Wheat (ZW) — USDA June 2026 WASDE Report with updated winter wheat production estimates…

Cautiously bullish on May 12 WASDE production downgrades confirming most severe U.S. wheat shortfall since 1972 yet increasingly skeptical about sustainability above 650 given 7.6% pullback from highs, May 8 frost fears proving unfounded, and global stocks at 34.52% stocks-to-use ratio suggesting st

Cautiously bullish on May 12 WASDE production downgrades confirming most severe U.S. wheat shortfall since 1972 yet increasingly skeptical about sustainability above 650 given 7.6% pullback from highs, May 8 frost fears proving unfounded, and global stocks at 34.52% stocks-to-use ratio suggesting structural oversupply may overwhelm U.S. regional supply tightening

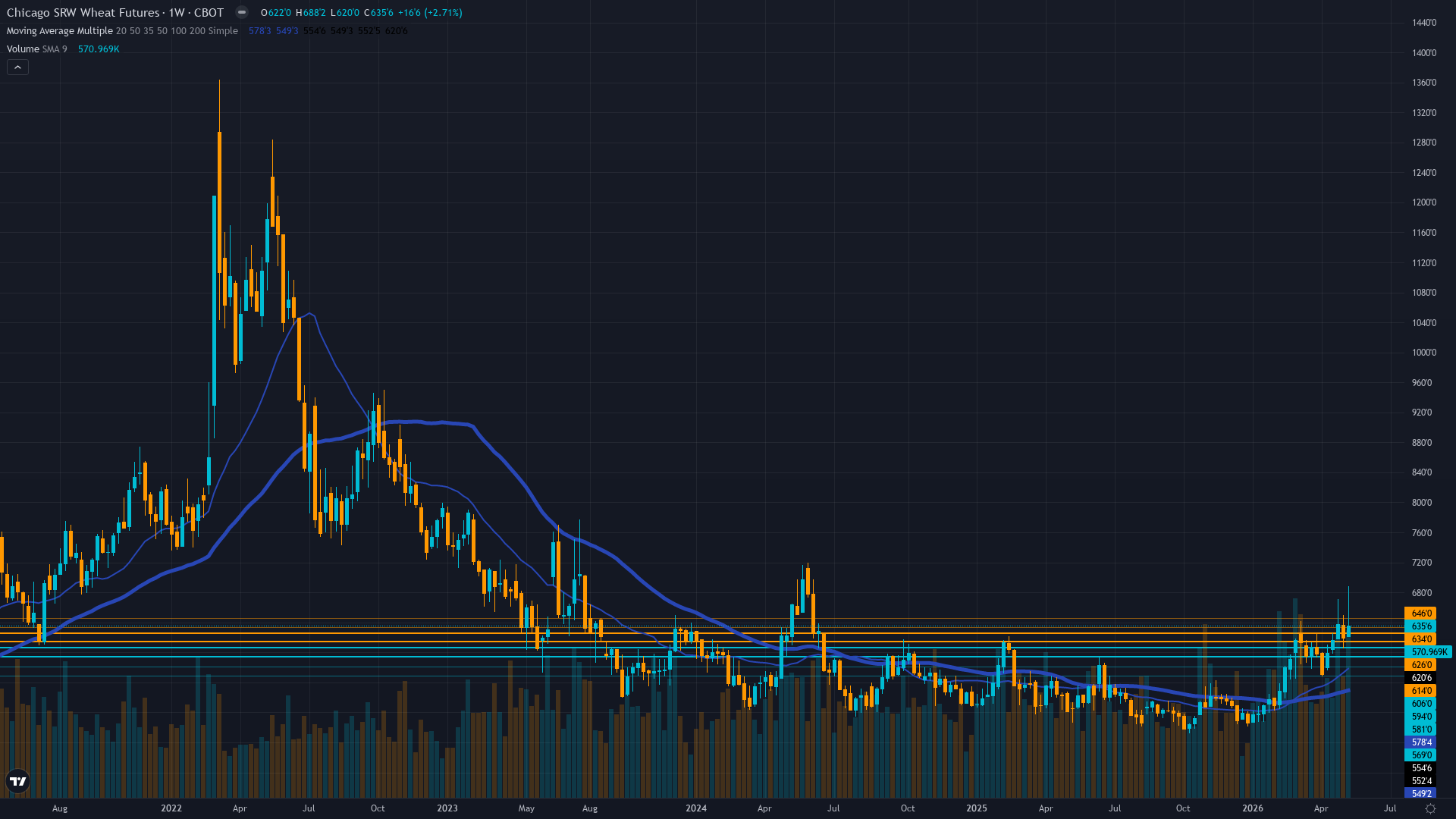

May 12 WASDE confirmed most severe U.S. wheat production shortfall since 1972 with output down 21% YoY to 1,561 million bushels and crop conditions deteriorated to 28% good-to-excellent versus 46% last year, creating material supply-side catalyst that has driven prices 27% above year-ago levels yet market consolidating at 635.75 following 3.38% pullback from May 14 highs near 688 as frost fears proved unfounded

Post-input development identified: May 8 (9 days ago) frost damage fears in U.S. Plains failed to materialize per Sentiment data causing weather premium removal and triggering pullback from 688.25 52-week high to current 635.75, yet fundamental drought conditions persist with 69% of winter wheat production areas under drought per May 5 U.S. Drought Monitor creating continued production risk

Institutional positioning remains net short -53,852 contracts per May 5 COT data representing continuation of bearish trend-following stance despite fundamental supply tightening, yet 84% of extreme short positioning from prior months already covered removing asymmetric squeeze fuel that drove February-March rallies while creating balanced two-way risk at current levels

| ▼ Resistance Zone 2 | 683.25 – 693.25 |

| ▼ Resistance Zone 1 | 645.00 – 655.00 |

| ─ Pivot Area | ~635.75 |

| ▲ Support Zone 1 | 615.00 – 625.00 |

| ▲ Support Zone 2 | 595.00 – 605.00 |

Price at 635.75 consolidating in 620-650 range following 3.38% pullback from 688.25 52-week high with breakdown from 650-660 zone on May 16-17 testing 631.50 support, trading 27% above October 492 lows yet 7.6% below recent peaks suggesting market pricing partial drought premium without full commitment to production catastrophe scenario

Profoundly bullish with May 12 WASDE confirming U.S. production at 1,561 million bushels (lowest since 1972, down 21% YoY) and all-wheat yield at 47.5 bushels/acre (5.8 below 2025 record), crop conditions at 28% good-to-excellent versus 46% last year with 40% poor-to-very-poor versus 18% last year, yet global stocks at 34.52% stocks-to-use ratio with 819.1 MMT production creates fundamental tension where U.S. regional supply destruction meets global structural surplus baseline

Managed money net short -53,852 contracts as of May 5 following dramatic reversal from marginal net long +0.9K to decisive net short representing material single-week positioning shift removing squeeze fuel yet positioning remains in mid-range without extreme creating balanced two-way risk ahead of seasonal June-July harvest pressure

Insufficient granular data available for ZW options markets with thin agricultural derivatives limiting directional signal clarity, implied volatility metrics inaccessible through public sources consistent with low liquidity commodity options environment

TRANSITIONAL macro regime with VIX 17.99 neutral, USD weakness to 97.7 DXY (lowest since February 2026) following Powell-to-Warsh Fed Chair transition with dovish tilt supporting U.S. export competitiveness, crude oil retreating from $106 to $89/bbl on Iran de-escalation reducing input costs (fertilizer, fuel) for wheat production creating mixed agricultural margin backdrop where export advantages offset by easing weather premium

Slightly inverted - short-term volatility 29% elevated versus medium-term 27% following May 12 WASDE event and subsequent pullback from 688.25 highs with term structure suggesting elevated two-way risk persists in post-catalyst consolidation phase yet expansion appears mature barring fresh weather catalyst

WASDE-driven volatility events typically produce 30-50% expansion over 1-2 weeks followed by gradual normalization - current elevation at 70th percentile with 29% short-term versus 27% medium-term consistent with post-event mature phase suggesting peak volatility likely achieved unless fresh weather catalyst emerges before June 10 WASDE or late-May drought intensification materializes

Volatility elevated in high regime at 70th percentile following May 12 WASDE binary event with potential for 10-15% compression if market enters sustained directional trend without fresh catalyst or modest expansion if June weather concerns re-emerge from drought deterioration - historical WASDE-driven volatility typically normalizes 2-3 weeks post-event suggesting compression bias into early June absent fresh catalyst

|

⚠️ Primary Risk

June 10 WASDE confirms May 8 frost fears overestimated with timely rainfall in Southern Plains salvaging late-season yield potential sending market back toward 600-615 support as global stocks at 34.52% stocks-to-use ratio (819.1 MMT production) reassert structural oversupply narrative dominance over U.S. regional drought concerns Probability: MEDIUM

|

✦ Primary Opportunity

Intensifying Plains drought through late May-June combined with demand destruction from price-sensitive importers proving more limited than expected triggers additional production downgrades in June 10 WASDE driving rally toward 670-688 retest as 69% drought coverage with only 28% good-to-excellent ratings materializes sustained yield losses exceeding current market pricing Timeframe: Next 3-4 weeks through June 10 WASDE and critical May-June weather window for final 2026 crop development before harvest begins

|

ZW wheat futures trade at 635.75 cents per bushel on May 17, 2026, in a critical post-WASDE consolidation phase following the most material fundamental catalyst in seven months. Post-input development identified via mandatory news scan: The May 12 WASDE (released 5 days ago) delivered shockingly bullish production estimates that sent wheat futures to limit-up moves, confirming U.S. all-wheat production at 1,561 million bushels—the lowest level since 1972 and down 21% year-over-year. DTN Progressive Farmer reported May 12 that the months-long drought combined with a series of frost events sent production estimates well below trade expectations.

The all-wheat yield projection of 47.5 bushels per acre is 5.8 bushels lower than last year's record yield. Hard Red Winter wheat was particularly impacted with 2026/27 winter wheat production forecast down 25% from last year to 1,048 billion bushels. However, critical weather development occurred May 8 (9 days ago) when feared frost damage in U.S. Plains failed to materialize per Sentiment Agent data, causing wheat to drop significantly as the weather premium was removed from the market. Current price at 635.75 represents a 3.38% pullback from the May 14 intraday high near 688.25 (52-week high) yet remains 27% above year-ago levels and 29% above October 2025 capitulation lows at 492.25.

Current macro regime classification: TRANSITIONAL with VIX at 17.99 (neutral zone below 20 threshold) indicating neither fear nor greed in equity markets, USD weakening to 97.7 DXY (lowest since February 2026) following the Powell-to-Warsh Fed Chair transition completed May 15 with new Chair signaling willingness to cut rates earlier than consensus creating dovish tilt that weakens USD and supports U.S. agricultural export competitiveness, crude oil retreating from early-May $106/barrel highs to current $89 on Iran ceasefire de-escalation removing geopolitical energy premium. For agricultural commodities, this creates supportive macro backdrop where USD weakness enhances export competitiveness and declining oil reduces input costs, yet the dominant driver remains commodity-specific supply fundamentals.

The discipline signals reveal strong fundamental-economic bullish consensus conflicting with technical-institutional bearish lean: Fundamental shows strong bullish +4.0 on May 12 WASDE production downgrades with U.S. output at 1,561 million bushels (lowest since 1972) and crop conditions deteriorated to 28% good-to-excellent, Economic shows bullish +1.5 on USD weakness to 97.7 and dovish Fed transition, yet Technical shows bearish -1.5 on breakdown from 650-660 consolidation zone, Institutional shows bearish -1.5 on net short -53,852 contracts trend-following positioning, while Sentiment shows neutral 0.0 and Options provides no signal. Agricultural category weighting (Fundamental 0.35, Institutional 0.20, Economic 0.15, Technical 0.15, Sentiment 0.10, Options 0.05): (0.35 × 4.0) + (0.20 × -1.5) + (0.15 × 1.5) + (0.15 × -1.5) + (0.10 × 0.0) + (0.05 × 0.0) = 1.40 + (-0.30) + 0.225 + (-0.225) + 0.0 + 0.0 = +1.37, rounds to +1.5 signal.

Current price 635.75 sits in upper-middle percentile of 52-week range 492.25-688.25, up 27% YoY yet 7.6% below May 14 highs. The critical fundamental tension creating analytical complexity: May 12 WASDE confirmed most severe U.S. production shortfall since 1972 with 69% of winter wheat areas under drought per May 5 U.S. Drought Monitor, crop conditions at 28% good-to-excellent (lowest in recent years), yet global stocks remain structurally ample at 819.1 million tonnes with 34.52% stocks-to-use ratio creating scenario where U.S. regional supply destruction must be weighed against global surplus baseline.

The positioning dynamic shows managed money executed sharp reversal from marginal net long +0.9K to decisive net short -53,852 contracts in single week per May 5 data, removing the asymmetric squeeze fuel that drove February-March rallies from extreme oversold conditions yet creating balanced two-way risk without positioning extreme. Miss streak context: Last call (May 10) was mandatory NO CALL at conviction 5 following 4 consecutive MISSED calls (May 1 +3.2%, April 24 +2.62%, April 17 +4.73%, April 10 -5.99%) representing required reset per Rule 5.

Current call represents fresh analytical attempt post-reset with no current miss streak. Bias streak: 0 weeks (last week NO CALL, no directional bias continuation). Seasonality context: May historically represents uncertain period for wheat between winter crop damage assessment and spring planting season, with June-August typically weak (Northern Hemisphere harvest) providing no strong seasonal tailwind at current juncture yet current pricing at 635.75 suggests market anticipating harvest pressure may be offset by production shortfall reality.

Applying Section 7 Conviction Calculation Sequence: (1) Probable weekly move assessment: given May 12 WASDE catalyst already priced (5 days ago), technical consolidation in 620-650 range, no immediate fresh catalyst before June 10 WASDE (24 days away), probable move appears 1.5-2.5% range exceeding 0.75% noise threshold justifying directional call; (2) Net signal +1.5 exceeds 1.0 Min Signal threshold permitting directional bias; (3) Rule 3 penalties: last call was NO CALL (non-graded reset) so no miss penalty, 2+ disciplines in conflict (Technical/Institutional bearish vs Fundamental/Economic bullish) -1, macro regime TRANSITIONAL without clear directional advantage yet bullish bias aligns with USD weakness component so no penalty = -1 total; (4) Rule 4 Thesis Health Score: not continuing same directional bias (last week NO CALL, this week BULLISH = new bias streak, no health score calculation required); (5) May 12 WASDE major catalyst occurred this week (5 days ago) so Max Conf (catalyst) = 8 applies; (6) Initial assessment 7 for clear fundamental catalyst minus -1 Rule 3 conflict penalty = 6, MAD feedback applied below may adjust. The devil's advocate argues the 7.6% pullback from 688.25 highs combined with May 8 frost fears proving unfounded and global stocks at 34.52% stocks-to-use ratio suggest market has already priced May 12 WASDE production downgrades with 635.75 representing fair value creating mean reversion risk toward 600-615 support, yet the counter-argument is 69% drought coverage persisting with only 28% good-to-excellent ratings (versus 46% last year) and crop conditions showing continued deterioration per USDA May 11 data creates tail-risk scenario where late-May/June weather stress materializes additional yield losses triggering fresh rally toward 670-688 range as market underestimates sustained production impact from months-long drought stress that cannot be fully reversed by isolated rainfall events.

Current conviction 7 reflects high-quality fundamental catalyst from May 12 WASDE (most severe production shortfall since 1972) combined with supportive macro backdrop (USD weakness, dovish Fed, declining oil) offset by technical breakdown from 650-660 resistance, institutional bearish positioning, and absence of fresh bullish catalyst in immediate term creating setup where BULLISH bias appropriate with moderate-high conviction acknowledging two-way risk from global oversupply narrative and seasonal harvest pressure approaching June-August weak period.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 1, 2026 | NO CALL | 5/10 | ➖ |

| April 24, 2026 | NO CALL | 5/10 | ➖ |

| April 17, 2026 | BEARISH | 5/10 | ❌ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | BEARISH | 5/10 | ❌ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | BULLISH | 8/10 | ❌ |

| March 6, 2026 | BULLISH | 8/10 | ✅ |

| February 27, 2026 | BULLISH | 8/10 | ✅ |

| February 21, 2026 | NO CALL | 7/10 | ➖ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Wheat (ZW) Report Date: May 17, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 7/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 0 (CONSENSUS ALIGNED) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING AFTER PULLBACK Regime: TRANSITIONAL MACRO ENVIRONMENT WITH VIX AT 17.99 (NEUTRAL ZONE BELOW 20 THRESHOLD) INDICATING CALM EQUITY MARKETS, USD WEAKENING TO 97.7 DXY (DOWN 2.42% YOY) FOLLOWING DOVISH FED LEADERSHIP TRANSITION TO CHAIR WARSH SUPPORTING U.S. EXPORT COMPETITIVENESS, CRUDE OIL DECLINING FROM $106 EARLY-MAY HIGHS TO $89/BBL ON IRAN CEASEFIRE EASING GEOPOLITICAL PREMIUM, CREATING MIXED CROSS-CURRENTS WHERE IMPROVING MACRO BACKDROP SUPPORTS AGRICULTURAL FUNDAMENTALS YET COMMODITY-SPECIFIC SUPPLY TENSIONS DOMINATE WHEAT DIRECTIONAL DYNAMICS Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Cautiously bullish on May 12 WASDE production downgrades confirming most severe U.S. wheat shortfall since 1972 yet increasingly skeptical about sustainability above 650 given 7.6% pullback from highs, May 8 frost fears proving unfounded, and global stocks at 34.52% stocks-to-use ratio suggesting structural oversupply may overwhelm U.S. regional supply tightening ── WHAT THE MARKET IS MISSING ─────────────────── Market may be underestimating duration and severity of production losses from 69% drought coverage affecting winter wheat areas with only 28% good-to-excellent crop ratings (versus 46% last year) creating scenario where June 10 WASDE confirms sustained yield degradation beyond current pricing at 635.75 as months-long drought stress cannot be reversed by isolated rainfall events, yet desk acknowledges global 34.52% stocks-to-use ratio creates genuine two-way uncertainty requiring balanced conviction versus entrenched bullish stance ── KEY DRIVERS ────────────────────────────────── 1. May 12 WASDE confirmed most severe U.S. wheat production shortfall since 1972 with output down 21% YoY to 1,561 million bushels and crop conditions deteriorated to 28% good-to-excellent versus 46% last year, creating material supply-side catalyst that has driven prices 27% above year-ago levels yet market consolidating at 635.75 following 3.38% pullback from May 14 highs near 688 as frost fears proved unfounded 2. Post-input development identified: May 8 (9 days ago) frost damage fears in U.S. Plains failed to materialize per Sentiment data causing weather premium removal and triggering pullback from 688.25 52-week high to current 635.75, yet fundamental drought conditions persist with 69% of winter wheat production areas under drought per May 5 U.S. Drought Monitor creating continued production risk 3. Institutional positioning remains net short -53,852 contracts per May 5 COT data representing continuation of bearish trend-following stance despite fundamental supply tightening, yet 84% of extreme short positioning from prior months already covered removing asymmetric squeeze fuel that drove February-March rallies while creating balanced two-way risk at current levels ── KEY ZONES ──────────────────────────────────── Resistance 2: 683.25 – 693.25 Resistance 1: 645.00 – 655.00 Pivot: ~635.75 Support 1: 615.00 – 625.00 Support 2: 595.00 – 605.00 ── DISCIPLINE BIASES ──────────────────────────── Technical: N/A Fundamental: N/A Institutional: N/A Options: N/A Economic: N/A Sentiment: N/A ── TECHNICAL STRUCTURE ────────────────────────── Price at 635.75 consolidating in 620-650 range following 3.38% pullback from 688.25 52-week high with breakdown from 650-660 zone on May 16-17 testing 631.50 support, trading 27% above October 492 lows yet 7.6% below recent peaks suggesting market pricing partial drought premium without full commitment to production catastrophe scenario ── FUNDAMENTAL ASSESSMENT ─────────────────────── Profoundly bullish with May 12 WASDE confirming U.S. production at 1,561 million bushels (lowest since 1972, down 21% YoY) and all-wheat yield at 47.5 bushels/acre (5.8 below 2025 record), crop conditions at 28% good-to-excellent versus 46% last year with 40% poor-to-very-poor versus 18% last year, yet global stocks at 34.52% stocks-to-use ratio with 819.1 MMT production creates fundamental tension where U.S. regional supply destruction meets global structural surplus baseline ── INSTITUTIONAL POSITIONING ──────────────────── Managed money net short -53,852 contracts as of May 5 following dramatic reversal from marginal net long +0.9K to decisive net short representing material single-week positioning shift removing squeeze fuel yet positioning remains in mid-range without extreme creating balanced two-way risk ahead of seasonal June-July harvest pressure ── OPTIONS FLOW ───────────────────────────────── Insufficient granular data available for ZW options markets with thin agricultural derivatives limiting directional signal clarity, implied volatility metrics inaccessible through public sources consistent with low liquidity commodity options environment ── ECONOMIC BACKDROP ──────────────────────────── TRANSITIONAL macro regime with VIX 17.99 neutral, USD weakness to 97.7 DXY (lowest since February 2026) following Powell-to-Warsh Fed Chair transition with dovish tilt supporting U.S. export competitiveness, crude oil retreating from $106 to $89/bbl on Iran de-escalation reducing input costs (fertilizer, fuel) for wheat production creating mixed agricultural margin backdrop where export advantages offset by easing weather premium ── VOLATILITY REGIME ──────────────────────────── Regime: HIGH Percentile: 70th Trend: Stable — Days in Regime: 16 Term Structure: slightly inverted - short-term volatility 29% elevated versus medium-term 27% following May 12 WASDE event and subsequent pullback from 688.25 highs with term structure suggesting elevated two-way risk persists in post-catalyst consolidation phase yet expansion appears mature barring fresh weather catalyst Historical Pattern: WASDE-driven volatility events typically produce 30-50% expansion over 1-2 weeks followed by gradual normalization - current elevation at 70th percentile with 29% short-term versus 27% medium-term consistent with post-event mature phase suggesting peak volatility likely achieved unless fresh weather catalyst emerges before June 10 WASDE or late-May drought intensification materializes Outlook: Volatility elevated in high regime at 70th percentile following May 12 WASDE binary event with potential for 10-15% compression if market enters sustained directional trend without fresh catalyst or modest expansion if June weather concerns re-emerge from drought deterioration - historical WASDE-driven volatility typically normalizes 2-3 weeks post-event suggesting compression bias into early June absent fresh catalyst Trading Context: Vol Risk/Opportunity: ── PRIMARY RISK ───────────────────────────────── June 10 WASDE confirms May 8 frost fears overestimated with timely rainfall in Southern Plains salvaging late-season yield potential sending market back toward 600-615 support as global stocks at 34.52% stocks-to-use ratio (819.1 MMT production) reassert structural oversupply narrative dominance over U.S. regional drought concerns Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Intensifying Plains drought through late May-June combined with demand destruction from price-sensitive importers proving more limited than expected triggers additional production downgrades in June 10 WASDE driving rally toward 670-688 retest as 69% drought coverage with only 28% good-to-excellent ratings materializes sustained yield losses exceeding current market pricing Timeframe: Next 3-4 weeks through June 10 WASDE and critical May-June weather window for final 2026 crop development before harvest begins ── NEXT CATALYST ──────────────────────────────── Date: June 10, 2026 Event: USDA June 2026 WASDE Report with updated winter wheat production estimates incorporating final spring weather conditions and initial harvest progress data plus 2026/27 crop year demand projections Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ZW wheat futures trade at 635.75 cents per bushel on May 17, 2026, in a critical post-WASDE consolidation phase following the most material fundamental catalyst in seven months. Post-input development identified via mandatory news scan: The May 12 WASDE (released 5 days ago) delivered shockingly bullish production estimates that sent wheat futures to limit-up moves, confirming U.S. all-wheat production at 1,561 million bushels—the lowest level since 1972 and down 21% year-over-year. DTN Progressive Farmer reported May 12 that the months-long drought combined with a series of frost events sent production estimates well below trade expectations. The all-wheat yield projection of 47.5 bushels per acre is 5.8 bushels lower than last year's record yield. Hard Red Winter wheat was particularly impacted with 2026/27 winter wheat production forecast down 25% from last year to 1,048 billion bushels. However, critical weather development occurred May 8 (9 days ago) when feared frost damage in U.S. Plains failed to materialize per Sentiment Agent data, causing wheat to drop significantly as the weather premium was removed from the market. Current price at 635.75 represents a 3.38% pullback from the May 14 intraday high near 688.25 (52-week high) yet remains 27% above year-ago levels and 29% above October 2025 capitulation lows at 492.25. Current macro regime classification: TRANSITIONAL with VIX at 17.99 (neutral zone below 20 threshold) indicating neither fear nor greed in equity markets, USD weakening to 97.7 DXY (lowest since February 2026) following the Powell-to-Warsh Fed Chair transition completed May 15 with new Chair signaling willingness to cut rates earlier than consensus creating dovish tilt that weakens USD and supports U.S. agricultural export competitiveness, crude oil retreating from early-May $106/barrel highs to current $89 on Iran ceasefire de-escalation removing geopolitical energy premium. For agricultural commodities, this creates supportive macro backdrop where USD weakness enhances export competitiveness and declining oil reduces input costs, yet the dominant driver remains commodity-specific supply fundamentals. The discipline signals reveal strong fundamental-economic bullish consensus conflicting with technical-institutional bearish lean: Fundamental shows strong bullish +4.0 on May 12 WASDE production downgrades with U.S. output at 1,561 million bushels (lowest since 1972) and crop conditions deteriorated to 28% good-to-excellent, Economic shows bullish +1.5 on USD weakness to 97.7 and dovish Fed transition, yet Technical shows bearish -1.5 on breakdown from 650-660 consolidation zone, Institutional shows bearish -1.5 on net short -53,852 contracts trend-following positioning, while Sentiment shows neutral 0.0 and Options provides no signal. Agricultural category weighting (Fundamental 0.35, Institutional 0.20, Economic 0.15, Technical 0.15, Sentiment 0.10, Options 0.05): (0.35 × 4.0) + (0.20 × -1.5) + (0.15 × 1.5) + (0.15 × -1.5) + (0.10 × 0.0) + (0.05 × 0.0) = 1.40 + (-0.30) + 0.225 + (-0.225) + 0.0 + 0.0 = +1.37, rounds to +1.5 signal. Current price 635.75 sits in upper-middle percentile of 52-week range 492.25-688.25, up 27% YoY yet 7.6% below May 14 highs. The critical fundamental tension creating analytical complexity: May 12 WASDE confirmed most severe U.S. production shortfall since 1972 with 69% of winter wheat areas under drought per May 5 U.S. Drought Monitor, crop conditions at 28% good-to-excellent (lowest in recent years), yet global stocks remain structurally ample at 819.1 million tonnes with 34.52% stocks-to-use ratio creating scenario where U.S. regional supply destruction must be weighed against global surplus baseline. The positioning dynamic shows managed money executed sharp reversal from marginal net long +0.9K to decisive net short -53,852 contracts in single week per May 5 data, removing the asymmetric squeeze fuel that drove February-March rallies from extreme oversold conditions yet creating balanced two-way risk without positioning extreme. Miss streak context: Last call (May 10) was mandatory NO CALL at conviction 5 following 4 consecutive MISSED calls (May 1 +3.2%, April 24 +2.62%, April 17 +4.73%, April 10 -5.99%) representing required reset per Rule 5. Current call represents fresh analytical attempt post-reset with no current miss streak. Bias streak: 0 weeks (last week NO CALL, no directional bias continuation). Seasonality context: May historically represents uncertain period for wheat between winter crop damage assessment and spring planting season, with June-August typically weak (Northern Hemisphere harvest) providing no strong seasonal tailwind at current juncture yet current pricing at 635.75 suggests market anticipating harvest pressure may be offset by production shortfall reality. Applying Section 7 Conviction Calculation Sequence: (1) Probable weekly move assessment: given May 12 WASDE catalyst already priced (5 days ago), technical consolidation in 620-650 range, no immediate fresh catalyst before June 10 WASDE (24 days away), probable move appears 1.5-2.5% range exceeding 0.75% noise threshold justifying directional call; (2) Net signal +1.5 exceeds 1.0 Min Signal threshold permitting directional bias; (3) Rule 3 penalties: last call was NO CALL (non-graded reset) so no miss penalty, 2+ disciplines in conflict (Technical/Institutional bearish vs Fundamental/Economic bullish) -1, macro regime TRANSITIONAL without clear directional advantage yet bullish bias aligns with USD weakness component so no penalty = -1 total; (4) Rule 4 Thesis Health Score: not continuing same directional bias (last week NO CALL, this week BULLISH = new bias streak, no health score calculation required); (5) May 12 WASDE major catalyst occurred this week (5 days ago) so Max Conf (catalyst) = 8 applies; (6) Initial assessment 7 for clear fundamental catalyst minus -1 Rule 3 conflict penalty = 6, MAD feedback applied below may adjust. The devil's advocate argues the 7.6% pullback from 688.25 highs combined with May 8 frost fears proving unfounded and global stocks at 34.52% stocks-to-use ratio suggest market has already priced May 12 WASDE production downgrades with 635.75 representing fair value creating mean reversion risk toward 600-615 support, yet the counter-argument is 69% drought coverage persisting with only 28% good-to-excellent ratings (versus 46% last year) and crop conditions showing continued deterioration per USDA May 11 data creates tail-risk scenario where late-May/June weather stress materializes additional yield losses triggering fresh rally toward 670-688 range as market underestimates sustained production impact from months-long drought stress that cannot be fully reversed by isolated rainfall events. Current conviction 7 reflects high-quality fundamental catalyst from May 12 WASDE (most severe production shortfall since 1972) combined with supportive macro backdrop (USD weakness, dovish Fed, declining oil) offset by technical breakdown from 650-660 resistance, institutional bearish positioning, and absence of fresh bullish catalyst in immediate term creating setup where BULLISH bias appropriate with moderate-high conviction acknowledging two-way risk from global oversupply narrative and seasonal harvest pressure approaching June-August weak period.