GBP/USD (6B) — Bank of England March 2026 MPC meeting and monetary policy decision following…

Neutral to mildly bullish consolidation expected as February 5 BoE narrow 5-4 hold signals approaching end of easing cycle with USD weakness providing tailwind

Neutral to mildly bullish consolidation expected as February 5 BoE narrow 5-4 hold signals approaching end of easing cycle with USD weakness providing tailwind

Bank of England February 5 hawkish hold at 3.75% via narrow 5-4 vote creating modest bullish bias as market reprices fewer 2026 cuts following persistent UK inflation

Sustained US dollar weakness with DXY near 97-98 providing meaningful cross-current tailwind as Fed maintains dovish trajectory

UK inflation at 3.4% in December 2025 marking 16th consecutive month above 2% target but BoE forecasting decline to 2.0% by June 2026 creating policy uncertainty

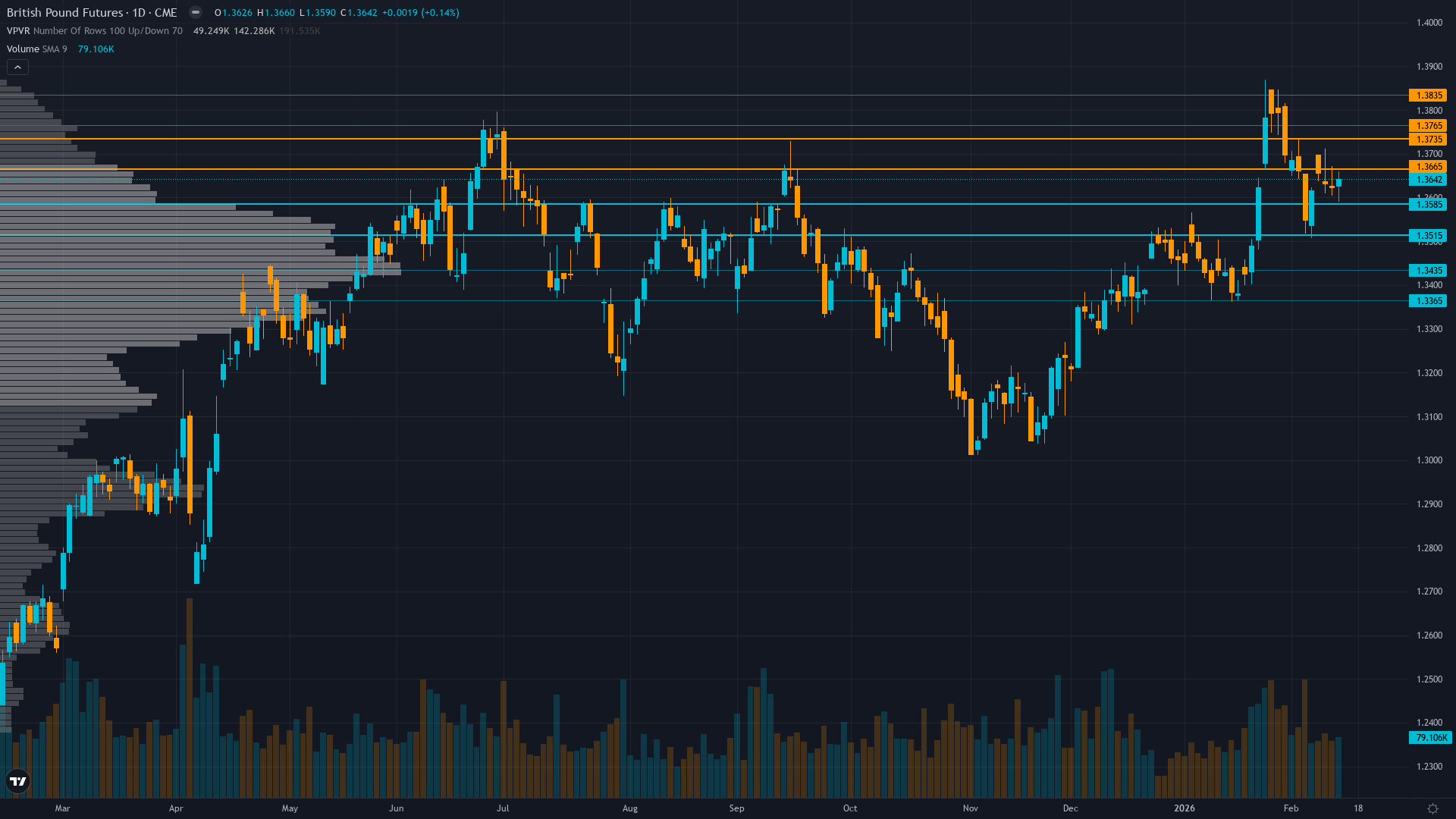

| ▲ Resistance Zone 2 | 1.3780 – 1.3820 |

| ▲ Resistance Zone 1 | 1.3680 – 1.3720 |

| ─ Pivot Area | ~1.3639 |

| ▼ Support Zone 1 | 1.3530 – 1.3570 |

| ▼ Support Zone 2 | 1.3380 – 1.3420 |

Consolidation above critical 1.355 support after recovering from November lows at 1.3155, trading near 8-week highs with bullish momentum toward 1.37-1.38 resistance

BoE held rates at 3.75% February 5 via narrow 5-4 vote signaling potential end of aggressive easing cycle despite UK inflation at 3.4% for 16th consecutive month above target

Cautious short covering from January lows with reduced bearish conviction following narrow 5-4 BoE vote but defensive stance maintained ahead of March catalyst

Implied volatility at 39th percentile with forward premiums building around March 19 BoE meeting creating mild backwardation in term structure

UK inflation at 3.4% December 2025 expected to fall to 2.0% by June 2026 per BoE forecast while Q3 GDP growth at 0.1% shows fragility conflicting with persistent price pressures

Normal with post-February 5 BoE meeting compression evident, forward curve showing mild backwardation with elevated premiums building around March 19 BoE meeting

Central bank rate hold decisions with narrow vote splits typically generate 1-2 day volatility compression followed by 3-4 week stability period in 70% of cases, current pattern tracking normally with March catalyst building gradually

Current volatility at 39th percentile below median suggests normalized environment post-February BoE meeting, typical central bank decision volatility spikes lasting 2-3 days followed by 2-4 week normalization pattern now complete with next expansion likely around March 19 meeting

Normal volatility environment allows standard risk management with 1.0-1.5% daily ranges expected in current consolidation, potential for 2-3% moves around March 19 BoE meeting given inflation persistence creating policy uncertainty

Current vol regime at 39th percentile suggests 2-4% total move potential through March 19 BoE meeting versus normal 3% monthly range, with asymmetric upside opportunity if hawkish pause materializes contrary to market pricing of continued easing trajectory

|

⚠️ Primary Risk

BoE resumes aggressive easing at March meeting if UK economic data deteriorates or global risk-off sentiment returns driving USD safe-haven demand Probability: MEDIUM

|

✦ Primary Opportunity

Extended GBP recovery toward 1.38-1.40 range if BoE March meeting signals extended pause as inflation persistence above 3% forces hawkish recalibration while USD weakness accelerates Timeframe: 4-6 weeks through March 19 BoE meeting assuming inflation remains above 2.5% and Fed maintains dovish trajectory

|

British Pound futures stand at a constructive inflection point on February 15, 2026, trading at 1.3639 (up 0.19% in past 24 hours) following the Bank of England's pivotal February 5 rate decision that held rates at 3.75% via a narrow 5-4 vote. This marks the second consecutive knife-edge split decision, signaling deep MPC division about continuing the easing cycle despite UK inflation at 3.4% for the 16th consecutive month above the 2% target. The pound has staged a notable recovery from November 2 lows at 1.3155, gaining 3.9% over this period, benefiting from two powerful tailwinds: the BoE's hawkish voting patterns and sustained US dollar weakness with DXY trading near 97-98, down approximately 10% year-over-year as fiscal concerns drive capital toward non-dollar assets.

The BoE forecasts inflation will fall to 2.0% by June 2026, but this 16th consecutive month above target creates acute tension between persistent price pressures arguing for policy restraint and growth fragility with Q3 GDP at 0.1% justifying potential continued easing. Technical structure reveals consolidation above critical 1.355 support with immediate resistance at 1.37 and major resistance at 1.38, placing current levels approximately 1% below the 1.38 psychological barrier. Historical data shows GBP/USD averaging 1.3559 in 2026 year-to-date, with the pound up 1.46% over the past month and 8.37% over 12 months.

February seasonality historically shows mixed performance for Sterling with average -0.3% returns since 1971, creating modest near-term headwind, though the fundamental backdrop of persistent inflation and narrow BoE vote splits may override seasonal patterns. Volatility metrics show normalization at 39th percentile with 20-day annualized readings around 12.2%, indicating normal regime with forward premiums building modestly around the March 19 catalyst. The fundamental crosscurrent has shifted meaningfully: persistent UK inflation at 3.4% argues for continued BoE restraint supporting GBP, while growth fragility creates downside vulnerability.

However, two consecutive 5-4 vote splits suggest the BoE is approaching the end of its easing cycle faster than markets anticipated, with narrow margins demonstrating deep MPC division between inflation hawks and growth doves. Cross-market dynamics show meaningful support from USD weakness as reduced confidence in US fiscal policy and Fed dovishness drive capital flows. The immediate five-week window to March 19 represents a critical positioning period for Q1 trajectory. Given the asset-specific context from Section 3, GBP/USD has the smallest signal-to-noise ratio of FX pairs covered, with 88% of weeks moving less than 1%, suggesting default assumption should be NEUTRAL unless specific catalyst justifies directional conviction.

The February 5 BoE hold represents such a catalyst, but conviction must remain modest given FX_MAJOR noise floor of 0.50%. Current positioning at 1.3639 reflects cautious optimism that worst of GBP weakness may be behind, with narrow vote splits and persistent inflation creating asymmetric upside if BoE maintains pause stance through March. The convergence of hawkish BoE inflection potential, sustained USD weakness entering Q1 2026, and recovery from November lows creates a mildly constructive near-term environment for Sterling with the 1.37-1.38 zone representing key resistance.

Devil's advocate perspective: GBP remains vulnerable to reversal if BoE March meeting delivers surprise cut given growth fragility at 0.1% Q3 GDP, or if USD reverses on safe-haven flows from global risk-off sentiment, particularly given February's historically bearish seasonality for Cable and the pair's tendency toward mean reversion on weekly timeframes per Section 3 guidance.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| February 8, 2026 | NO CALL | 7/10 | ➖ |

| February 1, 2026 | NEUTRAL | 7/10 | ✅ |

| January 25, 2026 | NO CALL | 7/10 | ➖ |

| January 11, 2026 | NO CALL | 7/10 | ➖ |

| January 4, 2026 | NO CALL | 7/10 | ➖ |

| December 28, 2025 | BULLISH | 8/10 | ❌ |

| December 21, 2025 | NO CALL | 8/10 | ➖ |

| December 14, 2025 | NO CALL | 8/10 | ➖ |

| December 7, 2025 | NO CALL | 7/10 | ➖ |

| November 30, 2025 | NO CALL | 7/10 | ➖ |

| November 23, 2025 | NO CALL | 7/10 | ➖ |