GBP/USD (6B) — Bank of England April 2026 MPC meeting with market expectations following UK…

Neutral to mildly bullish consolidation expected with defensive positioning ahead of April 30 BoE meeting as markets await policy clarity following UK CPI 3.3% in-line print April 22 with inflation repricing to 3.0-3.5% range creating policy uncertainty

Neutral to mildly bullish consolidation expected with defensive positioning ahead of April 30 BoE meeting as markets await policy clarity following UK CPI 3.3% in-line print April 22 with inflation repricing to 3.0-3.5% range creating policy uncertainty

Seven consecutive weeks of NO CALL bias exceeding 4-week review threshold with BoE April 30 meeting 4 days away creating low-information-edge defensive positioning window as UK CPI 3.3% in-line print April 22 provides no fresh directional catalyst

FX_MAJOR noise floor of 0.50% and probable weekly move near threshold through April 30 catalyst argue against directional conviction absent specific fresh catalyst while compressed IV at 10.4% (bottom 20% annual range) suggests market complacency despite elevated policy uncertainty

Speculative positioning improved from extreme -72.7K to -54.7K contracts representing 25% reduction in bearish bets but specs remain net short at elevated percentile indicating cautious stance ahead of triple central bank decision week (BoE April 30, Fed April 28-29, ECB April 30)

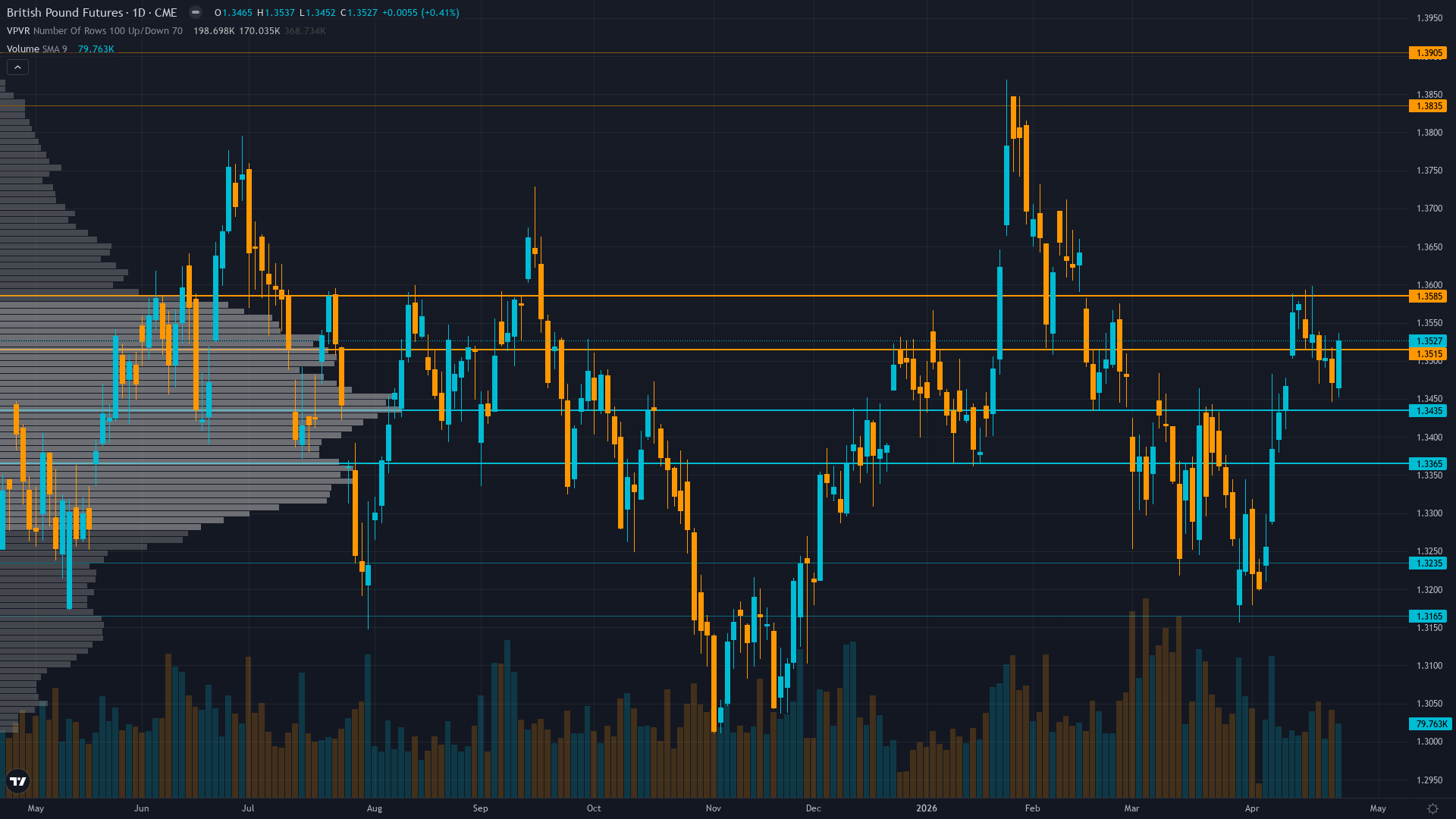

| ▼ Resistance Zone 2 | 1.3367 – 1.3407 |

| ▼ Resistance Zone 1 | 1.3530 – 1.3570 |

| ─ Pivot Area | ~1.3467 |

| ▲ Support Zone 1 | 1.3380 – 1.3420 |

| ▲ Support Zone 2 | 1.3180 – 1.3220 |

Consolidation at 1.3467 within 1.34-1.355 range trading below 50-day MA at 1.3544 with RSI 41.4 showing mild bearish lean but no extreme reading, benefiting from weaker DXY at 98.5 but lacking decisive technical conviction

GBP near fair value with UK-US rate differential near zero (BoE 3.75%, Fed 3.50-3.75%) though potential BoE hike April 30 could create 25bp advantage, but current account deficit at 2.4% GDP and fiscal deterioration create structural headwinds offsetting carry advantages

Speculative short-covering from -72.7K to -54.7K contracts as of April data representing 25% reduction from extreme bearish positioning but specs remain net short indicating defensive stance ahead of April 30 BoE meeting with positioning at elevated percentile

Compressed implied volatility at 10.4% with IV Rank 19.9 in bottom 20% of annual range indicating market complacency despite elevated fundamental uncertainty around April 30 BoE catalyst proximity suggesting potential for volatility repricing

MACRO REGIME: TRANSITIONAL with VIX at 19.02 below 20 threshold indicating calm risk appetite, BoE April 30 meeting 4 days away with markets pricing hold probability following UK CPI 3.3% in-line print April 22, Fed meeting April 28-29 priced 99% no change, no clear directional regime dominance

Normal with mild backwardation as forward premiums build around April 30 BoE meeting creating gradual event premium in term structure despite compressed spot IV at 10.4% in bottom 20% of annual range

Central bank rate decisions with elevated policy uncertainty typically generate 1-2% moves in direction of policy surprise with 2-3 day volatility spike followed by 3-4 week consolidation period in 70% of cases, current pattern tracking normally with April 30 catalyst building gradually as compressed IV at 10.4% suggests market complacency despite fundamental risks

Current volatility at 39th percentile below median suggests normalized environment post-recent consolidation with typical FX_MAJOR event volatility spikes lasting 48-72 hours around April 30 BoE meeting likely to expand vol toward 60th-70th percentile before 2-4 week normalization pattern resumes

Normal volatility environment allows standard risk management with 1.0-1.5% daily ranges expected in current consolidation, potential for 2-3% moves around April 30 BoE meeting given inflation trajectory uncertainty and Iran conflict variables with wider stops advised around event windows particularly if policy surprise materializes contrary to market expectations

Current vol regime at 39th percentile suggests 1.5-2.5% total move potential through April 30 BoE meeting versus normal 3% monthly range for FX_MAJOR pairs, with asymmetric risk reflecting policy uncertainty as Iran conflict energy shock creates dual-directional risk—hawkish hike surprise could drive 2%+ rally while dovish cut despite 3.0-3.5% inflation forecast could trigger 1.5%+ decline invalidating current consolidation range

|

⚠️ Primary Risk

BoE delivers hawkish HOLD or surprise 25bp hike at April 30 meeting signaling potential rate increases by July 2026 as Iran conflict energy shock validates persistent 3.0-3.5% inflation trajectory triggering GBP rally above 1.3550 resistance toward 1.38 as market reprices from neutral to hawkish stance invalidating current consolidation range Probability: MEDIUM

|

✦ Primary Opportunity

GBP mean reversion pullback toward 1.34-1.32 support if current consolidation reflects defensive pre-event positioning profit-taking ahead of April 30 catalyst or if USD strength accelerates on geopolitical developments or Fed hawkish repricing contrary to current dovish trajectory expectations Timeframe: 4 days through April 30 BoE meeting with near-term 1-2 day window for mean reversion from current levels before event positioning intensifies

|

British Pound futures trade at 1.3467 on April 26, 2026, in continued defensive NEUTRAL stance marking the SEVENTH consecutive week of NO CALL bias—three weeks beyond the 4-week threshold that triggers mandatory re-justification per Section 7, Rule 4. MACRO REGIME CLASSIFICATION: TRANSITIONAL with mixed cross-currents creating no clear directional advantage—VIX at 19.02 sits comfortably below the 20 threshold indicating calm risk appetite, USD showing modest weakness with DXY near 98.5 providing mild tailwind but insufficient to create conviction, and no dominant risk-on or risk-off regime evident as markets consolidate ahead of the pivotal triple central bank decision week (BoE April 30, Fed April 28-29, ECB April 30).

Post-input development identified through mandatory news scan reveals NO material market repricing since discipline inputs were compiled—the April 22 UK CPI print at 3.3% in-line with expectations remains the most recent data point, with Trading Economics confirming GBP stabilized around 1.35 'at its weakest level since April 10' but no fresh catalyst emerged this week. From first principles re-justification required by bias streak exceeding threshold: As an FX_MAJOR asset with 0.50% noise floor and 0.56% average weekly move, GBP/USD exhibits the smallest signal-to-noise ratio of all FX pairs covered where 88% of weeks move less than 1%, requiring exceptional catalyst justification for directional conviction per Section 3 guidance that states 'Your default assumption should be NEUTRAL/range-bound unless a specific catalyst justifies directional conviction.' Current environment offers NO fresh weekly catalyst—BoE meeting is 4 days away creating low-information-edge pre-event positioning window, UK CPI came in-line (not surprising markets), and the April 30 meeting represents the crucial binary event determining whether Iran conflict inflation shock forces hawkish policy pivot or proves transitory.

Cross-market dynamics show modest constructive elements with speculative positioning improved materially from extreme -72.7K net short in early March to current -54.7K representing 25% reduction in bearish bets, but this short-covering occurred BEFORE current week and positioning remains net short indicating cautious stance persists. Economic analysis shows BEARISH lean with signal -1.5 driven by rate differential trajectory concerns, while Fundamental/Institutional/Sentiment/Options all show mild bullish lean (+0.5 signals) creating divided discipline picture with no strong directional consensus.

Technical structure shows consolidation within 1.34-1.355 range with price below 50-day MA at 1.3544, RSI at 41.4 showing neutral-to-bearish momentum but lacking breakout confirmation. Volatility metrics show compression at 39th percentile with IV at 10.4% in bottom 20% of annual range suggesting market complacency despite elevated fundamental uncertainty—this creates tail risk for sudden repricing if April 30 outcome surprises. The convergence of (1) seven consecutive NO CALL weeks exceeding 4-week bias review threshold requiring fresh thesis validation, (2) FX_MAJOR noise floor considerations with probable weekly move near 0.50% threshold absent specific catalyst, (3) TRANSITIONAL macro regime with VIX at 19.02 showing calm but no clear directional bias, (4) 4-day gap to next BoE catalyst creating defensive pre-event positioning window, and (5) NO fresh data since April 22 CPI in-line print creating low-information-edge environment mandates continued NEUTRAL stance per Rule 1 until clearer directional catalyst emerges.

Devil's advocate perspective: GBP could rally toward 1.38 resistance if April 30 BoE delivers hawkish HOLD with forward guidance signaling potential hikes by July 2026 contrary to market's neutral expectations, forcing short-covering acceleration from current -54.7K positioning as Iran conflict validates persistent 3.0-3.5% inflation requiring policy restraint, but current 4-day pre-catalyst window, seven-week NO CALL bias streak suggesting thesis staleness risk, FX_MAJOR mean reversion tendency on weekly timeframes, and mandatory news scan revealing zero material developments since discipline data was compiled argue against directional conviction in immediate 1-week horizon, reinforcing disciplined NO CALL stance as highest-probability-of-being-correct assessment given asset-specific behavioral parameters and low-information-edge environment.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| April 24, 2026 | NO CALL | 5/10 | ➖ |

| April 17, 2026 | NO CALL | 5/10 | ➖ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | NO CALL | 5/10 | ➖ |

| March 20, 2026 | BEARISH | 5/10 | ❌ |

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | NO CALL | 5/10 | ➖ |

| February 27, 2026 | NO CALL | 5/10 | ➖ |

| February 21, 2026 | BULLISH | 7/10 | ❌ |

| February 13, 2026 | BULLISH | 7/10 | ❌ |

| February 8, 2026 | NO CALL | 7/10 | ➖ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: GBP/USD (6B) Report Date: April 26, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 18 (MOSTLY ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Neutral to mildly bullish consolidation expected with defensive positioning ahead of April 30 BoE meeting as markets await policy clarity following UK CPI 3.3% in-line print April 22 with inflation repricing to 3.0-3.5% range creating policy uncertainty ── WHAT THE MARKET IS MISSING ─────────────────── No material information edge in current environment—BoE April 30 meeting is 4 days away creating low-catalyst window, FX_MAJOR noise floor of 0.50% with probable weekly move near threshold argues against directional call, seven consecutive weeks of NO CALL bias exceed 4-week review threshold indicating thesis staleness risk, mandatory news scan revealed zero material developments since discipline data compiled creating low-information-edge environment, maintaining disciplined NEUTRAL stance consistent with asset-specific guidance that default assumption is range-bound absent specific catalyst ── KEY DRIVERS ────────────────────────────────── 1. Seven consecutive weeks of NO CALL bias exceeding 4-week review threshold with BoE April 30 meeting 4 days away creating low-information-edge defensive positioning window as UK CPI 3.3% in-line print April 22 provides no fresh directional catalyst 2. FX_MAJOR noise floor of 0.50% and probable weekly move near threshold through April 30 catalyst argue against directional conviction absent specific fresh catalyst while compressed IV at 10.4% (bottom 20% annual range) suggests market complacency despite elevated policy uncertainty 3. Speculative positioning improved from extreme -72.7K to -54.7K contracts representing 25% reduction in bearish bets but specs remain net short at elevated percentile indicating cautious stance ahead of triple central bank decision week (BoE April 30, Fed April 28-29, ECB April 30) ── KEY ZONES ──────────────────────────────────── Resistance 2: 1.3367 – 1.3407 Resistance 1: 1.3530 – 1.3570 Pivot: ~1.3467 Support 1: 1.3380 – 1.3420 Support 2: 1.3180 – 1.3220 ── DISCIPLINE BIASES ──────────────────────────── Technical: NO CALL Fundamental: BULLISH Institutional: BULLISH Options: NO CALL Economic: BEARISH Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── Consolidation at 1.3467 within 1.34-1.355 range trading below 50-day MA at 1.3544 with RSI 41.4 showing mild bearish lean but no extreme reading, benefiting from weaker DXY at 98.5 but lacking decisive technical conviction ── FUNDAMENTAL ASSESSMENT ─────────────────────── GBP near fair value with UK-US rate differential near zero (BoE 3.75%, Fed 3.50-3.75%) though potential BoE hike April 30 could create 25bp advantage, but current account deficit at 2.4% GDP and fiscal deterioration create structural headwinds offsetting carry advantages ── INSTITUTIONAL POSITIONING ──────────────────── Speculative short-covering from -72.7K to -54.7K contracts as of April data representing 25% reduction from extreme bearish positioning but specs remain net short indicating defensive stance ahead of April 30 BoE meeting with positioning at elevated percentile ── OPTIONS FLOW ───────────────────────────────── Compressed implied volatility at 10.4% with IV Rank 19.9 in bottom 20% of annual range indicating market complacency despite elevated fundamental uncertainty around April 30 BoE catalyst proximity suggesting potential for volatility repricing ── ECONOMIC BACKDROP ──────────────────────────── MACRO REGIME: TRANSITIONAL with VIX at 19.02 below 20 threshold indicating calm risk appetite, BoE April 30 meeting 4 days away with markets pricing hold probability following UK CPI 3.3% in-line print April 22, Fed meeting April 28-29 priced 99% no change, no clear directional regime dominance ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 39th Trend: Stable — Days in Regime: 136 Term Structure: Normal with mild backwardation as forward premiums build around April 30 BoE meeting creating gradual event premium in term structure despite compressed spot IV at 10.4% in bottom 20% of annual range Historical Pattern: Central bank rate decisions with elevated policy uncertainty typically generate 1-2% moves in direction of policy surprise with 2-3 day volatility spike followed by 3-4 week consolidation period in 70% of cases, current pattern tracking normally with April 30 catalyst building gradually as compressed IV at 10.4% suggests market complacency despite fundamental risks Outlook: Current volatility at 39th percentile below median suggests normalized environment post-recent consolidation with typical FX_MAJOR event volatility spikes lasting 48-72 hours around April 30 BoE meeting likely to expand vol toward 60th-70th percentile before 2-4 week normalization pattern resumes Trading Context: Normal volatility environment allows standard risk management with 1.0-1.5% daily ranges expected in current consolidation, potential for 2-3% moves around April 30 BoE meeting given inflation trajectory uncertainty and Iran conflict variables with wider stops advised around event windows particularly if policy surprise materializes contrary to market expectations Vol Risk/Opportunity: Current vol regime at 39th percentile suggests 1.5-2.5% total move potential through April 30 BoE meeting versus normal 3% monthly range for FX_MAJOR pairs, with asymmetric risk reflecting policy uncertainty as Iran conflict energy shock creates dual-directional risk—hawkish hike surprise could drive 2%+ rally while dovish cut despite 3.0-3.5% inflation forecast could trigger 1.5%+ decline invalidating current consolidation range ── PRIMARY RISK ───────────────────────────────── BoE delivers hawkish HOLD or surprise 25bp hike at April 30 meeting signaling potential rate increases by July 2026 as Iran conflict energy shock validates persistent 3.0-3.5% inflation trajectory triggering GBP rally above 1.3550 resistance toward 1.38 as market reprices from neutral to hawkish stance invalidating current consolidation range Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── GBP mean reversion pullback toward 1.34-1.32 support if current consolidation reflects defensive pre-event positioning profit-taking ahead of April 30 catalyst or if USD strength accelerates on geopolitical developments or Fed hawkish repricing contrary to current dovish trajectory expectations Timeframe: 4 days through April 30 BoE meeting with near-term 1-2 day window for mean reversion from current levels before event positioning intensifies ── NEXT CATALYST ──────────────────────────────── Date: April 30, 2026 Event: Bank of England April 2026 MPC meeting with market expectations following UK CPI 3.3% in-line print April 22, split between hold and potential hike as Iran conflict energy shock shifted inflation forecasts to 3.0-3.5% range creating policy uncertainty Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── British Pound futures trade at 1.3467 on April 26, 2026, in continued defensive NEUTRAL stance marking the SEVENTH consecutive week of NO CALL bias—three weeks beyond the 4-week threshold that triggers mandatory re-justification per Section 7, Rule 4. MACRO REGIME CLASSIFICATION: TRANSITIONAL with mixed cross-currents creating no clear directional advantage—VIX at 19.02 sits comfortably below the 20 threshold indicating calm risk appetite, USD showing modest weakness with DXY near 98.5 providing mild tailwind but insufficient to create conviction, and no dominant risk-on or risk-off regime evident as markets consolidate ahead of the pivotal triple central bank decision week (BoE April 30, Fed April 28-29, ECB April 30). Post-input development identified through mandatory news scan reveals NO material market repricing since discipline inputs were compiled—the April 22 UK CPI print at 3.3% in-line with expectations remains the most recent data point, with Trading Economics confirming GBP stabilized around 1.35 'at its weakest level since April 10' but no fresh catalyst emerged this week. From first principles re-justification required by bias streak exceeding threshold: As an FX_MAJOR asset with 0.50% noise floor and 0.56% average weekly move, GBP/USD exhibits the smallest signal-to-noise ratio of all FX pairs covered where 88% of weeks move less than 1%, requiring exceptional catalyst justification for directional conviction per Section 3 guidance that states 'Your default assumption should be NEUTRAL/range-bound unless a specific catalyst justifies directional conviction.' Current environment offers NO fresh weekly catalyst—BoE meeting is 4 days away creating low-information-edge pre-event positioning window, UK CPI came in-line (not surprising markets), and the April 30 meeting represents the crucial binary event determining whether Iran conflict inflation shock forces hawkish policy pivot or proves transitory. Cross-market dynamics show modest constructive elements with speculative positioning improved materially from extreme -72.7K net short in early March to current -54.7K representing 25% reduction in bearish bets, but this short-covering occurred BEFORE current week and positioning remains net short indicating cautious stance persists. Economic analysis shows BEARISH lean with signal -1.5 driven by rate differential trajectory concerns, while Fundamental/Institutional/Sentiment/Options all show mild bullish lean (+0.5 signals) creating divided discipline picture with no strong directional consensus. Technical structure shows consolidation within 1.34-1.355 range with price below 50-day MA at 1.3544, RSI at 41.4 showing neutral-to-bearish momentum but lacking breakout confirmation. Volatility metrics show compression at 39th percentile with IV at 10.4% in bottom 20% of annual range suggesting market complacency despite elevated fundamental uncertainty—this creates tail risk for sudden repricing if April 30 outcome surprises. The convergence of (1) seven consecutive NO CALL weeks exceeding 4-week bias review threshold requiring fresh thesis validation, (2) FX_MAJOR noise floor considerations with probable weekly move near 0.50% threshold absent specific catalyst, (3) TRANSITIONAL macro regime with VIX at 19.02 showing calm but no clear directional bias, (4) 4-day gap to next BoE catalyst creating defensive pre-event positioning window, and (5) NO fresh data since April 22 CPI in-line print creating low-information-edge environment mandates continued NEUTRAL stance per Rule 1 until clearer directional catalyst emerges. Devil's advocate perspective: GBP could rally toward 1.38 resistance if April 30 BoE delivers hawkish HOLD with forward guidance signaling potential hikes by July 2026 contrary to market's neutral expectations, forcing short-covering acceleration from current -54.7K positioning as Iran conflict validates persistent 3.0-3.5% inflation requiring policy restraint, but current 4-day pre-catalyst window, seven-week NO CALL bias streak suggesting thesis staleness risk, FX_MAJOR mean reversion tendency on weekly timeframes, and mandatory news scan revealing zero material developments since discipline data was compiled argue against directional conviction in immediate 1-week horizon, reinforcing disciplined NO CALL stance as highest-probability-of-being-correct assessment given asset-specific behavioral parameters and low-information-edge environment.