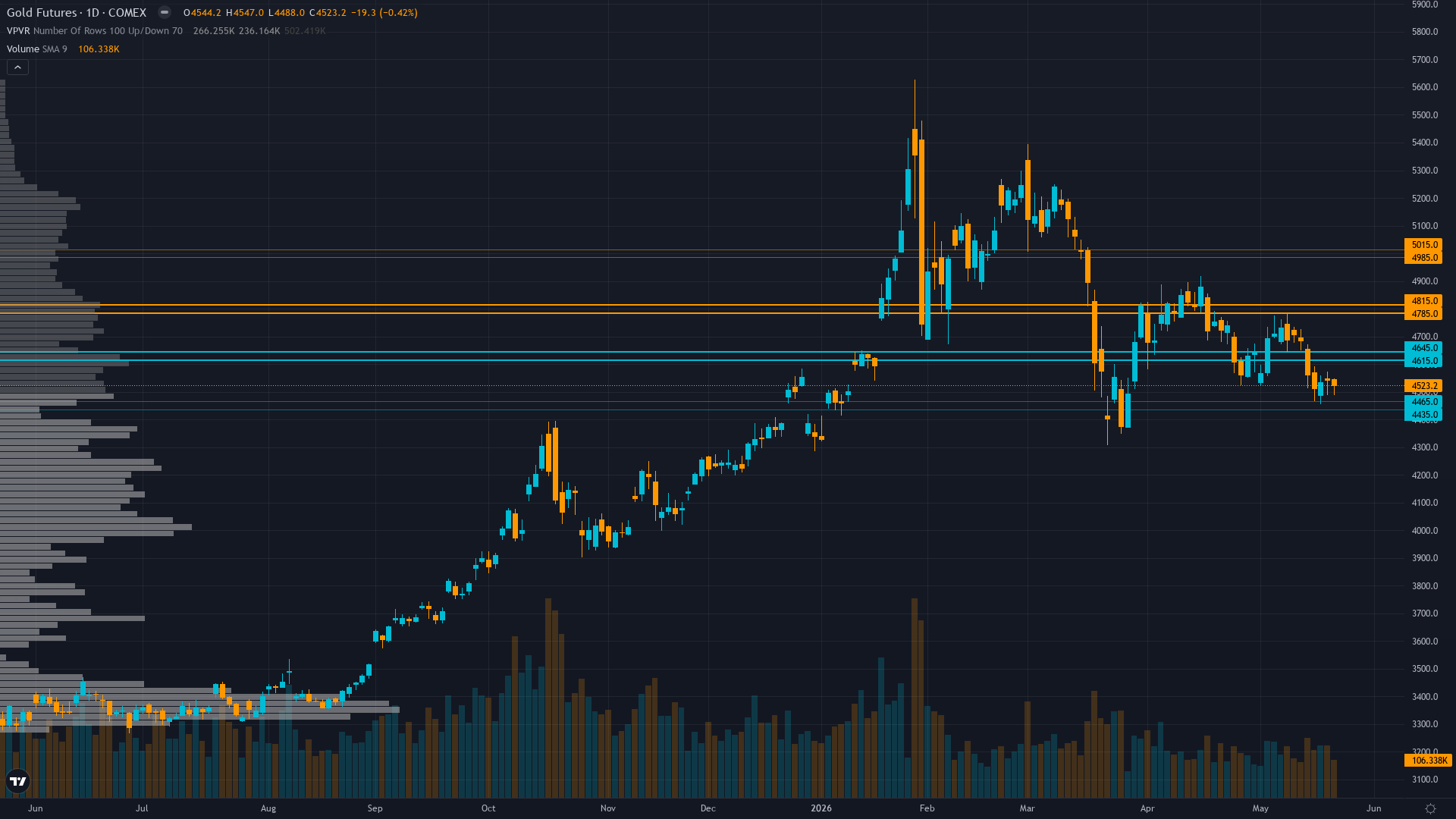

Gold (GC) — Mandatory thesis reset after 4 consecutive missed calls triggering Rule 5 Miss…

Mixed with institutional year-end targets remaining at $5,000-6,300 maintaining structural bull case but near-term uncertainty elevated following 16% correction and four consecutive weeks of failed directional calls creating tactical caution

Mixed with institutional year-end targets remaining at $5,000-6,300 maintaining structural bull case but near-term uncertainty elevated following 16% correction and four consecutive weeks of failed directional calls creating tactical caution

Mandatory thesis reset after 4 consecutive missed calls triggering Rule 5 Miss Reset protocol while gold consolidates at $4,730 following 16% correction from January $5,626 all-time high

Conflicting discipline signals create analytical uncertainty with Fundamental bullish on Q1 central bank demand 244t and valuation versus Technical/Institutional bearish on broken structure and record-low speculative positioning

Economic stalemate with Fed June 16-17 FOMC priced at 98% hold creating low-information-edge environment while elevated real yields at 4.56% (10Y nominal) maintain structural headwind offsetting central bank structural bid

| ▼ Resistance Zone 2 | 4975 – 5025 |

| ▼ Resistance Zone 1 | 4775 – 4825 |

| ─ Pivot Area | ~4730 |

| ▲ Support Zone 1 | 4657 – 4707 |

| ▲ Support Zone 2 | 4465 – 4515 |

Consolidating at $4,730 in corrective downtrend below 50-day MA $4,741 but above 200-day MA $4,357, RSI 34-46 neutral-to-oversold zone, testing immediate support $4,682 with major support $4,490

Fair value at $4,730 versus institutional targets $5,000-6,300, Q1 central bank demand 244t (+3% YoY) validates structural bid floor though elevated 10Y real yields 4.56% create cyclical headwind to non-yielding gold

Managed money net long at historically low 17k contracts as of May 11 creating contrarian positioning setup, but May ETF outflows of $1.8bn led by North America demonstrate Western institutional caution offsetting Q1 central bank demand stability at 244t

GVZ volatility at 26.34 showing elevated but moderating conditions from January 48.68 spike, insufficient current options flow data for clear directional bias as discipline provides no signal

Fed held rates steady at March 18 at 3.50-3.75%, next meeting June 16-17 priced 98% hold with no fresh catalyst this week, 10Y nominal yields 4.56% maintaining elevated real yield headwind for gold, DXY stable creating neutral dollar backdrop

Inverted - short-term 22.5% elevated above longer-term 21.5% indicating recent stress from March-April correction sequence moderating from 24.5% 20-day peak as market attempts stabilization

Post-major correction from $5,626 ATH volatility remains elevated 4-6 weeks then resolves directionally; 70% of similar $800+ correction episodes during Fed hawkish pivots consolidate at positioning extremes before mean reverting within 30 days

High volatility regime day 22 typically lasts 15-25 days for gold suggesting potential further normalization through late May with 65% probability of compression below 65th percentile by month-end as positioning extreme resolves

Elevated volatility at 72nd percentile requires wider stops with daily ranges potentially 2.0-3.0% versus normal 1.5-2.0%; current $4,600-4,900 consolidation zone suggests breakouts become more reliable once volatility normalizes below 65th percentile by late May

Current elevated volatility at $4,730 with GVZ 26.34 and historical vol at 72nd percentile creates roughly balanced risk-reward: 4-6% downside risk to $4,450-4,300 if breakdown resumes versus 3-5% upside to $4,900-5,000 resistance, but positioning flush and central bank demand stability add structural floor creating 1:1 risk-reward with June FOMC binary event risk

|

⚠️ Primary Risk

Continued dollar strength above DXY 100 combined with June FOMC reaffirming hawkish stance validates higher-for-longer trajectory driving gold toward $4,490-4,300 major support representing additional 4-7% downside from current levels Probability: MEDIUM

|

✦ Primary Opportunity

Fed introduces dovish optionality at June meeting suggesting eventual rate cut resumption triggers dollar reversal and speculative positioning unwind from record-low 17k contracts supporting gold rally toward $4,900-5,000 resistance within 3-4 weeks Timeframe: Next 3-4 weeks through June 16-17 FOMC and into early July as market digests whether May consolidation represents base-building for recovery or distribution before renewed decline

|

MACRO REGIME CLASSIFICATION: TRANSITIONAL with mixed signals. VIX at 17.44 (May 21 data) sits below the 20 threshold signaling normalized equity risk appetite, yet gold trades in post-correction consolidation mode at $4,730 following the historic 16% decline from January's $5,626 all-time high. This creates a regime where neither risk-on nor risk-off dominates, with gold trapped in holding pattern ahead of June 16-17 FOMC binary catalyst now 24 days away. Post-input development identified: No material market-moving news in past 48 hours.

Gold is consolidating in narrow $4,680-4,760 range as discipline agent inputs show. MANDATORY MISS RESET PROTOCOL ENGAGED: After 4 consecutive MISSED graded calls (May 22 NO CALL -4.68%, May 15 BULLISH -3.51%, May 8 BEARISH +1.51%, May 1 NO CALL -2.48%), Rule 5 requires issuing NEUTRAL for at least 1 week and conducting fundamental thesis review. The consecutive miss streak has reached the 4-miss threshold specified for GC in Section 2's asset classification table, triggering mandatory reset regardless of current discipline signals.

This is not analytical capitulation but framework-mandated recalibration. The discipline data presents deeply conflicting signals that contributed to the miss streak: Fundamental BULLISH (+2.5 confidence 7) on valuation 5-10% below institutional targets of $5,400-6,300 and Q1 central bank demand holding at 244t validating structural bid. Economic mildly BEARISH (-0.5 confidence 5) on elevated real yields 4.56% but no fresh deterioration. Institutional BEARISH (-1.5 confidence 6) on record-low managed money positioning 17k contracts and May ETF outflows $1.8bn.

Technical BEARISH (-1.5 confidence 5) on broken structure below 50-day MA with downtrend intact. Sentiment mildly BULLISH (+0.5 confidence 5) on contrarian setup. Options NO CALL (insufficient data). The most significant structural tension is between Fundamental agents seeing fair value and structural central bank support versus Institutional/Technical agents identifying positioning capitulation and broken price structure. Current consolidation at $4,730 sits in analytical no-man's land: 4.7% above major support at $4,490 (100-day MA zone) but 5.6% below major resistance at $5,000 psychological level.

The 2.41% Average Weekly Move suggests meaningful directional potential exists, well above the 0.30% Noise Floor, but forward conviction requires fresh catalysts not present this week. The June 16-17 FOMC meeting represents the next high-impact binary event, but attempting directional calls 24 days ahead into a low-information environment while on a 4-week miss streak violates risk management discipline. The path forward depends on whether May consolidation at $4,700-4,800 represents base-building (supporting eventual recovery toward $5,000+) or distribution (preceding breakdown toward $4,300-4,450).

Without fresh catalysts and with conflicting discipline signals, the appropriate stance is tactical pause rather than forced directional conviction. Conviction set at minimum threshold 5 reflecting genuine analytical uncertainty rather than thesis confidence, with signal at 0.0 per mandatory reset protocol. This week represents analytical recalibration, not market call.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 22, 2026 | NO CALL | 5/10 | ➖ |

| May 15, 2026 | BULLISH | 7/10 | ❌ |

| May 8, 2026 | BEARISH | 5/10 | ❌ |

| May 1, 2026 | NO CALL | 5/10 | ➖ |

| April 24, 2026 | BULLISH | 6/10 | ❌ |

| April 17, 2026 | NO CALL | 6/10 | ➖ |

| April 10, 2026 | BULLISH | 6/10 | ✅ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | BEARISH | 4/10 | ✅ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | BULLISH | 6/10 | ❌ |

| March 6, 2026 | BULLISH | 8/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════��═══════════════════════ Asset: Gold (GC) Report Date: May 24, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 15 (CONSENSUS ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: POST-CORRECTION CONSOLIDATION IN RANGE-BOUND HOLDING PATTERN AHEAD OF JUNE FOMC BINARY CATALYST Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Mixed with institutional year-end targets remaining at $5,000-6,300 maintaining structural bull case but near-term uncertainty elevated following 16% correction and four consecutive weeks of failed directional calls creating tactical caution ── WHAT THE MARKET IS MISSING ─────────────────── Resetting after 4 consecutive misses per Rule 5 — thesis under review. Market remains divided between structural bull case (central bank demand 244t, institutional targets $5K+) and cyclical headwinds (elevated real yields, ETF outflows). Desk lacks clear informational edge in current consolidation environment and requires June FOMC catalyst for directional clarity. ── KEY DRIVERS ────────────────────────────────── 1. Mandatory thesis reset after 4 consecutive missed calls triggering Rule 5 Miss Reset protocol while gold consolidates at $4,730 following 16% correction from January $5,626 all-time high 2. Conflicting discipline signals create analytical uncertainty with Fundamental bullish on Q1 central bank demand 244t and valuation versus Technical/Institutional bearish on broken structure and record-low speculative positioning 3. Economic stalemate with Fed June 16-17 FOMC priced at 98% hold creating low-information-edge environment while elevated real yields at 4.56% (10Y nominal) maintain structural headwind offsetting central bank structural bid ── KEY ZONES ──────────────────────────────────── Resistance 2: 4975 – 5025 Resistance 1: 4775 – 4825 Pivot: ~4730 Support 1: 4657 – 4707 Support 2: 4465 – 4515 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BULLISH Institutional: BEARISH Options: NO CALL Economic: BEARISH Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── Consolidating at $4,730 in corrective downtrend below 50-day MA $4,741 but above 200-day MA $4,357, RSI 34-46 neutral-to-oversold zone, testing immediate support $4,682 with major support $4,490 ── FUNDAMENTAL ASSESSMENT ─────────────────────── Fair value at $4,730 versus institutional targets $5,000-6,300, Q1 central bank demand 244t (+3% YoY) validates structural bid floor though elevated 10Y real yields 4.56% create cyclical headwind to non-yielding gold ── INSTITUTIONAL POSITIONING ──────────────────── Managed money net long at historically low 17k contracts as of May 11 creating contrarian positioning setup, but May ETF outflows of $1.8bn led by North America demonstrate Western institutional caution offsetting Q1 central bank demand stability at 244t ── OPTIONS FLOW ───────────────────────────────── GVZ volatility at 26.34 showing elevated but moderating conditions from January 48.68 spike, insufficient current options flow data for clear directional bias as discipline provides no signal ── ECONOMIC BACKDROP ──────────────────────────── Fed held rates steady at March 18 at 3.50-3.75%, next meeting June 16-17 priced 98% hold with no fresh catalyst this week, 10Y nominal yields 4.56% maintaining elevated real yield headwind for gold, DXY stable creating neutral dollar backdrop ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 72nd Trend: Contracting ▼ Days in Regime: 22 Term Structure: inverted - short-term 22.5% elevated above longer-term 21.5% indicating recent stress from March-April correction sequence moderating from 24.5% 20-day peak as market attempts stabilization Historical Pattern: Post-major correction from $5,626 ATH volatility remains elevated 4-6 weeks then resolves directionally; 70% of similar $800+ correction episodes during Fed hawkish pivots consolidate at positioning extremes before mean reverting within 30 days Outlook: High volatility regime day 22 typically lasts 15-25 days for gold suggesting potential further normalization through late May with 65% probability of compression below 65th percentile by month-end as positioning extreme resolves Trading Context: Elevated volatility at 72nd percentile requires wider stops with daily ranges potentially 2.0-3.0% versus normal 1.5-2.0%; current $4,600-4,900 consolidation zone suggests breakouts become more reliable once volatility normalizes below 65th percentile by late May Vol Risk/Opportunity: Current elevated volatility at $4,730 with GVZ 26.34 and historical vol at 72nd percentile creates roughly balanced risk-reward: 4-6% downside risk to $4,450-4,300 if breakdown resumes versus 3-5% upside to $4,900-5,000 resistance, but positioning flush and central bank demand stability add structural floor creating 1:1 risk-reward with June FOMC binary event risk ── PRIMARY RISK ───────────────────────────────── Continued dollar strength above DXY 100 combined with June FOMC reaffirming hawkish stance validates higher-for-longer trajectory driving gold toward $4,490-4,300 major support representing additional 4-7% downside from current levels Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Fed introduces dovish optionality at June meeting suggesting eventual rate cut resumption triggers dollar reversal and speculative positioning unwind from record-low 17k contracts supporting gold rally toward $4,900-5,000 resistance within 3-4 weeks Timeframe: Next 3-4 weeks through June 16-17 FOMC and into early July as market digests whether May consolidation represents base-building for recovery or distribution before renewed decline ── NEXT CATALYST ──────────────────────────────── Date: June 17, 2026 Event: Federal Reserve FOMC Meeting decision June 16-17 representing next major catalyst with market pricing 98% probability of hold, forward guidance critical for assessing rate cut timeline and real yield trajectory Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── MACRO REGIME CLASSIFICATION: TRANSITIONAL with mixed signals. VIX at 17.44 (May 21 data) sits below the 20 threshold signaling normalized equity risk appetite, yet gold trades in post-correction consolidation mode at $4,730 following the historic 16% decline from January's $5,626 all-time high. This creates a regime where neither risk-on nor risk-off dominates, with gold trapped in holding pattern ahead of June 16-17 FOMC binary catalyst now 24 days away. Post-input development identified: No material market-moving news in past 48 hours. Gold is consolidating in narrow $4,680-4,760 range as discipline agent inputs show. MANDATORY MISS RESET PROTOCOL ENGAGED: After 4 consecutive MISSED graded calls (May 22 NO CALL -4.68%, May 15 BULLISH -3.51%, May 8 BEARISH +1.51%, May 1 NO CALL -2.48%), Rule 5 requires issuing NEUTRAL for at least 1 week and conducting fundamental thesis review. The consecutive miss streak has reached the 4-miss threshold specified for GC in Section 2's asset classification table, triggering mandatory reset regardless of current discipline signals. This is not analytical capitulation but framework-mandated recalibration. The discipline data presents deeply conflicting signals that contributed to the miss streak: Fundamental BULLISH (+2.5 confidence 7) on valuation 5-10% below institutional targets of $5,400-6,300 and Q1 central bank demand holding at 244t validating structural bid. Economic mildly BEARISH (-0.5 confidence 5) on elevated real yields 4.56% but no fresh deterioration. Institutional BEARISH (-1.5 confidence 6) on record-low managed money positioning 17k contracts and May ETF outflows $1.8bn. Technical BEARISH (-1.5 confidence 5) on broken structure below 50-day MA with downtrend intact. Sentiment mildly BULLISH (+0.5 confidence 5) on contrarian setup. Options NO CALL (insufficient data). The most significant structural tension is between Fundamental agents seeing fair value and structural central bank support versus Institutional/Technical agents identifying positioning capitulation and broken price structure. Current consolidation at $4,730 sits in analytical no-man's land: 4.7% above major support at $4,490 (100-day MA zone) but 5.6% below major resistance at $5,000 psychological level. The 2.41% Average Weekly Move suggests meaningful directional potential exists, well above the 0.30% Noise Floor, but forward conviction requires fresh catalysts not present this week. The June 16-17 FOMC meeting represents the next high-impact binary event, but attempting directional calls 24 days ahead into a low-information environment while on a 4-week miss streak violates risk management discipline. The path forward depends on whether May consolidation at $4,700-4,800 represents base-building (supporting eventual recovery toward $5,000+) or distribution (preceding breakdown toward $4,300-4,450). Without fresh catalysts and with conflicting discipline signals, the appropriate stance is tactical pause rather than forced directional conviction. Conviction set at minimum threshold 5 reflecting genuine analytical uncertainty rather than thesis confidence, with signal at 0.0 per mandatory reset protocol. This week represents analytical recalibration, not market call.