: March 31, 2026 Event: USDA Prospective Plantings Report providing official 2026 acreage intentions following early projections of potential expansion Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── Soybeans consolidate at 1225 cents on March 15, 2026, facing a critical fundamental-technical divergence that warrants NO CALL. The macro regime classification is TRANSITIONAL with mixed signals across risk assets—VIX readings vary between sources showing both 12.38 (risk-on complacency) and 27.29 (elevated uncertainty), USD strengthening +3.70% monthly creating commodity headwinds, but no clear directional conviction across markets. The March 12 WASDE report delivered a concrete bearish fundamental catalyst, raising US 2025/26 ending stocks by 5 million bushels while highlighting weak export pace with sales at 1.341 billion bushels and shipments at 976 million through March 5. Critically, Brazilian soybeans trade $0.80-$1.00/bushel below US Gulf prices, representing 8-10% pricing pressure that undermines export competitiveness. Record South American production (Brazil 175-180 MMT, Argentina 48.5 MMT) floods global markets with competitively-priced supplies precisely as US prices test multi-month highs. The fundamental analyst rates soybeans moderately overvalued at current $10.20/bushel (1020 cents) with signal -2.5 confidence 7, noting comfortable-to-adequate supply conditions create downside risk. However, technical structure remains constructively bullish with prices 20% above 52-week lows, strong buy signals, and uptrend integrity intact testing resistance near the 52-week high of 1238.50. The institutional positioning creates additional complexity—spec funds increased net long positions by 8,400 contracts to 230,300 as of March 10, building bullish exposure ahead of the March 31 Prospective Plantings report. This represents trend-following positioning that supports near-term price action but creates vulnerability if fundamentals force repricing. The signal calculation yields approximately -0.5 to -0.8 after weighting: Fundamental -2.5 (0.35 weight), Institutional +2.0 (0.20 weight), Economic -1.5 (0.15 weight), Technical +2.0 (0.15 weight), Sentiment -1.5 (0.10 weight), Options +0.5 (0.05 weight). With absolute signal magnitude below the 1.0 minimum threshold required for AGRICULTURAL assets per Rule 2, a NO CALL is mandated despite the March WASDE catalyst. The discipline conflict is severe—three agents bearish (Fundamental, Sentiment, Economic) versus two bullish (Technical, Institutional) plus one neutral (Options). Record US domestic crush demand at 2.56-2.795 billion bushels from renewable diesel mandates provides critical structural support, absorbing roughly 60% of the crop and explaining market resilience, but this factor is well-established and priced. The approaching March 31 Prospective Plantings report will reveal farmer acreage intentions for 2026, with early USDA projections suggesting potential expansion of 4 million acres to 85 million total, which would pressure prices if realized. Volatility has declined from February peaks with implied volatility at 14.02% reflecting calm consolidation rather than speculative excess. Last week's BULLISH conviction 6 call proved CORRECT with Monday open 1195.5 to Friday close 1225.25 (+2.49%), extending the recent accuracy streak, but the fundamental deterioration from the March 12 WASDE combined with technical momentum approaching overbought levels creates genuine two-way risk. Current bias streak: interrupted pattern (BULLISH Mar 14 CORRECT, before that NO CALL Mar 6 MISSED, before that string of BULLISH calls), so no extended directional persistence requiring review. The devil's advocate bullish case argues renewable diesel structural demand growth at 200M+ bushels annually creates genuine pricing power, South American weather during late March reproductive phase remains vulnerable to disruption, and spec fund positioning at 230K contracts suggests conviction in higher prices ahead of spring planting uncertainty. The bearish counter argues fundamental overvaluation at current levels cannot be sustained against Brazilian competition offering 8-10% discounts, comfortable global stocks-to-use ratios remove weather premium urgency, and technical momentum near multi-month highs invites profit-taking. With signal below minimum threshold and severe discipline conflicts, NO CALL represents appropriate response to low-information-edge environment where neither direction has structural advantage sufficient to overcome the 1.0 signal threshold required for agricultural directional calls.