Wheat Forecast This Week — Outlook, Drivers & Key Levels

This week's Wheat outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

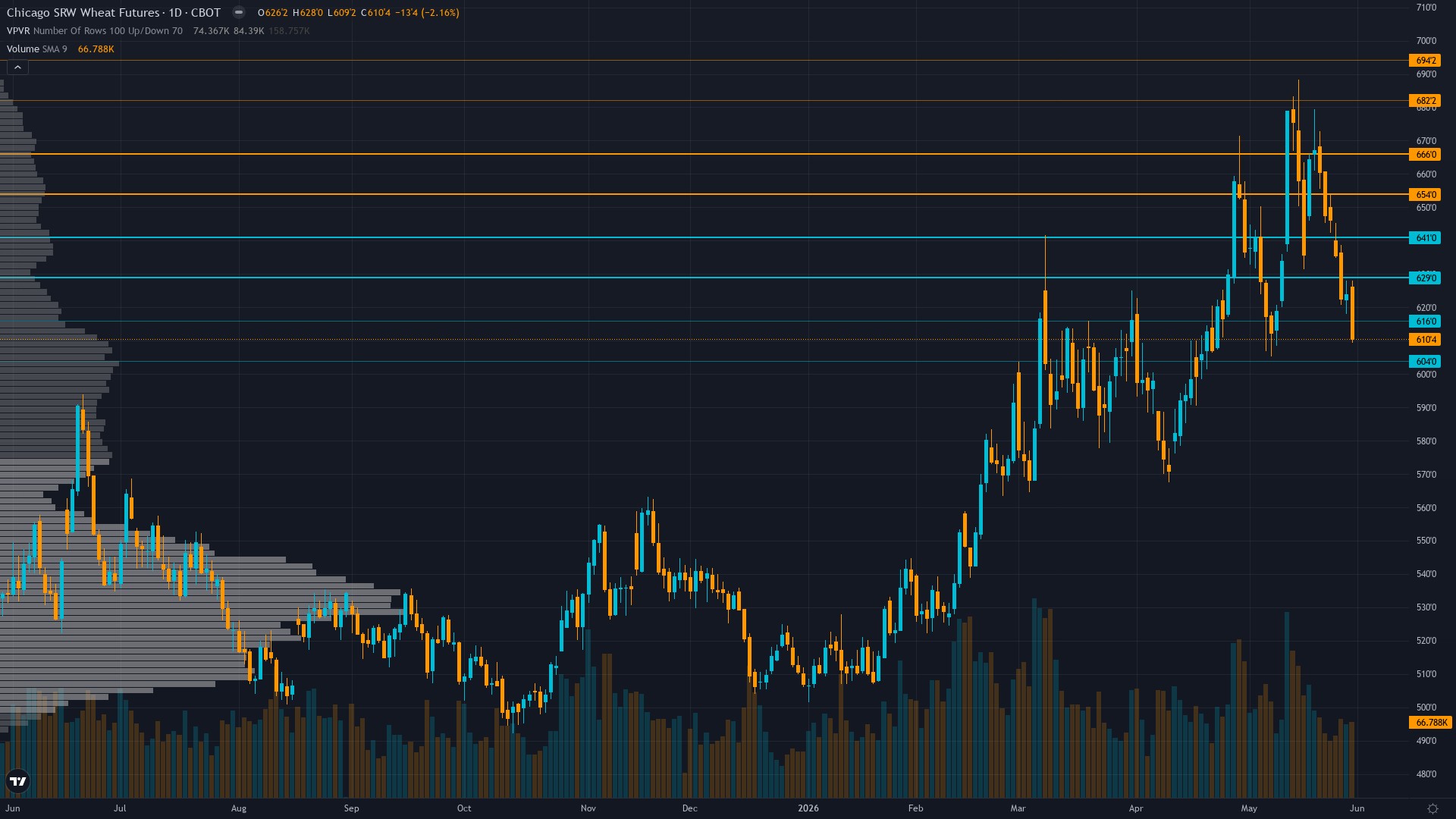

This Week's Starting Point

At 610.5, wheat has dropped 2.00% with sellers in control of the session. wheat futures is in a breaking down market state, requiring careful assessment of current conditions.

Bearish following May 13 WASDE rally reversal with market viewing advance as weather scare within structural oversupply environment expecting seasonal June-August harvest pressure to drive prices toward 575-590 support as global stocks at 954.6 million tonnes overwhelm U.S. regional tightening

Bull & Bear Case

Primary risk: Continued breakdown below 600 psychological support toward 575-590 range as June-August seasonally weak harvest pressure combines with failed drought premium thesis and global oversupply narrative at 954.6 million tonnes reasserting dominance over U.S. regional tightening concerns (Probability: high)

Primary opportunity: June 10 WASDE confirms additional U.S. production downgrades from persistent drought affecting 78% poor/fair rated crop triggering short-covering rally from current -16.7K positioning back above 620-630 as late-season yield losses materialize beyond current market pricing (Timeframe: Next 1-2 weeks through June 10 WASDE release and critical late-May/June weather window for final 2026 crop development before Southern Plains harvest completion)

This week's edge: Market has fully priced May 13 WASDE production shock (18 days aged) and is now repricing toward seasonally weak June-August harvest period, yet desk acknowledges fundamental conflict where 78% poor/fair U.S. crop ratings create tail-risk for additional June 10 WASDE production downgrades if late-May/June weather stress materializes yield losses beyond current expectations—BEARISH bias reflects breakdown confirmation yet constrained conviction 5 acknowledges two-way uncertainty and recent miss requiring analytical discipline

This Week's Catalysts & Drivers

Primary driver: Severe technical breakdown from 647 to 610.50 (-5.68% weekly decline) following May 29 MISSED BULLISH call erases two-week rally and confirms failure of drought-driven thesis as price breaks below critical 620 support despite May 13 WASDE production shock showing 1,561 million bushels (lowest since 1972)

Secondary factor: Entering historically weak June-August Northern Hemisphere harvest season with current price action DIVERGING from fundamental drought narrative (78% poor/fair crop ratings) suggesting market pricing global oversupply dominance at 954.6 million tonnes stocks over U.S. regional supply tightening creating fundamental-technical disconnect requiring resolution

Additional influence: Institutional positioning shifted from marginal net long to decisive net short -16.7K contracts as of May 8 removing squeeze fuel while month-end rebalancing flows today (May 31) and approaching Goldman Roll June 5-13 create additional near-term technical pressure on broken trend structure

Economic backdrop: TRANSITIONAL macro regime with VIX 17.44 neutral, USD at 98.94 DXY mid-range (neither strong headwind nor tailwind), Fed held at 3.50-3.75% since December 2025 with no May meeting, USDA forecast U.S. wheat exports at 775 million bushels (down 135M YoY) citing reduced price competitiveness creating mixed agricultural margin environment

Fundamental assessment: Profoundly conflicted - U.S. production at 1,561 million bushels (lowest since 1972, down 21% YoY) with only 22% good/excellent ratings creates severe supply tightening yet global stocks at 954.6 million tonnes (34.52% stocks-to-use ratio) provides structural buffer market pricing as dominant force

Technical Picture

Confirmed downtrend with price at 610.50 breaking below 620 consolidation zone and 50-day MA (~625), now testing 600 psychological support with RSI oversold low 30s, declining open interest at 238K signaling weakening conviction, immediate breakdown risk toward 575-590

At 4/10, trend strength is middling — enough to suggest a lean, but not enough to trade with high confidence.

Risk Environment

With vol at the 72th percentile, wheat price is trading in an elevated regime where daily ranges can surprise even experienced traders. Volatility is stable, with realised vol holding steady across timeframes. This equilibrium can persist but eventually resolves into expansion or contraction.

Daily ranges expanded from prior 15-20 cents to current 18-28 cent action following May 13 WASDE and subsequent breakdown requiring wider stops - sustained move below 600 psychological support or recovery above 620 would trigger accelerated directional moves given failed rally structure and elevated volatility environment with June 10 WASDE 10 days away representing next major binary catalyst

Seasonal Context

Historically, May 2026 has favoured the upside for CBOT wheat (62% win rate). Crop condition reports and weather risk peak.

Week Ahead Outlook

The next major catalyst is USDA June 2026 WASDE Report with updated winter wheat production estimates incorporating late-May/early-June weather conditions, final Southern Plains drought damage assessments, and initial 2026/27 crop year demand projections determining whether May 13 production downgrades represent floor or require further revision on Wednesday 10 June — a high-impact event that could materially shift the directional picture.

For wheat, the balance between existing momentum and scheduled risk events sets the stage for the week ahead.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime