AUD/USD (6A) — consolidating in normal regime

Shifting from bearish expecting RBA cuts toward cautiously bullish recognizing inflation-driven hawkish floor creates support but acknowledging 10% rally extension and China concerns tempering aggressive conviction

Shifting from bearish expecting RBA cuts toward cautiously bullish recognizing inflation-driven hawkish floor creates support but acknowledging 10% rally extension and China concerns tempering aggressive conviction

RBA hawkish regime shift maintaining 3.85% cash rate after February 3 hike reversing entire 2025 easing cycle creates unprecedented policy divergence vs Fed at 3.50-3.75%

Fed January 28 hold at 3.50-3.75% with uncertain 2026 cutting path narrows policy differential to 10-35bp currently with potential for 60-85bp inversion if divergence persists

China February PMI at 49.3 NBS maintaining contraction territory threatening Australia's largest export market accounting for 30% of demand offsetting hawkish RBA tailwinds

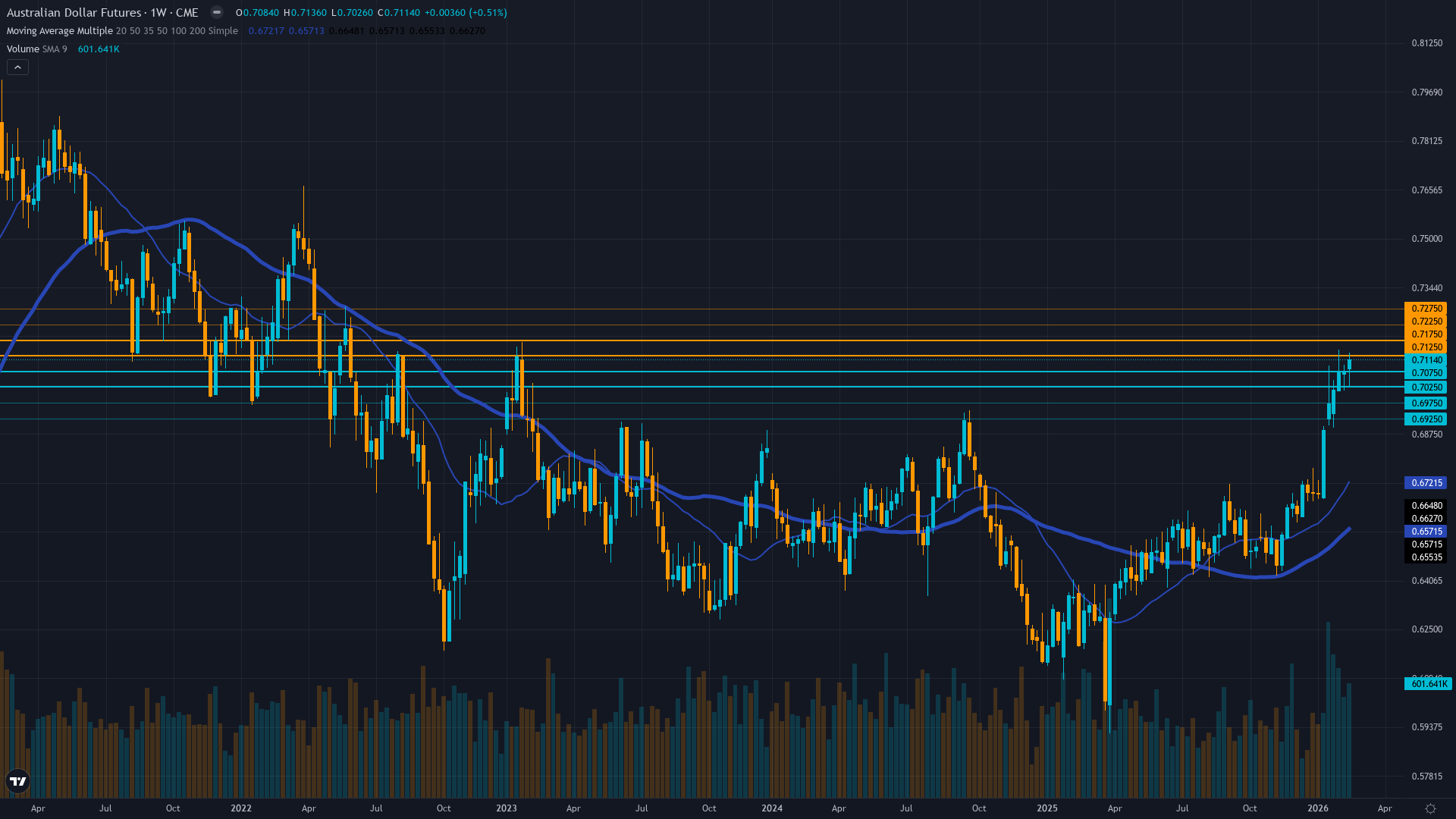

| ▲ Resistance Zone 2 | 0.7230 – 0.7270 |

| ▲ Resistance Zone 1 | 0.7130 – 0.7170 |

| ─ Pivot Area | ~0.7113 |

| ▼ Support Zone 1 | 0.7030 – 0.7070 |

| ▼ Support Zone 2 | 0.6930 – 0.6970 |

Trading at 14-month highs following 620bp rally from November lows, consolidating below 0.7150 resistance with strong moving average support across all timeframes

Policy divergence landscape transformed with RBA at 3.85% after February hike while Fed holds at 3.50-3.75% creating 10-35bp gap favoring AUD

Transitioning from November dovish expectations to constructive positioning on RBA hawkish pivot; COT shows net-long exposure at 1.7k contracts with shorts at 40-week low

Implied volatility normalized from October-November 72nd percentile to current 54-56th percentile as binary catalysts resolved

Unprecedented monetary policy divergence with Fed easing cycle paused at 3.50-3.75% while RBA pivoted to tightening at 3.85% after Q4 CPI shocked at 3.9%

Normal with short-term contracting toward long-term baseline after October-November elevated regime resolved

High volatility regimes around RBA meetings and inflation surprises typically persist 30-50 days then revert sharply; current normalization at day 115 since October peak suggests stable 60-75bp daily ranges

Strong 80% probability volatility continues normalizing toward 50th percentile over next 10-14 days as major catalysts digested before March 18 RBA potentially reignites

Normalizing volatility suggests 60-80bp daily ranges versus October's 100-150bp creating stable environment; breakouts above 0.7150 or below 0.7050 require sustained follow-through

Volatility compression from 72nd to 54th percentile reduces tail risk but March 18 RBA could trigger 100-150bp move within 48 hours if second hike delivered creating asymmetric opportunity

|

⚠️ Primary Risk

China PMI deterioration below 49.0 into deeper contraction threatening 30% of Australian export demand or Fed hawkish pause reversing easing cycle eliminating policy divergence advantage Probability: MEDIUM

|

✦ Primary Opportunity

RBA delivers second consecutive hike March-April to 4.10% while Fed continues measured easing creating 60-100bp policy inversion driving sustained rally toward 0.7250-0.7400 Timeframe: 4-8 weeks through March RBA meeting and Q1 CPI data as multi-hike cycle narrative gains momentum

|

The Australian Dollar stands at a transformative inflection point trading at 0.7113 on March 1, 2026, following the most dramatic fundamental regime shift in years. Just 14 weeks ago on November 23, AUD traded at 0.6458 with markets pricing 80% probability of continued RBA easing. Today it trades 655 basis points higher after the stunning February 3 RBA decision to hike 25bp to 3.85%, marking the shortest easing cycle on record and completely reversing policy direction in response to Q4 CPI shocking at 3.9% versus consensus 3.5%.

This creates unprecedented policy divergence: the Fed holds at 3.50-3.75% after January 28 decision with uncertain 2026 easing path, while the RBA not only halted easing but actively tightened, creating a 10-35bp differential favoring AUD that could expand to 60-85bp if divergence persists through H1 2026. However, critical crosscurrents persist. China's February manufacturing PMI deteriorated to 49.3 from January's 49.9, maintaining contraction territory and threatening Australia's largest trading partner accounting for 30% of exports.

The February 23 COT report shows bulls expressing confidence with asset managers flipping to net-long exposure for first time since October at 1.7k contracts, while shorts declined to 40-week low. Technical structure shows consolidation at 14-month highs with strong moving average support across all timeframes and technical rating showing Strong Buy. March seasonality is historically neutral for AUD. The currency trades at approximately 73rd percentile of 1-year range, elevated but not at extremes.

Volatility has normalized substantially from elevated 72nd percentile during October-November to current 54-56th percentile. The March 18 RBA meeting emerges as the critical near-term catalyst that will either validate the hawkish pivot with a second consecutive hike or signal pause, fundamentally determining whether this represents a sustained multi-hike cycle or one-off adjustment. Current positioning appears transitional as institutions shift from dovish consensus toward hawkish stance though not yet at extremes.

The balance of probabilities favors continued consolidation with modest upside bias toward 0.7150-0.7250 over the next 2-4 weeks as markets position for the March RBA decision and await confirmation that inflation trajectory justifies the hawkish repricing embedded in current 0.7113 pricing.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| February 27, 2026 | BULLISH | 6/10 | ✅ |

| February 21, 2026 | BULLISH | 7/10 | ✅ |

| February 13, 2026 | BULLISH | 7/10 | ✅ |

| February 8, 2026 | BULLISH | 8/10 | ✅ |

| February 1, 2026 | BULLISH | 8/10 | ✅ |

| January 25, 2026 | BULLISH | 8/10 | ✅ |

| January 11, 2026 | BULLISH | 8/10 | ❌ |

| January 4, 2026 | BULLISH | 8/10 | ❌ |

| December 28, 2025 | BULLISH | 8/10 | ❌ |

| December 21, 2025 | BULLISH | 7/10 | ✅ |

| December 14, 2025 | BULLISH | 8/10 | ❌ |

| December 7, 2025 | BULLISH | 8/10 | ✅ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: AUD/USD (6A) Report Date: March 1, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 6/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 35 (SLIGHT DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: RANGING WITH BULLISH BIAS Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Shifting from bearish expecting RBA cuts toward cautiously bullish recognizing inflation-driven hawkish floor creates support but acknowledging 10% rally extension and China concerns tempering aggressive conviction ── WHAT THE MARKET IS MISSING ─────────────────── Market appears under-appreciating duration of RBA hold scenario through Q2 2026 given Q4 CPI at 3.9% substantially above target suggests multi-quarter hawkish stance while over-weighting near-term China PMI weakness at 49.3 versus sustained 60-85bp policy inversion advantage representing strongest AUD fundamental backdrop since 2022 ── KEY DRIVERS ────────────────────────────────── 1. RBA hawkish regime shift maintaining 3.85% cash rate after February 3 hike reversing entire 2025 easing cycle creates unprecedented policy divergence vs Fed at 3.50-3.75% 2. Fed January 28 hold at 3.50-3.75% with uncertain 2026 cutting path narrows policy differential to 10-35bp currently with potential for 60-85bp inversion if divergence persists 3. China February PMI at 49.3 NBS maintaining contraction territory threatening Australia's largest export market accounting for 30% of demand offsetting hawkish RBA tailwinds ── KEY ZONES ──────────────────────────────────── Resistance 2: 0.7230 – 0.7270 Resistance 1: 0.7130 – 0.7170 Pivot: ~0.7113 Support 1: 0.7030 – 0.7070 Support 2: 0.6930 – 0.6970 ── DISCIPLINE BIASES ──────────────────────────── Technical: BULLISH Fundamental: BULLISH Institutional: BULLISH Options: NO CALL Economic: BULLISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Trading at 14-month highs following 620bp rally from November lows, consolidating below 0.7150 resistance with strong moving average support across all timeframes ── FUNDAMENTAL ASSESSMENT ─────────────────────── Policy divergence landscape transformed with RBA at 3.85% after February hike while Fed holds at 3.50-3.75% creating 10-35bp gap favoring AUD ── INSTITUTIONAL POSITIONING ──────────────────── Transitioning from November dovish expectations to constructive positioning on RBA hawkish pivot; COT shows net-long exposure at 1.7k contracts with shorts at 40-week low ── OPTIONS FLOW ───────────────────────────────── Implied volatility normalized from October-November 72nd percentile to current 54-56th percentile as binary catalysts resolved ── ECONOMIC BACKDROP ──────────────────────────── Unprecedented monetary policy divergence with Fed easing cycle paused at 3.50-3.75% while RBA pivoted to tightening at 3.85% after Q4 CPI shocked at 3.9% ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 54th Trend: Contracting ▼ Days in Regime: 20 Term Structure: normal with short-term contracting toward long-term baseline after October-November elevated regime resolved Historical Pattern: High volatility regimes around RBA meetings and inflation surprises typically persist 30-50 days then revert sharply; current normalization at day 115 since October peak suggests stable 60-75bp daily ranges Outlook: Strong 80% probability volatility continues normalizing toward 50th percentile over next 10-14 days as major catalysts digested before March 18 RBA potentially reignites Trading Context: Normalizing volatility suggests 60-80bp daily ranges versus October's 100-150bp creating stable environment; breakouts above 0.7150 or below 0.7050 require sustained follow-through Vol Risk/Opportunity: Volatility compression from 72nd to 54th percentile reduces tail risk but March 18 RBA could trigger 100-150bp move within 48 hours if second hike delivered creating asymmetric opportunity ── PRIMARY RISK ───────────────────────────────── China PMI deterioration below 49.0 into deeper contraction threatening 30% of Australian export demand or Fed hawkish pause reversing easing cycle eliminating policy divergence advantage Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── RBA delivers second consecutive hike March-April to 4.10% while Fed continues measured easing creating 60-100bp policy inversion driving sustained rally toward 0.7250-0.7400 Timeframe: 4-8 weeks through March RBA meeting and Q1 CPI data as multi-hike cycle narrative gains momentum ── NEXT CATALYST ──────────────────────────────── Date: March 18, 2026 Event: RBA March Monetary Policy Decision - critical for validating whether February hike was one-off or start of multi-hike cycle Expected Impact: HIGH ── FULL ANALYSIS ──────────────────────────────── The Australian Dollar stands at a transformative inflection point trading at 0.7113 on March 1, 2026, following the most dramatic fundamental regime shift in years. Just 14 weeks ago on November 23, AUD traded at 0.6458 with markets pricing 80% probability of continued RBA easing. Today it trades 655 basis points higher after the stunning February 3 RBA decision to hike 25bp to 3.85%, marking the shortest easing cycle on record and completely reversing policy direction in response to Q4 CPI shocking at 3.9% versus consensus 3.5%. This creates unprecedented policy divergence: the Fed holds at 3.50-3.75% after January 28 decision with uncertain 2026 easing path, while the RBA not only halted easing but actively tightened, creating a 10-35bp differential favoring AUD that could expand to 60-85bp if divergence persists through H1 2026. However, critical crosscurrents persist. China's February manufacturing PMI deteriorated to 49.3 from January's 49.9, maintaining contraction territory and threatening Australia's largest trading partner accounting for 30% of exports. The February 23 COT report shows bulls expressing confidence with asset managers flipping to net-long exposure for first time since October at 1.7k contracts, while shorts declined to 40-week low. Technical structure shows consolidation at 14-month highs with strong moving average support across all timeframes and technical rating showing Strong Buy. March seasonality is historically neutral for AUD. The currency trades at approximately 73rd percentile of 1-year range, elevated but not at extremes. Volatility has normalized substantially from elevated 72nd percentile during October-November to current 54-56th percentile. The March 18 RBA meeting emerges as the critical near-term catalyst that will either validate the hawkish pivot with a second consecutive hike or signal pause, fundamentally determining whether this represents a sustained multi-hike cycle or one-off adjustment. Current positioning appears transitional as institutions shift from dovish consensus toward hawkish stance though not yet at extremes. The balance of probabilities favors continued consolidation with modest upside bias toward 0.7150-0.7250 over the next 2-4 weeks as markets position for the March RBA decision and await confirmation that inflation trajectory justifies the hawkish repricing embedded in current 0.7113 pricing. ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com)