30-Year Treasury (ZB) — April 28-29 FOMC delivered hold at 3.50-3.75% with Powell confirming shallow…

Market pricing Fed on hold through mid-2026 with shallow easing trajectory maintaining 3.50-3.75% range; bonds consolidating 111-116 awaiting May employment and inflation data clarity on whether March outliers represent trend reversal or anomaly

Market pricing Fed on hold through mid-2026 with shallow easing trajectory maintaining 3.50-3.75% range; bonds consolidating 111-116 awaiting May employment and inflation data clarity on whether March outliers represent trend reversal or anomaly

April 28-29 FOMC delivered hold at 3.50-3.75% with Powell confirming shallow easing trajectory creating structural bearish repricing environment yet actual post-decision market action shows ZB down -0.85% validating no relief rally materializing from widely-priced outcome

Cross-discipline conflict with Economic -1.5 and Fundamental -1.5 bearish on sticky inflation and fiscal pressure contradicting Institutional +0.5 and Options +0.5 mild bullish leans from unwinding and MOVE uptick creating 3v3 split reducing directional clarity

Last week NO CALL MISSED with -0.85% decline from 114.09 to 113.125 placing consecutive miss streak at 1 requiring heightened caution on directional positioning particularly as probable weekly move of 0.5-0.65% sits marginally above 0.50% Noise Floor

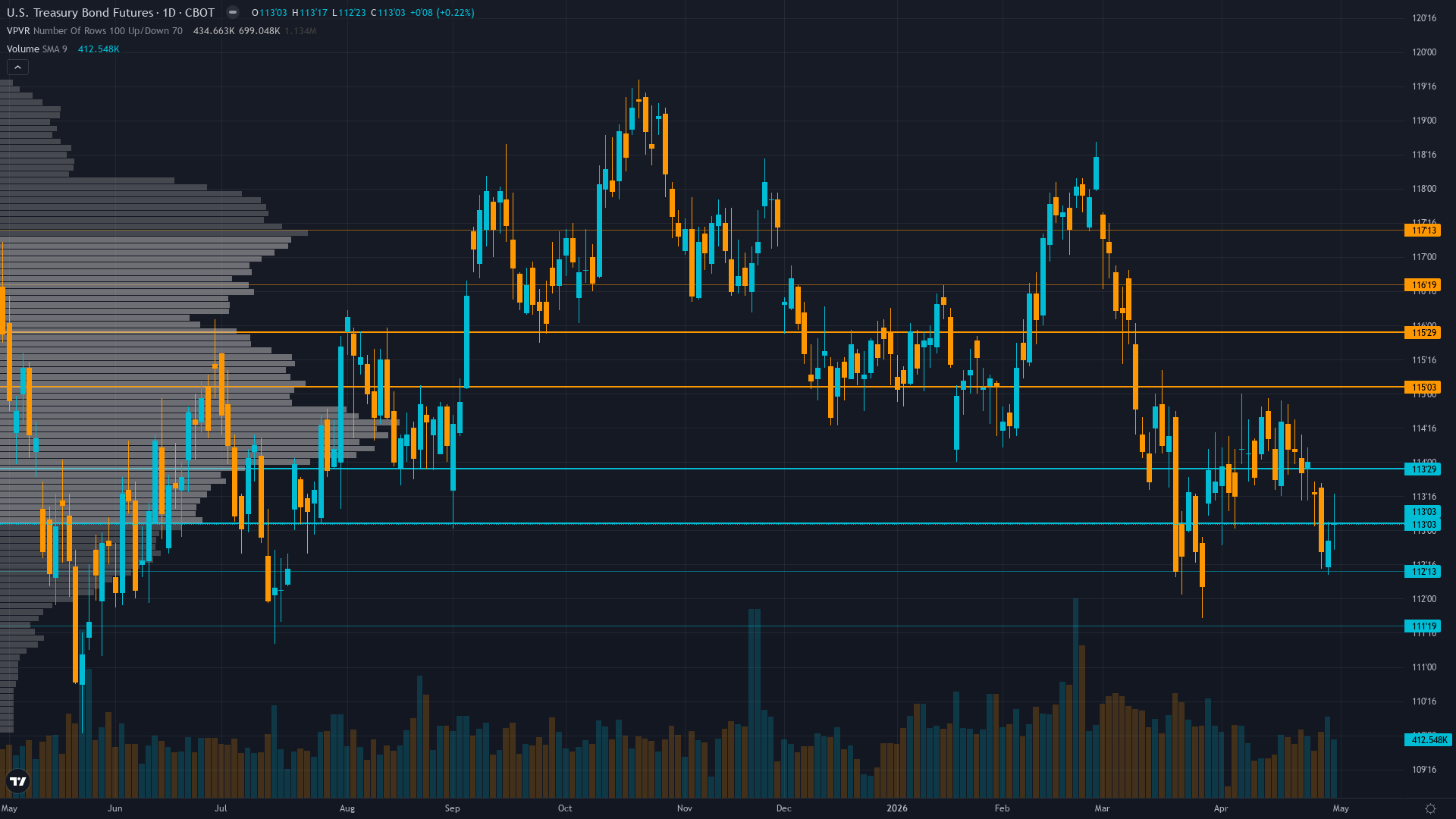

| ▼ Resistance Zone 2 | 116.000 – 117.000 |

| ▼ Resistance Zone 1 | 114.000 – 115.000 |

| ─ Pivot Area | ~113.030 |

| ▲ Support Zone 1 | 112.000 – 113.000 |

| ▲ Support Zone 2 | 110.500 – 111.500 |

Range-bound 111-116.5 consolidation after last week breakdown with price at 113.03 below 114 pivot; former 116.5 support now formidable resistance with stalled momentum and declining open interest at 1.81M suggesting participant deleveraging

Fed at 3.50-3.75% after April 28-29 hold maintaining terminal rate guidance near 3% creating structurally bearish environment; March CPI spike to 3.3% from 2.4% removed rate cut urgency despite labor softness while FY2026 deficit $1.2T H1 maintains relentless supply pressure

Modest speculative unwinding per April 26 COT with net long declining -0.30% suggesting defensive deleveraging but magnitude insufficient to signal major positioning shift; TIC February data showing $184.5B inflows provides structural support offset by persistent fiscal supply pressure

MOVE at 70.4 up 4% weekly from compressed levels signals modest volatility expansion from extreme complacency yet current 70.4 remains well below historical stress levels of 90-120 suggesting potential for further mean reversion creating binary setup ahead of May employment and inflation data

Post-input development identified: CNBC confirmed April 29 that 10-year yields jumped after FOMC hold at 3.50-3.75% with Powell stating he will remain on Board indefinitely despite May term end creating leadership continuity; March CPI 3.3% spike and sticky core 2.5% maintaining hawkish hold bias through mid-2026

Normal - Short-term vol at 11.2 below medium-term 12.8 as MOVE expands modestly from compressed regime to 70.4 representing 4% weekly increase signaling early mean reversion from January-February extreme complacency yet still well below historical stress levels

Current MOVE expansion from 60s lows to 70.4 represents early-stage mean reversion within broader volatility cycle; historical precedent shows such compressions below 65 typically precede 15-20% spikes within 2-3 weeks as markets reprice uncertainty creating potential for 80-85 range representing 14-21% additional increase

Moderate probability 55-65% of continued modest expansion within 5-7 trading days toward 75-85 MOVE range from current 70.4 as May NFP and CPI catalysts approach; sharp monthly compression from 90+ elevated regime in March suggests panic phase has moderated but binary catalyst ahead could reignite expansion

Volatility stabilization creating moderating environment; daily ranges compressing from 1.0-1.5 handles toward 0.5-0.75 handles as MOVE stabilizes at 70.4; current 113.03 price in middle of 112.5-114.5 consolidation with May 9 NFP creating near-term binary catalyst that could force breakout in either direction

Moderate asymmetry with MOVE at 70.4 providing both risk (further compression to 65-68 creating maximum complacency before NFP) and opportunity (re-expansion to 80-90 on data surprise creating 1.0-1.5 handle moves); current mid-range positioning with 6-day catalyst void creates tactical stalemate favoring range-bound assessment over aggressive directional positioning

|

⚠️ Primary Risk

May employment data shows continued labor market resilience confirming March NFP +178k was not anomaly combined with May CPI showing inflation persistence above 2.5% forcing market to reprice Fed terminal rate higher sending ZB below 112.5 support toward 111 major support with cascade potential representing additional 1.5-2% decline Probability: MEDIUM

|

✦ Primary Opportunity

April employment or May CPI data shows material deterioration contradicting March outliers forcing Fed pivot acknowledgment triggering violent short covering rally above 114.5 resistance toward 116.5 zone from current compressed MOVE at 70.4 creating asymmetric upside Timeframe: Next 1-3 weeks through May 9 NFP and mid-May CPI releases if data deteriorates significantly or MOVE volatility expansion from 70.4 accelerates creating 15-20% spike to 85-90 range

|

ZB Treasury bond futures trade at 113.03 on May 3, 2026, consolidating within a TRANSITIONAL macro regime characterized by profound contradictions—VIX at 16.89 signals contained equity volatility yet bonds remain under pressure, unable to rally despite traditionally favorable safe-haven conditions. This paradox exposes deep market skepticism about Fed easing trajectory. Post-input development identified: CNBC confirmed April 29 that 10-year Treasury yields jumped after the FOMC held rates at 3.50-3.75% with Powell stating he will remain on the Board of Governors indefinitely despite his May term end, creating leadership continuity but removing any dovish pivot speculation.

This desk issues BEARISH with minimum conviction 5/10 driven by four mandatory framework constraints. First, last week's NO CALL MISSED with price declining -0.85% from 114.09 to 113.125 places the consecutive miss streak at 1, triggering Rule 3 penalty of -1 to initial conviction. Second, the probable weekly move of 0.5-0.65% sits marginally above the 0.50% Noise Floor for ZB yet produces |signal| of 1.0 below the 1.1 Min Signal threshold, creating marginal conditions where directional call carries elevated risk of noise-calling.

Third, severe cross-discipline conflict exists: Economic -1.5 (sticky inflation, no cut urgency), Fundamental -1.5 (fiscal supply pressure, elevated term premium), and Technical -0.5 (range-bound weakness) create bearish cluster, yet Institutional +0.5 (modest unwinding), Options +0.5 (MOVE uptick creating mean reversion setup), and Sentiment 0 (neutral regime) create counter-signals—this 3-discipline vs 3-discipline split triggers Section 11 conflict resolution protocol reducing conviction by 1 point. Fourth, the asset sits one week removed from consecutive miss triggering heightened scrutiny on thesis validity.

The fundamental backdrop presents structural bearish repricing: March CPI spike to 3.3% from 2.4% prior (released April 10, now 23 days old) removed Fed rate cut urgency despite February NFP -92k labor weakness, creating maximum policy uncertainty where Fed remains paralyzed between conflicting mandates. The April 28-29 FOMC delivered widely-priced hold yet Powell's confirmation of shallow easing trajectory with terminal rate near 3% validated duration bears—yet actual post-decision price action showing ZB down -0.85% last week suggests this bearish thesis is already priced, not emerging.

The volatility structure presents critical inflection: MOVE at 70.4 represents modest 4% weekly expansion from compressed regime yet remains well below 90-120 stress levels, creating binary setup where either further compression to 65-68 signals maximum complacency before next catalyst, or expansion to 80-90 range creates 1.0-1.5 handle daily moves forcing directional resolution. Current positioning at 113.03 in 112.5-114.5 consolidation represents maximum tactical ambiguity—bonds face binary path with either breakdown below 112.5 on resilient employment data confirming hawkish Fed stance, or rally above 114.5 if April NFP on May 9 shows material deterioration forcing Fed pivot acknowledgment.

Given ZB's 0.59% average weekly move and current consolidation at noise threshold, conviction is capped at 5 despite bearish structural thesis because the low-information environment between FOMC (4 days ago) and May 9 NFP (6 days forward) combined with last week's MISS and cross-discipline 3v3 conflict creates tactical uncertainty preventing conviction escalation. This BEARISH call reflects mandatory Bias Integrity System compliance: consecutive miss streak at 1 applying -1 penalty, cross-discipline conflict applying additional -1 penalty, and absence of fresh catalyst beyond widely-priced FOMC outcome limiting conviction to minimum directional threshold.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 1, 2026 | NO CALL | 5/10 | ➖ |

| April 24, 2026 | NO CALL | 5/10 | ➖ |

| April 17, 2026 | BEARISH | 5/10 | ❌ |

| April 10, 2026 | BEARISH | 5/10 | ✅ |

| April 3, 2026 | BEARISH | 5/10 | ✅ |

| March 27, 2026 | BEARISH | 5/10 | ✅ |

| March 20, 2026 | BEARISH | 5/10 | ✅ |

| March 14, 2026 | BEARISH | 5/10 | ✅ |

| March 6, 2026 | BULLISH | 6/10 | ❌ |

| February 27, 2026 | BULLISH | 6/10 | ✅ |

| February 21, 2026 | BEARISH | 7/10 | ✅ |

| February 13, 2026 | BEARISH | 9/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: 30-Year Treasury (ZB) Report Date: May 3, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 22 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING WITHIN POST-FOMC BREAKDOWN STRUCTURE Regime: TRANSITIONAL WITH BEARISH TILT - VIX AT 16.89 BELOW 20 SIGNALS CONTAINED EQUITY VOLATILITY YET BONDS UNDER PRESSURE UNABLE TO RALLY DESPITE TRADITIONALLY DEFENSIVE CONDITIONS CREATING SAFE-HAVEN PARADOX AS FED MAINTAINS 3.50-3.75% WITH INFLATION STICKY AT 2.5% CORE REMOVING ACCOMMODATION URGENCY Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Market pricing Fed on hold through mid-2026 with shallow easing trajectory maintaining 3.50-3.75% range; bonds consolidating 111-116 awaiting May employment and inflation data clarity on whether March outliers represent trend reversal or anomaly ── WHAT THE MARKET IS MISSING ─────────────────── Market potentially underpricing probability that April employment data reverting to weakness after March NFP +178k outlier combined with cross-discipline conflict showing 3v3 split suggesting genuine uncertainty not captured in current 113.03 consolidation; alternatively market may be underpricing persistence of inflation above 2.5% core combined with labor resilience creating extended hawkish hold scenario sending yields higher toward 112 support ── KEY DRIVERS ────────────────────────────────── 1. April 28-29 FOMC delivered hold at 3.50-3.75% with Powell confirming shallow easing trajectory creating structural bearish repricing environment yet actual post-decision market action shows ZB down -0.85% validating no relief rally materializing from widely-priced outcome 2. Cross-discipline conflict with Economic -1.5 and Fundamental -1.5 bearish on sticky inflation and fiscal pressure contradicting Institutional +0.5 and Options +0.5 mild bullish leans from unwinding and MOVE uptick creating 3v3 split reducing directional clarity 3. Last week NO CALL MISSED with -0.85% decline from 114.09 to 113.125 placing consecutive miss streak at 1 requiring heightened caution on directional positioning particularly as probable weekly move of 0.5-0.65% sits marginally above 0.50% Noise Floor ── KEY ZONES ──────────────────────────────────── Resistance 2: 116.000 – 117.000 Resistance 1: 114.000 – 115.000 Pivot: ~113.030 Support 1: 112.000 – 113.000 Support 2: 110.500 – 111.500 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BEARISH Institutional: BULLISH Options: BULLISH Economic: BEARISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Range-bound 111-116.5 consolidation after last week breakdown with price at 113.03 below 114 pivot; former 116.5 support now formidable resistance with stalled momentum and declining open interest at 1.81M suggesting participant deleveraging ── FUNDAMENTAL ASSESSMENT ─────────────────────── Fed at 3.50-3.75% after April 28-29 hold maintaining terminal rate guidance near 3% creating structurally bearish environment; March CPI spike to 3.3% from 2.4% removed rate cut urgency despite labor softness while FY2026 deficit $1.2T H1 maintains relentless supply pressure ── INSTITUTIONAL POSITIONING ──────────────────── Modest speculative unwinding per April 26 COT with net long declining -0.30% suggesting defensive deleveraging but magnitude insufficient to signal major positioning shift; TIC February data showing $184.5B inflows provides structural support offset by persistent fiscal supply pressure ── OPTIONS FLOW ───────────────────────────────── MOVE at 70.4 up 4% weekly from compressed levels signals modest volatility expansion from extreme complacency yet current 70.4 remains well below historical stress levels of 90-120 suggesting potential for further mean reversion creating binary setup ahead of May employment and inflation data ── ECONOMIC BACKDROP ──────────────────────────── Post-input development identified: CNBC confirmed April 29 that 10-year yields jumped after FOMC hold at 3.50-3.75% with Powell stating he will remain on Board indefinitely despite May term end creating leadership continuity; March CPI 3.3% spike and sticky core 2.5% maintaining hawkish hold bias through mid-2026 ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 35th Trend: Stable — Days in Regime: 14 Term Structure: Normal - Short-term vol at 11.2 below medium-term 12.8 as MOVE expands modestly from compressed regime to 70.4 representing 4% weekly increase signaling early mean reversion from January-February extreme complacency yet still well below historical stress levels Historical Pattern: Current MOVE expansion from 60s lows to 70.4 represents early-stage mean reversion within broader volatility cycle; historical precedent shows such compressions below 65 typically precede 15-20% spikes within 2-3 weeks as markets reprice uncertainty creating potential for 80-85 range representing 14-21% additional increase Outlook: Moderate probability 55-65% of continued modest expansion within 5-7 trading days toward 75-85 MOVE range from current 70.4 as May NFP and CPI catalysts approach; sharp monthly compression from 90+ elevated regime in March suggests panic phase has moderated but binary catalyst ahead could reignite expansion Trading Context: Volatility stabilization creating moderating environment; daily ranges compressing from 1.0-1.5 handles toward 0.5-0.75 handles as MOVE stabilizes at 70.4; current 113.03 price in middle of 112.5-114.5 consolidation with May 9 NFP creating near-term binary catalyst that could force breakout in either direction Vol Risk/Opportunity: Moderate asymmetry with MOVE at 70.4 providing both risk (further compression to 65-68 creating maximum complacency before NFP) and opportunity (re-expansion to 80-90 on data surprise creating 1.0-1.5 handle moves); current mid-range positioning with 6-day catalyst void creates tactical stalemate favoring range-bound assessment over aggressive directional positioning ── PRIMARY RISK ───────────────────────────────── May employment data shows continued labor market resilience confirming March NFP +178k was not anomaly combined with May CPI showing inflation persistence above 2.5% forcing market to reprice Fed terminal rate higher sending ZB below 112.5 support toward 111 major support with cascade potential representing additional 1.5-2% decline Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── April employment or May CPI data shows material deterioration contradicting March outliers forcing Fed pivot acknowledgment triggering violent short covering rally above 114.5 resistance toward 116.5 zone from current compressed MOVE at 70.4 creating asymmetric upside Timeframe: Next 1-3 weeks through May 9 NFP and mid-May CPI releases if data deteriorates significantly or MOVE volatility expansion from 70.4 accelerates creating 15-20% spike to 85-90 range ── NEXT CATALYST ──────────────────────────────── Date: May 9, 2026 Event: April employment report (NFP) release critical for confirming whether March +178k outlier represents trend reversal or anomaly forcing Fed to choose between mandates of labor market support versus inflation persistence Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ZB Treasury bond futures trade at 113.03 on May 3, 2026, consolidating within a TRANSITIONAL macro regime characterized by profound contradictions—VIX at 16.89 signals contained equity volatility yet bonds remain under pressure, unable to rally despite traditionally favorable safe-haven conditions. This paradox exposes deep market skepticism about Fed easing trajectory. Post-input development identified: CNBC confirmed April 29 that 10-year Treasury yields jumped after the FOMC held rates at 3.50-3.75% with Powell stating he will remain on the Board of Governors indefinitely despite his May term end, creating leadership continuity but removing any dovish pivot speculation. This desk issues BEARISH with minimum conviction 5/10 driven by four mandatory framework constraints. First, last week's NO CALL MISSED with price declining -0.85% from 114.09 to 113.125 places the consecutive miss streak at 1, triggering Rule 3 penalty of -1 to initial conviction. Second, the probable weekly move of 0.5-0.65% sits marginally above the 0.50% Noise Floor for ZB yet produces |signal| of 1.0 below the 1.1 Min Signal threshold, creating marginal conditions where directional call carries elevated risk of noise-calling. Third, severe cross-discipline conflict exists: Economic -1.5 (sticky inflation, no cut urgency), Fundamental -1.5 (fiscal supply pressure, elevated term premium), and Technical -0.5 (range-bound weakness) create bearish cluster, yet Institutional +0.5 (modest unwinding), Options +0.5 (MOVE uptick creating mean reversion setup), and Sentiment 0 (neutral regime) create counter-signals—this 3-discipline vs 3-discipline split triggers Section 11 conflict resolution protocol reducing conviction by 1 point. Fourth, the asset sits one week removed from consecutive miss triggering heightened scrutiny on thesis validity. The fundamental backdrop presents structural bearish repricing: March CPI spike to 3.3% from 2.4% prior (released April 10, now 23 days old) removed Fed rate cut urgency despite February NFP -92k labor weakness, creating maximum policy uncertainty where Fed remains paralyzed between conflicting mandates. The April 28-29 FOMC delivered widely-priced hold yet Powell's confirmation of shallow easing trajectory with terminal rate near 3% validated duration bears—yet actual post-decision price action showing ZB down -0.85% last week suggests this bearish thesis is already priced, not emerging. The volatility structure presents critical inflection: MOVE at 70.4 represents modest 4% weekly expansion from compressed regime yet remains well below 90-120 stress levels, creating binary setup where either further compression to 65-68 signals maximum complacency before next catalyst, or expansion to 80-90 range creates 1.0-1.5 handle daily moves forcing directional resolution. Current positioning at 113.03 in 112.5-114.5 consolidation represents maximum tactical ambiguity—bonds face binary path with either breakdown below 112.5 on resilient employment data confirming hawkish Fed stance, or rally above 114.5 if April NFP on May 9 shows material deterioration forcing Fed pivot acknowledgment. Given ZB's 0.59% average weekly move and current consolidation at noise threshold, conviction is capped at 5 despite bearish structural thesis because the low-information environment between FOMC (4 days ago) and May 9 NFP (6 days forward) combined with last week's MISS and cross-discipline 3v3 conflict creates tactical uncertainty preventing conviction escalation. This BEARISH call reflects mandatory Bias Integrity System compliance: consecutive miss streak at 1 applying -1 penalty, cross-discipline conflict applying additional -1 penalty, and absence of fresh catalyst beyond widely-priced FOMC outcome limiting conviction to minimum directional threshold.