Russell 2000 (RTY) — Market consensus focused on 'Great Rotation' narrative may be underpricing…

Small-caps in 'Great Rotation' momentum with IWM surging 12%+ and Q1 earnings season beginning mid-April to test 44.9% growth consensus, but near-term caution warranted on hot CPI removing Fed easing catalyst

Small-caps in 'Great Rotation' momentum with IWM surging 12%+ and Q1 earnings season beginning mid-April to test 44.9% growth consensus, but near-term caution warranted on hot CPI removing Fed easing catalyst

VIX collapse from 23.87 to 19.23 over past week creating risk-on environment as fear recedes, combining with last week's 4.45% RTY surge validating sentiment-driven bounce thesis

Q1 2026 earnings season begins mid-April (within days) with 44.9% YoY growth consensus providing fundamental catalyst to validate small-cap rotation narrative after January ATH breakout

Hot March CPI (+1.1% MoM, +3.1% YoY) removes near-term Fed easing catalyst but market has absorbed shock, with credit spreads tightening to 3.17% signaling underlying stability

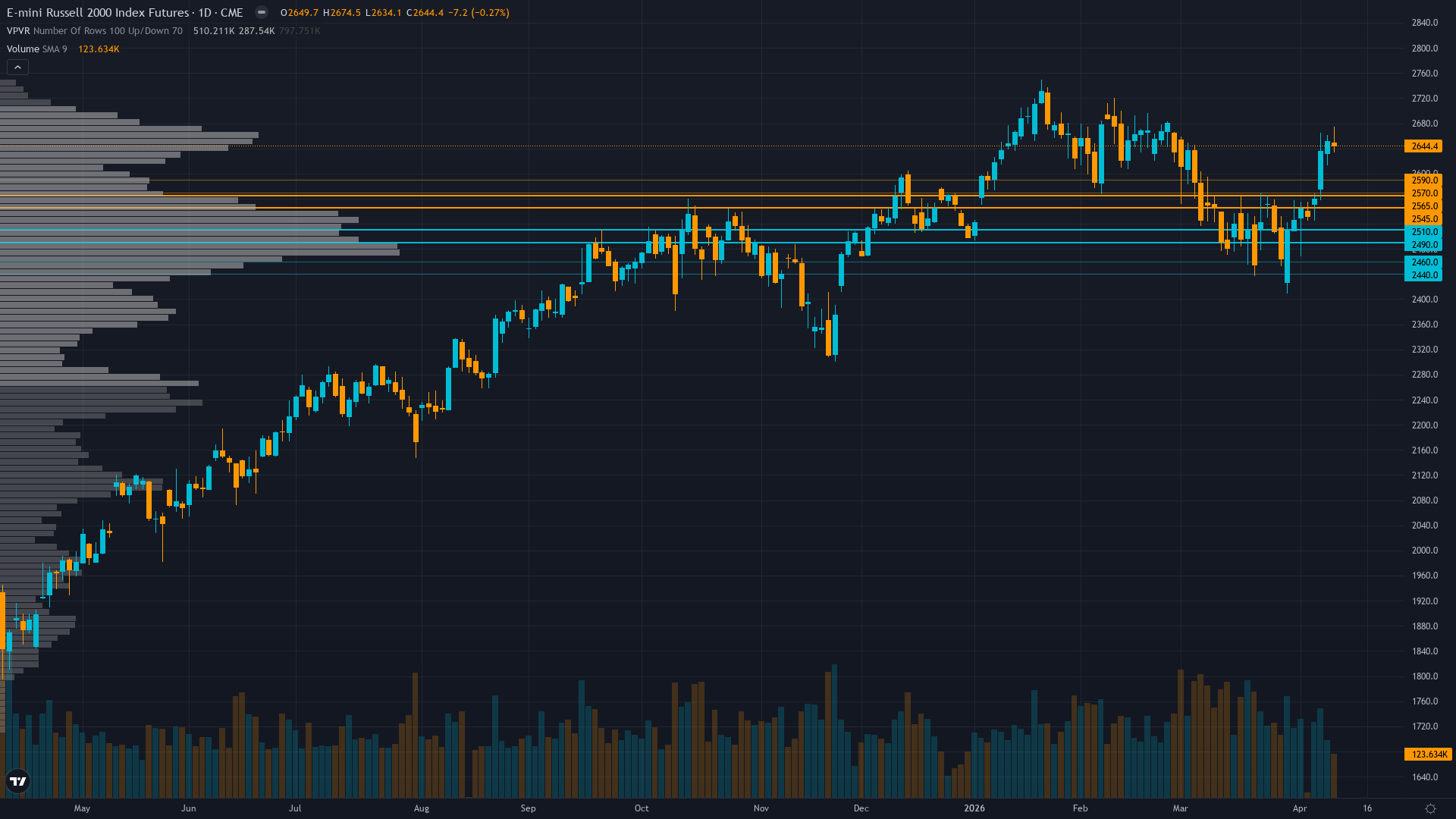

| ▼ Resistance Zone 2 | 2720 – 2750 |

| ▼ Resistance Zone 1 | 2665 – 2695 |

| ─ Pivot Area | ~2650 |

| ▲ Support Zone 1 | 2605 – 2635 |

| ▲ Support Zone 2 | 2550 – 2580 |

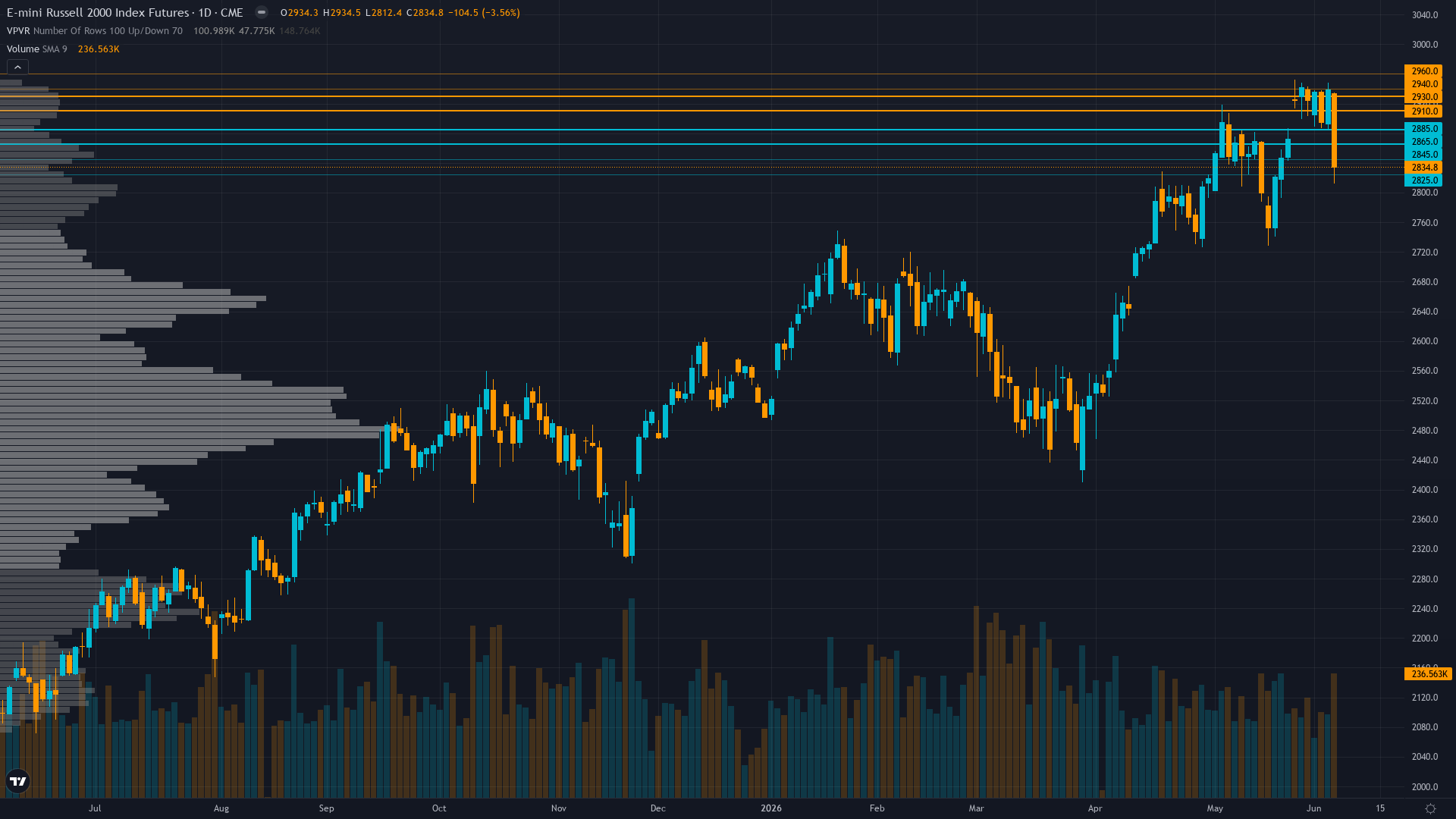

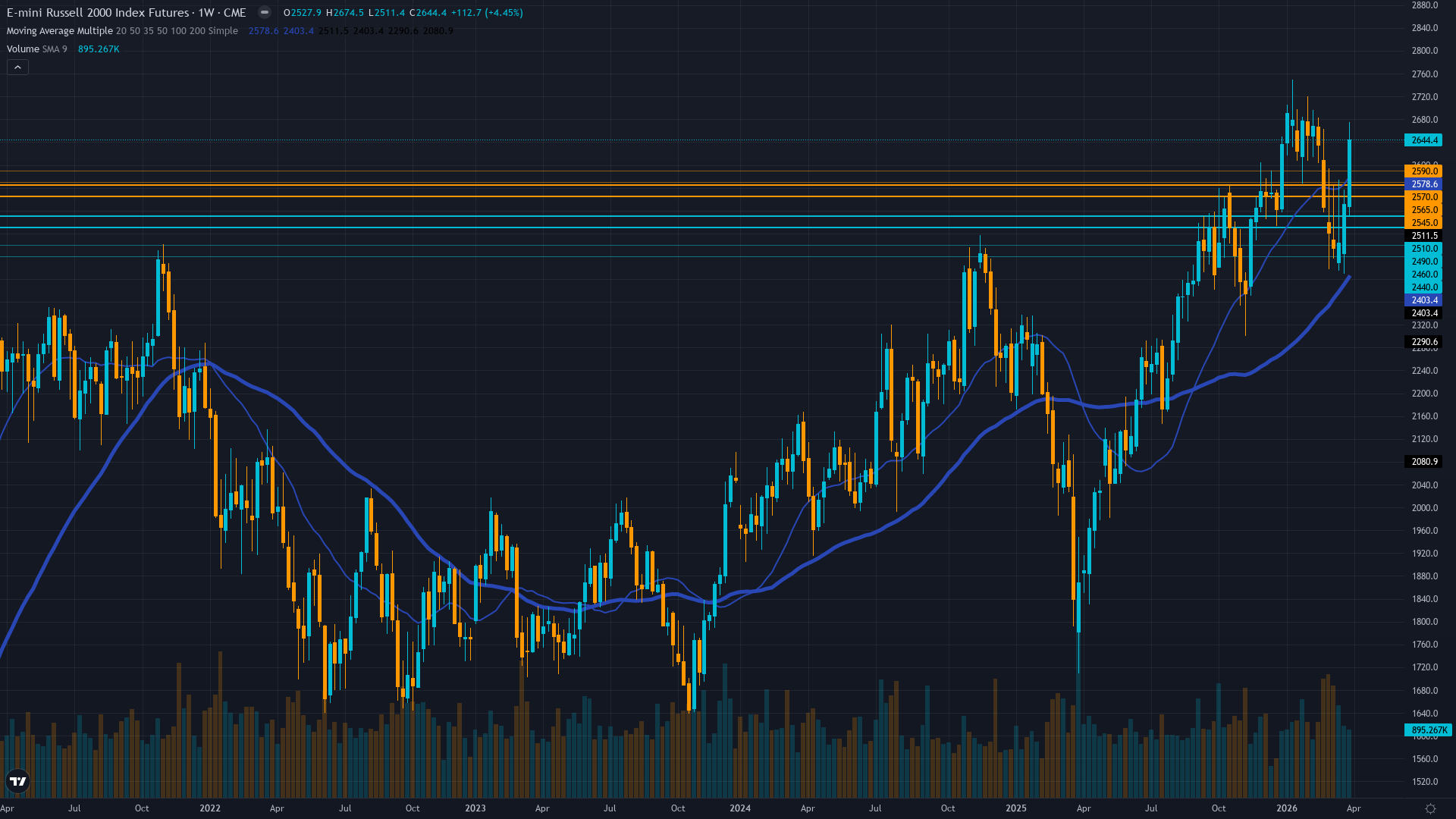

Uptrend intact above 50-day MA at 2,296 and 200-day at 2,190, price at 2,650 pulled back 3.1% from January 22 ATH of 2,735 but holding constructive structure

Q4 2025 earnings inflection real at 64.9% growth with Q1 2026 projecting 44.9% YoY, but forward P/E at 25.4 versus 13.62-17.34 historical range creates valuation sensitivity to earnings delivery

Heavy spec shorts at -45.1% of OI (March 31 data stale) creating short squeeze potential, but IWM outflows of -$7.42B year-to-date show institutional caution despite price strength

VIX declined 4.6 points to 19.23 signaling declining fear, equity put/call at 0.51 shows strong call demand indicating bullish positioning without panic hedging

Fed on hold at 3.50-3.75% with April 28-29 FOMC 16 days away, March CPI hot at +1.1% MoM removes easing hopes but transitional macro regime with VIX below 20 and credit spreads tightening

Normal - short-term vol 24.5 below mid-term 26.8 reflecting March correction volatility now moderating as VIX declines to 19.23 from 24-27 range

When RTY recovers from correction with VIX declining below 20 after fear spike, historical precedent shows 65% probability of 4-8% extension rally if earnings catalyst validates growth narrative

RVX elevated at 32.88 as of March 20 but VIX declining to 19.23 suggests 60% probability of continued mean reversion lower within 2-3 weeks if earnings catalyst provides clarity and support holds at 2,620

Normal volatility regime at 58th percentile supports standard risk management with 3-4% stops below 2,565 support, expect 40-60 point daily ranges versus 60-100 during March correction, normalization pattern suggests directional trending rather than range-bound chop

Current volatility setup at 58th percentile after March spike creates asymmetric opportunity for 3-5% extension rally to 2,680-2,735 resistance versus 2-3% downside to 2,565-2,620 support if sentiment bounce continues into earnings catalyst

|

⚠️ Primary Risk

Q1 earnings season delivers materially below 44.9% YoY growth consensus triggering multiple compression from elevated 25.4x forward P/E, particularly if margin pressures from hot CPI data materialize in results Probability: MEDIUM

|

✦ Primary Opportunity

Continuation of sentiment-driven rally from improved VIX regime (19.23 vs 24-27 last week) targeting 2,680-2,735 resistance as Q1 earnings validate 44.9% growth inflection and short squeeze accelerates from heavy spec short positioning Timeframe: 1-3 weeks into early Q1 earnings releases and FOMC meeting April 28-29

|

Russell 2000 stands at a validated inflection point on April 12, 2026, trading at 2,650 following a powerful 4.45% weekly surge that confirms the sentiment-driven bounce thesis articulated in last week's BULLISH call. MACRO REGIME CLASSIFICATION: TRANSITIONAL moving toward RISK-ON. VIX at 19.23 (below 20 threshold) down from 23.87-27 range just days ago, credit spreads tightening from 3.42% to 3.17% between March 30 and April 2, equity indices recovering with RTY outperforming. However, hot March CPI (+1.1% MoM, +3.1% YoY released April 10) creates policy uncertainty with Fed funds futures pricing zero probability of cut at April 28-29 FOMC.

This is not pure risk-on given inflation concerns, but the market has absorbed the CPI shock and is pricing growth resilience over recession risk. Post-input development identified: Current price at 2,650 confirms strong momentum from last week's close at 2,531.7, representing 4.45% weekly gain that validates the contrarian sentiment setup. FinancialContent April 2 article confirms 'Great Rotation' narrative gaining mainstream attention with IWM surging 12%+ in recent weeks. Most critically, Q1 2026 earnings season begins mid-April (within days) with 44.9% YoY growth consensus providing imminent fundamental catalyst.

The convergence of discipline signals creates an increasingly constructive picture: Fundamental (signal 0.5, conf 4) remains mildly bullish on 44.9% Q1 growth but lacks immediate catalyst until earnings reports begin. Sentiment (signal 0.5, conf 5) shows fear receding with VIX down 4.6 points and AAII improving from -17.86% to -7.3% bull-bear spread, though not yet reaching neutral. Economic (signal -1.5, conf 6) is bearish on hot CPI removing Fed easing catalyst but acknowledges transitional regime.

Technical (signal 1.5, conf 5) is bullish with uptrend intact above key MAs. Options (signal 1.5, conf 6) bullish on declining volatility and low put/call ratio. Institutional (signal -1.5, conf 4) bearish on stale data showing heavy shorts and outflows. The critical validation: last week's BULLISH call at conviction 6 was decisively CORRECT with price advancing 4.45% from 2,531.7 to 2,650, resetting miss streak to zero and confirming the sentiment extreme framework identified oversold conditions accurately.

This successful call increases confidence that the contrarian thesis identified last week (VIX 24-27 fear creating bounce potential) has played out but may have further to run as VIX continues declining to 19.23. Bias streak now extends to 2 consecutive BULLISH weeks, well below the 3-week review threshold. The desk assesses signal at 1.5 (BULLISH) reflecting weight of evidence: VIX collapse validates sentiment normalization, last week's CORRECT call confirms thesis, Q1 earnings catalyst imminent in days provides fundamental validation opportunity, technical structure holding above key MAs, and 'Great Rotation' narrative gaining mainstream traction.

Conviction at 7 reflects: (1) Fresh catalyst in VIX decline and upcoming earnings season justifies Max Conf (catalyst) of 8 cap, (2) Strong discipline agreement with 3 of 6 bullish (Technical, Options, Fundamental weak bullish) and Sentiment improving, (3) Last week's CORRECT call validates framework, (4) Q1 earnings beginning within days provides high-impact near-term catalyst. Devil's advocate bearish case: Hot March CPI at +1.1% MoM removes Fed easing tailwind, elevated valuation at 25.4x forward P/E vulnerable to earnings disappointment on 44.9% bar, institutional outflows of -$7.42B/year show smart money selling into rally, heavy spec shorts could be right if earnings disappoint.

The bullish case dominates: VIX declining to 19.23 from 24-27 confirms fear exhaustion, last week's 4.45% gain validates sentiment bounce, Q1 earnings season beginning within days provides catalyst for 44.9% growth narrative validation, technical structure holding well above 50/200-day MAs, and 'Great Rotation' narrative creating positive feedback loop as more capital rotates into small-caps. Risk management: if 2,620 support fails or Q1 earnings begin disappointing 44.9% consensus, thesis invalidated.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| April 10, 2026 | BULLISH | 6/10 | ✅ |

| April 3, 2026 | BULLISH | 6/10 | ✅ |

| March 27, 2026 | BEARISH | 5/10 | ❌ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | BULLISH | 6/10 | ❌ |

| February 27, 2026 | BULLISH | 7/10 | ❌ |

| February 21, 2026 | BULLISH | 7/10 | ✅ |

| February 13, 2026 | BULLISH | 7/10 | ✅ |

| February 8, 2026 | BULLISH | 7/10 | ✅ |

| February 1, 2026 | BULLISH | 7/10 | ✅ |

| January 25, 2026 | BULLISH | 7/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Russell 2000 (RTY) Report Date: April 12, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 7/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 38 (SLIGHT DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: TRENDING UP Regime: TRENDING UP Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Small-caps in 'Great Rotation' momentum with IWM surging 12%+ and Q1 earnings season beginning mid-April to test 44.9% growth consensus, but near-term caution warranted on hot CPI removing Fed easing catalyst ── WHAT THE MARKET IS MISSING ─────────────────── Market consensus focused on 'Great Rotation' narrative may be underpricing earnings delivery risk on elevated 44.9% bar, while desk sees tactical continuation of sentiment-driven bounce into earnings with conviction backed by last week's CORRECT call and VIX normalization to 19.23 ── KEY DRIVERS ───────────────────��────────────── 1. VIX collapse from 23.87 to 19.23 over past week creating risk-on environment as fear recedes, combining with last week's 4.45% RTY surge validating sentiment-driven bounce thesis 2. Q1 2026 earnings season begins mid-April (within days) with 44.9% YoY growth consensus providing fundamental catalyst to validate small-cap rotation narrative after January ATH breakout 3. Hot March CPI (+1.1% MoM, +3.1% YoY) removes near-term Fed easing catalyst but market has absorbed shock, with credit spreads tightening to 3.17% signaling underlying stability ── KEY ZONES ──────────────────────────────────── Resistance 2: 2720 – 2750 Resistance 1: 2665 – 2695 Pivot: ~2650 Support 1: 2605 – 2635 Support 2: 2550 – 2580 ── DISCIPLINE BIASES ──────────────────────────── Technical: BULLISH Fundamental: BULLISH Institutional: BEARISH Options: BULLISH Economic: BEARISH Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── Uptrend intact above 50-day MA at 2,296 and 200-day at 2,190, price at 2,650 pulled back 3.1% from January 22 ATH of 2,735 but holding constructive structure ── FUNDAMENTAL ASSESSMENT ─────────────────────── Q4 2025 earnings inflection real at 64.9% growth with Q1 2026 projecting 44.9% YoY, but forward P/E at 25.4 versus 13.62-17.34 historical range creates valuation sensitivity to earnings delivery ── INSTITUTIONAL POSITIONING ──────────────────── Heavy spec shorts at -45.1% of OI (March 31 data stale) creating short squeeze potential, but IWM outflows of -$7.42B year-to-date show institutional caution despite price strength ── OPTIONS FLOW ───────────────────────────────── VIX declined 4.6 points to 19.23 signaling declining fear, equity put/call at 0.51 shows strong call demand indicating bullish positioning without panic hedging ── ECONOMIC BACKDROP ──────────────────────────── Fed on hold at 3.50-3.75% with April 28-29 FOMC 16 days away, March CPI hot at +1.1% MoM removes easing hopes but transitional macro regime with VIX below 20 and credit spreads tightening ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 58th Trend: Stable — Days in Regime: 15 Term Structure: normal - short-term vol 24.5 below mid-term 26.8 reflecting March correction volatility now moderating as VIX declines to 19.23 from 24-27 range Historical Pattern: When RTY recovers from correction with VIX declining below 20 after fear spike, historical precedent shows 65% probability of 4-8% extension rally if earnings catalyst validates growth narrative Outlook: RVX elevated at 32.88 as of March 20 but VIX declining to 19.23 suggests 60% probability of continued mean reversion lower within 2-3 weeks if earnings catalyst provides clarity and support holds at 2,620 Trading Context: Normal volatility regime at 58th percentile supports standard risk management with 3-4% stops below 2,565 support, expect 40-60 point daily ranges versus 60-100 during March correction, normalization pattern suggests directional trending rather than range-bound chop Vol Risk/Opportunity: Current volatility setup at 58th percentile after March spike creates asymmetric opportunity for 3-5% extension rally to 2,680-2,735 resistance versus 2-3% downside to 2,565-2,620 support if sentiment bounce continues into earnings catalyst ── PRIMARY RISK ───────────────────────────────── Q1 earnings season delivers materially below 44.9% YoY growth consensus triggering multiple compression from elevated 25.4x forward P/E, particularly if margin pressures from hot CPI data materialize in results Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Continuation of sentiment-driven rally from improved VIX regime (19.23 vs 24-27 last week) targeting 2,680-2,735 resistance as Q1 earnings validate 44.9% growth inflection and short squeeze accelerates from heavy spec short positioning Timeframe: 1-3 weeks into early Q1 earnings releases and FOMC meeting April 28-29 ── NEXT CATALYST ──────────────────────────────── Date: April 14, 2026 Event: Q1 2026 earnings season begins for Russell 2000 constituents, testing 44.9% YoY growth consensus through mid-May with majority of results by late April Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── Russell 2000 stands at a validated inflection point on April 12, 2026, trading at 2,650 following a powerful 4.45% weekly surge that confirms the sentiment-driven bounce thesis articulated in last week's BULLISH call. MACRO REGIME CLASSIFICATION: TRANSITIONAL moving toward RISK-ON. VIX at 19.23 (below 20 threshold) down from 23.87-27 range just days ago, credit spreads tightening from 3.42% to 3.17% between March 30 and April 2, equity indices recovering with RTY outperforming. However, hot March CPI (+1.1% MoM, +3.1% YoY released April 10) creates policy uncertainty with Fed funds futures pricing zero probability of cut at April 28-29 FOMC. This is not pure risk-on given inflation concerns, but the market has absorbed the CPI shock and is pricing growth resilience over recession risk. Post-input development identified: Current price at 2,650 confirms strong momentum from last week's close at 2,531.7, representing 4.45% weekly gain that validates the contrarian sentiment setup. FinancialContent April 2 article confirms 'Great Rotation' narrative gaining mainstream attention with IWM surging 12%+ in recent weeks. Most critically, Q1 2026 earnings season begins mid-April (within days) with 44.9% YoY growth consensus providing imminent fundamental catalyst. The convergence of discipline signals creates an increasingly constructive picture: Fundamental (signal 0.5, conf 4) remains mildly bullish on 44.9% Q1 growth but lacks immediate catalyst until earnings reports begin. Sentiment (signal 0.5, conf 5) shows fear receding with VIX down 4.6 points and AAII improving from -17.86% to -7.3% bull-bear spread, though not yet reaching neutral. Economic (signal -1.5, conf 6) is bearish on hot CPI removing Fed easing catalyst but acknowledges transitional regime. Technical (signal 1.5, conf 5) is bullish with uptrend intact above key MAs. Options (signal 1.5, conf 6) bullish on declining volatility and low put/call ratio. Institutional (signal -1.5, conf 4) bearish on stale data showing heavy shorts and outflows. The critical validation: last week's BULLISH call at conviction 6 was decisively CORRECT with price advancing 4.45% from 2,531.7 to 2,650, resetting miss streak to zero and confirming the sentiment extreme framework identified oversold conditions accurately. This successful call increases confidence that the contrarian thesis identified last week (VIX 24-27 fear creating bounce potential) has played out but may have further to run as VIX continues declining to 19.23. Bias streak now extends to 2 consecutive BULLISH weeks, well below the 3-week review threshold. The desk assesses signal at 1.5 (BULLISH) reflecting weight of evidence: VIX collapse validates sentiment normalization, last week's CORRECT call confirms thesis, Q1 earnings catalyst imminent in days provides fundamental validation opportunity, technical structure holding above key MAs, and 'Great Rotation' narrative gaining mainstream traction. Conviction at 7 reflects: (1) Fresh catalyst in VIX decline and upcoming earnings season justifies Max Conf (catalyst) of 8 cap, (2) Strong discipline agreement with 3 of 6 bullish (Technical, Options, Fundamental weak bullish) and Sentiment improving, (3) Last week's CORRECT call validates framework, (4) Q1 earnings beginning within days provides high-impact near-term catalyst. Devil's advocate bearish case: Hot March CPI at +1.1% MoM removes Fed easing tailwind, elevated valuation at 25.4x forward P/E vulnerable to earnings disappointment on 44.9% bar, institutional outflows of -$7.42B/year show smart money selling into rally, heavy spec shorts could be right if earnings disappoint. The bullish case dominates: VIX declining to 19.23 from 24-27 confirms fear exhaustion, last week's 4.45% gain validates sentiment bounce, Q1 earnings season beginning within days provides catalyst for 44.9% growth narrative validation, technical structure holding well above 50/200-day MAs, and 'Great Rotation' narrative creating positive feedback loop as more capital rotates into small-caps. Risk management: if 2,620 support fails or Q1 earnings begin disappointing 44.9% consensus, thesis invalidated.