S&P 500 Forecast This Week — Outlook, Drivers & Key Levels

This week's S&P 500 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

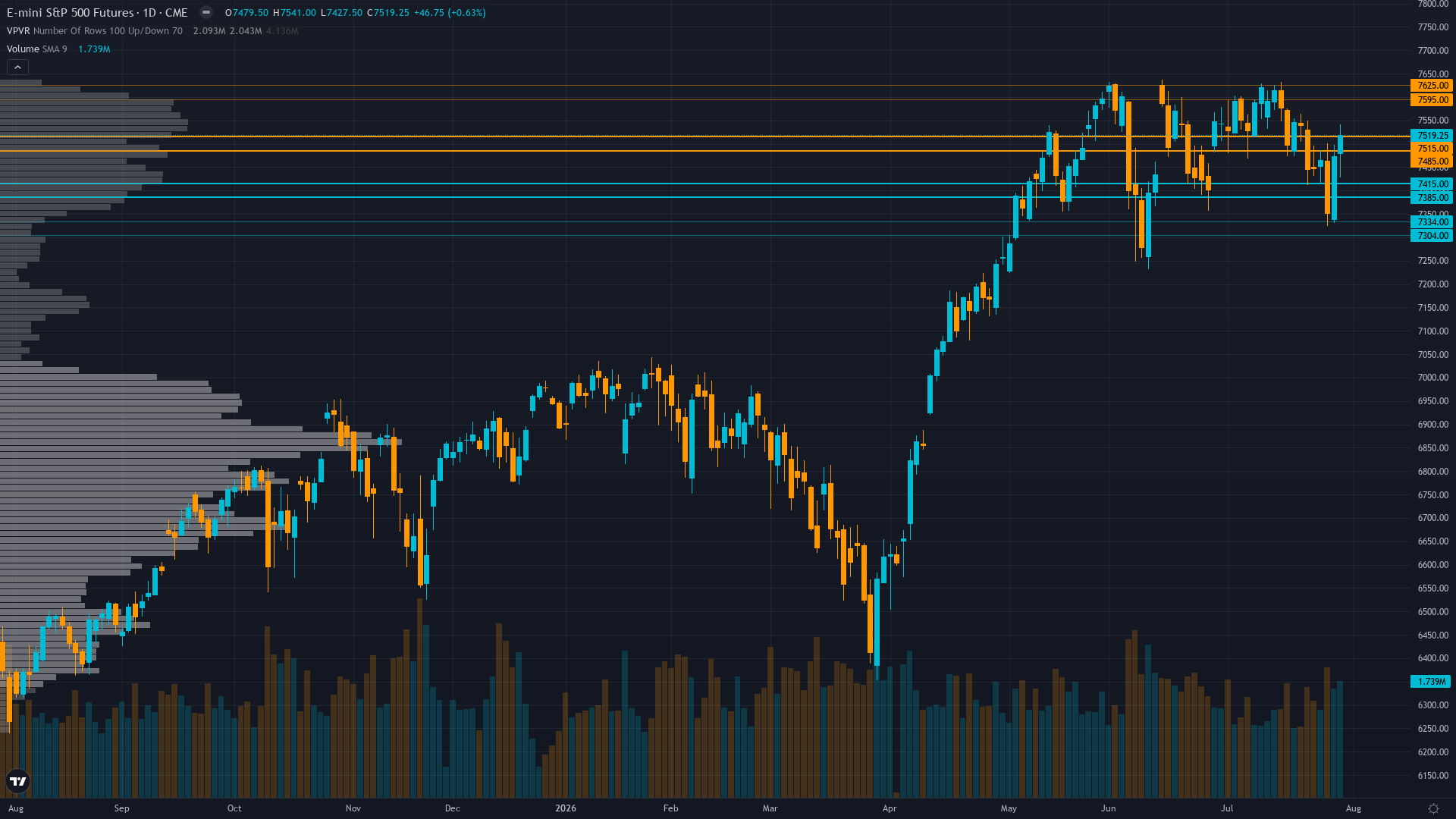

Where Things Stand

At 7435, S&P 500 has inched 0.47% higher in a measured advance. S&P 500 futures is consolidating, with price compressing into a narrower range as the market builds energy for its next move.

Divided between extreme sentiment fear suggesting oversold bounce toward 7,500-7,600 and technical breakdown continuation expecting 7,310-7,200 test, with majority positioning cautiously ahead of June 17 Warsh FOMC debut binary outcome determining resolution

What's Driving Price

Primary driver: Warsh FOMC debut June 16-17 binary catalyst approaching with extreme sentiment capitulation (AAII bears 47.7%, Fear & Greed 34) creating contrarian bullish setup, while VIX compression to 17.68 from 21.51 spike and technical consolidation at 200-day MA 7,430 inflection point creates dual-scenario risk ahead of potential hawkish language shift removing easing bias

Secondary factor: Options market shows contradictory signals with VIX 17.68 neutral range and declining volatility (-9.05% June 12) suggesting calm surface, yet equity put/call 0.56 extremely low call demand indicates complacency vulnerability despite retail survey sentiment showing extreme fear positioning at 1-year bearish highs creating wall-of-worry dynamic

Additional influence: Technical structure at critical inflection testing 200-day MA support 7,430.07 after breaking 50-day MA 7,441.23 with RSI 48.76 neutral and weak breadth (35.8% advancing vs 63.0% declining) but no confirmed breakdown yet as price holds major support creating consolidation pattern before June 17 catalyst resolution

Economic backdrop: Fed at 3.50-3.75% with Warsh debut June 16-17 FOMC pricing 99% hold but Forbes reports potential removal of easing bias language opening door to H2 2026 hikes, May ISM Manufacturing 54.0 expansion validates soft landing but Powell term expired May 15 creates policy communication uncertainty

Fundamental assessment: Forward PE 20.1-22.33x at modest 5-11% premium to 10-year average 19.0 justified by exceptional 23.2% projected CY2026 earnings growth with Q1 record margins, but Q2 margins show sequential compression risk and no new catalyst since June 5 FactSet data creating execution vulnerability

Chart Assessment

Critical inflection at 200-day MA 7,430.07 confluence after violating 50-day MA 7,441.23 on June 5 selloff, RSI 48.76 neutral after recovering from prior week's 19.67 oversold extreme, breadth weak 35.8% advancing creating corrective structure testing long-term trend support

With trend strength at 5/10, the directional signal is present but far from decisive.

Risk & Opportunity

Primary risk: Warsh FOMC June 17 delivers hawkish surprise removing easing bias language and raising terminal rate projections following May NFP beat 172K vs 85K and ISM Manufacturing 54.0 strength, triggering equity repricing from forward PE 20-22x elevated levels as put/call 0.56 complacency unwinds testing 7,310 then 7,200 support (Probability: medium)

Primary opportunity: Extreme sentiment capitulation with AAII bears 47.7% at 1-year high and Fear & Greed 34 creates contrarian reversal setup if June 17 FOMC maintains accommodative bias despite Chair transition, enabling breakout above 7,461 toward 7,620 June 2 ATH resistance as VIX compresses below 17 and RSI 48.76 neutral allows momentum expansion (Timeframe: June 17-30 2026)

This week's edge: Market may be underestimating significance of extreme sentiment capitulation with AAII bears 47.7% at 1-year high creating contrarian reversal setup within 3-7 days while overestimating June 17 FOMC hawkish surprise probability given Warsh debut typically produces cautious initial rhetoric despite Forbes easing bias removal report—extreme starting fear positioning at Fear & Greed 34 with 200-day MA 7,430 support holding creates structural bounce potential consensus underweights

Volatility Backdrop

ES futures volatility at the 52th percentile reflects a balanced environment where standard risk parameters apply. Volatility contraction continues, building the stored energy that typically precedes the next significant directional move.

Normal volatility regime suggests 1.0-1.5% daily ES moves expected with current 7,366-7,461 intraday range representing 1.3% width - June 17 FOMC binary outcome presents asymmetric expansion risk with potential 2-3% intraday swings on Warsh rhetoric surprise either direction while 200-day MA creates technical decision point

The Week Ahead

FOMC two-day meeting June 16-17 with Kevin Warsh debut as Fed Chair including SEP/dot plot release and Powell press conference 2:00pm ET June 17, markets scrutinizing rhetoric for hawkish shift after Forbes reported potential removal of easing bias language amid May data strength on Wednesday 17 June is a high-impact catalyst with the potential to redefine the near-term outlook entirely.

How S&P 500 navigates the confluence of consolidating conditions and incoming data will determine whether the current directional thesis holds or breaks.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime