Crude Oil Forecast This Week — Outlook, Drivers & Key Levels

This week's Crude Oil outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

Market Overview

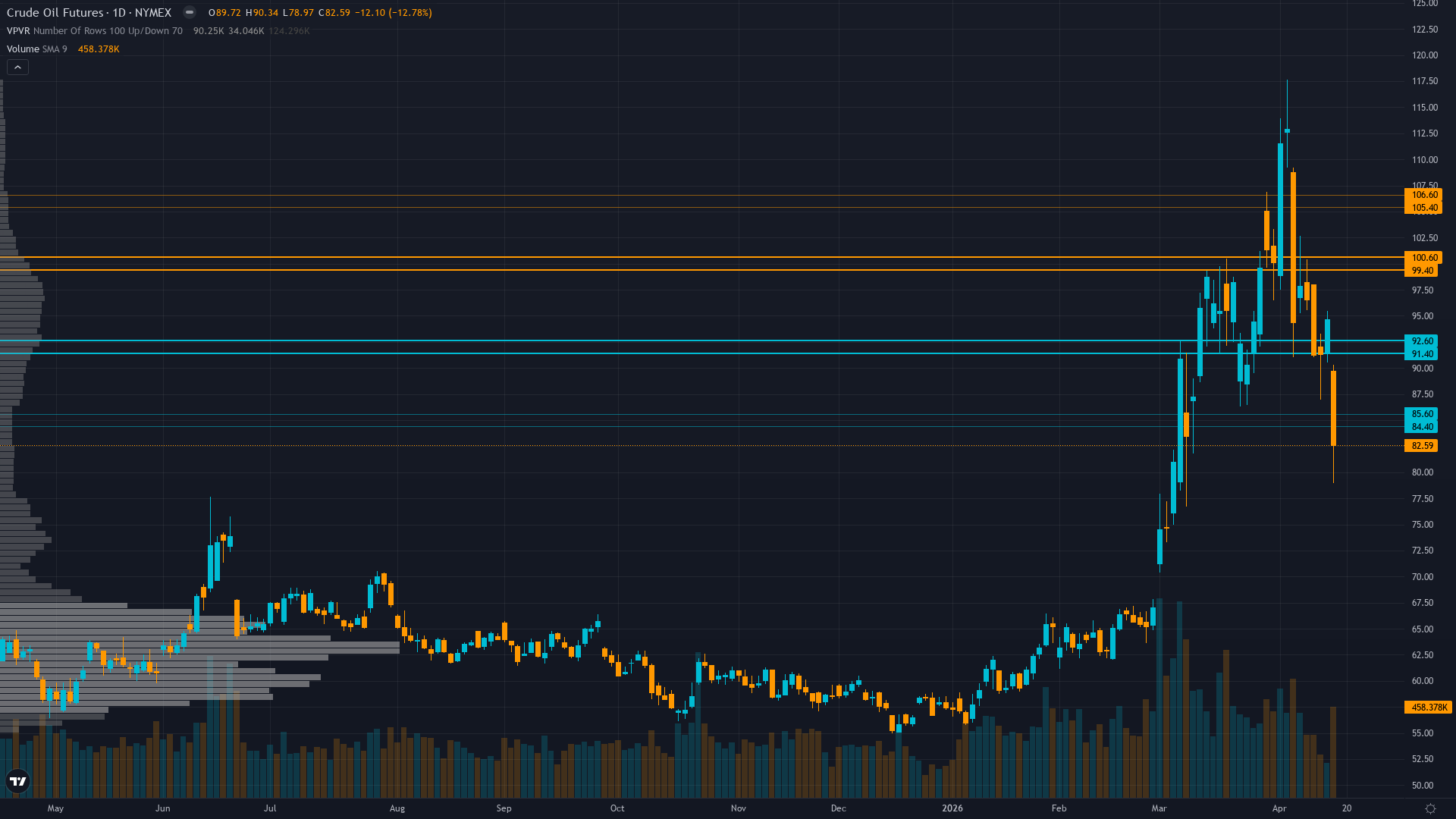

crude oil pushed to 84.36 on a 1.38% advance, reflecting sustained demand across the session. crude oil futures is in a breaking down market state, requiring careful assessment of current conditions.

Tactically bearish on ceasefire-driven geopolitical premium collapse but acknowledging fragility with April 22 expiration creating binary risk; structural oversupply forecasts (EIA $88/b Q4, Goldman $87 Q2, IEA 1.9 mb/d surplus) imply modest downside from current $84.36 once Hormuz fully normalizes, though some analysts cite IEA supply deficit creating fundamental floor

This Week's Catalysts & Drivers

Primary driver: Ceasefire extension developments creating regime uncertainty as Iran announces Strait of Hormuz 'completely open' during ceasefire remainder, accelerating geopolitical premium unwind from April 8-17 collapse that drove WTI from $112 to $84 (-25%) while IEA supply deficit projections collide with EIA fundamental bearish forecasts of Brent $88/b Q4 2026

Secondary factor: Technical breakdown confirmation with WTI at $84.36 lowest since March 2026, death cross complete (100 SMA below 200 SMA), breakdown below critical $88-92 support zone creating momentum acceleration toward $80 major support with RSI deteriorating and distribution volume patterns confirming bearish structure

Additional influence: Fundamental divergence intensifying as Strait reopening removes 20% supply disruption risk premium while structural bearish factors (IEA 1.9 mb/d surplus 2026, weak China demand, OPEC+ April production increase of 206k bpd) reassert dominance creating mean reversion setup toward EIA $88 Q4 forecast and Goldman Sachs $87 Q2 target

Economic backdrop: MACRO REGIME: TRANSITIONAL - VIX at 17.28 below 20 fear threshold indicating surprisingly calm broad market conditions despite crude's 25% collapse from $112 to $84, suggesting geopolitical risk contained to energy sector rather than systemic; Fed on hold at 3.50-3.75% with April 28-29 FOMC meeting 9 days forward expected to maintain for third consecutive meeting but energy inflation component critical given oil shock pass-through concerns

Fundamental assessment: Crude overvalued 5-10% versus fundamental fair value; IEA projects 1.5 mb/d supply deficit 2026 due to geopolitical disruption but EIA forecasts Brent declining to $88/b Q4 2026 (4% above current WTI equivalent) as Strait normalizes and structural oversupply reasserts with inventories already 4% below 5-year average creating tactical tightness insufficient to justify sustained premium

Technical Picture

Confirmed downtrend with death cross, price at $84.36 broke and holding below critical $88-92 support zone that launched prior rally, RSI deteriorating, 52-week high $117.63 now 39% overhead resistance, trading in lower third of range signaling distribution phase complete and breakdown acceleration phase beginning

At 3/10, trend strength is subdued, suggesting the market lacks a clear directional mandate.

Bull & Bear Case

Primary risk: Ceasefire collapses before or immediately after April 22 expiration with renewed U.S.-Israel strikes on Iran or complete Strait of Hormuz reclosure, forcing violent reversal back toward $100-110 range as 20% supply disruption risk premium reprices and invalidating mean reversion thesis based on diplomatic normalization trajectory (Probability: low)

Primary opportunity: Ceasefire extends to permanent agreement with full Strait of Hormuz normalization by April 22 expiration, triggering complete geopolitical premium unwind toward Goldman Sachs Q2 forecast $87 WTI and EIA Q4 projection $88 Brent-equivalent as structural oversupply fundamentals (IEA 1.9 mb/d surplus, weak China demand, OPEC+ production increase) overwhelm tactical support within 2-4 weeks (Timeframe: 2-4 weeks through late April into early May as April 22 ceasefire expiration provides binary clarity on diplomatic trajectory and Strait normalization completion)

This week's edge: Market may be underpricing probability of permanent ceasefire extension and complete Strait normalization by April 22, while overweighting IEA transient supply deficit versus EIA/Goldman structural oversupply forecasts; breakdown below $88-92 support with stubborn spec longs at 206.5K contracts creates asymmetric setup for continued downside toward $80-82 range if ceasefire holds, as technical structure confirms distribution phase complete and momentum favors further mean reversion toward fundamental fair value

Volatility Regime

Volatility for oil price sits at the 85th percentile over 90 days — an elevated regime that demands wider risk parameters and faster decision-making. The vol trend is flat, with no meaningful shift across timeframes. Stable vol environments often lull traders before a regime change arrives.

High but contracting vol requires moderately wide stops; expect 4-6% daily ranges currently versus 6-8% during peak conflict and 2-3% normal, as ceasefire stabilizes sentiment but April 22 expiration creates residual binary risk; intraday volatility elevated but declining suggesting coiled energy for directional resolution favoring downside continuation on ceasefire extension or violent reversal on collapse

What to Watch

The EIA Weekly Petroleum Status Report following Iran Strait of Hormuz reopening announcement and ceasefire extension developments, providing critical inventory data to validate whether supply normalization offsetting deficit projections or physical tightness persisting on Thursday 23 April stands as the week's primary risk event — high-impact and capable of overriding the existing technical and sentiment setup.

The interplay between breaking down market conditions and upcoming catalysts will define this week's trading landscape for WTI crude.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime