Russell 2000 Forecast This Week — Outlook, Drivers & Key Levels

This week's Russell 2000 outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Current Market Picture

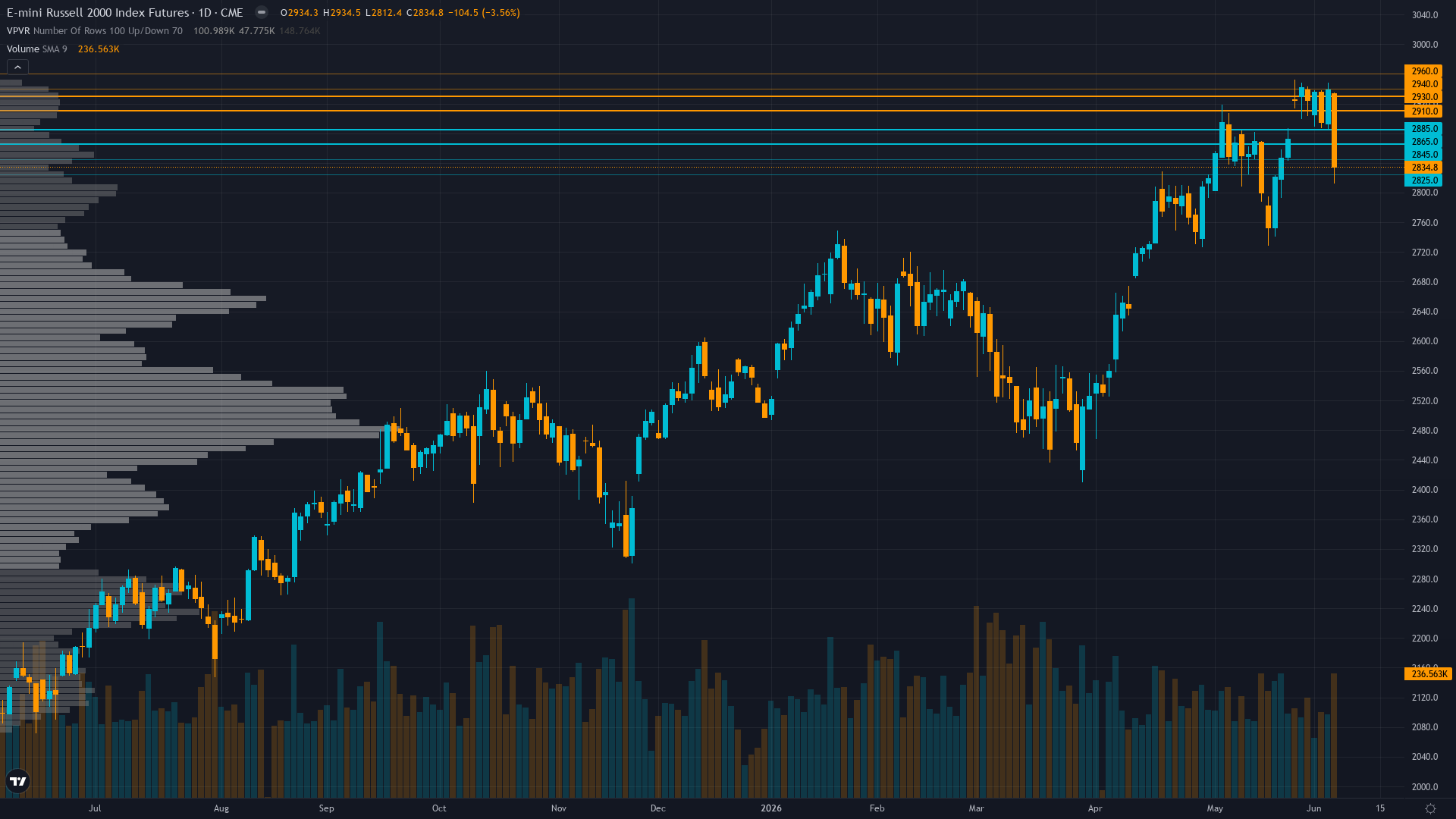

Russell 2000 sits at 2921.5 after slipping 0.15% — a shallow pullback rather than a decisive move. The market in Russell 2000 futures is coiling, with narrowing price ranges suggesting stored energy that will eventually release.

Small-caps consolidating near May 27 all-time high at 2,947 with market positioned for June 27 reconstitution flows to provide technical support, maintaining constructive longer-term view on 40%+ earnings growth trajectory while monitoring June FOMC for rate path clarity

Risk & Opportunity

Primary risk: Continuation of analytical framework failure evidenced by 5 consecutive missed calls totaling severe directional error, suggesting either market conditions unsuitable for small-cap directional calls or thesis methodology breakdown requiring extended recalibration period (Probability: high)

Primary opportunity: Reconstitution-driven flows into June 27 effective date create technical support if current 2900 level validates, targeting retest of 2935-2947 resistance zone as passive rebalancing overrides near-term fundamental concerns (Timeframe: 2-3 weeks through June 27 reconstitution effective date)

This week's edge: Resetting after 5 consecutive missed graded calls (well beyond 3-miss threshold) — analytical framework under mandatory review per Rule 5 regardless of current discipline signals or market setup

What's Driving Price

Primary driver: MANDATORY MISS RESET: Five consecutive MISSED graded calls (well beyond 3-miss threshold) triggers Rule 5 reset requiring NEUTRAL stance for at least one week to prevent thesis lock-in during extended losing streak

Secondary factor: Russell reconstitution approaching June 27 (20 days away) creates calendar-driven institutional flow catalyst worth estimated $200 billion in rebalancing, though current price action shows no directional conviction from this known event

Additional influence: VIX spike to 21.51 intraday June 5 combined with May retail sales collapse of -0.9% MoM signals transitional macro regime uncertainty, though VIX normalized back to 15.40 by June 7 removing immediate fear catalyst

Economic backdrop: Fed on hold at 4.25-4.50% with June 17-18 FOMC 10 days away, VIX normalized to 15.40 from June 5 spike to 21.51, May retail sales -0.9% creates transitional regime uncertainty between growth resilience and consumption weakness

Fundamental assessment: Q1 2026 earnings delivered 44.9% YoY growth validating inflection narrative, but elevated 25.39x forward P/E versus 13.62-17.34x historical range creates vulnerability to Q2 earnings delivery risk beginning mid-July

Chart Assessment

Price at 2921 consolidating 0.9% below May 27 ATH of 2947, RSI 33.73 oversold but no bullish divergence yet, trading range 2900-2935 reflects indecision

With trend strength at 4/10, the directional signal is present but far from decisive.

Volatility Context

At the 45th percentile, RTY futures volatility sits in a normal range, neither compressed enough to signal a breakout nor elevated enough to demand caution. Realised vol is holding its current level, suggesting the market has found a temporary equilibrium in its risk pricing.

Normal volatility regime at 45th percentile supports standard risk management with 2-3% stops below 2800 support, expect 30-50 point daily ranges versus 60-100 during elevated volatility periods, stable pattern suggests consolidation environment until June FOMC or reconstitution catalyst provides directional clarity

Seasonal Patterns

The seasonal picture for small-cap futures turns negative in June 2026 (42% win rate). Summer doldrums typically hit small-caps harder.

Looking Forward

All eyes turn to May 2026 CPI release scheduled June 11-12 window will test inflation trajectory following weak retail sales, critical for Fed policy expectations and small-cap rate sensitivity on Thursday 11 June, which carries enough weight to force a decisive directional move.

The week ahead for RTY futures hinges on whether the prevailing consolidating regime can absorb the scheduled catalysts without a regime shift.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime