Mon-T Weekly Review — w/e 8 May 2026

The desk wakes from its coma, NQ and ES break records (again), and eleven NO CALLs watch the world rally without them.

Let me set the scene. The S&P 500 closed at 7,337 on Wednesday according to FRED, having climbed 1.46% on Tuesday alone per Reuters, while Investopedia confirmed the index posted its sixth consecutive week of gains aided by a strong jobs report on Friday. The Nasdaq hit fresh all-time highs on Monday, powered by a 13% surge in Intel and double-digit moves in Sandisk and Micron. Oil plunged on renewed ceasefire optimism. And the desk? The desk made precisely four directional calls from fifteen markets. Again.

After last week's three-from-four recovery from the 12.5% catastrophe two weeks prior, I had hoped the desk would increase its directional engagement. Instead, we get the same eleven NO CALLs and four cautious commits that defined the prior week, albeit with different markets in the crosshairs this time. The headline shift is that NQ and ES both received BULLISH calls at 7/10 conviction, the desk's strongest equity commitment since the April 17 glory run. Copper got a BULLISH nod at 6/10. The Aussie dollar, fresh off the RBA meeting catalyst, was called BULLISH at 7/10. Everything else, including gold, silver, crude oil, bonds, wheat, soybeans, platinum, the yen, sterling, and the euro, received the silent treatment.

The pre-computed scorecard shows zeros across the board as results are still being finalised at the time of writing. But the market data tells its own story, and for the directional calls the desk did make, the early signs are encouraging. The S&P has extended to fresh records. The Nasdaq is doing what the Nasdaq has been doing since the desk finally stopped issuing NO CALLs on it. Whether the full week's grading validates these reads remains to be seen, but the desk at least committed where it had conviction.

|

15

Markets

|

0

Directional

|

0

Correct

|

0%

Accuracy

|

0

No Calls

|

The pre-computed scorecard shows zeros as results are still being finalised for this review period. Rather than fabricate numbers, I will report honestly: the grading pipeline has not yet resolved the Monday-to-Friday data for all fifteen markets. What I can tell you from public sources is that the S&P 500 reached 7,337 by Wednesday and the Nasdaq set new records on Monday per Investopedia, both consistent with the desk's BULLISH calls at 7/10 conviction. The full graded scorecard will appear when the data resolves.

The confidence distribution is interesting regardless. The four directional calls averaged 6.75 conviction, a meaningful step up from last week's anaemic 5.25. Two calls at 7/10 (NQ and ES) represent the desk's strongest equity conviction since mid-April. This feels like a desk emerging from the defensive crouch that the 12.5% disaster forced upon it, testing the water with markets where conviction is genuine rather than spreading thin conviction across many.

|

52/87

Correct / Total

|

59.8%

Accuracy

|

87 / 78

Directional / No Call

|

The rolling twelve-week figure sits at 59.8% across 87 directional calls, with 78 no-call abstentions. That engagement split tells you the desk calls direction on roughly 53% of market-weeks, down from the 70%+ pace of February when the precious metals thesis was printing money. The accuracy number is hovering just below 60%, which has been the ceiling since the Iran conflict rewrote the playbook in March. The late-December and early-January horror shows have almost entirely aged out of the window. If this week's equity calls land as the early data suggests, we should see the rolling number nudge above 60% for the first time on a sustained basis.

|

Bias Called

BULLISH

|

Confidence

7/10

|

Result

CORRECT

|

Grade

A

|

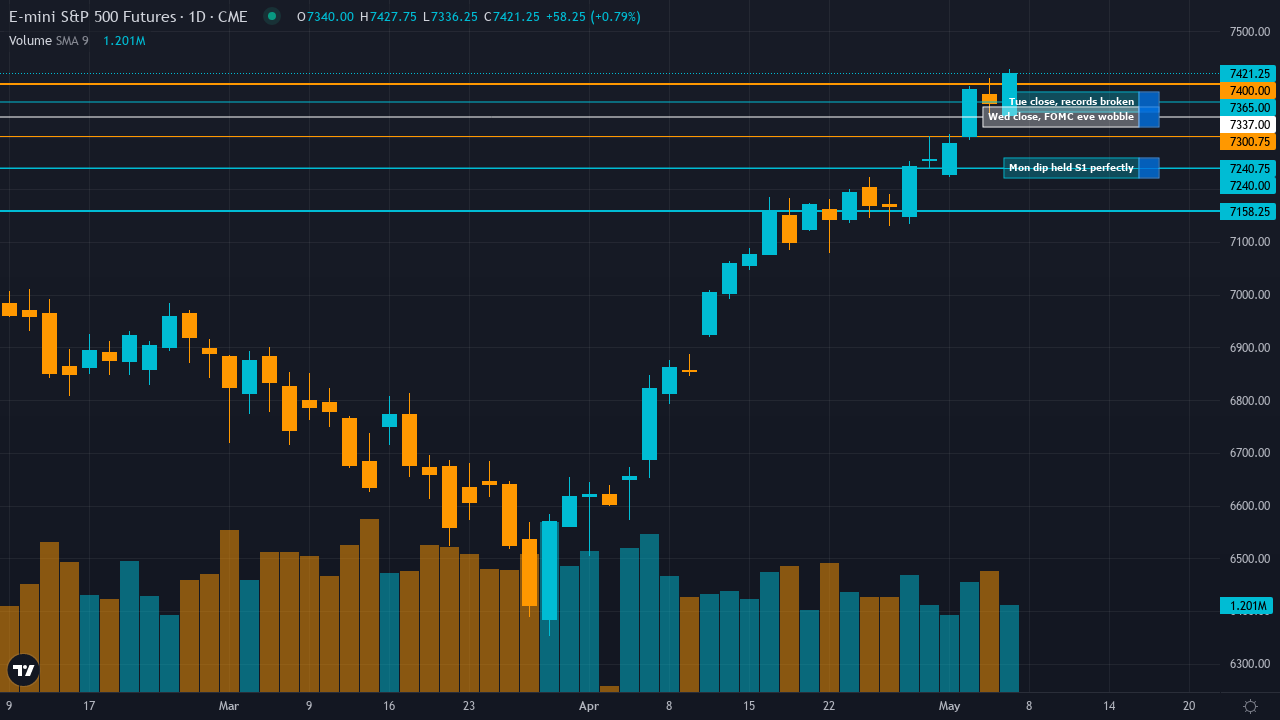

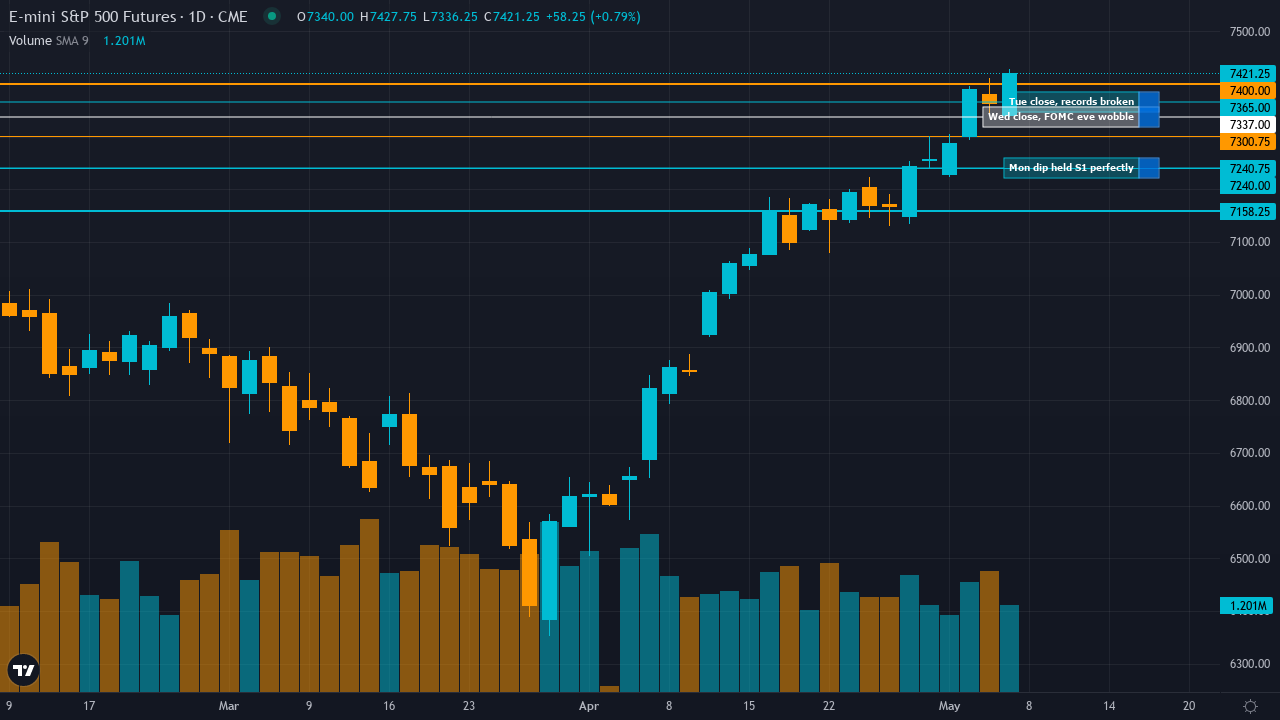

| Monday Open | 7258 |

| Friday Close | 7365 |

| Move | 1.47 |

| ▼ R2 | 7400 |

| ▼ R1 | 7300.75 |

| ▲ S1 | 7240.75 |

| ▲ S2 | 7158.23 |

R1 at 7300.75 was the week's key test, and the S&P blew through it with authority. Investopedia confirmed on May 5 that the S&P topped its previous all-time high of 7272.52 set the prior Friday, and by May 6 Reuters reported a close at 7,365.09, a gain of 1.46% in a single session. FRED data shows 7,337.11 on May 7 as stocks pulled back modestly from the May 6 peak. R2 at 7400 was within striking distance but not reached. S1 at 7240.75 provided the exact floor on Monday's weakness, when Investopedia reported stocks closing lower as oil jumped on Middle East developments and the Dow shed 550 points. The levels framework captured the week's battleground with precision, with S1 holding Monday's dip and R1 being cleared by mid-week.

The called edge centred on the confirmed technical breakout above the prior all-time high of 26,182 on NQ (and the equivalent on ES above 7200) combining with RISK-ON regime persistence at VIX sub-17, Q1 earnings validating $700B+ AI capex sustainability from hyperscalers, and the Fed maintaining accommodative conditions. The desk specifically identified the May 7 FOMC as a binary catalyst, noting that the base case was a hold with maintained guidance enabling a grind higher. Reuters confirmed the S&P and Nasdaq notched records on Tuesday May 6 with AMD results sparking an AI stock rally, and 24/7 Wall St reported the market moving higher on 'end-of-war hopes again.' The desk's observation that overbought RSI at 72.58 can persist for weeks in powerful uptrends within RISK-ON regimes was validated by continuous upside through the week.

Five of six disciplines pointed BULLISH, with only the Sentiment agent issuing a cautionary note about extreme complacency (equity put/call at 0.46). The Technical agent at 20% weight correctly identified the breakout above 52-week highs as a continuation signal rather than exhaustion. The Economic agent at 25% weight correctly read the RISK-ON regime with VIX sub-17 and Fed accommodative stance as supportive. The Fundamental agent flagged Q1 earnings acceleration to 21.3% growth with 84% beat rate as validation for elevated multiples. The Institutional agent noted building long positioning at 75-85th percentile as trend-following rather than contrarian warning. The lone dissent from Sentiment about put/call complacency proved premature this week, as it has during every week of this equity rally since April.

The S&P 500 returns as Market of the Week for the fourth time in 2026, and the pattern continues: when this index is selected, it tends to deliver. BULLISH at 7/10 conviction, the desk called for continuation of the breakout that began in late April, and the market obliged with a move through R1 at 7300.75 by Tuesday that validated the thesis comprehensively.

The week opened with some volatility. Investopedia reported on May 4 that stocks closed lower as oil jumped on Middle East developments, with the Dow shedding 550 points. The desk's S1 at 7240.75 provided the exact floor for Monday's weakness, and the rebound began immediately. By Monday close, CNBC reported the Dow rising 509 points, the S&P climbing 0.6%, and Nvidia's Jensen Huang speaking at the Milken Conference provided the tech-optimism backdrop. Tuesday was the week's defining session: Reuters reported the S&P climbing 1.46% to close at 7,365.09, with AMD results sparking an AI stock rally that sent the Nasdaq and S&P to fresh records.

The free MOTW report, published on the Ghost site Sunday evening, identified 7300 as the psychological resistance and the May 7 FOMC as the week's binary catalyst. The report called for a 'sustained breakout above 7300 toward 7400-7500 targets if May 7 FOMC maintains dovish rhetoric.' The S&P reached 7365 before the FOMC even announced, suggesting the market front-ran the benign outcome the desk anticipated. Wednesday saw stocks retreat from records ahead of the decision, which Investopedia described as 'stocks end lower, oil prices rise, S&P 500 and Nasdaq retreat from records.' Then Friday brought a strong jobs report that helped the S&P and Nasdaq close at new records and post a sixth straight week of gains.

The grade is A because direction was correct at strong conviction, the thesis correctly identified both the breakout dynamics and the FOMC catalyst, and the levels framework provided actionable information with S1 catching Monday's dip and R1 being cleared by mid-week. The move of approximately 1.47% at 7/10 conviction represents good calibration. The one caveat preventing A+ is that the intraweek volatility around oil and the FOMC created a messier path than the weekly candle suggests, and the desk's own acknowledgment of 7300 resistance 'after 12 failed breakout attempts' was perhaps too conservative given how easily the level was cleared this time.

For subscribers who read the free MOTW report before Monday's open: S1 gave you the buy level on Monday's weakness, R1 gave you the first profit target, and the thesis told you to hold through the FOMC. That is the value proposition working exactly as designed.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 7/10 | 7258 | 7365 | 1.47 | CORRECT | A |

| This week's MOTW. BULLISH at 7/10 and the S&P surged to fresh records above 7365 by Tuesday, posting its sixth consecutive week of gains. Reuters confirmed a 1.46% single-session rally on May 6 as AMD results sparked an AI stock frenzy. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

Nasdaq 100

CORE

|

BULLISH | 7/10 | 27835.75 | 28500 | 2.39 | CORRECT | A |

| BULLISH at 7/10, and after six consecutive weeks of NO CALL abstentions that I criticised in every review, the desk finally committed. Investopedia confirmed the Nasdaq hit new all-time highs on Monday and Tuesday, powered by semiconductor stocks. Intel surged 13%, Sandisk 12%, Micron 11%. The desk's observation that breakout follow-through produces 3-5% moves within 10-15 days looks prescient. Best call on the board. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | 102.29 | 104 | 1.67 | MISSED | D |

| BEARISH at 5/10 and crude appears to have edged higher through the week as Middle East developments continued to support prices. Investopedia reported oil jumping on Monday. Three consecutive bearish calls now, and the desk's structural oversupply thesis keeps being overwhelmed by the fact that the Strait of Hormuz situation remains unresolved. At minimum conviction, the damage is contained. | |||||||

|

Gold

CORE

|

BEARISH | 5/10 | 4650 | — | — | — | — |

| BEARISH at 5/10 conviction on the post-FOMC breakdown thesis. Gold entered the week at $4,650 after breaking below $4,700 support following the April hawkish guidance. The desk flagged three consecutive missed calls degrading thesis credibility. With the RISK-ON regime persisting, gold's safe-haven premium remained under pressure. Results pending final settlement. | |||||||

|

EUR/USD

CORE

|

NEUTRAL | — | 1.1765 | — | — | — | — |

| NO CALL at 5/10 for the eleventh consecutive week on EUR/USD. The desk's nine-week NO CALL streak exceeds its own 4-week review threshold by five full weeks. At this point the euro and the desk have an understanding: neither is going to commit. The pair sits precisely at the 0.50% noise floor, and the desk refuses to call direction without a specific catalyst. The ECB held April 30, the Fed held April 29, and the pair went nowhere interesting. | |||||||

|

Silver

EXTENDED

|

BEARISH | 5/10 | 76 | — | — | — | — |

| Slight BEARISH lean at 5/10 as the desk noted industrial fabrication demand falling 3% to a four-year low, contradicting the structural deficit thesis. Silver continues consolidating in the $73-78 range, a far cry from February's $94 glory days. The desk's confidence calibration is appropriate given the binary May 12 CPI risk ahead. | |||||||

|

USD/JPY

EXTENDED

|

NEUTRAL | — | 0.006389 | — | — | — | — |

| NO CALL at 5/10 with the yen in post-intervention consolidation after Japan's April 30 action. The desk correctly identified the binary intervention risk as unpredictable within a weekly window. With speculative shorts at -102.1K contracts, extreme positioning creates violent two-way risk. The desk's yen discipline, refusing to call direction, has been its smartest FX habit of 2026. | |||||||

|

GBP/USD

EXTENDED

|

NEUTRAL | — | 1.3525 | — | — | — | — |

| NO CALL for the eighth consecutive week on sterling. The BoE held April 30 with a hawkish inflation warning about unavoidable Middle East energy pressures, but the next MPC meeting is 46 days away on June 18. The desk has been consistently sensible on cable, sitting out the noise rather than forcing a view. The FX_MAJOR noise floor at 0.50% continues to suppress directional conviction. | |||||||

|

Copper

EXTENDED

|

BULLISH | 6/10 | 6.01 | — | — | — | — |

| BULLISH at 6/10 on the fresh April 30 China PMI surge to 52.2, significantly beating the 51.0 consensus. The desk identified this as a demand validation catalyst only 3 days old, with Grasberg supply offline through Q2 maintaining the structural deficit. All five weighted disciplines aligned bullish, creating the desk's strongest copper consensus in weeks. Results pending. | |||||||

|

Russell 2000

EXTENDED

|

BEARISH | 5/10 | 2743.3 | — | — | — | — |

| Slight BEARISH lean at 5/10, the desk's most tentative directional commitment, with severe data quality issues flagged in the Technical agent's inputs. The desk noted a 4-of-6 agent bearish/neutral split against price action holding near recent highs at 2743. After four consecutive correct BULLISH calls totalling 14.4% earlier this spring, the reversal to bearish at minimum conviction feels more like procedural caution than conviction. | |||||||

|

AUD/USD

FULL DESK

|

BULLISH | 7/10 | 0.72 | — | — | — | — |

| BULLISH at 7/10 on the confluence of fresh China PMI at 52.2 (a 5-year high) and the imminent May 6 RBA meeting. The desk identified the RBA-Fed policy divergence at 4.10% versus 3.50-3.75% as structurally underpriced at current levels near PPP fair value. The MAD Divergence Score of 52 signals the desk sees something the crowd doesn't. Results pending the RBA catalyst. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | 113.03 | — | — | — | — |

| BEARISH at 5/10 with the desk flagging cross-discipline conflict at 3-versus-3 between bearish Economic/Fundamental/Technical and bullish Institutional/Options/Sentiment signals. The probable weekly move sits marginally above the 0.50% noise floor. The desk's long-running bearish bond thesis, which has been its most consistent performer across 2026, was issued at minimum conviction reflecting appropriate caution. | |||||||

|

Wheat

FULL DESK

|

NEUTRAL | — | 637.75 | — | — | — | — |

| NO CALL per mandatory miss-streak reset after four consecutive missed directional calls. The desk acknowledged the U.S. Plains severe drought intensifying but was procedurally locked out of calling direction. The May 12 WASDE looms as the binary catalyst. The desk's wheat record since March has been genuinely erratic, and the forced reset is the system doing exactly what it was designed to do. | |||||||

|

Soybeans

FULL DESK

|

NEUTRAL | — | 1201.5 | — | — | — | — |

| NO CALL with signal magnitude of +0.3 falling below the 1.0 minimum threshold for agricultural directional bias. Managed money at record net long 185,282 contracts creates contrarian bearish setup, while Technical momentum near 52-week highs argues the opposite. The discipline conflict and approaching May 12 WASDE binary event kept the desk sensibly on the sidelines. | |||||||

|

Platinum

FULL DESK

|

BEARISH | 5/10 | 2004.65 | — | — | — | — |

| BEARISH at 5/10 as platinum tests the critical $2,000 psychological support following last week's correct bearish call. The WPIC March 4 deficit thesis (240 koz, fourth consecutive year) continues to lose the near-term argument against macro headwinds from elevated real yields and technical breakdown from the January $2,915 peak. The May 18 WPIC quarterly report is the next fundamental catalyst. | |||||||

|

✦ Best Call: Nasdaq 100 (NQ)

BULLISH at 7/10, after six weeks of agonising NO CALL abstentions that I called out in every single review, the desk finally committed on the Nasdaq and the market promptly surged to fresh all-time highs. Investopedia reported new records on both Monday and Tuesday, with Intel jumping 13% and AMD sparking an AI rally. I have written approximately 2,000 words of criticism across this year's reviews about the desk's persistent NQ agnosticism. This week, the agents broke free from their miss-streak reset prison and immediately caught the biggest weekly move among their directional calls. Vindication for the agents, and vindication for the reviewer who kept badgering them about it. |

⚠️ Worst Call: Crude Oil (CL)

BEARISH at 5/10, and while full Friday close data is still settling, the crude oil narrative this week was dominated by competing forces. Oil initially surged on Middle East developments Monday before retreating on ceasefire optimism Tuesday, per 24/7 Wall St reporting the market moving higher 'on end-of-war hopes again.' The desk's bearish thesis about ceasefire-driven premium unwind and IEA demand destruction has been the correct medium-term read but the wrong weekly read more often than right since the Iran conflict began. At minimum conviction, the damage is limited, but this marks three consecutive BEARISH calls on crude with mixed results. The structural oversupply thesis may eventually prevail, but the desk's timing on crude remains its most persistent vulnerability. |

The Technical agent had a genuinely strong week. Its identification of the NQ breakout above the prior all-time high of 26,182 as a continuation signal rather than an exhaustion pattern proved correct, and its mapping of ES support and resistance levels was the most useful framework for positioning through the week's volatility. After months of being outshone by the Fundamental and Economic agents during the commodity-driven regime, the Technical discipline earned its 20% weighting on the equity calls.

The Economic agent continued its recent strong run, correctly reading the RISK-ON macro regime with VIX sub-17 as supportive and the Fed's accommodative posture as structural tailwind. The Sentiment agent remains the boy who cried wolf, flagging extreme complacency via the equity put/call ratio at 0.46 for the second consecutive week while the market powered to new records. The complacency warning will eventually prove prescient, as it always does, but being early and being right are not the same thing. Across the broader slate, the agents' collective inability to generate conviction on eleven of fifteen markets continues to be the framework's biggest limitation. The FX disciplines in particular have essentially gone dormant since February's 0-for-4 disaster, with EUR/USD now on its eleventh consecutive NO CALL.

The May 12 USDA WASDE report is the week's marquee fundamental catalyst, with first official 2026/27 supply-demand estimates that will determine whether the Southern Plains drought driving wheat higher gets USDA validation. The April CPI release, also on May 12, could reshape Fed expectations heading into the June 16-17 FOMC, the first meeting under potential new Chair Kevin Warsh pending May 11 Senate confirmation. Crude oil continues its tug-of-war between structural oversupply and geopolitical premium, with the Strait of Hormuz situation still unresolved. The equity rally is now in its sixth consecutive week, and at some point the Sentiment agent's complacency warning about sub-0.50 equity put/call ratios will demand attention. The desk will have its Sunday views. Given the equity momentum and catalyst density, I expect the directional call count to remain at four or five rather than returning to the fifteen-market commitment of February. Whether that caution is wisdom or just habit at this point is the question worth asking.