Wheat Forecast This Week — Outlook, Drivers & Key Levels

This week's Wheat outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Where Things Stand

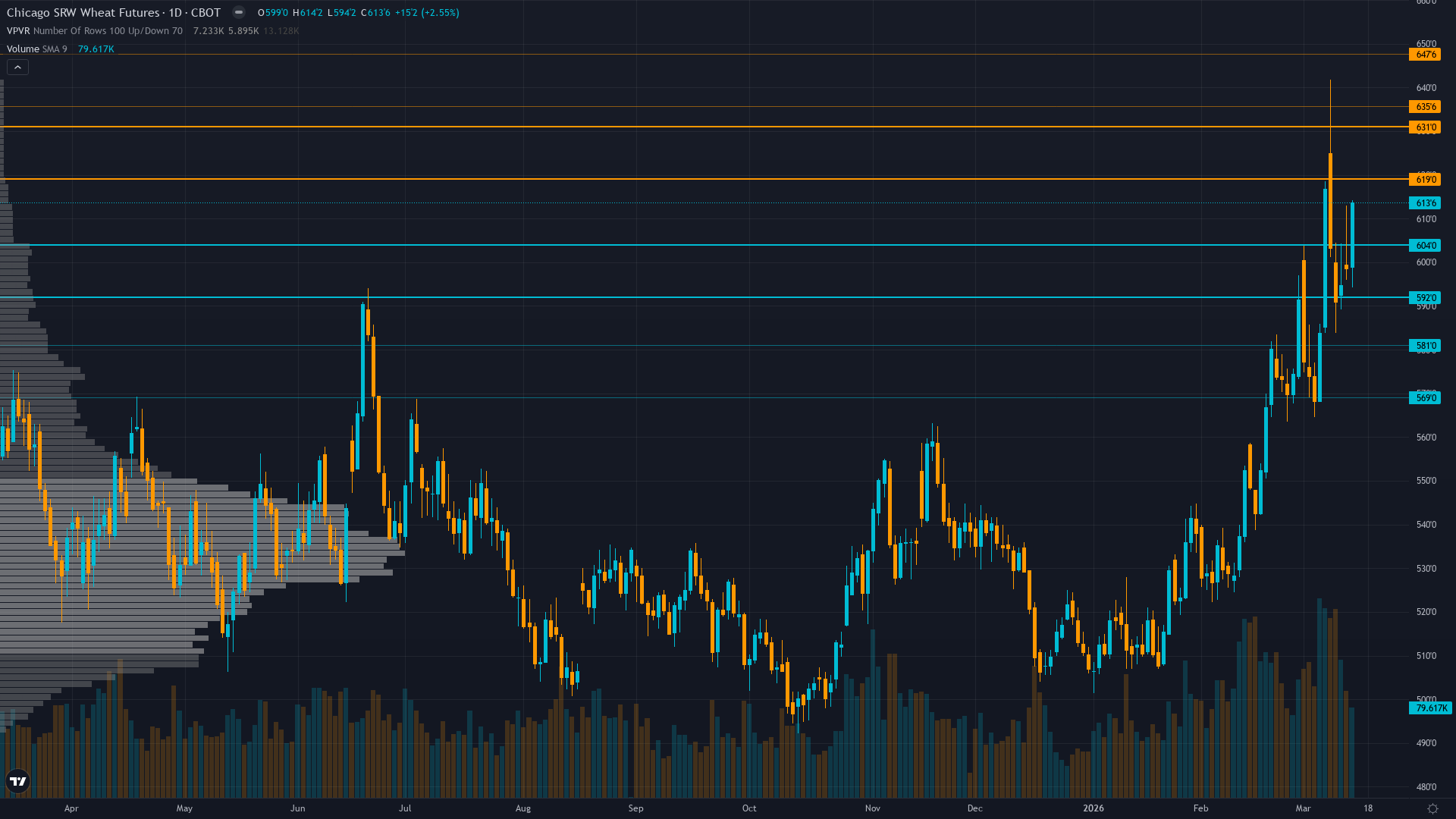

Trading at 613.75 after a 2.63% move higher, wheat continues to attract buying interest. wheat futures is consolidating, with price compressing into a narrower range as the market builds energy for its next move.

Cautiously neutral to bearish following March WASDE confirmation of ample supplies with rally viewed as short-covering event within structural bear market - consensus expects mean reversion toward 575-590 once weather premium fully dissipates

Risk-Reward Assessment

Primary risk: April WASDE confirms limited damage from February Arctic blast and early dormancy break with weather premium dissipating sending market back toward 575-590 support as structural oversupply narrative reasserts dominance and remaining spec longs exit positions (Probability: high)

Primary opportunity: March-April freeze event damages winter wheat that broke dormancy early in late February combined with geopolitical disruption to Black Sea exports triggering renewed short-covering and weather premium expansion toward 650-675 range (Timeframe: Next 3-8 weeks through April WASDE and critical March-April freeze vulnerability window)

This week's edge: Market may be underestimating March-April freeze risk from unusually early dormancy break in late February 2026 creating tail-risk scenario for severe crop damage if arctic air returns, yet positioning exhaustion and USD headwinds suggest limited edge for directional call at current levels - NEUTRAL stance appropriate given noise threshold proximity and catalyst void

Forces in Play

Primary driver: Post-WASDE consolidation at 613.75 after March 10 report showed no material changes to U.S. wheat balance sheets - market digesting 25% rally from October 492 lows while facing USD strength headwinds and declining open interest signaling weakening trend participation

Secondary factor: Short-covering exhaustion following massive spec short reduction from 109,483 contracts to 17,758 as of March 3 - 84% of bearish positioning unwound removes primary fuel for further rally without fresh catalyst

Additional influence: Structural oversupply fundamentals reasserting with global stocks at 277.5 million metric tons (five-year high) and 33.7% stocks-to-use ratio overwhelming any weather premium from February Arctic blast and early dormancy break concerns

Economic backdrop: USD strength accelerating to 100.5 DXY as of March 13 following Goldman Sachs rate cut delay to September creates direct export competitiveness headwind offsetting strong 900 million bushel U.S. export forecast

Fundamental assessment: Overwhelmingly bearish with record global supplies at 277.5 MMT yet strong U.S. export pace at 900 million bushels provides floor around 590-600 as market has fully discounted worst-case oversupply scenarios

Technical Landscape

Trading at 613.75 near 52-week high of 641.75 after 25% rally from October 492 lows but showing signs of exhaustion with declining open interest and failed breakout above 620-625 resistance zone

Trend strength registers at 6/10, suggesting meaningful but not extreme directional bias.

Volatility Backdrop

wheat price volatility at the 68th percentile reflects a balanced environment where standard risk parameters apply. Volatility remains anchored at current levels, with no clear signal of an imminent regime shift in either direction.

Daily ranges expanded from compressed 10-16 cents during late 2025 consolidation to current 20-30 cent action requiring wider stops - breakout above 625 or breakdown below 600 would trigger accelerated moves given resistance testing and elevated volatility environment

Historical Seasonal Bias

Seasonal analysis shows a historically bullish bias for CBOT wheat in March 2026, with a 58% win rate. Spring planting intentions report drives positioning.

What to Watch

USDA April 2026 WASDE Report with updated winter wheat acreage and spring planting estimates incorporating weather-adjusted production forecasts (Thursday 9 April) sits in the medium-impact category — unlikely to single-handedly shift the picture, but capable of adding directional fuel.

The interplay between consolidating market conditions and upcoming catalysts will define this week's trading landscape for ZW futures.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime