Crude Oil Forecast This Week — Outlook, Drivers & Key Levels

This week's Crude Oil outlook: key drivers, volatility context, risk-opportunity assessment and the week ahead.

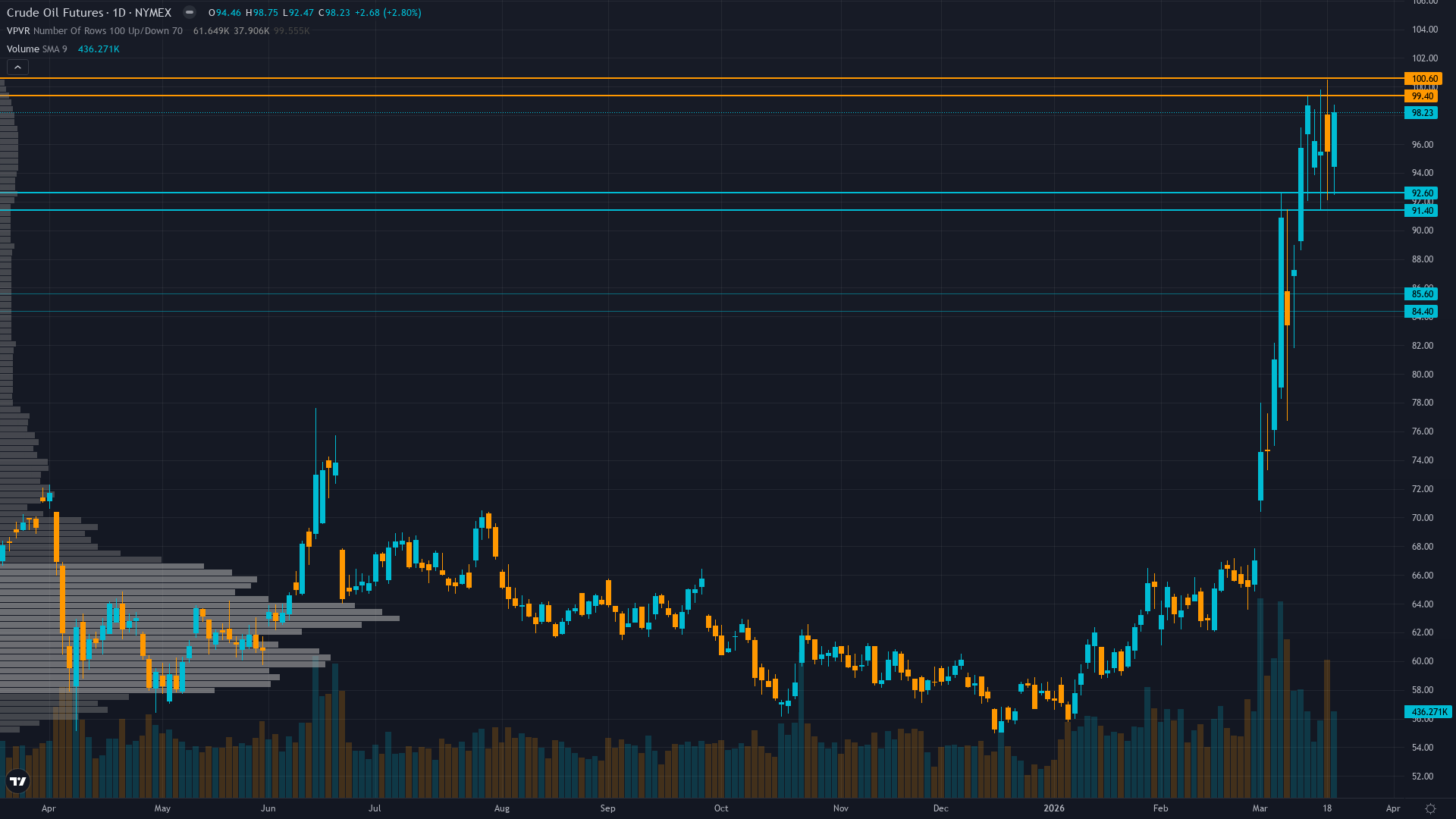

This Week's Starting Point

At 98.23, crude oil has eased 0.49% in a controlled retreat. crude oil futures is in a consolidating near resistance market state, requiring careful assessment of current conditions.

Tactically bullish short-term on geopolitical disruption sustaining but increasingly acknowledging Goldman Sachs Q4 forecast $71 Brent implies significant downside from current $98 WTI as structural oversupply fundamentals expected to reassert once Hormuz normalizes

Forces in Play

Primary driver: Geopolitical premium consolidation as Iran-U.S. Strait of Hormuz disruption enters week four with WTI consolidating $94-98 range below psychological $100 resistance, suggesting market adapting to sustained conflict as baseline rather than escalating war premium

Secondary factor: Structural oversupply fundamentals reasserting dominance with EIA projecting 1.9 mb/d global inventory builds 2026 once Hormuz normalizes, IEA cutting demand growth 210 kb/d to 640 kb/d, and OPEC+ March 1 modest 206k bpd production increase signaling cartel confidence in offsetting disruptions

Additional influence: Extreme speculative positioning at 351,032 net-long contracts (highest since 2020) creating asymmetric downside risk as producers aggressively hedge at $100+ levels signaling commercial forward bearish view contradicting crowd bullish extremes

Economic backdrop: MACRO REGIME: TRANSITIONAL - VIX at 26.78 (elevated above 25 threshold indicating risk-off conditions); Fed on hold at 3.5-3.75% with 1-cut forecast 2026; ISM Manufacturing 52.6 shows expansion but China GDP 4.5% reflects persistent demand weakness dampening global oil consumption outlook

Fundamental assessment: Crude overvalued 15-20% versus fair value $60-70 range; geopolitical premium unsustainable as IEA projects structural 1.9 mb/d surplus 2026 with demand revised down 210 kb/d offsetting temporary Strait of Hormuz supply disruption estimated at 8 mb/d curtailment

Technical Landscape

WTI consolidating $94-98 range after March 12 spike to $120, rejected sharply at $100 psychological resistance March 20 with bearish symmetrical triangle breakdown pattern forming; trading 18% below 52-week high $119.48 established during initial geopolitical shock

Trend strength registers at 6/10, suggesting meaningful but not extreme directional bias.

Risk-Reward Assessment

Primary risk: Iran-U.S. conflict escalates beyond current containment with sustained Strait of Hormuz closure disrupting 1-2+ mb/d flows for extended period, forcing Goldman Sachs bull-case $150/bbl scenario to materialize and invalidating structural oversupply mean reversion thesis (Probability: low)

Primary opportunity: Geopolitical premium fade accelerates within 2-3 weeks as historical pattern shows markets dismiss Middle East risks once initial shock absorbed, triggering mean reversion toward $70-75 range as extreme positioning unwinds, producer hedging validates commercial bearish view, and structural oversupply fundamentals overwhelm temporary supply disruption narrative (Timeframe: 2-4 weeks through late March into early April as conflict extends beyond month timeline typical for geopolitical premium persistence)

This week's edge: Market may be overextended on geopolitical premium at $98 WTI with extreme speculative positioning (351,032 net-long highest since 2020) creating asymmetric downside as producers aggressively hedge at $100+ signaling bearish forward view; consensus focused on supply disruption duration while underweighting U.S. policy response (sanctioned Iranian cargo releases plus SPR) and IEA demand downgrade of 210 kb/d creating mean reversion setup toward $70-75 range as historical pattern shows geopolitical premiums fade within 3-4 weeks maximum

Risk Environment

With vol at the 90th percentile, oil price is trading in an elevated regime where daily ranges can surprise even experienced traders. Volatility is stable, with realised vol holding steady across timeframes. This equilibrium can persist but eventually resolves into expansion or contraction.

Extreme and rapidly expanding vol requires very wide stops and defensive positioning; expect 5-8% daily ranges versus normal 2-3% as Iran war aftermath continues with Strait of Hormuz closure risk persisting into week four; intraday volatility creating severe whipsaw risk but consolidation below $100 resistance with distribution characteristics suggests mean reversion setup favoring downside resolution

Looking Forward

All eyes turn to EIA Weekly Petroleum Status Report following four-week geopolitical rally assessment and inventory trend validation of OPEC+ production discipline versus Hormuz disruption impact on Thursday 26 March, which carries enough weight to force a decisive directional move.

The week ahead for crude oil futures hinges on whether the prevailing consolidating near resistance regime can absorb the scheduled catalysts without a regime shift.

This analysis covers one dimension. Our full weekly report combines six specialist agents into a single actionable briefing with directional bias, key levels, and risk-opportunity matrix.

Start Free — Get the Market of the WeekFree weekly report · No credit card · Upgrade anytime