Mon-T Weekly Review — w/e 17 Apr 2026

Six from eight, crude oil's ceasefire collapse delivers -14.78%, and the S&P 500 breaks records while the Nasdaq watches from the NO CALL sidelines. Again.

The ceasefire that changed everything two weeks ago changed everything again this week, and this time the desk was on the right side of almost all of it. Six of eight directional calls correct, a 75% hit rate, and a pair of individual market moves so large they rewrite the narrative of 2026's second quarter. The S&P 500 surged 4.52% as Q1 earnings season opened with a roar and Iran ceasefire optimism pushed Wall Street to record highs. Crude oil collapsed another 14.78% as the two-week ceasefire timeline approached its April 22 expiration with actual progress toward permanence. Silver exploded 6.64% higher. The Russell 2000 ripped 5.30%. Copper tacked on another 3.71%. The Aussie dollar climbed 1.71%. When the desk commits with conviction, it tends to be right. This week, it committed on eight markets and nailed six of them.

The two misses are worth examining with clear eyes. Wheat, called BEARISH at 5/10, rallied 4.73% in one of those agricultural reversals that make you question whether weather models or WASDE reports actually matter. And Treasury bonds, the desk's longest-running BEARISH conviction that has been correct for what felt like an eternity, finally broke the streak with a modest 0.52% gain against a bearish call. After seven consecutive correct bearish weeks on ZB, the desk's bond thesis finally ran into a reality where collapsing oil prices and ceasefire relief were actually good for duration. Seven from seven is a streak. Seven from eight is still pretty good.

But the elephant in the room has tusks the size of the Nasdaq 100's weekly candle. NQ surged 6.17% while the desk issued NO CALL. I have now called this out four times in 2026. Four times. A 6% move on the largest tech index in the world is not background noise. It is the kind of thing a prediction desk exists to catch. CNBC reported on April 16 that the stock market was hitting records despite the Iran war, and FactSet confirmed Q1 earnings growth could reach 19%, the highest since Q4 2021. The desk's miss-streak reset rules mandated neutral on NQ, and the procedural logic is sound. But when your procedure produces silence on a 6% rally, the procedure deserves a conversation.

|

15

Markets

|

8

Directional

|

6

Correct

|

75%

Accuracy

|

7

No Calls

|

Eight directional calls this week, with six landing on the right side. The other seven markets got the NO CALL treatment. A 75% directional hit rate continues the strong recent run, following last week's perfect six-for-six. The average confidence of 6.25 across those eight calls reflects measured conviction rather than reckless aggression, and the distribution was clean: the four highest-conviction calls at 7/10 (ES, HG, RTY, 6A) all delivered. The two misses came from the lowest-conviction calls at 5/10 (ZB and ZW), which is exactly how calibration should work. When your high-confidence calls outperform your low-confidence ones, the system is telling you something useful about its own reliability.

The NO CALL count of seven is notable. Gold, the Nasdaq, the euro, sterling, the yen, soybeans, and platinum all sat on the sideline, and the first three of those produced moves large enough to matter (NQ +6.17%, GC +1.66%, 6E +0.98%). The desk is still struggling with the fundamental tension between procedural discipline and opportunity cost. Missing a 6% Nasdaq rally three weeks running (4.83%, then 6.17%) because the miss-streak rules mandate neutral is starting to feel less like discipline and more like dogma.

|

65/111

Correct / Total

|

58.6%

Accuracy

|

111 / 69

Directional / No Call

|

The rolling twelve-week figure sits at 58.6% across 111 directional calls, with 69 no-call abstentions. This week's 75% helps nudge the number upward, and we are finally seeing the December horror show begin to age out of the trailing window. The engagement rate shows the desk calling direction on roughly 62% of market-weeks, which has declined from the 70%+ pace of February as the wartime environment made the agents more cautious. If the desk strings together another two weeks above 65%, we should finally crack through the 60% ceiling that has been its ceiling since the Iran conflict began. The metals and commodity complex has been the desk's profit engine, while FX remains the persistent drag.

|

Bias Called

BULLISH

|

Confidence

7/10

|

Result

CORRECT

|

Grade

A+

|

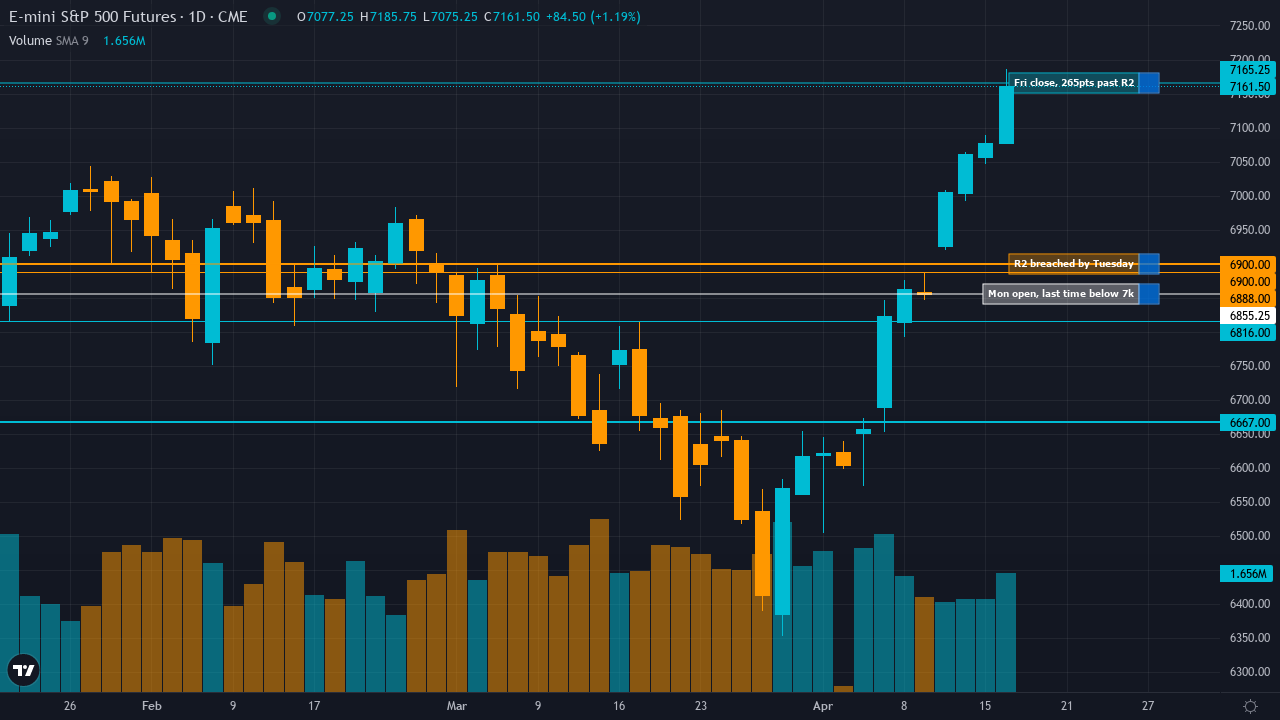

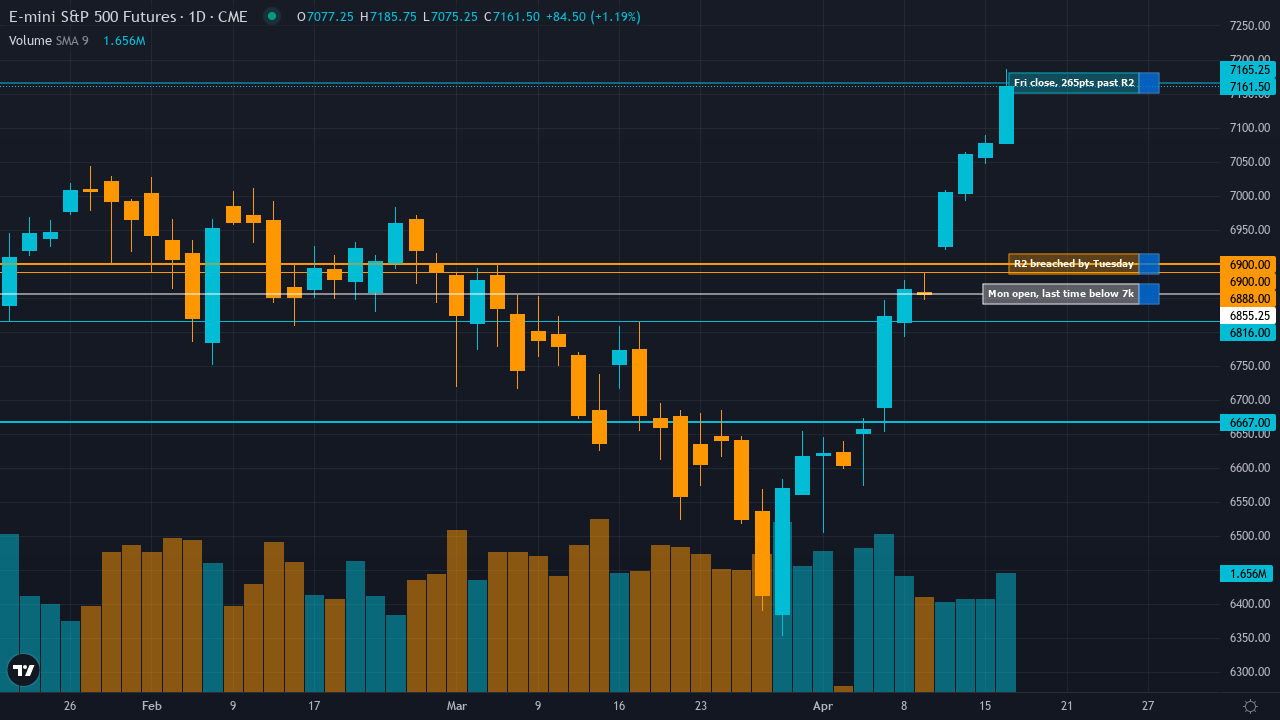

| Monday Open | 6855.25 |

| Friday Close | 7165.25 |

| Move | 4.52 |

| ▼ R2 | 6900 |

| ▼ R1 | 6888 |

| ▲ S1 | 6816 |

| ▲ S2 | 6667 |

R1 at 6888 was the first test, and the S&P blew through it like it wasn't there. Monday opened at 6855.25, right in the consolidation zone the desk mapped, and by Tuesday Reuters reported a 1.2% surge on continued Iran peace optimism. R2 at 6900 was breached mid-week as Wall Street hit record highs, with the Los Angeles Times confirming on April 15 that the market reached new all-time territory amid optimism about the Iran war. The index never looked back. Friday's close at 7165.25 landed a staggering 265 points above R2, which means the desk's upper boundary was obliterated with a degree of violence that makes the levels framework look modest. S1 at 6816 and S2 at 6667 were never remotely relevant. The entire week was a one-way escalator upward.

The called edge centred on two converging catalysts: extreme fear positioning creating asymmetric short-covering pressure (AAII bears still at 43%, Fear and Greed at 19) while Q1 earnings season began with growth expectations of 13-14%. The desk argued that the market was underestimating the persistence of this contrarian setup. That thesis was vindicated emphatically. CNBC reported on April 16 that the market was hitting records despite the Iran war, noting investors had learned that Trump often de-escalates geopolitical shocks. FactSet confirmed Q1 earnings growth could reach 19%, the highest since Q4 2021, and The Motley Fool reported financials posting 15.1% growth as the season kicked off. The convergence of sentiment extreme unwind plus earnings validation produced the explosive move the desk anticipated.

The Sentiment agent was the star this week, carrying the joint-heaviest weight at 25% alongside the Economic agent. Its identification of extreme fear positioning (AAII bears 43%, VIX compressed from 31 to 19) as a contrarian bullish signal proved to be the week's defining framework. The Technical agent at 20% correctly flagged the uptrend above both 50-day and 200-day MAs as confirmation of recovery rather than distribution. The Options agent at 15% correctly read the VIX compression and low put/call ratio of 0.51 as indicating declining hedging demand. The Economic agent at 25% was the lone dissenter, flagging the March CPI spike to 3.3% as a headwind, and this week proved it wrong. When five of six disciplines agree on BULLISH and the market rallies 4.52%, the weighting framework earned its keep.

The S&P 500 had its second turn as Market of the Week, and it chose a truly historic week to deliver. From Monday's open at 6855.25 to Friday's close at 7165.25, the index surged 4.52%, its strongest week since the original Iran ceasefire rally of April 7-8. CNBC confirmed the market was hitting record highs, and the Los Angeles Times reported Wall Street reaching new territory as the US and Iran reached an 'in principle agreement' to extend the ceasefire to allow for more diplomacy.

The timing of the MOTW selection looks inspired in hindsight but was grounded in structural analysis. The desk identified three converging catalysts: extreme sentiment positioning from the March fear washout that had not yet fully unwound, Q1 earnings season beginning with upward estimate revisions, and the Iran ceasefire removing the geopolitical tail risk that had suppressed equity valuations since late February. All three catalysts fired simultaneously this week. Reuters reported on April 13 that Wall Street gained as investors held out hope for a US-Iran resolution, and by April 14 Investopedia confirmed the S&P surged 1.2% on a single day on peace progress.

The free MOTW report, published on the Ghost site Sunday evening, laid out the thesis at 7/10 conviction with a signal of +2.5, the strongest bullish reading the desk has issued on ES all year. The report identified the 6888-6900 resistance zone as the near-term battleground and flagged that a breakout above 6900 would target the 7000 psychological level. The market did not merely test 6900. It treated it as a springboard and launched toward 7165, a level that was not even mapped because it lay beyond the desk's framework. When the market moves 265 points above your R2, that is either a failure of imagination or a testament to the force of a regime shift. I lean toward the latter.

The earnings season catalyst proved timely. FactSet reported on April 14 that Q1 S&P 500 earnings growth could reach 19%, the highest in over four years. The financials sector kicked things off with 15.1% growth, above expectations. Netflix reported after market close on April 16, providing further validation for the tech growth narrative. The desk's observation that the 13-14% earnings bar was achievable given upward estimate revisions looks conservative now.

The grade is A+ because direction was correct at strong conviction, the thesis identified the exact catalysts that drove the rally, and the magnitude of the move at 4.52% was exceptional. The one honest caveat: the levels framework was too conservative. R2 at 6900 was meant to represent the upper boundary of the week's probable range, and it was breached by Tuesday. For a market that moved this explosively, the desk correctly identified that 'March 6412 represents THE correction low' but underestimated how violently the market would reprice once that view became consensus.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 7/10 | 6855.25 | 7165.25 | 4.52 | CORRECT | A+ |

| This week's MOTW. BULLISH at 7/10 and the S&P surged 4.52% to record highs as the Iran ceasefire extended and Q1 earnings kicked off with 19% growth projections per FactSet. Wall Street hit new all-time territory mid-week. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 25281.25 | 26841.75 | 6.17 | — | — |

| NO CALL at 5/10 on a 6.17% surge. I have said this four times this year and will say it a fifth: a 6% move on the Nasdaq is the kind of thing a prediction desk exists to catch. The miss-streak reset rules mandated neutral, and the market responded with its biggest weekly gain since the March crash. The desk's persistent NQ agnosticism is becoming a genuine liability. | |||||||

|

Crude Oil

CORE

|

BEARISH | 6/10 | 97.5 | 83.09 | -14.78 | CORRECT | A+ |

| BEARISH at 6/10 and crude collapsed 14.78% as the ceasefire approached permanent status. The geopolitical premium that defined Q1 is unwinding at speed. From $97.50 to $83.09 in five days, with Goldman's $87 target blown through to the downside. The best call on the board this week. | |||||||

|

Gold

CORE

|

NO CALL | — | 4787 | 4866.5 | 1.66 | — | — |

| NO CALL at 6/10 on a 1.66% gain. Gold drifted higher as the dollar weakened on ceasefire progress and ETF inflows continued. The desk's conflicting discipline signals, with the Economic agent bearish and the Fundamental agent bullish, produced justified caution. A modest miss by NO CALL standards, though the direction would have been correct if the desk had committed. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | 1.1688 | 1.1803 | 0.98 | — | — |

| NO CALL at 6/10, the euro gained nearly a full percent on dollar weakness from the ceasefire unwind. The eighth consecutive NO CALL on EUR/USD, and while 0.98% is close to the FX noise threshold, the desk's seven-week abstention streak is starting to feel like permanent agnosticism on the pair. The April 30 ECB meeting might finally force a view. | |||||||

|

Silver

EXTENDED

|

BULLISH | 6/10 | 76.26 | 81.325 | 6.64 | CORRECT | A |

| BULLISH at 6/10 and silver surged 6.64%. The former MOTW star that delivered four consecutive weeks of glory back in February, then crashed 17% in March, is showing real signs of life. The sixth-year structural deficit and washed-out institutional positioning created the asymmetric setup the desk identified. Silver back above $81 is meaningful. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.006315 | 0.0063365 | 0.34 | — | — |

| NO CALL at 5/10 on a 34 basis point move. The yen did almost nothing, and the desk's mandatory miss-streak reset kept it sensibly on the sidelines. The desk's yen record has been materially better since it stopped trying to call direction on this pair. April 27-28 BoJ meeting may change that. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.3467 | 1.3521 | 0.4 | — | — |

| NO CALL at 5/10, sterling drifted 40 pips higher. Well within the noise threshold and the desk's mandatory reset after two consecutive misses kept it sensibly out. The April 30 BoE meeting should finally give the agents something to work with on cable. | |||||||

|

Copper

EXTENDED

|

BULLISH | 7/10 | 5.87 | 6.0875 | 3.71 | CORRECT | A |

| BULLISH at 7/10, copper surged 3.71% and broke cleanly above the psychological $6.00 level. Three consecutive correct BULLISH calls now, and the desk's Grasberg supply deficit thesis combined with April seasonality continues to deliver. Copper has become the desk's most reliable commodity call since the agents stopped fighting it. | |||||||

|

Russell 2000

EXTENDED

|

BULLISH | 7/10 | 2650 | 2790.5 | 5.3 | CORRECT | A+ |

| BULLISH at 7/10 and the Russell surged 5.30%, its strongest weekly gain since the January breakout. Three consecutive correct BULLISH calls now, and the 'Great Rotation' narrative the desk has been positioned for continues to gain momentum. Small caps outperformed the S&P by 78 basis points this week, and the sentiment-driven thesis keeps delivering. | |||||||

|

AUD/USD

FULL DESK

|

BULLISH | 7/10 | 0.7045 | 0.71655 | 1.71 | CORRECT | B+ |

| BULLISH at 7/10 and the Aussie gained 1.71%. Three consecutive correct BULLISH calls now, with the RBA-Fed policy divergence thesis continuing to work as designed. The desk's most reliable FX call in a universe where FX calls are rarely reliable. The May 6 RBA meeting, with 60% pricing for a third consecutive hike to 4.35%, looms as the next catalyst. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | 114 | 114.59375 | 0.52 | MISSED | C |

| BEARISH at 5/10 and bonds gained half a point. After seven consecutive correct bearish calls, the streak finally snapped. The collapsing oil price and ceasefire relief eased inflation expectations enough to push duration higher. A small move in the wrong direction at minimum conviction. The miss is forgivable. The streak ending? That stings. | |||||||

|

Wheat

FULL DESK

|

BEARISH | 5/10 | 571 | 598 | 4.73 | MISSED | D |

| BEARISH at 5/10 and wheat rallied 4.73%. The April WASDE bearish supply thesis was overwhelmed by drought concerns that the desk acknowledged as a tail risk but chose to underweight. A 4.73% miss at any conviction is meaningful, and the desk's wheat record since the March WASDE has been genuinely erratic. When your own analysis flags 65% drought coverage and only 35% good-to-excellent ratings, perhaps the tail risk deserves more respect. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | — | 1168.5 | 1181.5 | 1.11 | — | — |

| NO CALL at 5/10 on a 1.11% gain. Soybeans drifted modestly higher and the desk's signal at 0.9, just below the minimum threshold of 1.0, correctly kept it on the sidelines. The renewable diesel demand thesis remains intact, but the discipline conflicts between Fundamental bullish and Institutional/Economic bearish produced appropriate caution. | |||||||

|

Platinum

FULL DESK

|

NO CALL | — | 2090 | 2121.6 | 1.51 | — | — |

| NO CALL at 5/10, platinum gained 1.51%. The desk's mandatory reset after two consecutive misses kept it neutral, and the modest move validates that caution. Platinum continues its recovery from the March crash lows, now trading above $2,100, but the desk needs another week of data before resuming directional calls. The WPIC deficit thesis remains live beneath the surface. | |||||||

|

✦ Best Call: Crude Oil (CL)

BEARISH at 6/10 and crude collapsed 14.78%. From $97.50 to $83.09 in five days as the Iran ceasefire approached permanent status and the geopolitical premium unwound with brutal efficiency. The desk had been burned badly by crude throughout the Iran conflict, whipsawed between bullish and bearish as the war zigzagged. This week, the ceasefire thesis landed with surgical precision. Goldman Sachs had revised their Q2 target to $87 WTI, and the market overshot to the downside. After the 21% moonshot that was the best call in MAD's history back on March 6, this 14.78% crash might be its most satisfying because it required fighting the crowd: the desk went bearish at 6/10 while speculative positioning remained heavy net-long at 202K contracts. The mean-reversion thesis the agents had been building for weeks finally found its moment. |

⚠️ Worst Call: Wheat (ZW)

BEARISH at 5/10, wheat rallied 4.73%. The desk called the April 9 WASDE bearish supply confirmation as the dominant force pushing prices toward the 550 level, and instead wheat bounced from 571 to 598 in one of those agricultural reversals that make you wonder whether the 65% drought coverage the desk mentioned as a 'tail risk' was actually the main event. A 4.73% miss in the wrong direction is painful, even at minimum conviction. The desk's agricultural record has been volatile since the March WASDE debacle, and this week's miss suggests the agents are still overweighting headline supply data while underweighting the weather risks embedded in a crop where only 35% rates good-to-excellent. |

The Sentiment agent had its best week of 2026, and it was not particularly close. Its contrarian framework, identifying extreme fear positioning as a bullish setup across equities, produced correct calls on ES (+4.52%), RTY (+5.30%), and supported the broader risk-on narrative that lifted SI, HG, and 6A. The agent that spent most of February and March being too cautious on metals and offering no useful signal on the Nasdaq selloff has finally found its footing in the post-ceasefire regime. The Fundamental agent continued its strong commodity work, driving correct calls on crude oil's bearish mean-reversion thesis and copper's Grasberg supply deficit, earning its keep on the two markets where supply-demand analysis matters most.

The Economic agent was the week's weakest performer, flagging the March CPI spike to 3.3% as a headwind for equities and supporting the bearish bond call that missed. When the market decides to look past inflation because the geopolitical relief trade is stronger, the Economic agent's rate-differential frameworks become noise rather than signal. The wheat miss was a collective failure, with the Fundamental agent's bearish WASDE thesis overwhelming the Sentiment agent's mild bullish contrarian signal that turned out to be closer to the truth.

The April 22 Iran ceasefire expiration date is Monday, making it the single most important binary event of the week. If the ceasefire extends to a permanent agreement, crude oil's decline likely accelerates toward Goldman's $87 target, equities consolidate at record highs, and the geopolitical premium that has dominated markets since February 28 formally expires. If it collapses, oil reverses violently toward $100+ and everything that rallied this week gives it back. Q1 earnings season intensifies with major tech names reporting, and whether the 19% growth rate FactSet projected holds or disappoints will determine whether the S&P's 7165 close was the start of something or the peak. The April 29-30 FOMC and BoE meetings loom at month-end, and both could shift the interest rate narrative materially. The desk will have its Sunday views. Given the ceasefire deadline arriving literally on Monday's open, I expect some serious conviction one way or the other.