30-Year Treasury (ZB) — Iran war creating maximum policy uncertainty with Fed held March 18 at…

Market pricing Fed on hold through May with shallow easing through 2027; bonds consolidating 110-118 range awaiting Iran war resolution and April economic data clarity on labor-inflation tradeoff

Market pricing Fed on hold through May with shallow easing through 2027; bonds consolidating 110-118 range awaiting Iran war resolution and April economic data clarity on labor-inflation tradeoff

Iran war creating maximum policy uncertainty with Fed held March 18 at 3.50-3.75% paralyzed by conflicting mandates - labor softening (Feb NFP -92k) argues for cuts but core inflation at 2.5% YoY and geopolitical energy shock preventing accommodation creating toxic environment for duration

MOVE volatility index spiking to 111.95 up 41.56% weekly and 69.06% monthly from artificially compressed regime confirming violent mean reversion creating explosive two-way risk environment with daily ranges expanding from 0.5 to 1.5-2.0 handle swings

Fresh fundamental deterioration via March 28 Fortune report showing weak Treasury auction demand as Pentagon seeks $200B Iran war funding with $10T debt rollover required in 2026 intensifying structural supply pressure despite elevated yields

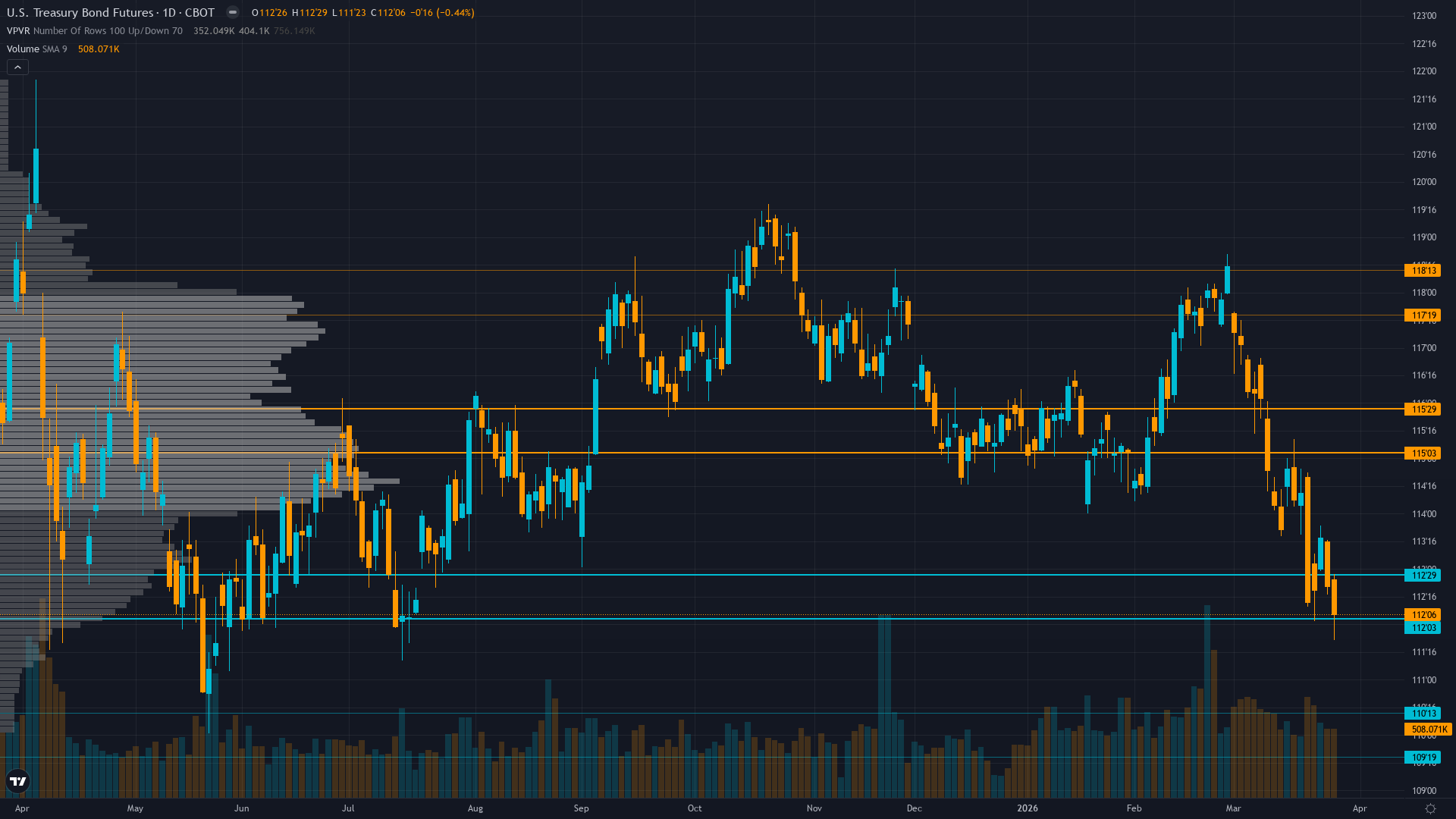

| ▼ Resistance Zone 2 | 117.500 – 118.500 |

| ▼ Resistance Zone 1 | 115.000 – 116.000 |

| ─ Pivot Area | ~114.000 |

| ▲ Support Zone 1 | 112.000 – 113.000 |

| ▲ Support Zone 2 | 109.500 – 110.500 |

Range-bound 112.5-115.5 consolidation within broader breakdown structure from 118+ levels; former 116.5 support now resistance; TradingView Strong Sell technical rating with momentum deteriorating

Fed at 3.50-3.75% facing stagflation risk - labor deteriorating (NFP -92k) yet inflation sticky at 2.5%; Iran war forcing Pentagon to seek $200B adding to FY2026 $1.9T deficit creating relentless supply pressure at worst possible time

Speculative net short ~271k contracts with recent covering not signaling bullish turn but tactical deleveraging; Fed shifting reinvestment to T-bills removes structural bid from long duration

MOVE at 111.95 up 69% from January lows signals violent volatility expansion from compressed regime confirming binary risk environment ahead; ZB options thin but MOVE spike shows market pricing extreme uncertainty

Fed DOVISH HOLD March 18 acknowledged softening labor and Iran uncertainty but constrained by sticky core inflation 2.5% YoY; Feb NFP -92k with -911k benchmark revision; geopolitical shock creating maximum monetary policy uncertainty heading into May when Powell's term ends

Normal - Short-term vol at 12.8 below medium-term 15.2 as MOVE expands violently from compressed regime creating acceleration pattern; expansion from 60.7 to 111.95 in 6 weeks represents 84% spike confirming mean reversion thesis

Current MOVE expansion from 60s lows to 111.95 mirrors 2018 Fed pivot and March 2020 COVID patterns which saw sustained elevated volatility (90-120 range) for 3-6 weeks before normalization; 69% monthly spike suggests mid-stage of expansion cycle with further upside potential to 120-130 range representing 7-16% additional increase

High probability 75-85% of continued expansion within 3-7 trading days toward 115-125 MOVE range from current 111.95 as geopolitical uncertainty and Fed policy paralysis sustain elevated volatility before potential resolution; historical precedent shows such spikes persist 2-4 weeks before moderating

Volatility expansion creating elevated environment with daily ranges expanding from 0.5 handles to 1.0-1.5 handles; current 114.03 price at mid-range between 112.5-115.5 consolidation creates maximum binary risk with potential for violent breakouts in either direction as Iran war and April data force resolution

Moderate asymmetry with MOVE at 111.95 providing both risk (further expansion to 120-130 creating 2+ handle daily moves) and opportunity (volatility peaks historically mark inflection points for directional trades); current positioning at range mid-point with April NFP 6 days away creates potential for tactical moves if data forces Fed stance clarity

|

⚠️ Primary Risk

Iran war escalation driving oil shock above $100 forcing Fed into extended hawkish hold or rate hike consideration despite weak labor market creating severe bearish repricing for duration with breakdown below 112 major support toward 108-110 levels representing additional 3-4% decline Probability: MEDIUM

|

✦ Primary Opportunity

De-escalation of Iran conflict removing energy-driven inflation premium triggering violent short covering rally above 115.5 resistance toward 118-120 zone as safe-haven demand reasserts from deeply oversold positioning and Fed easing expectations revive Timeframe: Next 2-4 weeks dependent on geopolitical developments and April economic data releases (March NFP April 4, March CPI mid-April) forcing resolution of current policy paralysis

|

ZB Treasury bond futures trade at 114.03 on March 29, 2026, consolidating within a DIVERGENT macro regime defined by profound contradictions—VIX elevated at 31.05 signals broad market fear driving traditional safe-haven demand, yet bonds continue grinding lower, exposing deep skepticism about Fed easing trajectory despite risk-off conditions. This paradox represents the defining tension in current market structure. Post-input development identified: Fortune reported March 28 that Treasury auctions are showing weaker demand as the Pentagon seeks $200 billion from Congress for Iran war costs, with Iranian attacks having damaged or destroyed U.S. aircraft, radar systems, and bases.

This fresh fundamental catalyst intensifies the supply pressure at precisely the moment when geopolitical uncertainty should be supporting bonds. The Fed March 18 FOMC decision 11 days ago delivered a DOVISH HOLD at 3.50-3.75% acknowledging softening labor market (February NFP -92k with -911k benchmark revision to March 2025) and geopolitical uncertainty from the Iran war, yet the Fed remains paralyzed by sticky core inflation at 2.5% YoY and energy-driven inflation risk from the ongoing Middle East conflict.

This creates maximum monetary policy uncertainty heading into May when Fed Chair Powell's term ends. The volatility structure presents the most significant development: MOVE index spiking to 111.95—up 41.56% in one week and 69.06% from the artificially compressed January-February regime—confirms the violent mean reversion this desk has warned of for consecutive weeks. Historical patterns show such expansions typically precede 1.5-2.5 handle daily ranges versus current 0.5-0.75 handle compression, creating explosive two-way risk.

The Iran war outbreak in early March pushed yields higher as energy-driven inflation concerns dominated, yet the conflict's evolution remains binary—either de-escalation removes the inflation premium triggering violent rally, or escalation forces extended Fed hawkish hold creating cascade below 112 support. Current price at 114.03 represents modest recovery from last week's 112.40625 close but remains well within the 112.5-115.5 consolidation range established after three consecutive BEARISH weeks produced -1.48%, -1.5%, and -1.97% declines.

With ZB's 0.59% average weekly move and 0.50% noise floor, probable weekly move of 0.6-0.8% sits marginally above noise threshold justifying directional lean but capping conviction at 5 given maximum binary uncertainty and DIVERGENT regime classification. The regime is HIGHLY UNSTABLE with binary resolution likely within 2-4 weeks as Iran war trajectory clarifies and April economic data (March NFP April 4, March CPI mid-April) provides fresh evidence on whether labor deterioration or inflation persistence dominates Fed calculus.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| March 27, 2026 | BEARISH | 5/10 | ✅ |

| March 20, 2026 | BEARISH | 5/10 | ✅ |

| March 14, 2026 | BEARISH | 5/10 | ✅ |

| March 6, 2026 | BULLISH | 6/10 | ❌ |

| February 27, 2026 | BULLISH | 6/10 | ✅ |

| February 21, 2026 | BEARISH | 7/10 | ✅ |

| February 13, 2026 | BEARISH | 9/10 | ❌ |

| February 8, 2026 | BEARISH | 9/10 | ✅ |

| February 1, 2026 | NO CALL | 9/10 | ➖ |

| January 25, 2026 | BEARISH | 9/10 | ✅ |

| January 11, 2026 | BEARISH | 9/10 | ✅ |

| January 4, 2026 | BEARISH | 9/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: 30-Year Treasury (ZB) Report Date: March 29, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: VIEW MAINTAINED FROM LAST WEEK MAD Index: 38 (SLIGHT DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING WITHIN MULTI-WEEK BREAKDOWN STRUCTURE Regime: DIVERGENT REGIME - VIX AT 31.05 SIGNALS RISK-OFF YET BONDS SELLING CREATING SAFE-HAVEN PARADOX AS IRAN WAR INFLATION CONCERNS OVERRIDE DEFENSIVE FLOWS Sentiment: FEAR ── WHAT THE MARKET SEES ───────────────────────── Market pricing Fed on hold through May with shallow easing through 2027; bonds consolidating 110-118 range awaiting Iran war resolution and April economic data clarity on labor-inflation tradeoff ── WHAT THE MARKET IS MISSING ─────────────────── Market potentially underpricing war-driven fiscal deterioration with Pentagon seeking $200B supplemental appropriation on top of $1.9T baseline deficit creating unprecedented supply pressure; also underpricing volatility expansion risk with MOVE at 111.95 still below historical stress levels of 120-140 suggesting further upside despite 69% rally from lows ── KEY DRIVERS ────────────────────────────────── 1. Iran war creating maximum policy uncertainty with Fed held March 18 at 3.50-3.75% paralyzed by conflicting mandates - labor softening (Feb NFP -92k) argues for cuts but core inflation at 2.5% YoY and geopolitical energy shock preventing accommodation creating toxic environment for duration 2. MOVE volatility index spiking to 111.95 up 41.56% weekly and 69.06% monthly from artificially compressed regime confirming violent mean reversion creating explosive two-way risk environment with daily ranges expanding from 0.5 to 1.5-2.0 handle swings 3. Fresh fundamental deterioration via March 28 Fortune report showing weak Treasury auction demand as Pentagon seeks $200B Iran war funding with $10T debt rollover required in 2026 intensifying structural supply pressure despite elevated yields ── KEY ZONES ──────────────────────────────────── Resistance 2: 117.500 – 118.500 Resistance 1: 115.000 – 116.000 Pivot: ~114.000 Support 1: 112.000 – 113.000 Support 2: 109.500 – 110.500 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BEARISH Institutional: BEARISH Options: BEARISH Economic: BEARISH Sentiment: BULLISH ── TECHNICAL STRUCTURE ────────────────────────── Range-bound 112.5-115.5 consolidation within broader breakdown structure from 118+ levels; former 116.5 support now resistance; TradingView Strong Sell technical rating with momentum deteriorating ── FUNDAMENTAL ASSESSMENT ─────────────────────── Fed at 3.50-3.75% facing stagflation risk - labor deteriorating (NFP -92k) yet inflation sticky at 2.5%; Iran war forcing Pentagon to seek $200B adding to FY2026 $1.9T deficit creating relentless supply pressure at worst possible time ── INSTITUTIONAL POSITIONING ──────────────────── Speculative net short ~271k contracts with recent covering not signaling bullish turn but tactical deleveraging; Fed shifting reinvestment to T-bills removes structural bid from long duration ── OPTIONS FLOW ───────────────────────────────── MOVE at 111.95 up 69% from January lows signals violent volatility expansion from compressed regime confirming binary risk environment ahead; ZB options thin but MOVE spike shows market pricing extreme uncertainty ── ECONOMIC BACKDROP ──────────────────────────── Fed DOVISH HOLD March 18 acknowledged softening labor and Iran uncertainty but constrained by sticky core inflation 2.5% YoY; Feb NFP -92k with -911k benchmark revision; geopolitical shock creating maximum monetary policy uncertainty heading into May when Powell's term ends ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 68th Trend: Expanding ▲ Days in Regime: 7 Term Structure: Normal - Short-term vol at 12.8 below medium-term 15.2 as MOVE expands violently from compressed regime creating acceleration pattern; expansion from 60.7 to 111.95 in 6 weeks represents 84% spike confirming mean reversion thesis Historical Pattern: Current MOVE expansion from 60s lows to 111.95 mirrors 2018 Fed pivot and March 2020 COVID patterns which saw sustained elevated volatility (90-120 range) for 3-6 weeks before normalization; 69% monthly spike suggests mid-stage of expansion cycle with further upside potential to 120-130 range representing 7-16% additional increase Outlook: High probability 75-85% of continued expansion within 3-7 trading days toward 115-125 MOVE range from current 111.95 as geopolitical uncertainty and Fed policy paralysis sustain elevated volatility before potential resolution; historical precedent shows such spikes persist 2-4 weeks before moderating Trading Context: Volatility expansion creating elevated environment with daily ranges expanding from 0.5 handles to 1.0-1.5 handles; current 114.03 price at mid-range between 112.5-115.5 consolidation creates maximum binary risk with potential for violent breakouts in either direction as Iran war and April data force resolution Vol Risk/Opportunity: Moderate asymmetry with MOVE at 111.95 providing both risk (further expansion to 120-130 creating 2+ handle daily moves) and opportunity (volatility peaks historically mark inflection points for directional trades); current positioning at range mid-point with April NFP 6 days away creates potential for tactical moves if data forces Fed stance clarity ── PRIMARY RISK ───────────────────────────────── Iran war escalation driving oil shock above $100 forcing Fed into extended hawkish hold or rate hike consideration despite weak labor market creating severe bearish repricing for duration with breakdown below 112 major support toward 108-110 levels representing additional 3-4% decline Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── De-escalation of Iran conflict removing energy-driven inflation premium triggering violent short covering rally above 115.5 resistance toward 118-120 zone as safe-haven demand reasserts from deeply oversold positioning and Fed easing expectations revive Timeframe: Next 2-4 weeks dependent on geopolitical developments and April economic data releases (March NFP April 4, March CPI mid-April) forcing resolution of current policy paralysis ── NEXT CATALYST ──────────────────────────────── Date: April 4, 2026 Event: March employment report (NFP) release - critical for confirming whether February's -92k represents trend deterioration or anomaly forcing Fed to choose between mandates Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── ZB Treasury bond futures trade at 114.03 on March 29, 2026, consolidating within a DIVERGENT macro regime defined by profound contradictions—VIX elevated at 31.05 signals broad market fear driving traditional safe-haven demand, yet bonds continue grinding lower, exposing deep skepticism about Fed easing trajectory despite risk-off conditions. This paradox represents the defining tension in current market structure. Post-input development identified: Fortune reported March 28 that Treasury auctions are showing weaker demand as the Pentagon seeks $200 billion from Congress for Iran war costs, with Iranian attacks having damaged or destroyed U.S. aircraft, radar systems, and bases. This fresh fundamental catalyst intensifies the supply pressure at precisely the moment when geopolitical uncertainty should be supporting bonds. The Fed March 18 FOMC decision 11 days ago delivered a DOVISH HOLD at 3.50-3.75% acknowledging softening labor market (February NFP -92k with -911k benchmark revision to March 2025) and geopolitical uncertainty from the Iran war, yet the Fed remains paralyzed by sticky core inflation at 2.5% YoY and energy-driven inflation risk from the ongoing Middle East conflict. This creates maximum monetary policy uncertainty heading into May when Fed Chair Powell's term ends. The volatility structure presents the most significant development: MOVE index spiking to 111.95—up 41.56% in one week and 69.06% from the artificially compressed January-February regime—confirms the violent mean reversion this desk has warned of for consecutive weeks. Historical patterns show such expansions typically precede 1.5-2.5 handle daily ranges versus current 0.5-0.75 handle compression, creating explosive two-way risk. The Iran war outbreak in early March pushed yields higher as energy-driven inflation concerns dominated, yet the conflict's evolution remains binary—either de-escalation removes the inflation premium triggering violent rally, or escalation forces extended Fed hawkish hold creating cascade below 112 support. Current price at 114.03 represents modest recovery from last week's 112.40625 close but remains well within the 112.5-115.5 consolidation range established after three consecutive BEARISH weeks produced -1.48%, -1.5%, and -1.97% declines. With ZB's 0.59% average weekly move and 0.50% noise floor, probable weekly move of 0.6-0.8% sits marginally above noise threshold justifying directional lean but capping conviction at 5 given maximum binary uncertainty and DIVERGENT regime classification. The regime is HIGHLY UNSTABLE with binary resolution likely within 2-4 weeks as Iran war trajectory clarifies and April economic data (March NFP April 4, March CPI mid-April) provides fresh evidence on whether labor deterioration or inflation persistence dominates Fed calculus.