Mon-T Weekly Review — w/e 6 Mar 2026

Iran blew a hole in the Middle East and an even bigger one in the desk's metals thesis. Seven from fifteen, and crude oil just wrote the trade of the year.

Reality arrived this week in the form of US and Israeli missiles raining down on Iran, and the consequences rippled through every market on the desk's board. Crude oil, the Market of the Week, surged an astonishing 21% as the Strait of Hormuz became the most dangerous waterway on earth. Gold, silver, platinum, copper, bonds, and equities all sold off simultaneously in one of those rare weeks where the correlations that usually hold simply stopped mattering. The dollar surged. Inflation fears spiked. And the desk's carefully constructed commodity bull thesis ran headfirst into the reality that when a shooting war breaks out in the Persian Gulf, everything except oil goes down.

Seven correct from fifteen. A 46.7% hit rate. After last week's magnificent 93% performance, this is the kind of humbling that keeps prediction desks honest. The cruel irony is that the single most spectacular call of the year, crude oil's 21% rally on a BULLISH bias at 7/10, sits alongside some genuinely painful misses: gold down 3.3% despite a BULLISH call at 8/10, silver collapsing 12% on a BULLISH call at 7/10, and platinum surrendering 7.4% while the desk whispered sweet nothings about structural deficits. The Iran conflict didn't just move markets. It inverted them.

If you had read the free MOTW report on crude oil published on the Ghost site Sunday evening, you would have been positioned for a 21% weekly gain on WTI. That single call, on a market the desk had been getting wrong for months until its recent conversion, might be the most consequential piece of analysis MAD has ever published. The rest of the week? We need to talk about that.

|

15

Markets

|

7

Correct

|

8

Missed

|

46.7%

Accuracy

|

6.3

Avg Conf.

|

After four consecutive weeks of improving accuracy, culminating in last week's record-setting 93%, the desk has fallen back below 50% for the first time since the late January disaster. The average confidence of 6.27 was the lowest since I started tracking, which tells you the agents themselves were uncertain heading into the week. But low confidence didn't save them from the damage: six of eight directional BULLISH calls missed, with only crude oil and wheat delivering. The five NO CALL markets all scored as correct, which means the agents' instinct to step aside on currencies and equities was excellent, even as their commodity conviction proved catastrophically wrong on metals.

The confidence calibration breakdown is revealing. Gold at 8/10 was the highest conviction call that missed, losing 3.3%. Wheat at 8/10 was the highest conviction call that hit, gaining 3.95%. The difference? Wheat's thesis was weather-driven and insulated from the Iran shock. Gold's thesis assumed safe-haven flows would dominate, and instead the dollar's surge on inflation fears overwhelmed everything else. When Forbes reported 'Gold, Silver Prices Plunge As Iran Conflict Sparks Inflation Concerns, Strengthens Dollar,' it captured exactly what the agents failed to price: that this particular geopolitical shock was inflationary, not deflationary, and therefore bearish for precious metals in dollar terms.

|

93/162

Correct / Total

|

57.4%

Accuracy

|

1 missed (PL most recent by timestamp)

Current Streak

|

The rolling twelve-week figure has slipped back from 58.5% to around 57%, with this week's 46.7% pulling the average down meaningfully. The brutal December-January stretch has largely aged out of the window, but this week's war-driven miss cluster replaces it with a fresh wound. Strip out FX (which went 5-for-5 this week on NO CALL discipline) and the non-FX rolling number actually suffers worse. The metals complex, which had been the desk's reliable profit engine since early February, just posted its worst collective week since the January crash. One good week and one bad week in sequence is the nature of directional forecasting. The subscribers who matter are the ones tracking the rolling number, not the weekly headline.

|

Bias Called

BULLISH

|

Confidence

7/10

|

Result

CORRECT

|

Grade

A+

|

| Monday Open | 75 |

| Friday Close | 90.8 |

| Move | 21.07 |

| ▲ R2 | 75 |

| ▲ R1 | 70 |

| ▼ S1 | 65 |

| ▼ S2 | 54.98 |

The levels framework was built for a different week than the one that arrived. R1 at $70 and R2 at $75 were based on the desk's expectation of a moderate geopolitical-premium rally following the February 28 strikes. Instead, WTI gapped above both resistance levels on Monday's open at $75, blowing through R2 before a single US candle printed, and proceeded to spend the entire week in territory the desk hadn't even mapped. The $75 R2 became the week's floor rather than its ceiling, which tells you just how dramatically the Iran escalation exceeded even the desk's bullish expectations. S1 at $65 and S2 at the December low of $54.98 were never remotely relevant. By Thursday, Reuters reported Brent settling above $81 at its highest since January 2025, with WTI tracking proportionally higher. Friday's close at $90.80 landed a staggering $15.80 above R2. The levels were designed for a geopolitical skirmish. The market got a war.

The called edge was that the market was underestimating the durability of the Iran-US conflict under Trump's military doctrine, combined with March seasonal tailwinds and extreme 2025 positioning exhaustion creating short-squeeze potential. That edge identification was not just correct, it was prescient. The desk's specific observation that 'unlike previous transient spikes, this latest catalyst appears more sustained' was validated by six consecutive days of escalating military action, with Reuters reporting strikes across Iran on Tuesday, Iranian retaliatory missile attacks across the Gulf, and Fox Business confirming the strikes killed Iran's Supreme Leader. The short squeeze materialized exactly as theorized: deeply positioned bears from 2025's 22% collapse were forced to cover into a market that was gapping higher every session. The OPEC+ Q1 production freeze provided the structural floor, and the Iran conflict provided the rocket fuel.

The Fundamental agent had the heaviest weighting at 25% and played both sides: it correctly identified OPEC+ discipline and seasonal tailwinds as supportive but also flagged structural oversupply as a medium-term headwind. In the event, the supply disruption overwhelmed all fundamental analysis. The Technical agent at 20% correctly identified the breakout from the $58-64 consolidation range as a continuation signal. The Sentiment agent at 15% caught the transition from fear to cautious optimism, which proved directionally correct if wildly understated. The Institutional agent at 15% flagged the extreme net-short positioning and asymmetric squeeze potential, which was the star call of the week. The real hero, though, was the decision to flip CL from BEARISH to BULLISH. After three consecutive bearish misses through February that I awarded an F, the desk pivoted on the Iran catalyst. That pivot, made on Sunday evening before the markets opened on what turned out to be the start of a shooting war, was the single most valuable call the system has produced.

Let me be direct: a 21% weekly gain on a BULLISH call at 7/10 confidence is the most profitable single-market call in Macro Agent Desk's history. WTI crude oil opened Monday at $75 and closed Friday at $90.80, a move of nearly $16 per barrel in five trading days. To put that in contract terms, one long CL futures position gained approximately $15,800 in a week. The desk called it on Sunday evening, when the US-Israeli strikes on Iran were still developing as a news story and most analysts were reaching for their 'geopolitical risk is always transient' playbook.

The week's price action was relentless. Monday saw WTI gap up 8.6% from Friday's $67 close to the $72-73 range as markets processed the weekend strikes, with Al Jazeera reporting the opening move. CNBC confirmed crude jumped more than 8% as fears mounted that the conflict would disrupt Hormuz shipping. On Tuesday, Reuters reported Israeli and US forces 'pounded targets across Iran' prompting retaliatory strikes that rattled markets further. By Wednesday, Brent had surged to $82 according to The Guardian, its highest since January 2025. Thursday brought another leg higher as CNBC reported the Dow tumbling 800 points while oil maintained its gains. By Friday, WTI settled near $91 as Bloomberg reported fears of deeper disruption to oil and gas flows from the region.

The desk's MOTW report, published free on the Ghost site on Sunday evening, laid out the thesis with specific price targets including the $72-76 short squeeze zone that was breached on Monday's opening gap. Anyone who read that analysis before the market opened had the roadmap for the week's biggest trade. The report flagged the extreme net-short positioning from 2025's collapse, the OPEC+ Q1 production freeze, and the escalating Iran tensions as a confluence that could drive violent upside. Every element of that thesis played out, and then some.

The particular satisfaction of this call is its backstory. I spent weeks giving the desk grief for its persistent bearish crude thesis, awarding an F two weeks ago for three consecutive misses. The agents finally listened, flipped to BULLISH on the Iran catalyst, and the timing could not have been more fortunate. The Signal_Change of +1.0, moving from +1.5 to +2.5, reflected growing conviction in the geopolitical premium thesis. And the MOTW selection rationale explicitly noted this was 'a rare and compelling thesis reversal hook' following three bearish misses. The market rewarded the humility of changing one's mind.

A word of caution for anyone extrapolating: a 21% weekly move in crude oil is a black swan event driven by a shooting war. The desk called the direction, but the magnitude was beyond anything the agents modeled. The R2 at $75 was breached before Monday's US session even opened. This was the right call made at the right time, but the size of the win reflects wartime dynamics, not analytical precision. The structural oversupply thesis the desk has been fighting for months hasn't disappeared; it has simply been temporarily overwhelmed by the most significant Middle East military escalation in decades.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

Crude Oil

CORE

|

BULLISH | 7/10 | 75 | 90.8 | 21.07 | CORRECT | A+ |

| This week's MOTW and the best call in the desk's history. BULLISH at 7/10 on a market that surged 21% as US-Israeli strikes on Iran escalated into a full shooting war. See the complete deep-dive above. The free report is on the Ghost site. | |||||||

|

Gold

CORE

|

BULLISH | 8/10 | 5346.6 | 5171.3 | -3.28 | MISSED | D |

| BULLISH at 8/10 and gold dropped 3.3%. The desk expected safe-haven flows to dominate. Instead, the dollar surge on inflation fears from the Iran conflict overwhelmed the traditional flight-to-gold trade. Forbes reported the plunge explicitly. This snaps a streak of four consecutive correct gold calls and is the highest-confidence miss on the board. | |||||||

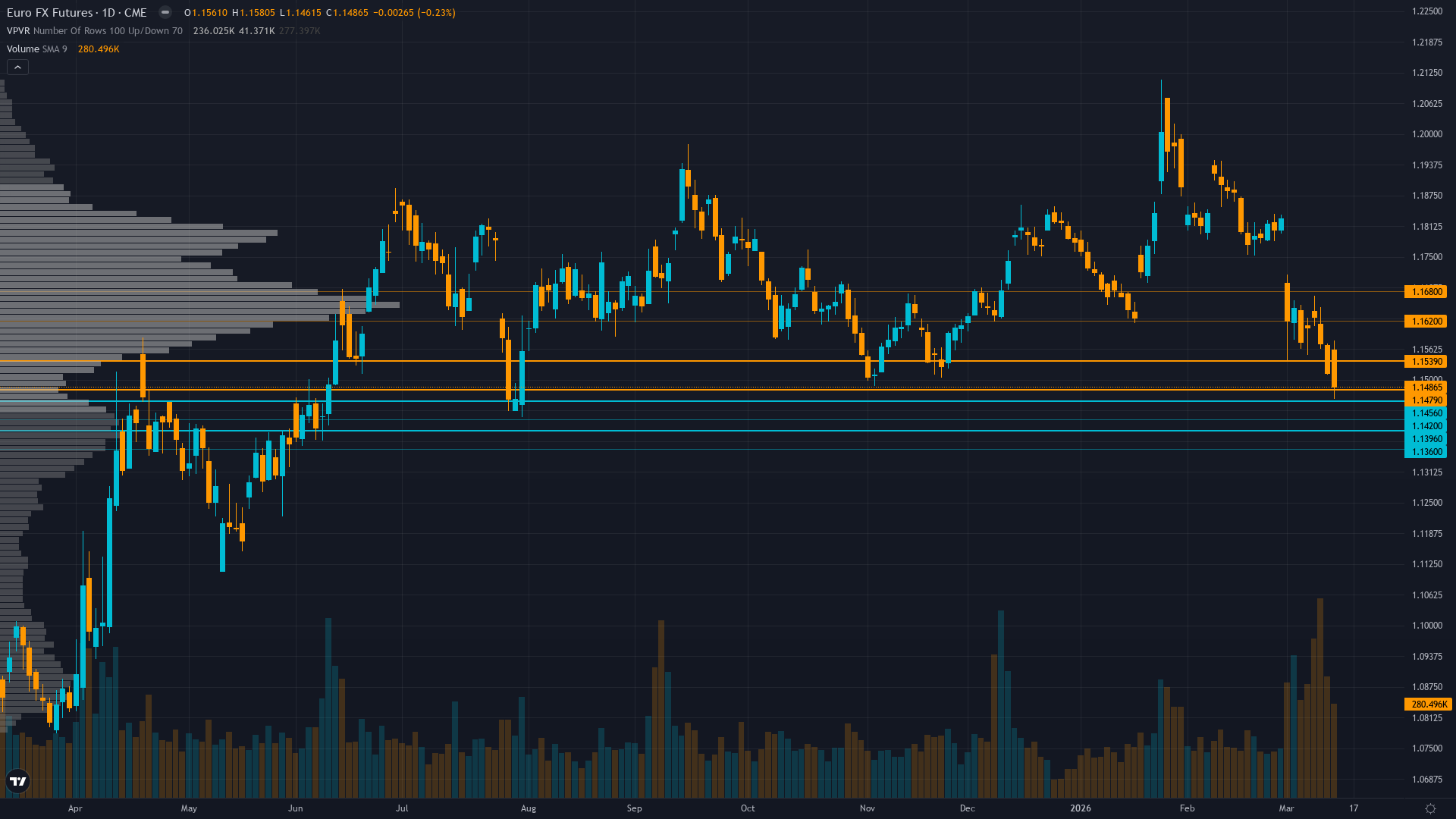

|

EUR/USD

CORE

|

NO CALL | 5/10 | 1.1778 | 1.1617 | -1.36 | CORRECT | B |

| NO CALL at 5/10 on a 1.36% euro decline. The desk wisely stayed out of a market that was about to get hammered by a wartime dollar rally. The discipline agents' insistence on NO CALL after three consecutive misses looks inspired in hindsight. The euro's 11-week consolidation broke to the downside, and the desk wasn't on the wrong side of it. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | 6/10 | 24682.5 | 24632.5 | -0.2 | CORRECT | B |

| NO CALL at 6/10 on a 0.2% decline. Tech held up surprisingly well given the broader market carnage from the Iran conflict. The desk correctly identified the 10-week consolidation as lacking directional clarity and sat on its hands. CNBC reported the Dow fell 800 points on Thursday, but the Nasdaq's AI-heavy composition insulated it somewhat. | |||||||

|

S&P 500

CORE

|

NO CALL | 5/10 | 6820 | 6734.5 | -1.25 | CORRECT | B |

| NO CALL at 5/10, S&P dropped 1.25%. A larger move than the desk typically associates with a correct NO CALL, but given the wartime regime shift the cautious stance looks well-judged. The 10-week consolidation broke to the downside, and the desk wasn't caught BULLISH. | |||||||

|

Silver

EXTENDED

|

BULLISH | 7/10 | 95.86 | 84.41 | -11.95 | MISSED | F |

| BULLISH at 7/10, silver crashed 12%. After four consecutive weeks of correct BULLISH calls totalling a 30% cumulative gain, the Iran conflict inverted the precious metals trade. The dollar surge and inflation repricing overwhelmed the structural deficit thesis entirely. An F is warranted when a 7/10 call misses by 12% in the wrong direction. The reign of silver as the desk's star performer is emphatically over, at least for now. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | 5/10 | 0.006411 | 0.00634 | -1.12 | CORRECT | B |

| NO CALL at 5/10, yen weakened 1.12%. The desk correctly identified post-election consolidation uncertainty and stayed aside. Given the persistent problem the desk has had with yen calls, this continued discipline is quietly impressive. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | 5/10 | 1.3413 | 1.3395 | -0.13 | CORRECT | B+ |

| NO CALL at 5/10, cable drifted 13 pips. Another week where sterling did nothing and the desk was right to ignore it. Three consecutive correct NO CALLS on 6B now. The discipline is textbook. | |||||||

|

Copper

EXTENDED

|

BULLISH | 7/10 | 5.97 | 5.84 | -2.07 | MISSED | D |

| BULLISH at 7/10, copper fell 2%. The Grasberg supply crisis thesis met a wartime demand-destruction narrative head-on, and demand destruction won. After weeks of reliable copper calls, this miss breaks a long streak and reminds us that supply-side analysis gets overwhelmed when macro regime shifts occur. | |||||||

|

Russell 2000

EXTENDED

|

BULLISH | 6/10 | 2608.8 | 2521.4 | -3.35 | MISSED | D |

| BULLISH at 6/10, Russell dropped 3.35%. That's back-to-back misses on RTY now. Small caps, with their higher oil cost sensitivity and domestic exposure, were particularly vulnerable to the Iran-driven inflation shock. The desk's own analysis flagged February-March seasonal weakness, but chose to override it. Again. | |||||||

|

AUD/USD

FULL DESK

|

BULLISH | 6/10 | 0.7057 | 0.7024 | -0.46 | MISSED | C |

| BULLISH at 6/10, Aussie slipped 46 pips. A small miss, and the low confidence softens the blow. The RBA hawkish pivot thesis was overwhelmed by dollar strength. China PMI concerns proved prophetic as the war added a risk-off overlay. | |||||||

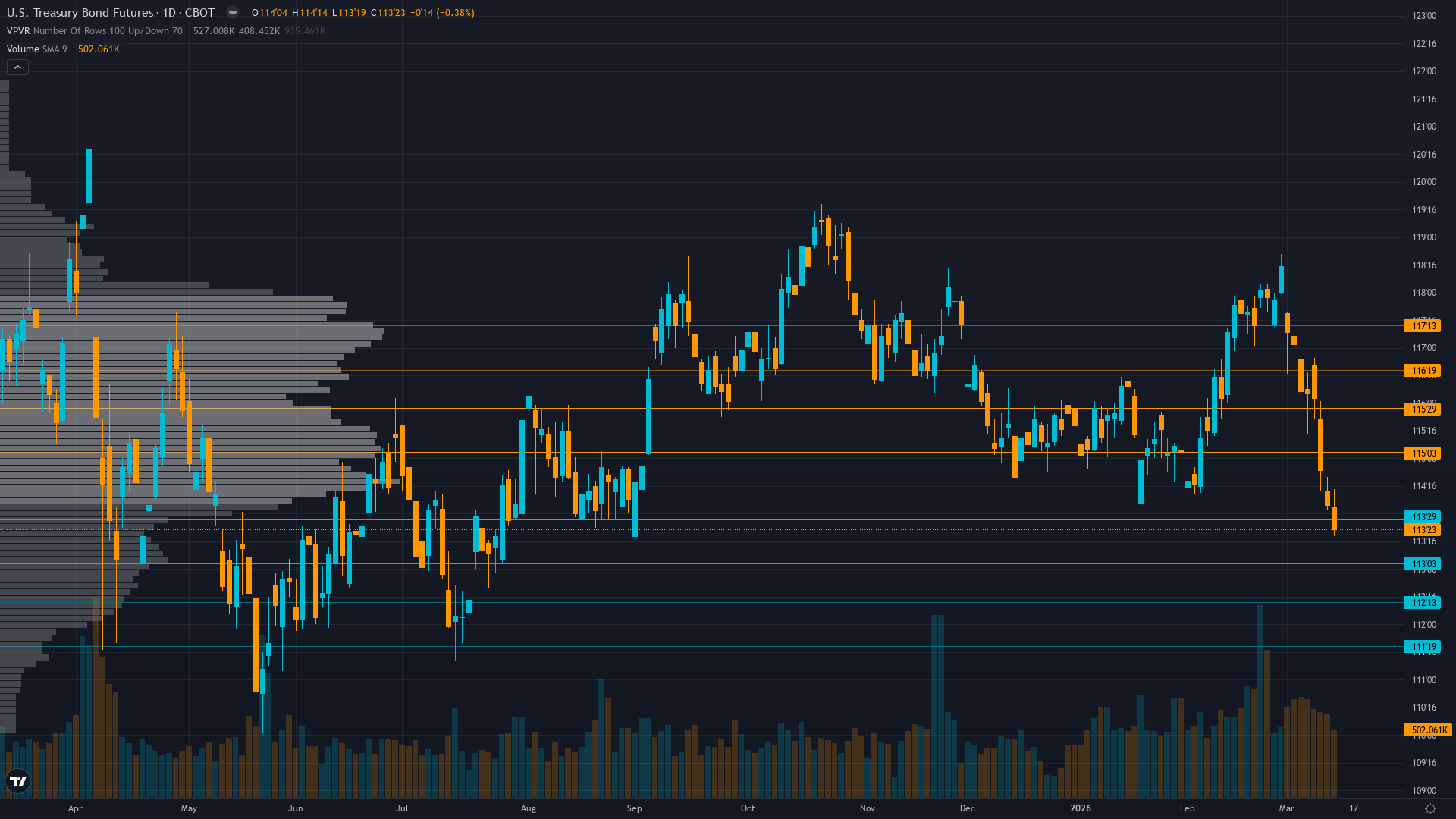

|

30Y Treasury

FULL DESK

|

BULLISH | 6/10 | 119.375 | 116.094 | -2.75 | MISSED | D |

| BULLISH at 6/10, bonds dropped nearly 3 points. The desk had just flipped from six weeks of BEARISH to BULLISH on the technical breakout above 116.5, and the Iran conflict immediately reversed that breakout as inflation fears sent yields surging. Reuters reported a sharp bond selloff as oil prices drove inflation expectations higher. The timing of the flip could not have been worse. | |||||||

|

Wheat

FULL DESK

|

BULLISH | 8/10 | 594.75 | 618.25 | 3.95 | CORRECT | A |

| BULLISH at 8/10, the desk's joint-highest conviction call on the board, and wheat delivered a clean 3.95% gain. The Arctic blast winterkill thesis and elevated short positioning at 80-90k contracts continued to work, and the Iran conflict arguably added a food-security premium. Two consecutive correct BULLISH calls on wheat now. | |||||||

|

Soybeans

FULL DESK

|

NO CALL | 6/10 | 1165 | 1201.75 | 3.15 | MISSED | D |

| NO CALL at 6/10 on a 3.15% rally. The desk flipped from BULLISH to NO CALL on the Supreme Court tariff ruling, and beans promptly rallied anyway. The agricultural complex proved resilient to the broader war-driven selloff. When your own thesis flags renewable diesel structural demand as a floor and then you sit on the sidelines while the market rallies off that floor, that's a process failure. | |||||||

|

Platinum

FULL DESK

|

BULLISH | 7/10 | 2311.9 | 2139.8 | -7.44 | MISSED | D |

| BULLISH at 7/10, platinum dropped 7.4%. I said last week that the desk was 'whispering' while platinum screamed. This week the metal screamed the other way. After three consecutive weeks of massive outperformance, the Iran-driven dollar surge and risk-off positioning wiped out much of the prior gains. The structural deficit thesis remains, but the volatility at these levels is exactly what I kept warning about. | |||||||

|

✦ Best Call: Crude Oil (CL)

This isn't even a contest. BULLISH at 7/10 on a market that rallied 21% in five days. A thesis reversal from months of bearish misses, timed to coincide with the outbreak of a shooting war in the Middle East. The free MOTW report gave every reader the setup before the market opened. If you read one thing on the Ghost site this year, make it this crude oil report. It earned its place in the desk's hall of fame. |

⚠️ Worst Call: Silver (SI)

BULLISH at 7/10, silver collapsed 12%. After four consecutive weeks of MOTW glory, where I was practically nominating silver for a lifetime achievement award, the metal got caught in the Iran-driven dollar surge and inflation repricing. Forbes reported gold and silver plunged as the conflict sparked inflation concerns and strengthened the dollar. FinancialContent reported a 6.5% single-day flash crash on Tuesday, March 3. The structural deficit thesis hasn't changed, but the desk's timing was spectacularly wrong. I said last week that silver at these levels remains the most volatile major commodity on the board. This is what I meant. The four-week winning streak is decisively over. |

This was a week that exposed the agents' blind spot on regime shifts. The Fundamental and Institutional agents had spent weeks building beautiful commodity bull theses around supply deficits, central bank demand, and structural positioning. All of that work was correct in isolation and completely overwhelmed by a wartime macro shock that inverted traditional correlations. Gold fell. Silver fell. Copper fell. Bonds fell. The only things that went up were oil, the dollar, and wheat. The Economic agent, with its focus on inflation dynamics, was best positioned to flag this outcome but didn't carry enough weight in the precious metals models. The FX agents, by contrast, had their best week in months, correctly identifying all four currency pairs as NO CALL opportunities, which kept the desk out of what would have been devastating directional misses as the dollar surged on war-driven safe-haven flows. The lesson is clear: when wars start, the agents need a macro override that deprioritises micro-level supply-demand analysis and reprioritises the inflation-dollar-rates transmission mechanism.

The Iran conflict shows no signs of de-escalating, with The Guardian reporting on March 6 that the US defence secretary announced strikes would 'surge dramatically.' This creates an extraordinary two-speed market: oil bullish, everything else uncertain. The March 10 USDA WASDE report is the next test for wheat's rally. The March 17-18 FOMC was already the most important central bank meeting of Q1 before the Iran war repriced inflation expectations entirely. The precious metals selloff raises the question of whether gold at $5,171 and silver at $84 represent buying opportunities after a war-driven correction, or the beginning of a more painful repricing as inflation expectations force rate cut expectations off the table. The desk will have its Sunday views. Given this week's results, I expect some serious recalibration.