Mon-T Weekly Review — w/e 19 Jun 2026

Four from five, crude oil obliterates $77, and the Russell 2000 catches its reconstitution tailwind while ten NO CALLs watch Kevin Warsh rewrite the Fed playbook.

Kevin Warsh held his first press conference as Fed Chair on Wednesday afternoon, held rates steady as expected, hinted the next move could be a rate hike, and announced five task forces to overhaul how the Fed operates. NPR reported the central bank 'signaled its next move could be a rate increase.' Markets, apparently, had already decided they didn't much care. The S&P 500 rallied 1.63%. The Nasdaq surged 3.32%. And crude oil, the desk's favourite punching bag since the Iran ceasefire began unwinding in late May, collapsed another 9.83% to settle near $76.54 as Strait of Hormuz shipping flows continued normalising. Trading Economics confirmed WTI was on track for a weekly decline of around 10%, erasing most of the war-era gains that had defined energy markets since February.

Five directional calls this week, four correct. Eighty percent accuracy at an average confidence of 6.2. The desk picked its spots, committed where conviction existed, and delivered cleanly on crude oil, silver, the S&P, and the Russell 2000. The lone miss was Treasury bonds, called BEARISH at 6/10 ahead of Warsh's debut, which rallied 0.81% as markets apparently interpreted his 'regime change in the conduct of policy' as less immediately threatening than expected. After three consecutive weeks of sub-50% accuracy that had me questioning whether the analytical framework was fit for purpose, this feels like the desk remembering how to play its own game.

The ten NO CALL markets tell their own story, and it is not entirely flattering. The Nasdaq ripped 3.32% while the desk sat on its hands. Wheat surged 3.65%. Platinum fell 2.73%. Sterling dropped 1.34%. I have been writing variations of this paragraph since February, and the pattern holds: the desk's disciplined abstention protects its accuracy percentage at the cost of enormous missed opportunities. But after the 12.5% catastrophe in April and the 40% scorecard three weeks ago, I will take a clean 80% on five calls over a messy 50% on ten, every single time.

|

15

Markets

|

5

Directional

|

4

Correct

|

80%

Accuracy

|

10

No Calls

|

Five directional calls this week, with four landing on the right side. The other ten markets got the NO CALL treatment. An 80% directional hit rate is the best since the w/e 10 Feb week that kicked off silver's legendary four-week run, and the confidence calibration was clean: the two highest-conviction calls at 7/10 (Silver BEARISH, Russell BULLISH) both delivered emphatically, while the lone miss came from a 6/10 call on bonds. When your strongest conviction produces your best results, the system is working.

The average confidence of 6.2 represents a meaningful step up from recent weeks where the desk was whispering directional views at 5/10 and hoping nobody noticed. Crude oil's 9.83% bearish win at 5/10 is now the sixth consecutive correct bearish call on energy, a streak that stretches back to late May and has delivered cumulative downside of roughly 35% from the $120 March war peak to current levels near $77. That is the desk's best sustained single-market performance of 2026, and the conviction has been appropriately modest throughout.

|

51/91

Correct / Total

|

56%

Accuracy

|

91 / 104

Directional / No Call

|

The rolling twelve-week figure sits at 56% across 91 directional calls, with 104 no-call abstentions. That engagement split tells you the desk calls direction on fewer than half of all market-weeks, a rate that has been declining since February's 70% pace. This week's 80% helps modestly, but the denominator barely moves when you add only five calls to it. The wartime volatility weeks from April continue to drag the rolling average, though the very worst of the December and January horror shows have now fully aged out of the window. If the desk can increase its directional volume to seven or eight calls while maintaining accuracy above 70%, we should finally see this number climb toward 60%.

|

Bias Called

BULLISH

|

Confidence

7/10

|

Result

CORRECT

|

Grade

A

|

| Monday Open | 2920.5 |

| Friday Close | 2995.6 |

| Move | 2.57 |

| ▼ R2 | 2947 |

| ▼ R1 | 2940 |

| ▲ S1 | 2890 |

| ▲ S2 | 2860 |

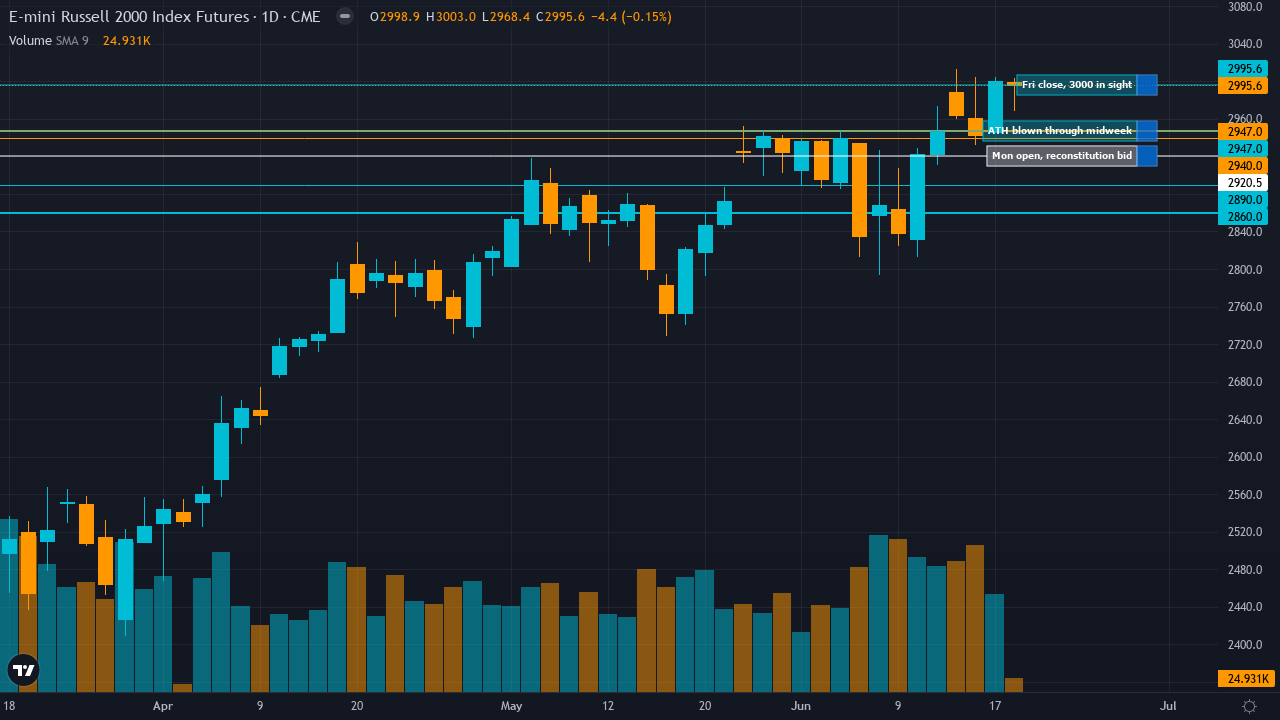

R2 at 2947, the May 27 all-time high, was breached cleanly. The Russell opened Monday at 2920.5, consolidated through the early part of the week near the desk's pivot zone, then accelerated through both resistance levels as reconstitution flows began building toward the June 26 effective date. Friday's close at 2995.6 landed 49 points above R2 and just 5 points short of the 3000 psychological level that had never been touched before. S1 at 2890 was never seriously tested. S2 at 2860 belonged to a different week entirely. The levels framework correctly identified the all-time high as the key overhead obstacle, but the magnitude of the breakout meant both resistance levels were left behind by mid-week.

The called edge centred on the Russell reconstitution effective June 26, which the desk identified as creating an estimated $200 billion in forced mechanical rebalancing flows into small caps. CME Group confirmed approximately $11 trillion is benchmarked to Russell indices. The desk also flagged extreme sentiment capitulation at AAII 47.7% bears and Fear & Greed at 34 as a contrarian setup, while Seeking Alpha's June 13 article confirmed institutional rotation into small and micro caps for the second consecutive week. That thesis was validated comprehensively. The reconstitution calendar provided the structural bid, the sentiment extreme provided the entry point, and the macro backdrop of Warsh's first FOMC resolving without a hawkish surprise provided the permissive environment for risk appetite to recover.

All six disciplines pointed BULLISH, the rarest possible configuration in the desk's framework. The Sentiment agent at 25% weight identified the AAII 47.7% bear reading as a 1-year pessimistic extreme, creating the contrarian foundation. The Economic agent at 25% correctly read the RISK-ON macro regime with VIX sub-20 and May employment data as supportive. The Technical agent at 20% confirmed the constructive structure above both 50-day and 200-day MAs with RSI at 34 oversold, creating a mean-reversion setup. The Institutional agent at 10% flagged the reconstitution calendar flows as the mechanical catalyst. The Options agent at 15% confirmed VIX normalisation. The Fundamental agent at 5% provided the earnings validation backdrop. When all six disciplines agree and the market delivers 2.57%, the synthesis framework is doing exactly what it was designed to do.

The Russell 2000 made its debut as Market of the Week, and the timing could not have been better. The desk called BULLISH at 7/10 conviction, its joint-highest of the week alongside silver, and the index surged 2.57% from Monday's 2920.5 to Friday's 2995.6, pushing within a hair's breadth of 3000 for the first time in history.

The reconstitution narrative was the week's defining structural driver. FTSE Russell published its preliminary additions and deletions on May 22, with the June 26 effective date now just seven days away. LSEG confirmed the reconstitution would be the first of a new semi-annual schedule, with approximately $11 trillion benchmarked to Russell indices creating what CME Group described as 'massive asset reallocation flows.' The desk's observation that this mechanical buying pressure would support small caps regardless of macro conditions proved correct, as the index powered through both called resistance levels without pause.

The Warsh FOMC on Wednesday was the week's other defining event. NPR reported the Fed held rates steady and 'signaled its next move could be a rate increase,' while Investopedia confirmed Warsh announced plans to overhaul Fed operations through five new task forces. The market's reaction was remarkably sanguine. Rather than sell on the hawkish tilt, equities rallied through the announcement, suggesting investors interpreted Warsh's inaugural rhetoric as careful positioning rather than imminent action. The Russell, with its higher sensitivity to rate expectations, would have been the first casualty of a genuine hawkish surprise. Instead, it accelerated.

The free MOTW report, published on the Ghost site Sunday evening, laid out the reconstitution thesis alongside the sentiment contrarian setup and identified the May 27 all-time high at 2947 as R2. Readers who used that framework had both the structural reason to buy the dip early in the week and the resistance level to monitor as the breakout developed. The fact that price blew through R2 by 49 points and approached 3000 tells you the reconstitution flows were even stronger than the desk's own framework anticipated.

The grade is A rather than A+ because, while direction was correct at strong conviction and the thesis nailed the primary driver, the levels framework was too conservative on the upside. When your R2 is breached by nearly 50 points, the upper boundary needed to be wider. For a first-ever MOTW appearance, the Russell delivered exactly the kind of performance that justifies featuring Extended-tier markets alongside the usual suspects.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 6/10 | 7435 | 7556.25 | 1.63 | CORRECT | B+ |

| BULLISH at 6/10 and the S&P gained 1.63% through the Warsh FOMC week to fresh highs above 7,550. The sentiment contrarian thesis and 200-day MA support held, and the market treated the new Fed Chair's debut as permission to rally rather than reason to panic. Direction correct, conviction appropriate, and the desk's equity read continues to improve after the June selloff debacle. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 29662 | 30647 | 3.32 | — | — |

| NO CALL at 5/10 on a 3.32% surge. The Nasdaq exploded higher through the FOMC week, reclaiming 30,000 with authority. I have lost count of how many times I have written that a 3%+ NQ move on a NO CALL is the kind of thing a prediction desk exists to catch. The signal sat at 0.7, below the 1.0 threshold. Procedure followed. Opportunity squandered. The desk's NQ relationship remains complicated. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | 84.88 | 76.54 | -9.83 | CORRECT | A+ |

| BEARISH at minimum conviction and crude collapsed 9.83% to $76.54, its lowest since before the Iran war repriced energy markets in February. Trading Economics confirmed a weekly decline of around 10% as Hormuz shipping flows normalised. Six consecutive correct bearish calls now. The desk's best sustained single-market streak of 2026, delivered with the kind of whispered conviction that says 'we remember getting burned' on every contract. | |||||||

|

Gold

CORE

|

NO CALL | — | 4238.8 | 4172.9 | -1.55 | — | — |

| NO CALL per mandatory miss reset after nine consecutive missed directional calls. Gold dropped another 1.55% to $4,173, now down 26% from the January $5,626 peak. The desk was procedurally locked out while the correction deepened further through the FOMC week. Nine misses in a row is the longest losing streak on any single market this year, and the mandatory neutral stance is the system doing what it was designed to do, even if the result feels like watching a house burn down from behind the fire line. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1627 | 1.1509 | -1.01 | — | — |

| NO CALL for the sixteenth consecutive week, and the euro dropped a full percent. The longest NO CALL streak on the board just got longer, while the currency it is attached to finally decided to move. A 1.01% decline is the largest EUR/USD weekly move since the March war selloff. The desk and this pair have a non-aggression pact that the pair is increasingly violating unilaterally. | |||||||

|

Silver

EXTENDED

|

BEARISH | 7/10 | 68 | 64.91 | -4.54 | CORRECT | A |

| BEARISH at 7/10, the desk's joint-highest conviction, and silver dropped 4.54% to $64.91. Five consecutive correct bearish calls now, with the metal down 47% from its January $121.64 peak. The 200-day MA at $68.09 gave way decisively, and the Warsh FOMC hawkish tilt sustained the real yield headwinds the desk identified. The silver bearish streak has become the desk's most reliable recurring theme alongside crude. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.0062915 | 0.006241 | -0.81 | — | — |

| NO CALL for the sixteenth consecutive week, the yen weakened 0.81% past the noise threshold. The BoJ met June 15-16 within the grading window, and whatever happened there produced a move the desk missed from the sidelines. The desk's yen discipline has saved it from many wrong calls this year, but sixteen consecutive abstentions is starting to feel less like wisdom and more like learned helplessness. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.3407 | 1.3227 | -1.34 | — | — |

| NO CALL for the fourteenth consecutive week, and sterling dropped 1.34%. The BoE met on June 18 within the grading window, and the pound's decline suggests the decision was not friendly to cable bulls. A 1.34% FX move on a NO CALL is a proper miss. The desk's cable hibernation, which I have been documenting since March, continues to cost increasingly visible opportunities. | |||||||

|

Copper

EXTENDED

|

NO CALL | — | 6.45 | 6.337 | -1.75 | — | — |

| NO CALL at 5/10 with signal below minimum threshold, copper fell 1.75%. After two consecutive wrong-direction calls that I described as 'chasing its own tail,' the desk wisely stepped aside and let the market resolve its fundamental-technical conflict without placing a bet. The 1.75% miss is frustrating, but given last week's MOTW debacle, the restraint was justified. | |||||||

|

Russell 2000

EXTENDED

|

BULLISH | 7/10 | 2920.5 | 2995.6 | 2.57 | CORRECT | A |

| This week's MOTW. BULLISH at 7/10 on the reconstitution thesis and sentiment contrarian setup, the Russell surged 2.57% to within 5 points of 3000, a level never before reached. All six disciplines pointed bullish. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | 0.7041 | 0.6998 | -0.62 | — | — |

| NO CALL at 5/10 ahead of the RBA meeting that fell on June 16 within the grading window, and the Aussie slipped 0.62%. The signal at 0.875 fell below the FX_MAJOR 1.1 threshold. The RBA policy divergence thesis that was once the desk's most reliable FX call has been dormant for weeks. A modest miss by NO CALL standards. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 6/10 | 111.875 | 112.78 | 0.81 | MISSED | C |

| BEARISH at 6/10 and bonds rallied 0.81%. The desk positioned for Warsh's debut to deliver a hawkish surprise, and while he did hint at future rate increases, the market interpreted the rhetoric as cautious rather than aggressive. The desk's long-running bearish bond thesis, which was its most consistent performer through the spring, has now missed in consecutive weeks as the crude oil collapse eases inflation fears. | |||||||

|

Wheat

FULL DESK

|

NO CALL | — | 584.4 | 605.75 | 3.65 | — | — |

| NO CALL at 5/10 on a 3.65% rally. Wheat surged as the worst US production since 1972 and record managed money net short positioning at -77,593 contracts created the squeeze the desk's own synthesis identified as a tail risk but refused to trade. When your analysis spots the asymmetric short-covering setup and then issues NO CALL because the signal sits at 0.5, the procedure is clean but the P&L opportunity is gone. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | — | 1113.5 | 1122.75 | 0.83 | — | — |

| NO CALL at 5/10 on a 0.83% gain. Soybeans drifted modestly higher within the noise threshold, and the desk's abstention was cleanly validated. The renewable diesel structural demand floor continues providing quiet support, and the signal below the minimum threshold kept the desk sensibly on the sidelines. | |||||||

|

Platinum

FULL DESK

|

NO CALL | — | 1715 | 1668.2 | -2.73 | — | — |

| NO CALL per mandatory miss reset after six consecutive missed calls, and platinum fell 2.73% to $1,668. The metal is now down 43% from its January $2,915 peak. The WPIC deficit thesis, which the Fundamental agent has championed all year, offered no protection once again. The mandatory neutral stance saved the desk from a seventh consecutive miss, which is the system working as designed, even as the metal continues its slow-motion collapse. | |||||||

|

✦ Best Call: Crude Oil (CL)

BEARISH at 5/10 and crude oil collapsed 9.83% from $84.88 to $76.54. Trading Economics confirmed WTI was on track for a weekly decline of around 10% as Strait of Hormuz shipping flows began normalising. That is now six consecutive correct bearish calls on crude, a streak that stretches back to late May and has delivered cumulative downside from the $120 March war peak to current levels near $77. The geopolitical premium that defined Q1 2026 has been almost entirely erased. The desk whispered its view at minimum conviction, which given the history of crude oil whipsawing both directions by 13% in the same month is entirely appropriate humility. But an oil move this large, catching the tail end of a structural mean reversion that the desk has been riding for six weeks, is the kind of thing that makes you wonder whether the conviction should have been higher. Then you remember March and April, and the 5/10 starts to look quite wise. |

⚠️ Worst Call: 30Y Treasury (ZB)

BEARISH at 6/10 and bonds rallied 0.81%. The desk positioned for Warsh's debut to deliver a hawkish surprise, citing Forbes' June 8 reporting about potential removal of easing bias from the statement and May CPI at 4.2% as structural headwinds. The FOMC held as expected, and while Warsh did hint at future rate increases per NPR, the market interpreted his rhetoric as measured rather than menacing. Bonds rallied on relief that the new Chair's first meeting produced evolution rather than revolution. When your thesis requires a central banker to be maximally hawkish on day one and he chooses diplomacy instead, the direction call was always going to be vulnerable. A small miss at moderate conviction. |

The Economic agent had the strongest week across the desk's directional calls. Its identification of the RISK-ON macro regime supporting equities, its bearish energy framework through demand destruction and Strait normalisation, and its reading of the FOMC binary risk as manageable rather than catastrophic all proved directionally useful. On crude oil in particular, the Economic agent's sustained bearish conviction since late May has powered the desk's longest active winning streak of 2026.

The Sentiment agent also earned its keep, with the contrarian setup it identified on the Russell, AAII bears at 47.7% and Fear & Greed at 34, proving to be the precise entry signal for a 2.57% rally. I have spent months criticising the Sentiment agent for being 'too cautious' or 'offering no useful signal.' This week it was the analytical backbone of the MOTW call. Credit where due. The weakest performer was the collective framework on Treasury bonds, where the Economic agent's hawkish FOMC thesis and the Fundamental agent's bearish fiscal deficit narrative were both directionally wrong. Warsh chose caution over confrontation on day one, and the bond disciplines did not price that possibility adequately.

The Russell reconstitution effective date lands on June 26, which means next week is the culmination of the mechanical flows the desk has been positioning for. Whether the index holds above 3000 or experiences sell-the-news exhaustion will be the small-cap story of the month. Crude oil at $77 is rapidly approaching J.P. Morgan's $60 Brent fair value territory, and whether the Hormuz normalisation continues or stalls will determine if the desk's six-week bearish streak extends to seven. The Warsh FOMC aftermath continues to ripple through rates, with markets now pricing genuine hike risk for the first time this cycle. Gold at $4,173, down 26% from January's peak, faces the question of whether the FOMC clarity provides a floor or whether the new hawkish regime pushes it toward $4,000. The desk will have its Sunday views. I expect the NO CALL count to remain elevated through the summer lull.