USD/JPY (6J) — Market significantly underpricing political constraint on BOJ from Takaichi…

USD/JPY consolidation with slight bearish JPY bias on persistent rate differentials; Takaichi election victory seen constraining BOJ normalization through political pressure

USD/JPY consolidation with slight bearish JPY bias on persistent rate differentials; Takaichi election victory seen constraining BOJ normalization through political pressure

Japan election aftermath creating policy uncertainty as Takaichi landslide victory on Feb 8 strengthens fiscal expansion mandate pressuring yen

Japanese 10-year JGB yields at 2.21% down from 2.26% peak creating fiscal relief but still near 21st-century highs limiting BOJ policy space

Fed maintaining 3.5-3.75% rate while BOJ holds at 0.75% preserving 275-300bp differential favoring structural USD strength despite convergence narrative

| ▲ Resistance Zone 2 | 0.0047 – 0.0087 |

| ▲ Resistance Zone 1 | 0.0046 – 0.0086 |

| ─ Pivot Area | ~0.0065 |

| ▼ Support Zone 1 | 0.0043 – 0.0083 |

| ▼ Support Zone 2 | 0.0043 – 0.0083 |

Range consolidation 152-158 USD/JPY with weakening directional momentum; price testing post-election equilibrium after volatile Feb 8 reaction

Policy divergence narrative complicated by Takaichi fiscal expansion mandate creating BOJ normalization headwinds versus persistent Fed-BOJ rate differential

Mixed positioning post-election with net short JPY reduced from extremes but elevated; 299K open interest reflecting cautious two-way engagement

Implied volatility at 9.41 (68th percentile) elevated post-election but declining from Feb 8 event peak reflecting residual uncertainty normalization

Fed holding 3.5-3.75% through May per consensus while BOJ at 0.75% faces political pressure from Takaichi election victory on Feb 8

Normal - short-term 9.8% below medium 10.5% and long 11.8% reflecting post-February 8 election event compression from pre-catalyst anxiety

Similar post-election consolidations see volatility compress 15-20% over 2-3 weeks then re-expand on next catalyst; current 68th percentile positioning suggests room for 25-30% expansion if March BOJ surprises

Volatility likely to continue contracting 5-7 days post-election toward 50th percentile before re-expanding into March 19 BOJ meeting; typical pattern shows 15-20% decline within 2 weeks of major political events

High volatility regime suggests 80-100 pip daily ranges (0.00050-0.00065 in 6J terms) versus normal 50-60 pips; March 19 BOJ meeting likely triggers 150-250 pip move in 24-48 hours; breakouts from 152-158 consolidation more reliable if accompanied by 120+ pip sustained moves

Elevated 68th percentile volatility indicates 1.2-1.5% daily move potential versus normal 0.6-0.8%; March 19 BOJ meeting creates binary risk premium with potential 200-300 pip move (2+ standard deviations) on surprise outcome representing asymmetric reward for directional positioning post-clarity

|

⚠️ Primary Risk

Takaichi fiscal expansion accelerates JGB yield surge above 2.30% forcing BOJ bond market intervention and undermining normalization credibility Probability: MEDIUM

|

✦ Primary Opportunity

Yen mean reversion rally toward 0.0065-0.0068 range (150-147 USD/JPY) if BOJ accelerates normalization despite political pressure or US data weakens Timeframe: 3-6 weeks through March BOJ meeting

|

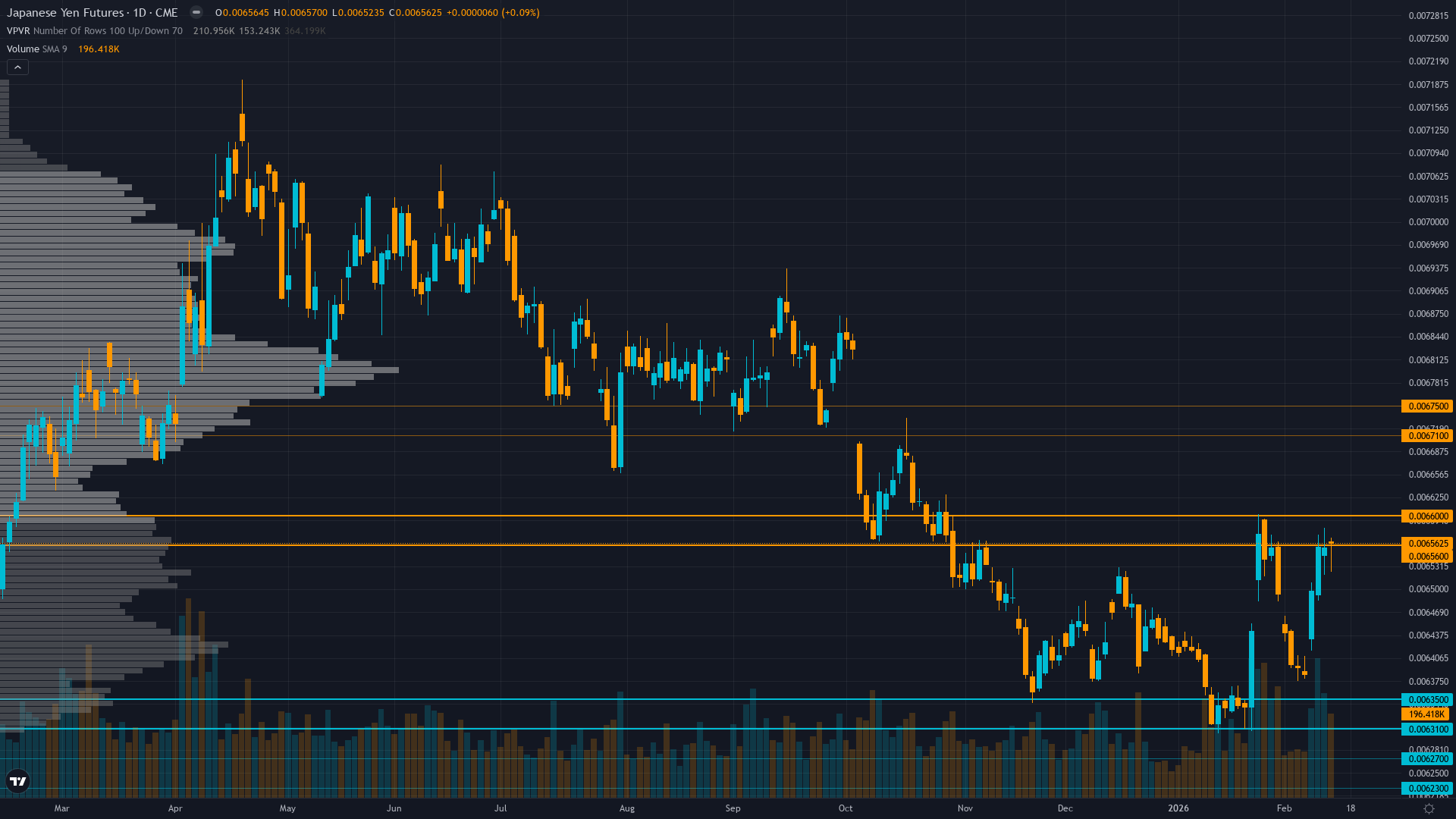

The Japanese Yen futures (6J) sit at a critical post-election crossroads on February 15, 2026, trading at 0.006548 (USD/JPY 152.7) after Prime Minister Sanae Takaichi's historic landslide victory on February 8 fundamentally altered the policy landscape. The election delivered Takaichi a commanding mandate for her fiscally aggressive agenda including consumption tax cuts and abandonment of primary balance targets, creating immediate market repricing. USD/JPY initially weakened on election day but has since stabilized in a 152-158 consolidation range as markets digest the implications.

The fundamental backdrop remains anchored by the 275-300bp Fed-BOJ rate differential (Fed 3.5-3.75% vs BOJ 0.75%), but Takaichi's victory introduces asymmetric risks. Japanese 10-year JGB yields have eased to 2.21% from the 2.26% peak seen before the election, providing temporary fiscal relief, yet remain near 21st-century highs that threaten debt sustainability with Japan's 260% debt-to-GDP ratio. The BOJ faces an impossible trilemma under Takaichi: continue normalization and risk bond market stress, pause normalization and embed inflation expectations, or intervene in JGBs and sacrifice credibility.

Governor Ueda's January 23 meeting revealed internal hawkish pressure with board member Takata's dissenting vote for 1%, but the election outcome likely constrains aggressive action near-term. Market positioning shows defensive reduction in net short JPY from 2025 extremes but remains elevated at 299K open interest, creating fuel for violent moves. Volatility has compressed to the 68th percentile (9.41 implied vol) from February 8 event peaks but stays elevated versus historical norms, reflecting ongoing uncertainty.

The immediate 6-week period post-election typically shows policy paralysis as governments form agendas, suggesting range-bound consolidation until the March 19 BOJ meeting clarifies the path. February seasonality historically shows neutral-to-slight JPY strength, though 2026's unique political catalyst overrides normal patterns. Current valuation near 152.7 sits in the middle of the 2025 range (139.88-159.46), providing balanced risk-reward. The consensus expects continued USD strength on rate differentials, but this consensus is fragile—vulnerable to either accelerated BOJ normalization if wage data stays strong (spring Shunto negotiations key) or dovish Fed pivot if US data weakens.

The edge lies in recognizing the market significantly underprices the political constraint on BOJ policy flexibility. Takaichi's election victory is not just noise—it represents a fundamental regime shift toward fiscal dominance that will force the BOJ to subordinate monetary policy to debt sustainability concerns. This creates a tactical setup: near-term yen weakness on policy paralysis, but medium-term mean reversion potential if fiscal concerns force official response or if the Fed proves more dovish than currently priced.

Devil's advocate: The counterargument for yen strength is that Takaichi's fiscal expansion could actually accelerate nominal growth and inflation, forcing the BOJ to hike faster than consensus expects despite political pressure, while simultaneously the Fed may need to ease more aggressively if Trump tariffs slow US growth. However, Japan's 30-year yield hitting record 3.88% on January 20 suggests bond vigilantes are increasingly skeptical of fiscal sustainability, making aggressive BOJ tightening politically and economically untenable.

Current positioning favors patient tactical longs in yen (short USD/JPY) targeting the 150-152 range on post-election consolidation fatigue and mean reversion dynamics, but sizing must be defensive given the persistent rate differential headwind and range-bound regime.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| February 8, 2026 | BULLISH | 7/10 | ❌ |

| February 1, 2026 | NEUTRAL | 7/10 | ❌ |

| January 25, 2026 | BULLISH | 7/10 | ❌ |

| January 11, 2026 | BULLISH | 7/10 | ❌ |

| January 4, 2026 | BEARISH | 6/10 | ✅ |

| December 28, 2025 | BEARISH | 6/10 | ✅ |

| December 21, 2025 | BULLISH | 7/10 | ✅ |

| December 14, 2025 | BULLISH | 7/10 | ❌ |

| December 7, 2025 | BEARISH | 6/10 | ✅ |

| November 30, 2025 | BEARISH | 6/10 | ❌ |

| November 23, 2025 | BEARISH | 7/10 | ❌ |