USD/JPY (6J) — Policy stalemate ahead of March 18 FOMC with Fed-BoJ differential unchanged at…

USD/JPY consolidation with slight bearish yen bias on persistent rate differentials; market expecting range-bound behavior ahead of FOMC

USD/JPY consolidation with slight bearish yen bias on persistent rate differentials; market expecting range-bound behavior ahead of FOMC

Policy stalemate ahead of March 18 FOMC with Fed-BoJ differential unchanged at 275-300bp and no fresh catalyst this week

Intervention threshold raised to above 160 per Reuters March 13 as Middle East conflict adds geopolitical pressure on yen

Japanese fiscal year-end repatriation flows in final 16 days create seasonal yen support counterbalancing rate differential headwinds

| ▼ Resistance Zone 2 | 0.0046 – 0.0086 |

| ▼ Resistance Zone 1 | 0.0045 – 0.0085 |

| ─ Pivot Area | ~0.0063 |

| ▲ Support Zone 1 | 0.0042 – 0.0082 |

| ▲ Support Zone 2 | 0.0043 – 0.0083 |

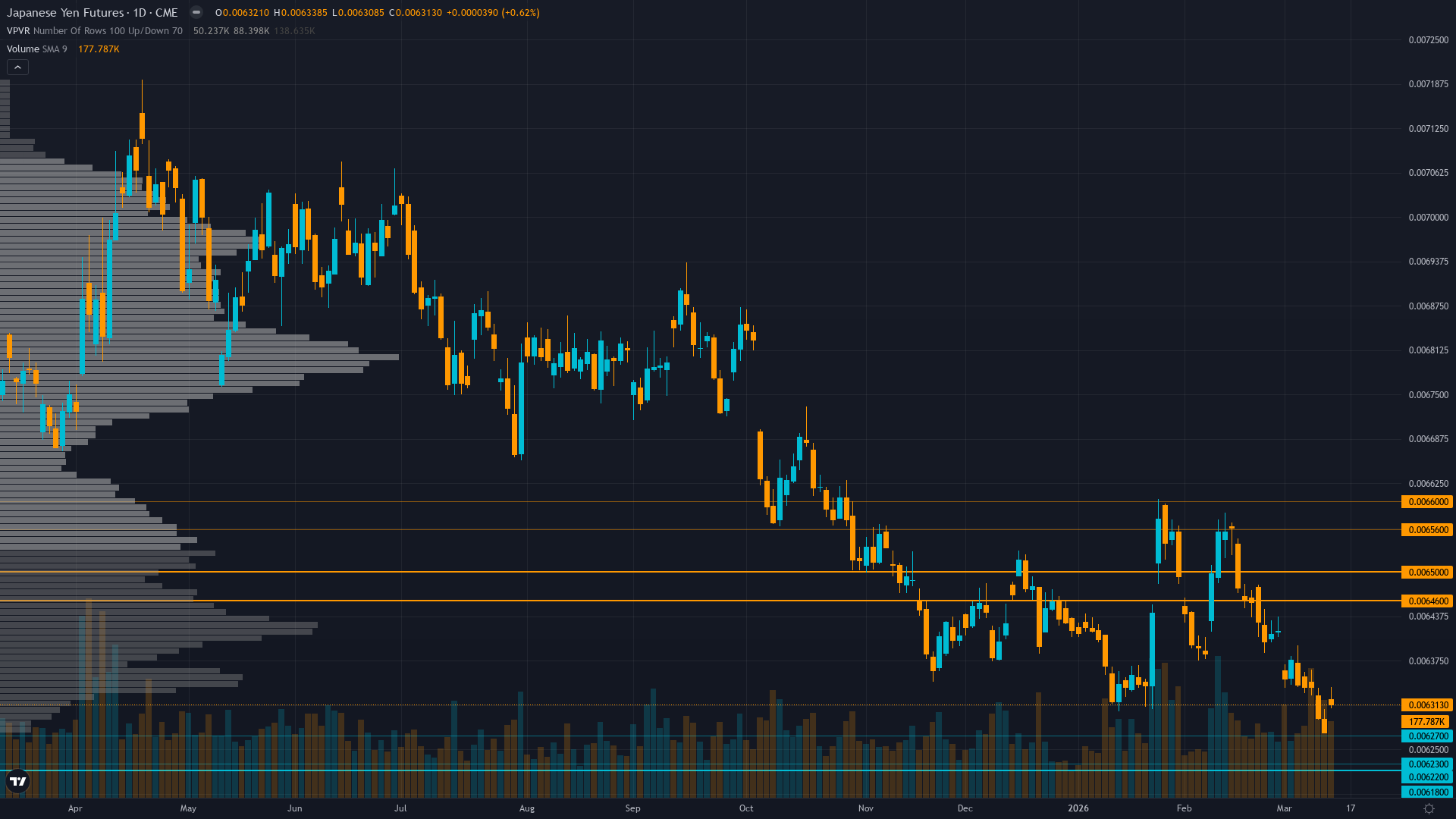

Downtrend confirmed below 50-day and 200-day MAs, consolidating 0.00620-0.00640 range with weakening momentum

Yen modestly undervalued by PPP but rate differential at 275-300bp provides structural USD support; no fresh fundamental catalyst this week

Modest net short at -19,106 contracts per March 10 COT - neutral positioning with no extreme readings creating low contrarian signal

Implied volatility compressed at 10% reflecting complacency and low event risk pricing ahead of FOMC catalyst

Fed on hold at 3.5-3.75% with 94% probability of March 18 hold; BoJ at 0.75% with next meeting not until April; no data surprises this week

Normal - short-term 9.8% below medium 10.2% and long 11.8% reflecting post-event compression with residual uncertainty ahead of March 18 FOMC

Similar pre-FOMC consolidations see volatility compress to 60th-65th percentile range then spike to 85th+ percentile within 24 hours of decision; current 68th percentile consistent with 3-day-out positioning

Volatility likely to continue contracting 1-3 days then re-expand sharply into March 18 FOMC; typical pattern shows 15-20% compression pre-event followed by 30-50% spike on decision day

High volatility regime suggests 80-100 pip daily ranges (0.00050-0.00065 in 6J terms) versus normal 50-60 pips; FOMC March 18 likely triggers 150-250 pip move in 24-48 hours; current consolidation breakouts unreliable without catalyst confirmation

Elevated 68th percentile volatility indicates 1.2-1.5% daily move potential versus normal 0.6-0.8%; March 18 FOMC creates binary event premium with potential 200-300 pip move (2+ standard deviations) on surprise dovish or hawkish shift representing asymmetric reward for post-catalyst positioning

|

⚠️ Primary Risk

Middle East geopolitical escalation forcing sharp yen safe-haven rally overriding rate differential dynamics Probability: MEDIUM

|

✦ Primary Opportunity

Mean reversion rally toward 0.0065-0.0068 range (154-147 USD/JPY) if FOMC signals dovish shift or fiscal year-end repatriation accelerates Timeframe: 3-10 days through FOMC decision and March 31 fiscal year-end

|

The Japanese Yen futures sit in an uncomfortable equilibrium on March 15, 2026, trading at 0.006291 (USD/JPY 159.0) as multiple conflicting forces create paralysis three days before the FOMC decision. The macro regime is TRANSITIONAL - neither clear risk-on nor risk-off, with VIX data unavailable but equity markets showing mixed performance and the yen trapped between structural bearish drivers and emerging tactical support factors. Post-input development identified: Reuters reported March 13 that Japan's intervention bar is now HIGHER than historical precedent despite USD/JPY approaching the 160 trigger zone, with Middle East conflict cited as current pressure on the yen.

This materially changes the intervention risk calculus - while proximity to 160 historically meant imminent action, authorities now have reduced scope or willingness to intervene. The fundamental picture remains dominated by the 275-300bp Fed-BoJ rate differential (Fed 3.5-3.75% vs BoJ 0.75%), a structural headwind that all six discipline agents acknowledge but with no change from prior weeks. The most recent discipline data shows complete policy stalemate: Economic agent reports no material changes this week, Fundamental agent notes no new catalyst, Institutional agent confirms modest net short positioning at -19,106 contracts (far from extremes), Technical agent identifies consolidation with weakening momentum, Options agent finds compressed 10% implied volatility reflecting complacency, and Sentiment agent notes elevated VIX creating fear regime but bearish Yen consensus without extremes.

The critical insight is that we are in a classic low-information-edge environment: no discipline agent has provided fresh data from THIS WEEK, all themes are carryovers from prior analysis, and the market is simply waiting for the March 18 FOMC catalyst. The only new elements are: (1) we are now in the final 16 days before Japan's March 31 fiscal year-end when repatriation flows historically provide temporary yen support, and (2) the Reuters intervention threshold report suggests authorities are constrained despite proximity to historical trigger levels.

With my last three graded calls being CORRECT (all NO CALLs), I have zero consecutive misses and zero bias streak concerns. However, the expected 0.66% weekly move for 6J is only marginally above the 0.50% noise floor, and crucially there is NO CATALYST between now and Friday's close before the March 18 FOMC (which occurs after this week's grading period). The technical structure shows a downtrend below key moving averages, but momentum is stuck and the 20-pip consolidation range suggests market indecision rather than directional conviction.

Volatility at the 68th percentile is elevated versus norms but compressed from prior event peaks, pricing minimal near-term movement. The discipline synthesis yields conflicting leans: Economic and Fundamental agents are mildly bearish on yen (supporting USD strength), Institutional is mildly bullish on yen (contrarian to modest shorts), and Technical/Options/Sentiment provide no directional conviction. When synthesis history, current data, and forward catalysts are integrated, the conclusion is unambiguous: this is a range-bound, catalyst-dependent setup where calling direction before the FOMC would be noise-calling rather than signal identification.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | NO CALL | 5/10 | ➖ |

| February 27, 2026 | NO CALL | 5/10 | ➖ |

| February 21, 2026 | BULLISH | 6/10 | ❌ |

| February 13, 2026 | BULLISH | 6/10 | ❌ |

| February 8, 2026 | BULLISH | 7/10 | ❌ |

| February 1, 2026 | NO CALL | 7/10 | ➖ |

| January 25, 2026 | BULLISH | 7/10 | ❌ |

| January 11, 2026 | BULLISH | 7/10 | ❌ |

| January 4, 2026 | BEARISH | 6/10 | ✅ |

| December 28, 2025 | BEARISH | 6/10 | ✅ |

| December 21, 2025 | BULLISH | 7/10 | ✅ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: USD/JPY (6J) Report Date: March 15, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 18 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── USD/JPY consolidation with slight bearish yen bias on persistent rate differentials; market expecting range-bound behavior ahead of FOMC ── WHAT THE MARKET IS MISSING ─────────────────── Market underpricing fiscal year-end repatriation flows (16 days remaining) and overestimating intervention deterrent given Reuters report of raised threshold; however NO CALL issued as expected sub-0.70% weekly move below conviction threshold and no catalyst before Friday close - low information edge environment ── KEY DRIVERS ────────────────────────────────── 1. Policy stalemate ahead of March 18 FOMC with Fed-BoJ differential unchanged at 275-300bp and no fresh catalyst this week 2. Intervention threshold raised to above 160 per Reuters March 13 as Middle East conflict adds geopolitical pressure on yen 3. Japanese fiscal year-end repatriation flows in final 16 days create seasonal yen support counterbalancing rate differential headwinds ── KEY ZONES ──────────────────────────────────── Resistance 2: 0.0046 – 0.0086 Resistance 1: 0.0045 – 0.0085 Pivot: ~0.0063 Support 1: 0.0042 – 0.0082 Support 2: 0.0043 – 0.0083 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BEARISH Institutional: BULLISH Options: NO CALL Economic: BEARISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Downtrend confirmed below 50-day and 200-day MAs, consolidating 0.00620-0.00640 range with weakening momentum ── FUNDAMENTAL ASSESSMENT ─────────────────────── Yen modestly undervalued by PPP but rate differential at 275-300bp provides structural USD support; no fresh fundamental catalyst this week ── INSTITUTIONAL POSITIONING ──────────────────── Modest net short at -19,106 contracts per March 10 COT - neutral positioning with no extreme readings creating low contrarian signal ── OPTIONS FLOW ───────────────────────────────── Implied volatility compressed at 10% reflecting complacency and low event risk pricing ahead of FOMC catalyst ── ECONOMIC BACKDROP ──────────────────────────── Fed on hold at 3.5-3.75% with 94% probability of March 18 hold; BoJ at 0.75% with next meeting not until April; no data surprises this week ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 68th Trend: Contracting ▼ Days in Regime: 7 Term Structure: Normal - short-term 9.8% below medium 10.2% and long 11.8% reflecting post-event compression with residual uncertainty ahead of March 18 FOMC Historical Pattern: Similar pre-FOMC consolidations see volatility compress to 60th-65th percentile range then spike to 85th+ percentile within 24 hours of decision; current 68th percentile consistent with 3-day-out positioning Outlook: Volatility likely to continue contracting 1-3 days then re-expand sharply into March 18 FOMC; typical pattern shows 15-20% compression pre-event followed by 30-50% spike on decision day Trading Context: High volatility regime suggests 80-100 pip daily ranges (0.00050-0.00065 in 6J terms) versus normal 50-60 pips; FOMC March 18 likely triggers 150-250 pip move in 24-48 hours; current consolidation breakouts unreliable without catalyst confirmation Vol Risk/Opportunity: Elevated 68th percentile volatility indicates 1.2-1.5% daily move potential versus normal 0.6-0.8%; March 18 FOMC creates binary event premium with potential 200-300 pip move (2+ standard deviations) on surprise dovish or hawkish shift representing asymmetric reward for post-catalyst positioning ── PRIMARY RISK ───────────────────────────────── Middle East geopolitical escalation forcing sharp yen safe-haven rally overriding rate differential dynamics Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Mean reversion rally toward 0.0065-0.0068 range (154-147 USD/JPY) if FOMC signals dovish shift or fiscal year-end repatriation accelerates Timeframe: 3-10 days through FOMC decision and March 31 fiscal year-end ── NEXT CATALYST ──────────────────────────────── Date: March 18, 2026 Event: FOMC policy decision with dot plot and Powell press conference - market pricing 94.1% probability of hold but 45.8% probability of cut by May Expected Impact: MEDIUM ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── The Japanese Yen futures sit in an uncomfortable equilibrium on March 15, 2026, trading at 0.006291 (USD/JPY 159.0) as multiple conflicting forces create paralysis three days before the FOMC decision. The macro regime is TRANSITIONAL - neither clear risk-on nor risk-off, with VIX data unavailable but equity markets showing mixed performance and the yen trapped between structural bearish drivers and emerging tactical support factors. Post-input development identified: Reuters reported March 13 that Japan's intervention bar is now HIGHER than historical precedent despite USD/JPY approaching the 160 trigger zone, with Middle East conflict cited as current pressure on the yen. This materially changes the intervention risk calculus - while proximity to 160 historically meant imminent action, authorities now have reduced scope or willingness to intervene. The fundamental picture remains dominated by the 275-300bp Fed-BoJ rate differential (Fed 3.5-3.75% vs BoJ 0.75%), a structural headwind that all six discipline agents acknowledge but with no change from prior weeks. The most recent discipline data shows complete policy stalemate: Economic agent reports no material changes this week, Fundamental agent notes no new catalyst, Institutional agent confirms modest net short positioning at -19,106 contracts (far from extremes), Technical agent identifies consolidation with weakening momentum, Options agent finds compressed 10% implied volatility reflecting complacency, and Sentiment agent notes elevated VIX creating fear regime but bearish Yen consensus without extremes. The critical insight is that we are in a classic low-information-edge environment: no discipline agent has provided fresh data from THIS WEEK, all themes are carryovers from prior analysis, and the market is simply waiting for the March 18 FOMC catalyst. The only new elements are: (1) we are now in the final 16 days before Japan's March 31 fiscal year-end when repatriation flows historically provide temporary yen support, and (2) the Reuters intervention threshold report suggests authorities are constrained despite proximity to historical trigger levels. With my last three graded calls being CORRECT (all NO CALLs), I have zero consecutive misses and zero bias streak concerns. However, the expected 0.66% weekly move for 6J is only marginally above the 0.50% noise floor, and crucially there is NO CATALYST between now and Friday's close before the March 18 FOMC (which occurs after this week's grading period). The technical structure shows a downtrend below key moving averages, but momentum is stuck and the 20-pip consolidation range suggests market indecision rather than directional conviction. Volatility at the 68th percentile is elevated versus norms but compressed from prior event peaks, pricing minimal near-term movement. The discipline synthesis yields conflicting leans: Economic and Fundamental agents are mildly bearish on yen (supporting USD strength), Institutional is mildly bullish on yen (contrarian to modest shorts), and Technical/Options/Sentiment provide no directional conviction. When synthesis history, current data, and forward catalysts are integrated, the conclusion is unambiguous: this is a range-bound, catalyst-dependent setup where calling direction before the FOMC would be noise-calling rather than signal identification.