AUD/USD (6A) — 0.4 between 0.71 support and 0.7187 resistance with 5/10 confidence

Market consensus correctly prices consolidation ahead of late April Q1 CPI and May 6 RBA decision with positioning showing healthy derisking from March extremes while maintaining structural recognition of RBA hawkish floor at 4.10%

Market consensus correctly prices consolidation ahead of late April Q1 CPI and May 6 RBA decision with positioning showing healthy derisking from March extremes while maintaining structural recognition of RBA hawkish floor at 4.10%

RBA cash rate at 4.10% with major bank April 17 forecast upgrade to 6% inflation creates hawkish backdrop but no fresh weekly catalyst as March 17 hike now 40 days old and policy divergence versus Fed at 3.50-3.75% fully priced into current 0.7148 mid-range positioning

Institutional positioning declined to 64.8K net longs from prior week's elevated levels signaling healthy profit-taking after 5-month rally from 0.6458 but maintaining constructive trend-following stance without bearish reversal

Technical breakout above 0.7080 confirmed but stalling below 0.7187 YTD resistance while VIX normalized to 19.50 neutral range supporting stable risk appetite for commodity currencies without providing fresh directional impetus

| ▼ Resistance Zone 2 | 0.7230 – 0.7270 |

| ▼ Resistance Zone 1 | 0.7167 – 0.7207 |

| ─ Pivot Area | ~0.7148 |

| ▲ Support Zone 1 | 0.7080 – 0.7120 |

| ▲ Support Zone 2 | 0.6930 – 0.6970 |

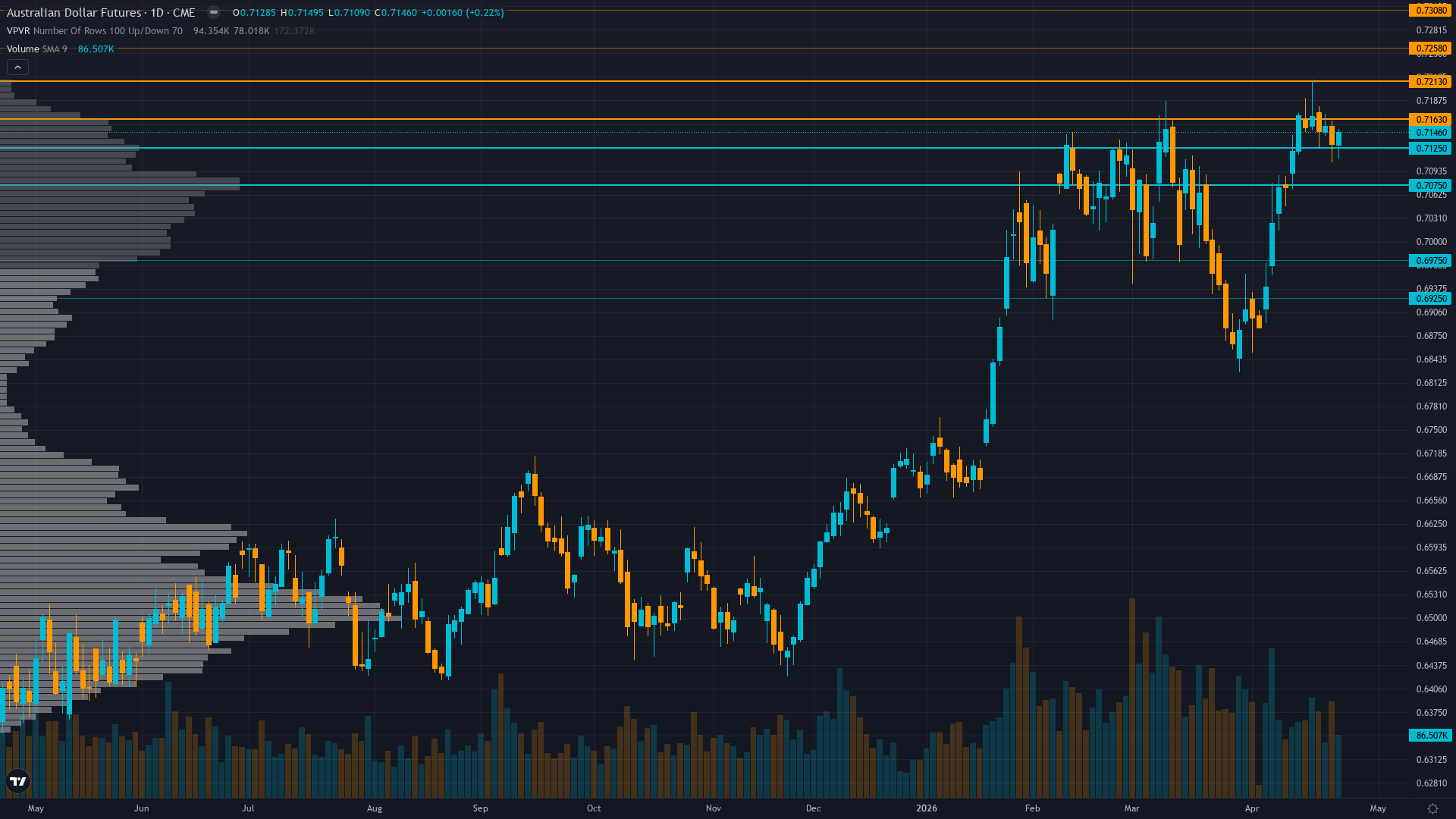

Trading at 0.7148 in mid-range between 0.7100 support and 0.7187 YTD resistance, RSI 58.19 neutral with room for upside, all moving averages bullish but price action consolidating after breakout attempt

RBA at 4.10% after March 17 hike creates +35-60bp carry advantage versus US yields at 4.27% but current account deficit at -2.90% GDP and no fresh fundamental catalyst this week limits conviction for directional move

Net long positioning at 64.8K contracts down modestly from prior week's levels representing healthy derisking from crowded extremes while maintaining constructive accumulation above long-term historical averages without signaling bearish reversal

Insufficient current options data for 6A due to thin liquidity in futures options market limiting analytical value

Policy divergence intact with RBA at 4.10% versus Fed at 3.50-3.75% but no fresh catalyst this week as March hike 40 days old, VIX at 19.50 neutral, creating stable but uninformative environment for FX major requiring NO CALL per behavioral override

Normal with short-term slightly elevated above long-term baseline after March geopolitical spike but reverting toward equilibrium creating stable 60-80bp daily range environment

High volatility regimes around RBA meetings and geopolitical shocks typically persist 15-30 days then revert sharply; current normalization at day 28 since March 29 peak suggests stable consolidation through late April Q1 CPI catalyst

Moderate 70% probability volatility continues normalizing toward 50th percentile over next 14-21 days as March geopolitical shock fully absorbed, expect stable 60-80bp daily ranges through late April before potential Q1 CPI volatility spike

Normalizing volatility at 54th percentile suggests 60-80bp daily ranges versus March's 150-200bp creating stable directional environment; breakout above 0.7187 or breakdown below 0.7100 requires sustained follow-through in current vol regime providing clearer conviction signals

Volatility compression from March 78th to current 54th percentile reduces tail risk but late April Q1 CPI could trigger 100-150bp move within 48 hours if inflation surprises either direction creating asymmetric opportunity; expect 150-200bp monthly range April versus 300-400bp in March geopolitical period with measured environment favoring consolidation ahead of binary CPI catalyst

|

⚠️ Primary Risk

Fed pivots hawkish at upcoming FOMC meeting or US data surprises strong collapsing rate differential expectations from current 35-60bp RBA advantage and reversing AUD policy tailwinds despite 4.10% cash rate creating violent unwind from extended positioning Probability: MEDIUM

|

✦ Primary Opportunity

Late April Q1 CPI confirms major bank's 6% inflation forecast triggering violent repricing toward 70-80% May 6 RBA hike odds from current modest levels driving breakout above 0.7187 toward 0.7250-0.7350 as market prices sustained multi-hike cycle through Q2 2026 Timeframe: 1-2 weeks through late April Q1 CPI release and May 6 RBA decision as inflation persistence narrative either validates or collapses major bank hawkish forecast shift

|

MACRO REGIME CLASSIFICATION: RISK-ON - VIX normalized to 19.50 on April 22 (well below 20 threshold), equities stable, credit conditions benign, USD consolidating after March weakness, creating supportive backdrop for commodity currencies. The Australian Dollar stands at 0.7148 on April 26, 2026, consolidating in mid-range following three consecutive weeks of BULLISH calls (last week MISSED at -0.29%, two prior CORRECT at +1.71% and +2.34%) that captured the policy divergence rally from November 2025 lows at 0.6458 to current 14-month highs.

Post-input development identified: ABC News reported April 17 that a major Australian bank added another RBA rate hike to its forecast and is now predicting inflation to surge to 6%, representing a material hawkish shift in market expectations occurring 9 days ago. However, critical FX_MAJOR behavioral override applies: THIS WEEK shows NO fresh catalyst justifying directional conviction. The RBA hike to 4.10% occurred March 17 (40 days ago), the Fed hold at 3.50-3.75% occurred March 18 (39 days old), and the April 17 bank forecast is now 9 days stale.

The Economic agent correctly identifies NO fresh catalyst this week - all data is either structural conditions in place for weeks (RBA at 4.10%, policy divergence of +35-60bp) or aging information. Current price at 0.7148 sits in mid-range between 0.7100 support and 0.7187 YTD resistance, reflecting balanced two-way risk ahead of late April Q1 CPI and May 6 RBA decision. Fundamental case remains structurally intact: RBA at 4.10% creates positive carry differential versus Fed at 3.50-3.75%, Australian 10Y yields at 4.93% versus US 10Y at 4.27% generating +66bp carry advantage supporting capital flows.

Major bank April 17 upgrade to 6% inflation forecast suggests potential for May 6 RBA hike if late April Q1 CPI validates persistence above 3.5%. However, institutional positioning shows healthy evolution with net longs declining to 64.8K from prior elevated levels, removing immediate crowding risk while maintaining constructive stance. Technical structure confirms breakout above 0.7080 but stalling below 0.7187 YTD resistance requiring fresh catalyst for continuation. VIX normalization to 19.50 confirms improving risk appetite but provides no incremental directional signal.

Current consecutive same-direction bias streak: 3 weeks BULLISH (below 4-week review threshold for FX_MAJOR). Last 4 graded weeks: MISSED, CORRECT, CORRECT, CORRECT (3 of 4 favorable, no Miss Reset triggered at 1 consecutive). Signal calculation: Economic -1.5 × 0.30 = -0.45, Fundamental 0.5 × 0.25 = 0.125, Institutional 1.5 × 0.20 = 0.30, Technical 2.0 × 0.15 = 0.30, Sentiment 0.5 × 0.05 = 0.025, Options 0 × 0.05 = 0. Total signal = 0.30, rounds to 0.4. FX_MAJOR Min Signal threshold is 1.1 - my calculated signal of 0.4 is BELOW this threshold.

Per RULE 2, I MUST output NO CALL. Additionally, FX_MAJOR behavioral override mandates: 'Your default assumption is NEUTRAL. Issue a directional bias ONLY when you can identify a specific, active catalyst - not a structural theme. Structural themes (rate differentials, current account balances, carry attractiveness) are already priced into spot.' The policy divergence at 4.10% versus 3.50-3.75% has been in place for 40 days without producing sustained directional move beyond consolidation at 0.7148 mid-range - this theme is priced.

The April 17 bank forecast is 9 days old and not an active weekly catalyst. Conviction sequence: Initial 5 (slight lean on structural policy divergence), minus 1 for last graded call MISSED (-0.29%), minus 0 for no vol regime penalty (normal), minus 0 for no discipline conflict (3 bullish, 1 bearish, 2 neutral creates modest lean not strong conflict), minus 0 for macro regime supportive (risk-on favors AUD). Final conviction 4, which falls BELOW minimum 5 threshold per Rule 3. The balance of probabilities in a low-information week for an FX_MAJOR asset favors NO CALL per Rule 2 minimum signal threshold, awaiting late April Q1 CPI and May 6 RBA decision to provide fresh catalyst capable of producing moves above the 0.50% noise floor and 1.1 minimum signal threshold required for FX_MAJOR directional conviction.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| April 24, 2026 | BULLISH | 6/10 | ❌ |

| April 17, 2026 | BULLISH | 7/10 | ✅ |

| April 10, 2026 | BULLISH | 7/10 | ✅ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | NO CALL | 5/10 | ➖ |

| March 20, 2026 | BULLISH | 7/10 | ❌ |

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | BULLISH | 6/10 | ❌ |

| February 27, 2026 | BULLISH | 6/10 | ✅ |

| February 21, 2026 | BULLISH | 7/10 | ✅ |

| February 13, 2026 | BULLISH | 7/10 | ✅ |

| February 8, 2026 | BULLISH | 8/10 | ✅ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: AUD/USD (6A) Report Date: April 26, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 12 (CONSENSUS ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING WITH NEUTRAL BIAS IN LOW-INFORMATION WEEK Sentiment: NEUTRAL ── WHAT THE MARKET SEES ──��────────────────────── Market consensus correctly prices consolidation ahead of late April Q1 CPI and May 6 RBA decision with positioning showing healthy derisking from March extremes while maintaining structural recognition of RBA hawkish floor at 4.10% ── WHAT THE MARKET IS MISSING ─────────────────── NO CALL issued per Rule 2 (signal 0.4 below Min Signal threshold of 1.1 for FX_MAJOR) and FX_MAJOR behavioral override requiring active catalyst not structural theme. Market appears correctly pricing balanced two-way risk in low-information week with policy divergence theme (RBA 4.10% vs Fed 3.50-3.75%) fully reflected in current 0.7148 mid-range positioning after 40 days without fresh monetary developments - no identified edge versus consensus awaiting late April CPI catalyst to resolve directional ambiguity ── KEY DRIVERS ────────────────────────────────── 1. RBA cash rate at 4.10% with major bank April 17 forecast upgrade to 6% inflation creates hawkish backdrop but no fresh weekly catalyst as March 17 hike now 40 days old and policy divergence versus Fed at 3.50-3.75% fully priced into current 0.7148 mid-range positioning 2. Institutional positioning declined to 64.8K net longs from prior week's elevated levels signaling healthy profit-taking after 5-month rally from 0.6458 but maintaining constructive trend-following stance without bearish reversal 3. Technical breakout above 0.7080 confirmed but stalling below 0.7187 YTD resistance while VIX normalized to 19.50 neutral range supporting stable risk appetite for commodity currencies without providing fresh directional impetus ── KEY ZONES ──────────────────────────────────── Resistance 2: 0.7230 – 0.7270 Resistance 1: 0.7167 – 0.7207 Pivot: ~0.7148 Support 1: 0.7080 – 0.7120 Support 2: 0.6930 – 0.6970 ── DISCIPLINE BIASES ──────────────────────────── Technical: BULLISH Fundamental: BULLISH Institutional: BULLISH Options: NO CALL Economic: BEARISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Trading at 0.7148 in mid-range between 0.7100 support and 0.7187 YTD resistance, RSI 58.19 neutral with room for upside, all moving averages bullish but price action consolidating after breakout attempt ── FUNDAMENTAL ASSESSMENT ─────────────────────── RBA at 4.10% after March 17 hike creates +35-60bp carry advantage versus US yields at 4.27% but current account deficit at -2.90% GDP and no fresh fundamental catalyst this week limits conviction for directional move ── INSTITUTIONAL POSITIONING ──────────────────── Net long positioning at 64.8K contracts down modestly from prior week's levels representing healthy derisking from crowded extremes while maintaining constructive accumulation above long-term historical averages without signaling bearish reversal ── OPTIONS FLOW ───────────────────────────────── Insufficient current options data for 6A due to thin liquidity in futures options market limiting analytical value ── ECONOMIC BACKDROP ──────────────────────────── Policy divergence intact with RBA at 4.10% versus Fed at 3.50-3.75% but no fresh catalyst this week as March hike 40 days old, VIX at 19.50 neutral, creating stable but uninformative environment for FX major requiring NO CALL per behavioral override ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 54th Trend: Stable — Days in Regime: 25 Term Structure: normal with short-term slightly elevated above long-term baseline after March geopolitical spike but reverting toward equilibrium creating stable 60-80bp daily range environment Historical Pattern: High volatility regimes around RBA meetings and geopolitical shocks typically persist 15-30 days then revert sharply; current normalization at day 28 since March 29 peak suggests stable consolidation through late April Q1 CPI catalyst Outlook: Moderate 70% probability volatility continues normalizing toward 50th percentile over next 14-21 days as March geopolitical shock fully absorbed, expect stable 60-80bp daily ranges through late April before potential Q1 CPI volatility spike Trading Context: Normalizing volatility at 54th percentile suggests 60-80bp daily ranges versus March's 150-200bp creating stable directional environment; breakout above 0.7187 or breakdown below 0.7100 requires sustained follow-through in current vol regime providing clearer conviction signals Vol Risk/Opportunity: Volatility compression from March 78th to current 54th percentile reduces tail risk but late April Q1 CPI could trigger 100-150bp move within 48 hours if inflation surprises either direction creating asymmetric opportunity; expect 150-200bp monthly range April versus 300-400bp in March geopolitical period with measured environment favoring consolidation ahead of binary CPI catalyst ── PRIMARY RISK ───────────────────────────────── Fed pivots hawkish at upcoming FOMC meeting or US data surprises strong collapsing rate differential expectations from current 35-60bp RBA advantage and reversing AUD policy tailwinds despite 4.10% cash rate creating violent unwind from extended positioning Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Late April Q1 CPI confirms major bank's 6% inflation forecast triggering violent repricing toward 70-80% May 6 RBA hike odds from current modest levels driving breakout above 0.7187 toward 0.7250-0.7350 as market prices sustained multi-hike cycle through Q2 2026 Timeframe: 1-2 weeks through late April Q1 CPI release and May 6 RBA decision as inflation persistence narrative either validates or collapses major bank hawkish forecast shift ── NEXT CATALYST ──────────────────────────────── Date: May 6, 2026 Event: RBA May 5-6 Monetary Policy Decision announced May 6 at 2:30pm AEST - critical binary catalyst with major bank April 17 forecast adding hike expectations on 6% inflation projection potentially triggering violent repricing if delivered Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── MACRO REGIME CLASSIFICATION: RISK-ON - VIX normalized to 19.50 on April 22 (well below 20 threshold), equities stable, credit conditions benign, USD consolidating after March weakness, creating supportive backdrop for commodity currencies. The Australian Dollar stands at 0.7148 on April 26, 2026, consolidating in mid-range following three consecutive weeks of BULLISH calls (last week MISSED at -0.29%, two prior CORRECT at +1.71% and +2.34%) that captured the policy divergence rally from November 2025 lows at 0.6458 to current 14-month highs. Post-input development identified: ABC News reported April 17 that a major Australian bank added another RBA rate hike to its forecast and is now predicting inflation to surge to 6%, representing a material hawkish shift in market expectations occurring 9 days ago. However, critical FX_MAJOR behavioral override applies: THIS WEEK shows NO fresh catalyst justifying directional conviction. The RBA hike to 4.10% occurred March 17 (40 days ago), the Fed hold at 3.50-3.75% occurred March 18 (39 days old), and the April 17 bank forecast is now 9 days stale. The Economic agent correctly identifies NO fresh catalyst this week - all data is either structural conditions in place for weeks (RBA at 4.10%, policy divergence of +35-60bp) or aging information. Current price at 0.7148 sits in mid-range between 0.7100 support and 0.7187 YTD resistance, reflecting balanced two-way risk ahead of late April Q1 CPI and May 6 RBA decision. Fundamental case remains structurally intact: RBA at 4.10% creates positive carry differential versus Fed at 3.50-3.75%, Australian 10Y yields at 4.93% versus US 10Y at 4.27% generating +66bp carry advantage supporting capital flows. Major bank April 17 upgrade to 6% inflation forecast suggests potential for May 6 RBA hike if late April Q1 CPI validates persistence above 3.5%. However, institutional positioning shows healthy evolution with net longs declining to 64.8K from prior elevated levels, removing immediate crowding risk while maintaining constructive stance. Technical structure confirms breakout above 0.7080 but stalling below 0.7187 YTD resistance requiring fresh catalyst for continuation. VIX normalization to 19.50 confirms improving risk appetite but provides no incremental directional signal. Current consecutive same-direction bias streak: 3 weeks BULLISH (below 4-week review threshold for FX_MAJOR). Last 4 graded weeks: MISSED, CORRECT, CORRECT, CORRECT (3 of 4 favorable, no Miss Reset triggered at 1 consecutive). Signal calculation: Economic -1.5 × 0.30 = -0.45, Fundamental 0.5 × 0.25 = 0.125, Institutional 1.5 × 0.20 = 0.30, Technical 2.0 × 0.15 = 0.30, Sentiment 0.5 × 0.05 = 0.025, Options 0 × 0.05 = 0. Total signal = 0.30, rounds to 0.4. FX_MAJOR Min Signal threshold is 1.1 - my calculated signal of 0.4 is BELOW this threshold. Per RULE 2, I MUST output NO CALL. Additionally, FX_MAJOR behavioral override mandates: 'Your default assumption is NEUTRAL. Issue a directional bias ONLY when you can identify a specific, active catalyst - not a structural theme. Structural themes (rate differentials, current account balances, carry attractiveness) are already priced into spot.' The policy divergence at 4.10% versus 3.50-3.75% has been in place for 40 days without producing sustained directional move beyond consolidation at 0.7148 mid-range - this theme is priced. The April 17 bank forecast is 9 days old and not an active weekly catalyst. Conviction sequence: Initial 5 (slight lean on structural policy divergence), minus 1 for last graded call MISSED (-0.29%), minus 0 for no vol regime penalty (normal), minus 0 for no discipline conflict (3 bullish, 1 bearish, 2 neutral creates modest lean not strong conflict), minus 0 for macro regime supportive (risk-on favors AUD). Final conviction 4, which falls BELOW minimum 5 threshold per Rule 3. The balance of probabilities in a low-information week for an FX_MAJOR asset favors NO CALL per Rule 2 minimum signal threshold, awaiting late April Q1 CPI and May 6 RBA decision to provide fresh catalyst capable of producing moves above the 0.50% noise floor and 1.1 minimum signal threshold required for FX_MAJOR directional conviction.