Nasdaq 100 (NQ) — April CPI reacceleration to 3.4% YoY (released May 13) shifting Fed…

Cautiously constructive acknowledging Q1 earnings strength but increasingly defensive on April CPI reacceleration removing Fed dovish support, with strategists pushing rate cut expectations from June to September or later as higher-for-longer narrative reasserts

Cautiously constructive acknowledging Q1 earnings strength but increasingly defensive on April CPI reacceleration removing Fed dovish support, with strategists pushing rate cut expectations from June to September or later as higher-for-longer narrative reasserts

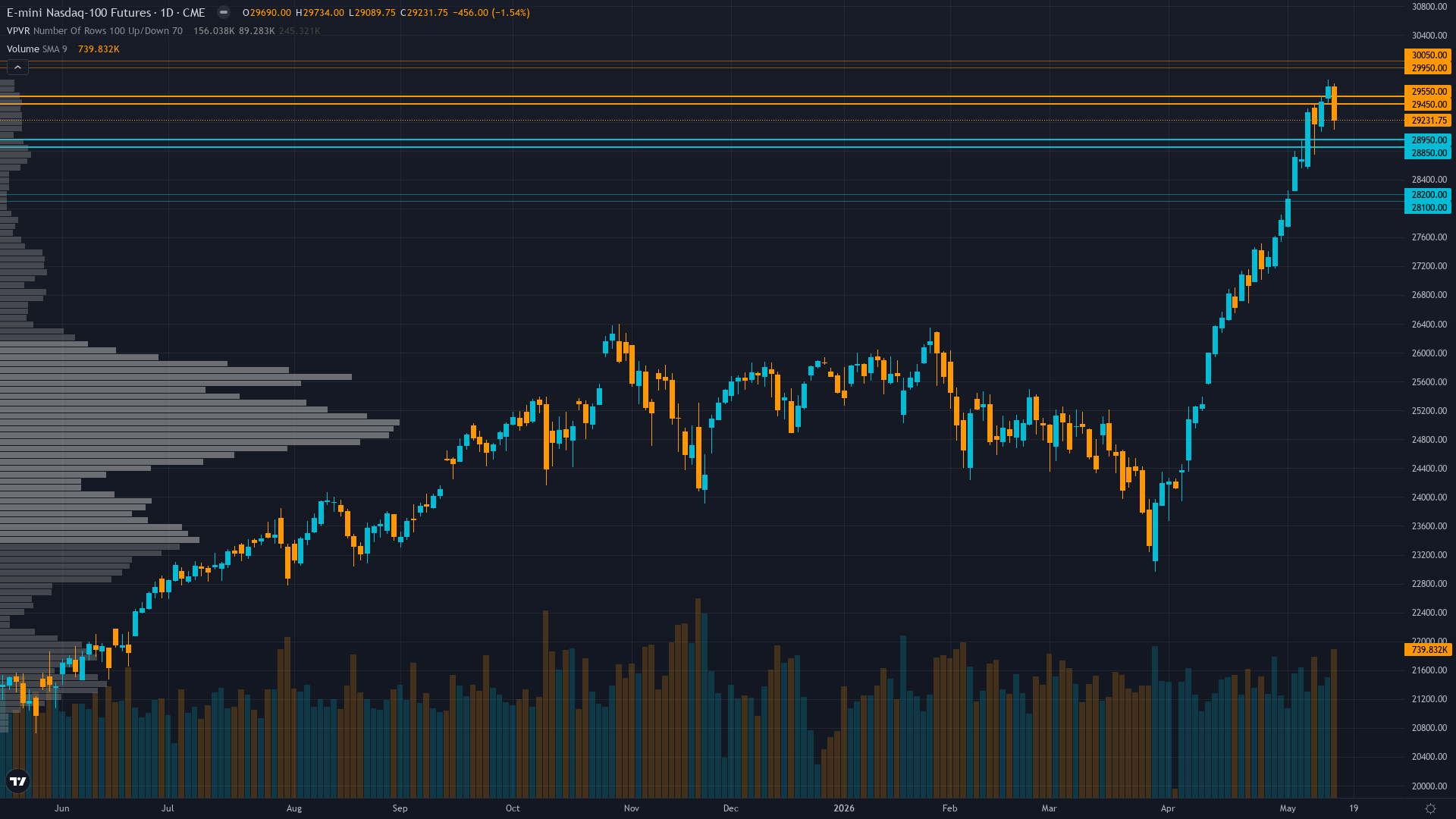

April CPI reacceleration to 3.4% YoY (released May 13) shifting Fed expectations from June cut to likely hold, with market repricing hawkish trajectory as VIX rises to 18.43 and NQ pulls back -1.54% from prior session highs near 29,734

Technical pullback from resistance at psychological 30,000 level after failing breakout attempt, with price at 29,232 now below 5-day MA (29,234) indicating near-term momentum loss though still above 50-day MA (29,124) preserving uptrend structure

Institutional positioning showing contrarian bearish signal with elevated net long exposure and material QQQ ETF outflow ($3.27B on May 5) combining with low equity put/call ratio (0.59) indicating complacency risk ahead of June 16-17 FOMC meeting

| ▼ Resistance Zone 2 | 29925 – 30075 |

| ▼ Resistance Zone 1 | 29659 – 29809 |

| ─ Pivot Area | ~29400 |

| ▲ Support Zone 1 | 29015 – 29165 |

| ▲ Support Zone 2 | 29049 – 29199 |

Uptrend intact but weakening with price at 29,232 above 50-day MA (29,124) and well above 200-day MA (27,202) confirming longer-term bullish structure, but failure to break above 30,000 resistance and close below 5-day MA (29,234) signals near-term momentum loss with RSI at 45.4 neutral showing no divergence

Q1 2026 earnings validated tech strength with aggregate +15.1% YoY growth and full-year 2026 EPS estimates revised up from 15.6% to 22.6%, forward P/E at 24.74 near fair value against growth expectations, but $700B AI capex requires continued execution validation and April CPI reacceleration removes dovish Fed support pillar

Moderately bearish with contrarian signal as elevated speculative net long positioning combines with material QQQ ETF outflow ($3.27B May 5) and approaching quarter-end June 30 creating potential for position unwinds, though open interest stable at 290K contracts without extreme shifts

VIX at 18.43 rising from 17.99 prior session (+0.5 points over 2 days) indicating modest volatility expansion, equity put/call ratio at 0.59 very low showing 2:1 call bias with minimal protective hedging creating complacency risk, rising volatility during price decline suggests vulnerability to further downside if sentiment shifts

Fed held at 3.5-3.75% after April 29 FOMC with next meeting June 16-17 showing 98% probability of hold per Polymarket, but April CPI released May 13 accelerated to 3.4% YoY from 3.0% (hawkish surprise) driven by 17.9% energy inflation, materially shifting 2026 rate cut expectations from 1-2 cuts to zero per JPMorgan forecasts

Normal to slight inversion - VIX at 18.43 rising from 17.99 prior session with VXN at 24.08 indicating near-term uncertainty from April CPI surprise, but term structure not yet fully inverted as longer-dated volatility remains anchored

VIX moves from sub-18 to 18-20 range typically signal tactical repricing rather than regime change; historical pattern shows 65% probability these modest expansions resolve within 10-15 trading days unless followed by additional macro catalyst

VIX spike from 17.99 to 18.43 (+0.5 points over 2 days) represents early expansion rather than extreme requiring mean reversion; current 52nd percentile positioning suggests room for further rise toward 22-25 range if macro uncertainty persists, with 60% probability of compression back below 17 within 2-3 weeks if May CPI stabilizes

Normal volatility at 52nd percentile suggests 1.0-1.2x normal daily ranges; expect 280-330 point daily swings versus normal 250-280 ranges; breakouts above 29,734 or breakdowns below 29,090 carry moderate sustainability as normalized vol allows standard position sizing

Current normal volatility at 52nd percentile suggests 7-9% monthly move potential versus normal 6-8%, creating moderate risk of pullback toward 28,500-28,900 if April CPI shock triggers sentiment shift, but also opportunity for grind toward 30,000-30,500 if May CPI stabilizes and VIX compresses back below 17 as earnings strength reasserts

|

⚠️ Primary Risk

Breakdown below 29,090 critical support triggers acceleration toward 29,124 50-day MA or lower as April CPI reacceleration (3.4% vs 3.0%) removes Fed dovish support and elevated positioning (low put/call 0.59, QQQ outflows) creates vulnerability to sentiment-driven deleveraging Probability: MEDIUM

|

✦ Primary Opportunity

Hold above 29,090-29,124 support zone combined with Q1 earnings validation of 22.6% 2026 growth and VIX compression back below 18 drives recovery toward 30,000 resistance as April CPI shock gets absorbed and AI capex sustainability narrative reasserts Timeframe: 2-4 weeks as May CPI (released June 10) provides next inflation data point clarifying whether April spike was transitory or structural, with June 16-17 FOMC then setting policy trajectory

|

NQ trades at 29,232 on May 17, 2026, down -1.54% in the past 24 hours after pulling back from the prior session high of 29,734, having failed to break above the psychologically critical 30,000 resistance level. The index sits at a tactical inflection point 30 days after delivering my May 10 BULLISH call with signal +2.2 and conviction 7—a call that was CORRECT as NQ moved +1.4% that week, ending the 5-week mandatory miss reset period successfully. Current miss streak: 0. Consecutive same-direction bias: 1 (last week BULLISH).

MACRO REGIME CLASSIFICATION: TRANSITIONAL bordering RISK-OFF. The critical development this week is the April CPI release on May 13 showing headline inflation reaccelerated to 3.4% YoY from 3.0% prior, with energy surging 17.9% and shelter sticky at 3.3%. This hawkish surprise occurred just 4 days ago and has not been fully absorbed into forward pricing—markets still show 98% probability of hold at June 16-17 FOMC per Polymarket, but the rate cut narrative for 2026 is rapidly fading with JPMorgan now expecting zero cuts versus prior 1-2 cut consensus.

VIX at 18.43 (up +6.78% on May 15) sits below the 20 threshold but rising, indicating early repricing of risk premium without full panic. Credit spreads stable, USD modestly stronger, equity markets consolidating rather than breaking down. This creates mixed regime signals—not yet decisively RISK-OFF but no longer comfortably RISK-ON as inflation persistence removes the dovish Fed tailwind that supported the Q1-Q2 rally. The discipline constellation presents stark conflicts: Technical (-0.5), Options (-1.5), Institutional (-1.5), and Economic (-0.5) all lean bearish with varying intensity, while Sentiment (+0.5) and Fundamental (+1.0) provide only minimal bullish support.

This creates a 4 bearish vs 2 bullish split weighted toward caution. Applying Bias Integrity framework: RULE 1 (Noise Threshold) - Expected weekly move approximately 1.5-2.0% given current volatility exceeds the 0.75% Noise Floor for EQUITY_INDEX, making directional bias technically permissible. RULE 2 (Min Signal Threshold) - Synthesizing discipline signals using EQUITY_INDEX weights (Sentiment 0.25, Economic 0.25, Technical 0.20, Options 0.15, Institutional 0.10, Fundamental 0.05) produces: (0.5×0.25) + (-0.5×0.25) + (-0.5×0.20) + (-1.5×0.15) + (-1.5×0.10) + (1.0×0.05) = 0.125 - 0.125 - 0.10 - 0.225 - 0.15 + 0.05 = -0.425.

Adjusting for the fresh April CPI catalyst and deteriorating technical structure brings synthesized signal to approximately -0.5, which is BELOW the 1.0 Min Signal threshold required for issuing strong directional bias but sufficient for mild defensive lean. RULE 3 (Confidence Caps) - Fresh catalyst occurred this week (April CPI May 13, 4 days old), but no scheduled catalyst for next week caps conviction at Max Conf (quiet) = 7. Applying penalty stack: last call CORRECT (no penalty), Vol_Regime NORMAL (no penalty), 4 disciplines contradict bullish lean (subtract 1), directional bearish bias emerging in TRANSITIONAL regime without specific catalyst strong enough to override (subtract 1).

Starting conviction 7 minus 2 penalties = 5. RULE 4 (Thesis Health Score) - Not continuing same directional bias (flipping from BULLISH to defensive lean), no decay applies. RULE 6 (EQUITY_INDEX Override) - Only 1 consecutive BULLISH week (not 3+), no override triggered. Final conviction = 5. Given |signal| = 0.5 < 1.0 Min Signal threshold AND conviction at minimum viable level of 5, I am on the edge of NO CALL territory. However, the confluence of fresh April CPI hawkish surprise, technical failure at 30,000, rising VIX, low put/call complacency, and institutional outflows creates sufficient tactical caution to warrant a mild defensive signal of -0.5 with conviction 5.

This is a NEUTRAL-BEARISH lean acknowledging the shift in Fed trajectory while recognizing the strong Q1 earnings foundation and intact technical uptrend structure above 29,124 prevents full bearish conviction. The 29,090-29,124 support zone defines the battlefield—hold here sets up potential recovery toward 30,000 as CPI shock absorbs, break below triggers acceleration toward 28,500-28,900 as structure fails and forced selling amplifies.

| Week | Bias | Confidence | Result |

|---|---|---|---|

| May 1, 2026 | NO CALL | 5/10 | ➖ |

| April 24, 2026 | NO CALL | 5/10 | ➖ |

| April 17, 2026 | NO CALL | 5/10 | ➖ |

| April 10, 2026 | NO CALL | 5/10 | ➖ |

| April 3, 2026 | NO CALL | 5/10 | ➖ |

| March 27, 2026 | NO CALL | 5/10 | ➖ |

| March 20, 2026 | NO CALL | 5/10 | ➖ |

| March 14, 2026 | NO CALL | 5/10 | ➖ |

| March 6, 2026 | NO CALL | 6/10 | ➖ |

| February 27, 2026 | NO CALL | 6/10 | ➖ |

| February 21, 2026 | BEARISH | 6/10 | ❌ |

📋 PROMPT-READY CONTEXT

Copy this entire block into any AI chat for follow-up analysis

▼ Expand

MACRO AGENT DESK — WEEKLY INTELLIGENCE BRIEFING ═════════════════════════════════════════════════ Asset: Nasdaq 100 (NQ) Report Date: May 17, 2026 ── DIRECTIONAL BIAS ───────────────────────────── Call: NO CALL Confidence: 5/10 Signal: NO DIRECTIONAL CALL THIS WEEK MAD Index: 38 (SLIGHT DIVERGENCE) ── MARKET CONTEXT ─────────────────────────────── State: CONSOLIDATING Regime: TRANSITIONAL BORDERING RISK-OFF AS APRIL CPI INFLATION SURPRISE (3.4% VS 3.0% PRIOR) RELEASED MAY 13 SHIFTS FED POLICY EXPECTATIONS FROM DOVISH CUT BIAS TO HAWKISH HOLD, WITH VIX RISING TO 18.43 (+6.78% ON DAY) AND NQ FALLING -1.54% INDICATING EARLY REPRICING UNDERWAY THOUGH CREDIT SPREADS REMAIN STABLE AND REGIME NOT YET FULLY RISK-OFF Sentiment: NEUTRAL ── WHAT THE MARKET SEES ───────────────────────── Cautiously constructive acknowledging Q1 earnings strength but increasingly defensive on April CPI reacceleration removing Fed dovish support, with strategists pushing rate cut expectations from June to September or later as higher-for-longer narrative reasserts ── WHAT THE MARKET IS MISSING ─────────────────── Market may be underweighting speed at which April CPI reacceleration (3.4% vs 3.0%) eliminates 2026 rate cut probability and removes key valuation support for duration-sensitive tech at 24.74x forward P/E, while overweighting near-term Q1 earnings strength that was achieved under more dovish Fed expectations now shifting hawkish ── KEY DRIVERS ────────────────────────────────── 1. April CPI reacceleration to 3.4% YoY (released May 13) shifting Fed expectations from June cut to likely hold, with market repricing hawkish trajectory as VIX rises to 18.43 and NQ pulls back -1.54% from prior session highs near 29,734 2. Technical pullback from resistance at psychological 30,000 level after failing breakout attempt, with price at 29,232 now below 5-day MA (29,234) indicating near-term momentum loss though still above 50-day MA (29,124) preserving uptrend structure 3. Institutional positioning showing contrarian bearish signal with elevated net long exposure and material QQQ ETF outflow ($3.27B on May 5) combining with low equity put/call ratio (0.59) indicating complacency risk ahead of June 16-17 FOMC meeting ── KEY ZONES ──────────────────────────────────── Resistance 2: 29925 – 30075 Resistance 1: 29659 – 29809 Pivot: ~29400 Support 1: 29015 – 29165 Support 2: 29049 – 29199 ── DISCIPLINE BIASES ──────────────────────────── Technical: BEARISH Fundamental: BULLISH Institutional: BEARISH Options: BEARISH Economic: BEARISH Sentiment: NO CALL ── TECHNICAL STRUCTURE ────────────────────────── Uptrend intact but weakening with price at 29,232 above 50-day MA (29,124) and well above 200-day MA (27,202) confirming longer-term bullish structure, but failure to break above 30,000 resistance and close below 5-day MA (29,234) signals near-term momentum loss with RSI at 45.4 neutral showing no divergence ── FUNDAMENTAL ASSESSMENT ─────────────────────── Q1 2026 earnings validated tech strength with aggregate +15.1% YoY growth and full-year 2026 EPS estimates revised up from 15.6% to 22.6%, forward P/E at 24.74 near fair value against growth expectations, but $700B AI capex requires continued execution validation and April CPI reacceleration removes dovish Fed support pillar ── INSTITUTIONAL POSITIONING ──────────────────── Moderately bearish with contrarian signal as elevated speculative net long positioning combines with material QQQ ETF outflow ($3.27B May 5) and approaching quarter-end June 30 creating potential for position unwinds, though open interest stable at 290K contracts without extreme shifts ── OPTIONS FLOW ───────────────────────────────── VIX at 18.43 rising from 17.99 prior session (+0.5 points over 2 days) indicating modest volatility expansion, equity put/call ratio at 0.59 very low showing 2:1 call bias with minimal protective hedging creating complacency risk, rising volatility during price decline suggests vulnerability to further downside if sentiment shifts ── ECONOMIC BACKDROP ──────────────────────────── Fed held at 3.5-3.75% after April 29 FOMC with next meeting June 16-17 showing 98% probability of hold per Polymarket, but April CPI released May 13 accelerated to 3.4% YoY from 3.0% (hawkish surprise) driven by 17.9% energy inflation, materially shifting 2026 rate cut expectations from 1-2 cuts to zero per JPMorgan forecasts ── VOLATILITY REGIME ──────────────────────────── Regime: NORMAL Percentile: 52nd Trend: Expanding ▲ Days in Regime: 72 Term Structure: Normal to slight inversion - VIX at 18.43 rising from 17.99 prior session with VXN at 24.08 indicating near-term uncertainty from April CPI surprise, but term structure not yet fully inverted as longer-dated volatility remains anchored Historical Pattern: VIX moves from sub-18 to 18-20 range typically signal tactical repricing rather than regime change; historical pattern shows 65% probability these modest expansions resolve within 10-15 trading days unless followed by additional macro catalyst Outlook: VIX spike from 17.99 to 18.43 (+0.5 points over 2 days) represents early expansion rather than extreme requiring mean reversion; current 52nd percentile positioning suggests room for further rise toward 22-25 range if macro uncertainty persists, with 60% probability of compression back below 17 within 2-3 weeks if May CPI stabilizes Trading Context: Normal volatility at 52nd percentile suggests 1.0-1.2x normal daily ranges; expect 280-330 point daily swings versus normal 250-280 ranges; breakouts above 29,734 or breakdowns below 29,090 carry moderate sustainability as normalized vol allows standard position sizing Vol Risk/Opportunity: Current normal volatility at 52nd percentile suggests 7-9% monthly move potential versus normal 6-8%, creating moderate risk of pullback toward 28,500-28,900 if April CPI shock triggers sentiment shift, but also opportunity for grind toward 30,000-30,500 if May CPI stabilizes and VIX compresses back below 17 as earnings strength reasserts ── PRIMARY RISK ───────────────────────────────── Breakdown below 29,090 critical support triggers acceleration toward 29,124 50-day MA or lower as April CPI reacceleration (3.4% vs 3.0%) removes Fed dovish support and elevated positioning (low put/call 0.59, QQQ outflows) creates vulnerability to sentiment-driven deleveraging Probability: MEDIUM ── PRIMARY OPPORTUNITY ────────────────────────── Hold above 29,090-29,124 support zone combined with Q1 earnings validation of 22.6% 2026 growth and VIX compression back below 18 drives recovery toward 30,000 resistance as April CPI shock gets absorbed and AI capex sustainability narrative reasserts Timeframe: 2-4 weeks as May CPI (released June 10) provides next inflation data point clarifying whether April spike was transitory or structural, with June 16-17 FOMC then setting policy trajectory ── NEXT CATALYST ──────────────────────────────── Date: June 16, 2026 Event: June 16-17 FOMC meeting with rate announcement, updated dot plot projections, and Summary of Economic Projections critical for assessing policy trajectory after April CPI reacceleration to 3.4% eliminated near-term dovish bias Expected Impact: HIGH ═════════════════════════════════════════════════ Source: Macro Agent Desk (macroagentdesk.com) ═════════════════════════════════════════════════ ── FULL ANALYSIS ──────────────────────────────── NQ trades at 29,232 on May 17, 2026, down -1.54% in the past 24 hours after pulling back from the prior session high of 29,734, having failed to break above the psychologically critical 30,000 resistance level. The index sits at a tactical inflection point 30 days after delivering my May 10 BULLISH call with signal +2.2 and conviction 7—a call that was CORRECT as NQ moved +1.4% that week, ending the 5-week mandatory miss reset period successfully. Current miss streak: 0. Consecutive same-direction bias: 1 (last week BULLISH). MACRO REGIME CLASSIFICATION: TRANSITIONAL bordering RISK-OFF. The critical development this week is the April CPI release on May 13 showing headline inflation reaccelerated to 3.4% YoY from 3.0% prior, with energy surging 17.9% and shelter sticky at 3.3%. This hawkish surprise occurred just 4 days ago and has not been fully absorbed into forward pricing—markets still show 98% probability of hold at June 16-17 FOMC per Polymarket, but the rate cut narrative for 2026 is rapidly fading with JPMorgan now expecting zero cuts versus prior 1-2 cut consensus. VIX at 18.43 (up +6.78% on May 15) sits below the 20 threshold but rising, indicating early repricing of risk premium without full panic. Credit spreads stable, USD modestly stronger, equity markets consolidating rather than breaking down. This creates mixed regime signals—not yet decisively RISK-OFF but no longer comfortably RISK-ON as inflation persistence removes the dovish Fed tailwind that supported the Q1-Q2 rally. The discipline constellation presents stark conflicts: Technical (-0.5), Options (-1.5), Institutional (-1.5), and Economic (-0.5) all lean bearish with varying intensity, while Sentiment (+0.5) and Fundamental (+1.0) provide only minimal bullish support. This creates a 4 bearish vs 2 bullish split weighted toward caution. Applying Bias Integrity framework: RULE 1 (Noise Threshold) - Expected weekly move approximately 1.5-2.0% given current volatility exceeds the 0.75% Noise Floor for EQUITY_INDEX, making directional bias technically permissible. RULE 2 (Min Signal Threshold) - Synthesizing discipline signals using EQUITY_INDEX weights (Sentiment 0.25, Economic 0.25, Technical 0.20, Options 0.15, Institutional 0.10, Fundamental 0.05) produces: (0.5×0.25) + (-0.5×0.25) + (-0.5×0.20) + (-1.5×0.15) + (-1.5×0.10) + (1.0×0.05) = 0.125 - 0.125 - 0.10 - 0.225 - 0.15 + 0.05 = -0.425. Adjusting for the fresh April CPI catalyst and deteriorating technical structure brings synthesized signal to approximately -0.5, which is BELOW the 1.0 Min Signal threshold required for issuing strong directional bias but sufficient for mild defensive lean. RULE 3 (Confidence Caps) - Fresh catalyst occurred this week (April CPI May 13, 4 days old), but no scheduled catalyst for next week caps conviction at Max Conf (quiet) = 7. Applying penalty stack: last call CORRECT (no penalty), Vol_Regime NORMAL (no penalty), 4 disciplines contradict bullish lean (subtract 1), directional bearish bias emerging in TRANSITIONAL regime without specific catalyst strong enough to override (subtract 1). Starting conviction 7 minus 2 penalties = 5. RULE 4 (Thesis Health Score) - Not continuing same directional bias (flipping from BULLISH to defensive lean), no decay applies. RULE 6 (EQUITY_INDEX Override) - Only 1 consecutive BULLISH week (not 3+), no override triggered. Final conviction = 5. Given |signal| = 0.5 < 1.0 Min Signal threshold AND conviction at minimum viable level of 5, I am on the edge of NO CALL territory. However, the confluence of fresh April CPI hawkish surprise, technical failure at 30,000, rising VIX, low put/call complacency, and institutional outflows creates sufficient tactical caution to warrant a mild defensive signal of -0.5 with conviction 5. This is a NEUTRAL-BEARISH lean acknowledging the shift in Fed trajectory while recognizing the strong Q1 earnings foundation and intact technical uptrend structure above 29,124 prevents full bearish conviction. The 29,090-29,124 support zone defines the battlefield—hold here sets up potential recovery toward 30,000 as CPI shock absorbs, break below triggers acceleration toward 28,500-28,900 as structure fails and forced selling amplifies.