Soybeans Forecast This Week — Outlook, Drivers & Key Levels

This week's Soybeans outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

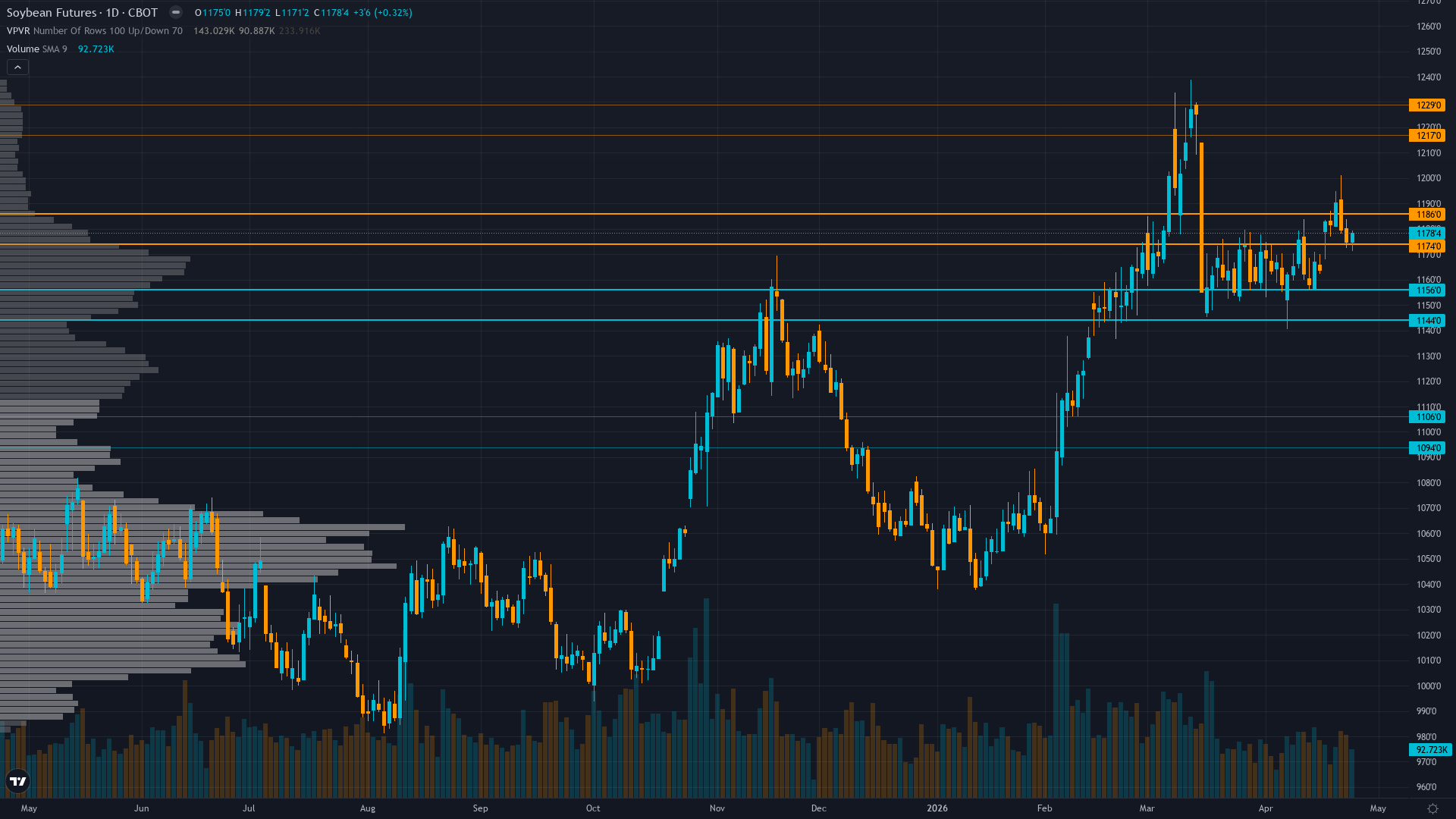

Market Overview

soybeans is trading at 1174.75, up a modest 0.36% as the market edges higher. soybean futures is range-bound and tightening, with decreasing volatility signalling a directional resolution ahead.

Mixed with technical bulls citing intact uptrend and renewable diesel structural support offset by fundamental bears noting export sales collapse to China and Brazilian pricing advantages creating range-bound consolidation expectations

This Week's Catalysts & Drivers

Primary driver: Export competitiveness crisis persists with week ending April 9 showing NO new sales to China per Brownfield Ag, confirming structural demand weakness despite 79.66% YoY export increase measured against 2025 boycott baseline

Secondary factor: Fundamental overvaluation at $11.75/bushel with global ending stocks comfortable at 124.79 MMT and Brazil's record 180 MMT harvest creating persistent 8-10% pricing pressure versus US Gulf despite renewable diesel structural floor at 2.61B bushels

Additional influence: Managed money positioning reduction continuing with 14,479 contract liquidation in week ending April 14 creating bearish institutional momentum, current net long at 192,884 contracts representing cautious repositioning from recent peaks

Economic backdrop: TRANSITIONAL macro regime with mixed signals—DXY weakness at 98.5 theoretically supporting export competitiveness offset by delayed Fed rate cuts (first cut pushed to late 2026 per Reuters April 22 poll) and crude oil at $115/bbl elevating agricultural input costs

Fundamental assessment: Moderately overvalued at current levels with comfortable global stocks and record South American production creating pricing headwinds, offset partially by tight US balance sheets at 350M bushel ending stocks and record renewable diesel demand providing structural floor

Technical Picture

Consolidating at 1174.75 cents in upper third of 52-week range (965-1223) with price holding above 50-day and 200-day moving averages, momentum constructive but approaching overbought levels near March highs

At 5/10, trend strength is middling — enough to suggest a lean, but not enough to trade with high confidence.

Bull & Bear Case

Primary risk: Sustained export sales weakness below 300K MT weekly combined with May WASDE downward revision to export projections forcing market repricing toward 1100-1150 support representing 5-8% downside as Brazilian competition at $0.80-$1.00 discount maintains persistent pricing advantage (Probability: medium)

Primary opportunity: South American late-season weather disruption during April-May critical window or unexpected surge in Chinese demand reversing export weakness triggering short-covering rally toward 1200-1223 resistance zone representing 3-5% upside (Timeframe: Next 2-4 weeks through May 9 WASDE and resolution of April export sales weakness pattern)

This week's edge: Signal magnitude -0.4 falls below 1.0 minimum threshold for AGRICULTURAL directional bias per Rule 2, mandating NO CALL despite persistent export weakness and fundamental deterioration, as severe discipline conflicts (3 bearish vs 2 bullish/neutral plus 1 no call) and TRANSITIONAL macro regime create insufficient conviction for directional lean in low-information-edge environment

Volatility Regime

Volatility for soybean price is at the 60th percentile over 90 days — a normal regime that allows for standard position sizing and conventional trade management. The vol trend is down, with contraction across timeframes creating the kind of coiled conditions that historically resolve explosively.

Current normal volatility at 60th percentile suggests 15-20 cent daily ranges near typical agricultural baseline, consolidation patterns likely with range-bound behavior requiring patience for directional conviction, standard stop placement appropriate at 20-25 cents

What to Watch

The USDA May WASDE report updating supply-demand balances, South American harvest finalization, and critical assessment of US export pace versus projections following April export weakness on Saturday 9 May stands as the week's primary risk event — high-impact and capable of overriding the existing technical and sentiment setup.

The interplay between consolidating market conditions and upcoming catalysts will define this week's trading landscape for CBOT soybeans.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime