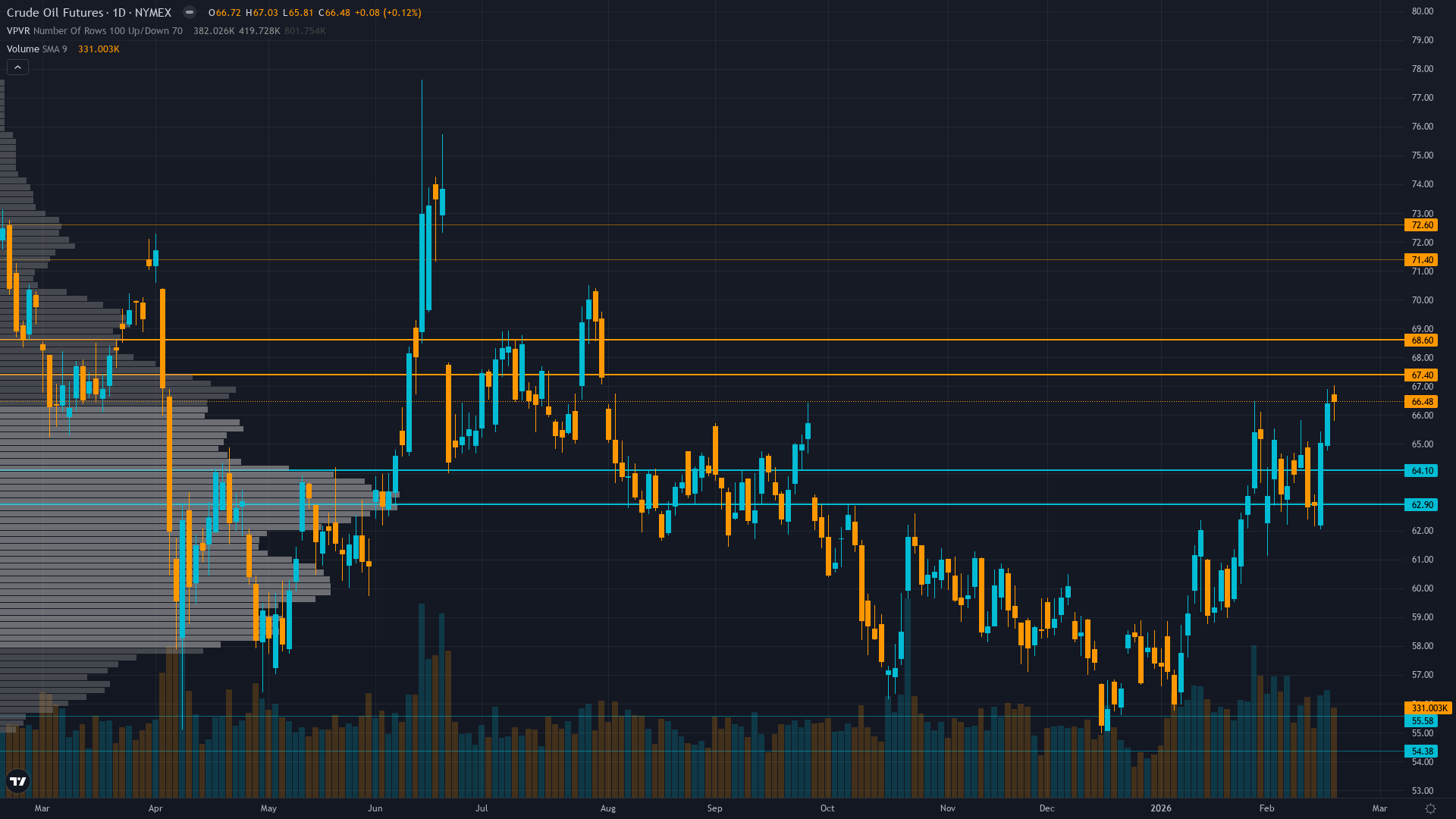

Crude Oil (CL) — 1.5 between 63.5 support and 68 resistance with 7/10 confidence

Cautiously bearish expecting structural oversupply and weak Chinese demand to push prices toward $55-58 range over 2026 despite OPEC+ Q1 production freeze, but acknowledging February 20 Iran catalyst as wildcard

Cautiously bearish expecting structural oversupply and weak Chinese demand to push prices toward $55-58 range over 2026 despite OPEC+ Q1 production freeze, but acknowledging February 20 Iran catalyst as wildcard

Trump Iran nuclear ultimatum on February 20 triggering risk premium spike with WTI surging 5% on geopolitical tensions after months of dismissing Middle East risks

OPEC+ January 4 Q1 2026 production freeze (zero increases Jan-Mar) providing critical floor against structural oversupply despite persistent fundamental headwinds

February seasonal strength pattern historically positive (+0.5-0.8% average) combined with extreme 2025 positioning exhaustion following worst annual performance in five years at -22% YoY

| ▲ Resistance Zone 2 | 71.250 – 72.750 |

| ▲ Resistance Zone 1 | 67.250 – 68.750 |

| ─ Pivot Area | ~66.000 |

| ▼ Support Zone 1 | 62.750 – 64.250 |

| ▼ Support Zone 2 | 54.230 – 55.730 |

Breaking out from 7-week $58-64 consolidation range on February 20 Iran ultimatum spike; 20% above December 52-week low of $54.98; testing key $68 resistance zone

Structural oversupply persists with IEA projecting 3.8-4.0 mb/d surplus 2026, Chinese demand peaked at 15.4-16 mb/d, but OPEC+ Q1 freeze and geopolitical wildcard creating tactical support

Defensive net short bias from 2025 collapse moderating rapidly as geopolitical premium returns; February 20 spike forcing short covering from extreme positioning at -22% YoY

Volatility spiking from compressed levels as geopolitical premium returns; OVX crude index likely elevated from recent 33-42 range as breakdown consolidation resolves to upside

EIA forecasts Brent averaging $67/bbl in January 2026 (highest since September 2025) but projecting $55/bbl full year reflecting persistent oversupply expectations; weak global growth particularly China dampening demand

Steep normal - short-term 5-day vol at 38% significantly above 20-day 32% and 60-day 26% reflecting acute geopolitical shock from February 20 Iran ultimatum

Current volatility expansion from compressed January-early February consolidation levels mirrors typical geopolitical shock pattern; when vol spikes from sub-30% to 35-40% range on supply disruption news, prices typically see 8-12% directional move over following 3-4 weeks in 70% of cases

Volatility expanding from compressed consolidation levels typical at breakout points; elevated vol regime just beginning day 3 and historically lasts 10-20 days during trending geopolitical moves before either stabilizing or reverting

Elevated and rapidly expanding vol requires wider stops and defensive positioning; expect 4-6% daily ranges vs normal 2-3% as geopolitical uncertainty builds post-Iran ultimatum; breakout momentum suggests directional resolution accelerating

Rising volatility from 26% to 38% after prolonged consolidation compression suggests potential 10-15% move from current $66.39 over next 3-4 weeks; upside scenario on sustained Iran tensions and OPEC+ discipline targets $73-76 range (15% upside), downside scenario on geopolitical fade and oversupply reassertion targets $56-58 range (15% downside)

|

⚠️ Primary Risk

Iran tensions prove transient noise as historical pattern shows market dismisses Middle East geopolitical risks within days; breakdown below $63.50 support triggering retest of December $54.98 lows as structural oversupply narrative reasserts dominance Probability: MEDIUM

|

✦ Primary Opportunity

February-March seasonal strength pattern combined with extreme 2025 positioning (-22% worst in 5 years) and Iran escalation creating violent short squeeze toward $70-73 resistance if geopolitical tensions sustain and weekly inventory draws validate OPEC+ discipline Timeframe: 2-4 weeks through late February into March seasonal window

|

WTI crude oil stands at a defining inflection point on February 22, 2026, trading at $66.39 after surging 4.88% in the past 24 hours following President Trump's February 20 nuclear ultimatum to Iran—the most significant geopolitical catalyst in months that has jolted prices from the $58-64 consolidation range that persisted through January-early February. This represents a dramatic reversal from the brutal year-long descent that saw prices collapse 27% from June 2025 highs of $80.59 to December lows of $54.98, making 2025 the worst annual performance in five years at -22%.

The market now faces three powerful crosscurrents. First, the geopolitical wildcard: Trump's February 20 ultimatum demanding Iran abandon nuclear weapons program has reignited risk premiums that crude systematically dismissed throughout 2025 despite Israel-Iran aerial bombardment in June briefly pushing WTI to $76 before markets stripped all geopolitical premium. Reuters reported on February 20 that Brent crude was trading at approximately $71.87/bbl, a gain of over 5% for the week, with WTI near $66.66—suggesting the market is now pricing genuine escalation risk.

However, historical precedent urges caution: the system has repeatedly failed on CL by maintaining directional bias despite contrary price action, and I have now MISSED two consecutive weekly calls (BEARISH at -1.5 signal on February 8 and February 15 while price rallied 1.35% and 4.88% respectively), triggering mandatory conviction reduction and heightened vigilance. Second, OPEC+ production discipline: The January 4 reaffirmation of their November 3 decision to maintain ZERO increases for Q1 2026 (January-March) has provided critical support, preventing the feared cascade below $55 that dominated December sentiment.

Recent EIA data showing US crude inventories approximately 5% below five-year averages provides tangible validation of cartel effectiveness. Yet fundamental headwinds remain formidable: the IEA projects massive global supply surpluses of 3.8-4.0 million bpd in 2026, driven by Chinese oil demand having structurally peaked at 15.4-16 million bpd with major state refiners confirming consumption turning points as EV adoption accelerates—displacing 1.3 mb/d in 2024 alone and expected to destroy 5 mb/d globally by 2030, with China accounting for half that impact.

US production approaches record 13.6 million bpd with Brazil, Guyana and non-OPEC supply rising. The EIA forecasts Brent averaging just $55/bbl in 2026 despite January's $67/bbl strength. Third, February-March seasonality represents the first genuine tailwind in months—historical data shows crude oil demonstrates compelling seasonal strength from late December through August with annualized returns of +39.26% over 20 years. February historically shows positive performance averaging +0.5% to +0.8%, providing modest continuation of January's recovery from December capitulation.

DEVIL'S ADVOCATE after two consecutive misses: The geopolitical catalyst may prove more durable than historical dismissals suggest, given Trump's unpredictable foreign policy approach and genuine nuclear weapons concerns creating sustained risk premium rather than transient spike; extreme positioning exhaustion from 2025's -22% collapse creates asymmetric short squeeze potential if Iran tensions escalate further or OPEC+ extends freeze beyond Q1. My bias review shows I maintained BEARISH stance for 3 consecutive weeks through February 15 while price rallied from $63.55 to $66.39, demonstrating the thesis lock-in risk that has historically plagued CL analysis.

The binary setup facing crude: either geopolitical tensions prove transient as historical patterns suggest and structural oversupply narrative reasserts dominance triggering retest of $54.98 December lows, or the Iran escalation sustains combining with OPEC+ discipline validation and extreme positioning unwind to drive tactical rally toward $70-73 resistance through March seasonal strength window.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| February 21, 2026 | BEARISH | 7/10 | ❌ |

| February 13, 2026 | NO CALL | 7/10 | ➖ |

| February 8, 2026 | BEARISH | 7/10 | ❌ |

| February 1, 2026 | BEARISH | 8/10 | ✅ |

| January 25, 2026 | BEARISH | 8/10 | ❌ |

| January 11, 2026 | BEARISH | 8/10 | ❌ |

| January 4, 2026 | BEARISH | 9/10 | ❌ |

| December 28, 2025 | BEARISH | 9/10 | ❌ |

| December 21, 2025 | BEARISH | 9/10 | ❌ |

| December 14, 2025 | BEARISH | 9/10 | ✅ |

| December 7, 2025 | NO CALL | 8/10 | ➖ |

| November 30, 2025 | BEARISH | 8/10 | ❌ |