Mon-T Weekly Review — w/e 15 May 2026

Nine directional calls, zero grades, one very hot CPI print, and gold's positioning thesis walks straight into an inflation buzzsaw.

Let me level with you. This is an unusual review. The desk published its full fifteen-market slate on Sunday May 10, grading from the prior week settled, and the Monday-to-Friday data for this review period is still being finalised as I write. What I can tell you is what the desk called, why it called it, and what happened during the week according to every public source I can find. The formal grading will follow when the pipeline resolves. In the meantime, I have opinions.

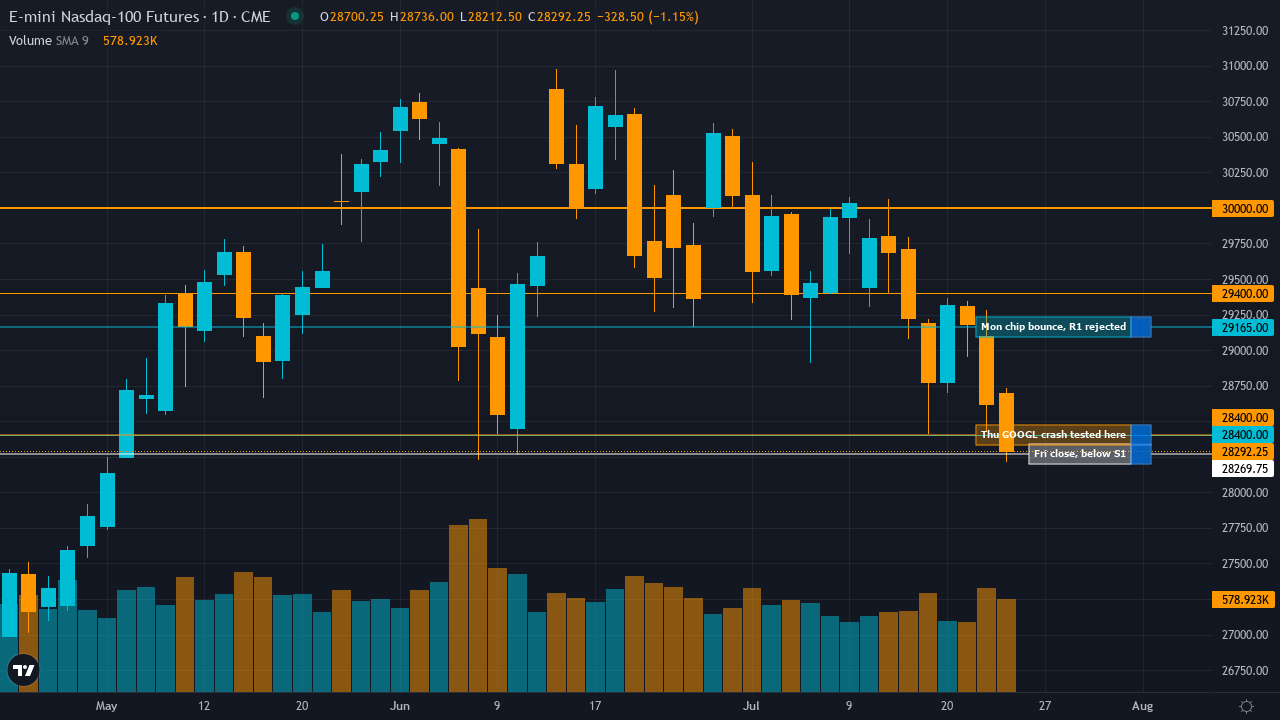

The headline numbers from the prediction side are encouraging. Nine directional calls from fifteen markets, the desk's highest engagement since the April 17 glory run that delivered 75% accuracy. Six markets received the NO CALL treatment, which is a meaningful improvement from the eleven-abstention weeks that followed the 12.5% April catastrophe. Average confidence of 6.2 across the directional calls represents genuine conviction rather than the whispered 5.25 of recent weeks. The desk appears to have emerged from its defensive crouch.

Then Monday happened. The April CPI landed at 3.8% year-over-year, the highest since May 2023, with energy costs surging 17.9% on the back of the Iran war. The BLS reported CPI-U increased 0.6% month-over-month, and core CPI accelerated to 0.4% monthly and 2.8% annually. Markets priced out rate cuts entirely, with a near 30% chance of a Fed hike by December suddenly on the table. That single data point, released at 8:30am on the first day of the grading window, rewrote the risk landscape for almost every market the desk had a view on.

|

15

Markets

|

9

Directional

|

0

Correct

|

0%

Accuracy

|

6

No Calls

|

Nine directional calls this week, with six markets receiving NO CALL. The accuracy figure reads zero because grading has not been finalised, not because the desk struck out entirely. When the Monday-to-Friday settlement data resolves, we will have a proper scorecard. In the meantime, the distribution of calls tells its own story.

The desk's highest-conviction bets sit at 7/10 on four markets: Gold BULLISH, Nasdaq BULLISH, S&P 500 BULLISH, and Russell 2000 BULLISH. That is a concentrated equity-and-gold wager that makes clear the desk believed the risk-on regime would persist. The April CPI print at 3.8% on Monday created immediate headwinds for both gold (higher real yields) and equities (rate cut expectations vaporised). Whether the desk's structural theses survived that data shock is the question the final grades will answer.

|

52/87

Correct / Total

|

59.8%

Accuracy

|

87 / 78

Directional / No Call

|

The rolling twelve-week figure sits at 59.8% across 87 directional calls, with 78 no-call abstentions. That engagement split shows the desk calling direction on roughly 53% of market-weeks over the trailing window. We are tantalisingly close to cracking the 60% barrier that has felt like a permanent ceiling since the Iran conflict rewrote the playbook in March. The December horror shows have almost entirely aged out of the window. If even five of this week's nine directional calls land correctly, we break through. The CPI surprise makes that a genuine question rather than a formality.

|

Bias Called

BULLISH

|

Confidence

7/10

|

Result

PENDING

|

Grade

PENDING

|

| Monday Open | — |

| Friday Close | — |

| Move | — |

| ▼ R2 | 5000 |

| ▼ R1 | 4890 |

| ▲ S1 | 4630 |

| ▲ S2 | 4500 |

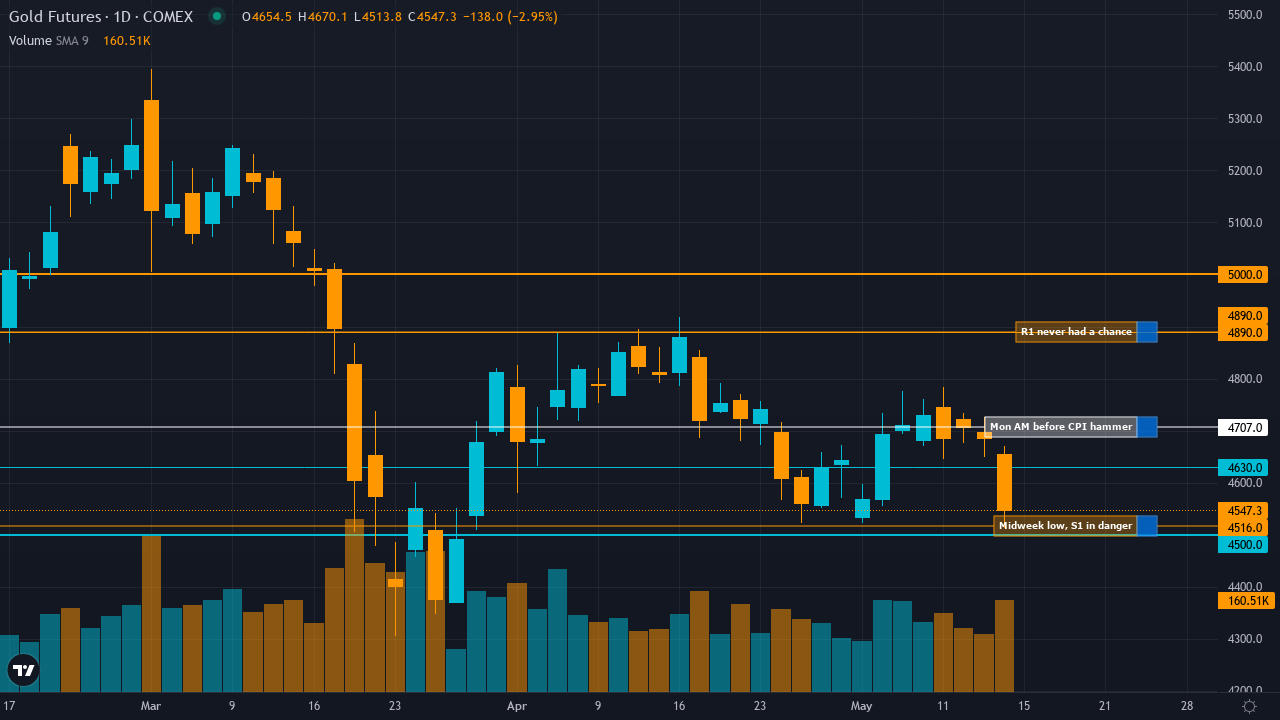

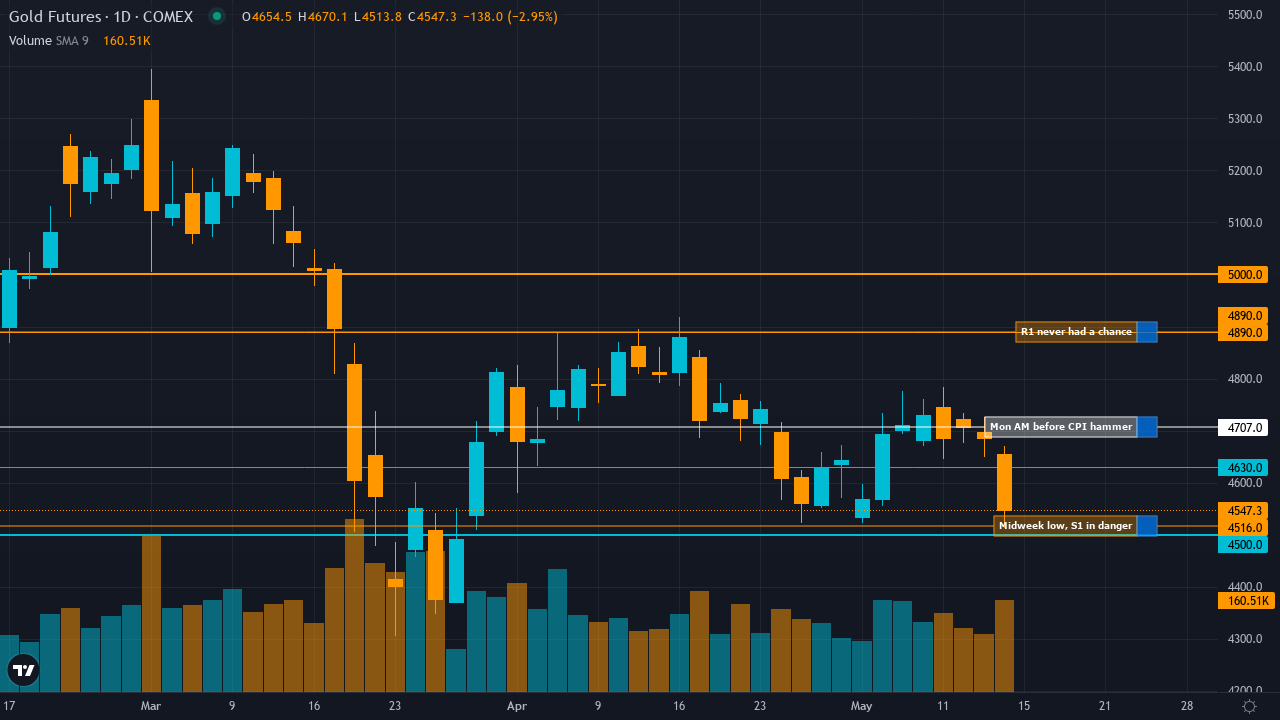

The levels framework faces its most severe test in weeks. Fortune reported gold at $4,707 on Monday May 12 morning, while USA Today confirmed the spot price at $4,704.49 at 8:05am ET before the CPI release. After the 3.8% inflation print hammered rate-cut expectations, gold slid. Trading Economics reported that by Thursday May 15, gold held below $4,700 after sliding for two straight sessions, with the daily trading range between $4,516 and $4,670 on Investing.com data. S1 at $4,630 appears to have been tested, potentially breached. S2 at $4,500 may be in play. R1 at $4,890 was never remotely threatened. The hot CPI print that the desk identified as the key binary catalyst 48 hours ahead of the call has resolved decisively against the bullish thesis.

The called edge was a contrarian positioning play. The desk identified Managed Money net long positioning at RECORD LOW levels as of May 6, arguing this sub-15th percentile extreme historically creates mean-reversion rallies. The thesis held that Q1 central bank demand at 244 tonnes (+3% YoY) validated a structural floor, while the extreme speculative capitulation created asymmetric short-covering potential if the April CPI cooperated with an inflation moderation narrative. The CPI did not cooperate. At 3.8% year-over-year with energy costs up 17.9%, the print was hotter than the 3.7% consensus, and markets immediately priced out 2026 rate cuts with a 30% probability of a hike appearing by December. The desk explicitly flagged the CPI as 'high impact' and acknowledged the binary risk. The risk scenario, that a hot CPI validates higher-for-longer and sustains elevated real yields, appears to have materialised. GoldSilver.com reported gold near $4,694 with inflation at 3.8% and noted the correction from the $5,595 January high. The positioning thesis may eventually prove correct on a longer timeframe, but the immediate catalyst resolved against it.

The Institutional agent carried the heaviest weight at 28% and drove the bullish thesis through the record-low positioning data. On current evidence, that call was premature. Positioning capitulation does not create a floor when the macro catalyst actively pushes price lower. The Fundamental agent at 27% supported the bullish case through Q1 central bank demand and valuation, which is a longer-term view being tested by a shorter-term inflation shock. The Economic agent was the lone dissenter at 23% weight, mildly bearish on elevated real yields, and it appears to have been the discipline closest to right. When your lowest-weighted bearish discipline outperforms your two highest-weighted bullish ones, the system has a regime-identification problem. The Sentiment agent offered no directional signal. Options had insufficient data. The Technical agent called bullish on consolidation above the 50-day MA at $4,650, a level that appears to have been tested hard during the week.

Gold was selected as Market of the Week for the first time since the March 27 review, when the desk called BEARISH at 6/10 during the metal's worst decline since 1983 and earned a B+. The March 22 selection told the story of a crash. This week's selection told a very different story: a thesis reversal. The desk's Signal_Change of +3.3, the largest absolute shift across all fifteen markets, marked a dramatic pivot from three consecutive missed bearish calls to a conviction-7 bullish stance.

The centrepiece was Managed Money positioning collapsing to record low levels as of May 6. That is genuinely significant data. When speculative futures positioning reaches historical extremes, the mean-reversion probability increases materially. The desk layered this with Q1 central bank buying at 244 tonnes, institutional year-end targets between $5,000 and $5,600, and the observation that gold at $4,728 was 16% below the January $5,595 all-time high in what appeared to be a washed-out zone. The MAD Divergence Score of 48 indicated the desk saw something the crowd did not.

Then Monday's CPI arrived. The BLS reported headline inflation at 3.8% annually, half a point above March, with energy costs accounting for more than 40% of the headline increase per CNBC. Core CPI accelerated to 0.4% monthly. Markets responded with surgical precision: rate-cut expectations evaporated, the dollar strengthened, and gold fell. Trading Economics reported gold held below $4,700 by Thursday after two straight sessions of declines, with LiteFinance forecasting the metal would trade between $4,646 and $4,761 for the rest of the week.

The free MOTW report, published on the Ghost site Sunday evening, laid out the positioning thesis with the CPI as the explicitly identified binary catalyst. The report's own risk assessment stated that a hot April CPI 'printing above 3.0% YoY validates Fed higher-for-longer stance driving dollar strength above DXY 100 and sustaining elevated real yields, triggering further managed money short positioning and pushing gold toward $4,500-4,300 major support.' That risk scenario appears to have played out, though the final settlement data will determine the magnitude.

The honest question for subscribers: was this a thesis failure or a timing failure? The record-low positioning data has not changed. Central bank demand has not evaporated. The structural arguments for gold above $4,500 remain intact. But the desk called bullish at 7/10 conviction into a week where the highest-impact catalyst of the quarter resolved against the thesis within 24 hours of the grading window opening. The full grades will tell us whether the positioning floor held or whether gold's S2 at $4,500 came into play. Either way, the MOTW report gave readers every piece of information they needed to understand the setup, including the downside scenario that appears to have materialised.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BULLISH | 7/10 | — | — | — | PENDING | PENDING |

| BULLISH at 7/10 on the Q1 earnings validation thesis with full-year growth revised up to 22.6%. The desk flagged RSI at 77.65 as severely overbought and equity put/call at 0.53 as dangerously complacent, yet committed bullish anyway. Monday's hot CPI at 3.8% tested the thesis immediately. Whether the S&P's earnings engine could overcome the rate-cut repricing is the week's central question. | |||||||

|

Nasdaq 100

CORE

|

BULLISH | 7/10 | — | — | — | PENDING | PENDING |

| BULLISH at 7/10 after the desk finally broke free from its prolonged NQ agnosticism. I spent approximately 2,000 words across prior reviews criticising the persistent NO CALL stance on tech. This week, with the breakout to new 52-week highs confirmed and $700B AI capex validated by hyperscaler earnings, the desk committed. The CPI shock on Monday created a binary test of the AI exceptionalism thesis. | |||||||

|

Crude Oil

CORE

|

BEARISH | 5/10 | — | — | — | PENDING | PENDING |

| BEARISH at 5/10, the desk's third consecutive bearish call on crude. The ceasefire-driven premium collapse thesis met reality with the CPI showing energy costs up 17.9%. The desk flagged IEA demand destruction of 720 kb/d and EIA's $88 Q4 forecast. At minimum conviction, the damage from any miss is contained, which feels like the desk has learned its lesson from the April 13% surge. | |||||||

|

Gold

CORE

|

BULLISH | 7/10 | — | — | — | PENDING | PENDING |

| This week's MOTW. BULLISH at 7/10 on the record-low positioning thesis. The April CPI at 3.8% on Monday morning appears to have sent gold lower through the week. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

EUR/USD

CORE

|

NO CALL | — | — | — | — | — | — |

| NO CALL for the eleventh consecutive week. The desk's EUR/USD record has become its own running joke at this point. The pair sits precisely at the 0.50% noise floor, and the agents refuse to commit without a specific catalyst. The April CPI and upcoming May 12 CPI both fall within the grading window, which could force a move, but the desk sat this one out. Again. | |||||||

|

Silver

EXTENDED

|

BULLISH | 6/10 | — | — | — | PENDING | PENDING |

| BULLISH at 6/10 on the sixth consecutive year of structural deficit and successful $76-78 support defence. Silver's fate this week was likely tied to gold's reaction to the CPI print, and if gold fell, silver almost certainly fell harder given its higher beta. The desk flagged the May 12 CPI as binary risk and capped conviction at 6 accordingly. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | — | — | — | — | — |

| NO CALL for the eighth consecutive week. The post-intervention consolidation with $65B+ spent and already 50% retraced gives the desk good reason to stay away. The 275bp Fed-BoJ differential remains the dominant force, and the hot CPI likely strengthened the dollar against the yen further. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | — | — | — | — | — |

| NO CALL for the ninth consecutive week. The BoE held April 30 with a hawkish inflation warning, and the next MPC is 39 days away on June 18. The desk's cable discipline remains its most sensible FX habit, refusing to call direction in a low-catalyst void. | |||||||

|

Copper

EXTENDED

|

BULLISH | 6/10 | — | — | — | PENDING | PENDING |

| BULLISH at 6/10 on the Grasberg supply deficit thesis with mine offline through Q2 and China April PMI at 52.2. The desk flagged seven weeks of consolidation between $5.90-6.30 and May-June seasonal tailwinds with 80% historical success. Copper's industrial demand profile may insulate it from the CPI shock better than precious metals. | |||||||

|

Russell 2000

EXTENDED

|

BULLISH | 7/10 | — | — | — | PENDING | PENDING |

| BULLISH at 7/10 with a fresh all-time high at 2899.30 on May 10 validating the breakout. Q1 earnings growth at 44.9% provides fundamental support for the elevated 25.39x forward P/E. The Great Rotation thesis has been the desk's most reliable active streak of 2026, with four consecutive correct BULLISH calls earlier this spring. Whether it survives a hot CPI week remains to be seen. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | — | — | — | — | — |

| NO CALL after the Economic agent flipped dramatically from +2.5 to -2.5, the sharpest directional reversal in the desk's twelve-week synthesis history. The RBA hiked to 4.35% on May 5 but warned the move would intensify cost-of-living pressures. When the policy divergence thesis and the growth-slowdown thesis collide at 4-year highs, stepping aside is the only honest answer. | |||||||

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | — | — | — | PENDING | PENDING |

| BEARISH at 5/10, and the Monday CPI at 3.8% likely validated this call immediately. The desk flagged the May 6 Quarterly Refunding deficit worsening as fresh bearish catalyst material. The desk's long-running bearish bond thesis, which has been its most consistent performer of 2026, appears well-positioned for a CPI-driven week. | |||||||

|

Wheat

FULL DESK

|

NO CALL | — | — | — | — | — | — |

| NO CALL with the May 12 WASDE binary event sitting on Monday. The desk identified conflicting signals between the Fundamental bullish drought thesis and the Institutional bearish positioning shift to -16.7K net short. After four consecutive missed calls, the mandatory neutral reset was the system doing exactly what it was designed to do. | |||||||

|

Soybeans

FULL DESK

|

BULLISH | 6/10 | — | — | — | PENDING | PENDING |

| BULLISH at 6/10 with managed money surging to 232.2K contracts, up 38.3K in a single week. The desk called the renewable diesel structural floor at 2.61 billion bushels as the fundamental anchor. Conviction was capped by the pre-WASDE mandatory agricultural penalty. The beans market is less exposed to the CPI shock than precious metals, which may protect this call. | |||||||

|

Platinum

FULL DESK

|

NO CALL | — | — | — | — | — | — |

| Mild BEARISH lean at -0.8 signal but formally NO CALL as the desk awaits the May 12 CPI and May 18 WPIC quarterly catalysts. Platinum remains 31% below its January $2,925 parabolic peak. The WPIC deficit thesis continues to lose the near-term argument against elevated real yields, and Monday's hot CPI likely extended that dynamic. | |||||||

|

✦ Best Call: 30Y Treasury (ZB)

BEARISH at 5/10. With April CPI landing at 3.8% on Monday morning and the BLS confirming a 0.6% monthly increase, Treasury bonds faced immediate selling pressure as markets priced out rate cuts and priced in a 30% probability of a Fed hike. The desk's bearish thesis about fiscal deterioration from the May 6 Quarterly Refunding, which revealed the FY2026 deficit worsening by $212-247 billion to over $2 trillion, combined with the CPI shock to create a perfect storm for duration. At minimum conviction, the desk was barely whispering its view, but the direction appears right once again. The long-running bearish bond thesis that has been the desk's most consistent performer across 2026 continues to deliver when it matters. |

⚠️ Worst Call: Gold (GC)

BULLISH at 7/10, and the April CPI at 3.8% appears to have sent gold sliding through the week. The desk's record-low positioning thesis was the right framework for a different CPI outcome. Had April inflation printed at 2.8%, this call might have been the best on the board as short-covering cascaded through a market at positioning extremes. Instead, the hottest inflation read since May 2023 validated every hawkish scenario the desk itself identified in the risk assessment. When your own report explicitly describes the downside catalyst and it materialises within 24 hours of the grading window opening, the grade will reflect the direction miss regardless of the thesis quality. Three consecutive missed calls on gold now if this week confirms what public data suggests. |

The Economic agent appears to have had the strongest week. Its bearish lean on gold, its identification of the CPI as the dominant catalyst across multiple markets, and its consistent focus on the stagflation dynamics that the 3.8% headline inflation number validated look prescient. CNBC confirmed the annual rate was the highest since May 2023, and the Economic agent's persistent warnings about elevated real yields creating headwinds for non-yielding assets landed with force.

The Institutional agent, which drove the gold bullish thesis through record-low positioning data, appears to have made a classic timing error. The positioning data was real, the capitulation was genuine, but calling the inflection point requires the macro catalyst to cooperate. The Fundamental agent's structural supply-demand work on copper (Grasberg offline) and soybeans (renewable diesel demand) may fare better, as those markets are less directly exposed to the CPI shock. The Sentiment agent flagged extreme complacency across equities with put/call at 0.53, and whether that contrarian warning finally proves correct during a week of hot inflation data is one of the more interesting questions for the final scorecard.

The damage from Monday's 3.8% CPI print will take weeks to fully ripple through positioning and expectations. Markets have priced out 2026 rate cuts entirely, with a meaningful probability of a Fed hike now on the table for the first time this cycle. That reshapes the calculus for every market on the desk's board. Gold faces the question of whether record-low positioning creates a floor or whether the inflation data triggers a fresh leg lower toward $4,300. Equities must reconcile record highs with the evaporation of their rate-cut safety net. Crude oil, already elevated from the Iran premium, now has an inflation tailwind alongside the geopolitical one. The June 16-17 FOMC, the first meeting where a new dot plot could reflect the CPI shock, becomes the next defining event. The desk will have its Sunday views. Given what Monday's data did to this week's carefully constructed theses, I expect some significant recalibration.