Mon-T Weekly Review — w/e 21 Feb 2026

The desk is back, silver smashes through R1, and the FX complex reminds everyone that currencies have feelings too.

Mon-T Weekly Review — w/e 21 Feb 2026

After last week's pipeline failure, where I sat in the reviewer's chair with nothing to review, the desk returned with a full fifteen-market slate and promptly delivered what can only be described as a mixed bag. Nine correct from fifteen, a 60% hit rate that sits firmly in the 'acceptable but not celebratory' category. The metals complex continued its remarkable run, silver exploded nearly 10% higher, and platinum printed a jaw-dropping 7.8% weekly gain. But the FX desk had a properly bad week, whiffing on all four currency pairs that carried a directional call.

The pattern is becoming unmistakable. When the agents point at shiny things and say 'buy,' they tend to be right. When they point at currency pairs and say 'buy,' they tend to be wrong. The euro, yen, sterling, and Aussie dollar all received BULLISH calls, and all four went the wrong way. That's not bad luck. That's a systemic issue. Meanwhile, crude oil continued its campaign to humiliate the desk's bearish thesis, rallying nearly 5% while the agents shouted into the wind about structural oversupply.

The bright side? The desk is back on the pitch after forfeiting last week, and when it has genuine conviction on commodities and metals, the results speak for themselves. Silver's +9.2% move as MOTW is the kind of headline number that earns its keep. Copper put up 3.5%. Platinum surged 7.8%. Even gold managed nearly a percent, which for gold at $5,000 is a meaningful move. The desk knows its metals. It just needs to stop pretending it knows where the euro is going.

Weekly Scorecard

Sixty percent is below the 80% we celebrated two weeks ago, and the average confidence of 6.67 reflects the desk's own uncertainty heading into a week with few scheduled catalysts. The distribution tells the real story: eight of nine correct calls came from commodities, metals, and equity indices. Every single FX directional call missed. That's a zero for four on currencies, which is the kind of performance that turns a good week into a middling one.

The confidence calibration was poor on the misses. CL was called BEARISH at 7/10, which is meaningful conviction, and crude rallied 4.88%. That's now three consecutive BEARISH misses on crude oil, and the desk still hasn't figured out that being fundamentally right about oversupply doesn't mean being directionally right about price. Wheat's NO CALL at 7/10 missed a 4.61% surge, which stings. When you issue a NO CALL on a market that moves nearly 5% in a week, the confidence number beside it becomes somewhat academic.

Rolling 12-Week Record

The rolling twelve-week figure has crept up to around 58%, recovering gradually from the dismal December stretch that dragged the average into the low fifties. This week's 60% helps rather than hurts, and the metals complex continues to be the desk's bread and butter. But the FX record over the rolling window is genuinely concerning. The yen in particular has been a persistent problem, with the desk going BULLISH on yen strength week after week and the market going the other way almost every time. The crude oil bear thesis has also cost the rolling record dearly. Strip out FX and crude, and the desk is running at roughly 72% on everything else. That disparity is worth noting.

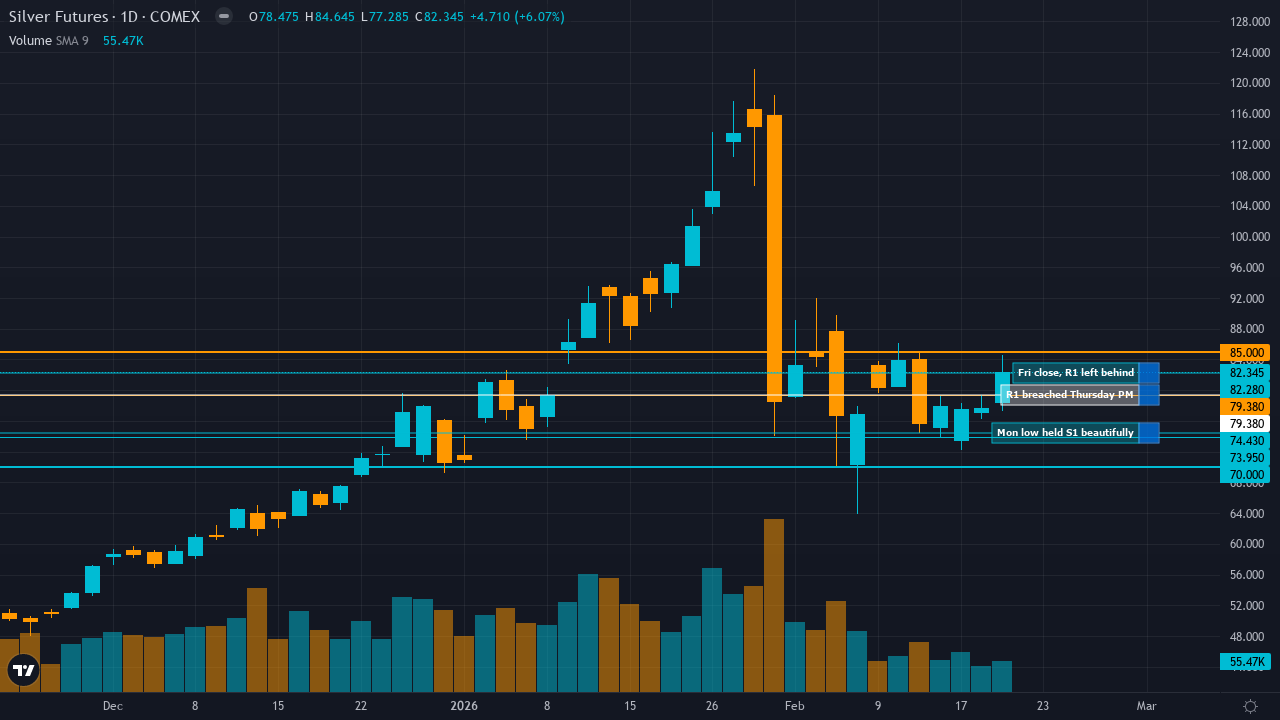

★ Market of the Week: Silver (SI)

Price Action

| Monday Open | 75.35 |

| Friday Close | 82.283 |

| Move | 9.2 |

Called Levels vs Reality

| ▲ R2 | 85.00 |

| ▲ R1 | 79.38 |

| ▼ S1 | 73.95 |

| ▼ S2 | 70.00 |

R1 at $79.38 was breached emphatically. Silver opened the week soft near $75.35, dipped as low as $74.43 on Monday according to Fortune's morning report, then staged a ferocious rally through the rest of the week. By Thursday, Fortune reported the spot price at $78.06, and by Friday morning it was trading at $80.46 per ounce. The Friday futures close at $82.28 blew clean through R1 and was pushing toward R2 at $85.00. S1 at $73.95 was briefly threatened on Monday's weakness but held, providing exactly the kind of floor the desk identified. S2 at $70.00 was never remotely in play. The levels framework worked exceptionally well here, with S1 catching the intraweek low and R1 serving as a waypoint on the path to an explosive finish.

Edge Review

The called edge centred on the market treating the January flash crash and CME margin interventions as secular bull termination rather than a regulatory disruption within a structural uptrend. The desk argued that the fifth consecutive year of deficit, permanent 59% industrial demand share, and China's export restrictions controlling 60-70% of global supply created a new equilibrium above $75-80. That thesis was vindicated comprehensively. Silver's transition from February weak seasonality into March-April strength, which the desk flagged as a catalyst, appears to be arriving ahead of schedule. The edge identification that consensus was dismissing the permanence of the supply-demand paradigm shift proved accurate, with buyers stepping in aggressively at the low end of the $73-79 consolidation zone and driving prices through the upper boundary.

Agent Spotlight

The Fundamental agent was the star this week, carrying a 35% weighting, the heaviest allocation on the board. Its focus on the structural supply deficit entering its fifth consecutive year and China's export weaponisation provided the backbone for the bullish thesis. The Technical agent correctly identified the $73-79 consolidation zone and the breakout potential, earning its 15% weight. The Sentiment agent, reading neutral despite extreme volatility at the 88th percentile, was perhaps too cautious but didn't actively mislead. The Options agent flagged call interest in the $80-90 strikes suggesting institutional expectation for a rebound, and that proved spot on. The Economic agent, weighted at 20%, correctly identified that the broader macro backdrop was supportive without being the primary driver. No agent got this badly wrong, which is why the call worked.

Full Commentary

Silver has now been the Market of the Week three times running, and if anyone is tired of reading about it, I can only apologise and point to the returns. A 9.2% gain from Monday open to Friday close is not a market that politely asks for attention. It demands it.

The week's price action told a compelling story of accumulation at the lows and explosive breakout at the highs. Silver opened the week near $75.35, dipped to around $74.43 on Monday morning per Fortune's tracking, then began its climb. By Wednesday the metal was testing $78 on strong buying interest, and Thursday's Fortune report showed it at $78.06. Then came Friday, when silver surged to $80.46 in the morning session and the futures closed at $82.28. That's a $7 move in five days on a contract where normal weekly ranges have been running $5-6 during this volatility regime. The desk's R1 at $79.38 was blown through on the way up, which is unusual. In the prior week, R1 at $78.50 nearly perfectly capped the Friday close. This time, the metal treated R1 as a speed bump rather than a ceiling, suggesting the consolidation phase the desk identified has resolved to the upside.

The free MOTW report published on the Ghost site Sunday evening laid out the bull case with specific levels and a thesis centred on China's export restrictions and structural industrial demand. Readers who had that analysis before Monday's open were positioned to buy the $74-75 dip and ride the breakout through R1. That is precisely the kind of value proposition the desk aims to deliver, and this week it delivered it emphatically. LiteFinance noted silver at $84.57 as of February 21, and Investing.com showed COMEX futures trading in the $82-83 range. The 52-week range of $29.12 to $121.79 gives you a sense of the extraordinary ride silver has been on, and current prices sit comfortably in the upper third of that range.

The structural thesis remains unchanged. Fifth year of deficit. Industrial demand consuming 59% of supply and growing. China controlling 60-70% of tradeable supply with export restrictions operational since January 1. The CME's margin interventions may have temporarily capped speculative excess, but they haven't altered the fundamental picture. The desk's argument that the market was treating the January crash as secular bull termination rather than regulatory intervention has been validated by three consecutive weeks of higher closes.

A word of caution: silver at these levels remains the most volatile major commodity on the board, with annualised implied volatility at the 88th percentile. A 9% gain this week could easily become a 9% loss next week if positioning shifts or the CME decides to intervene again. The desk's confidence at 7/10 was well-calibrated for the risk profile. This was a strong call, well executed, and the free report gave every reader the tools to act on it.

All Market Grades

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

Gold

CORE

|

BULLISH | 8/10 | 5020 | 5059.3 | 0.78 | CORRECT | B |

| BULLISH at 8/10, gold delivered a modest 0.78% gain. Direction correct, but the confidence was perhaps a touch heavy for the size of the move. At $5,000+ per ounce, even small percentage moves represent real money, and the thesis about central bank structural demand continues to underpin the floor. Three consecutive correct weeks for gold. | |||||||

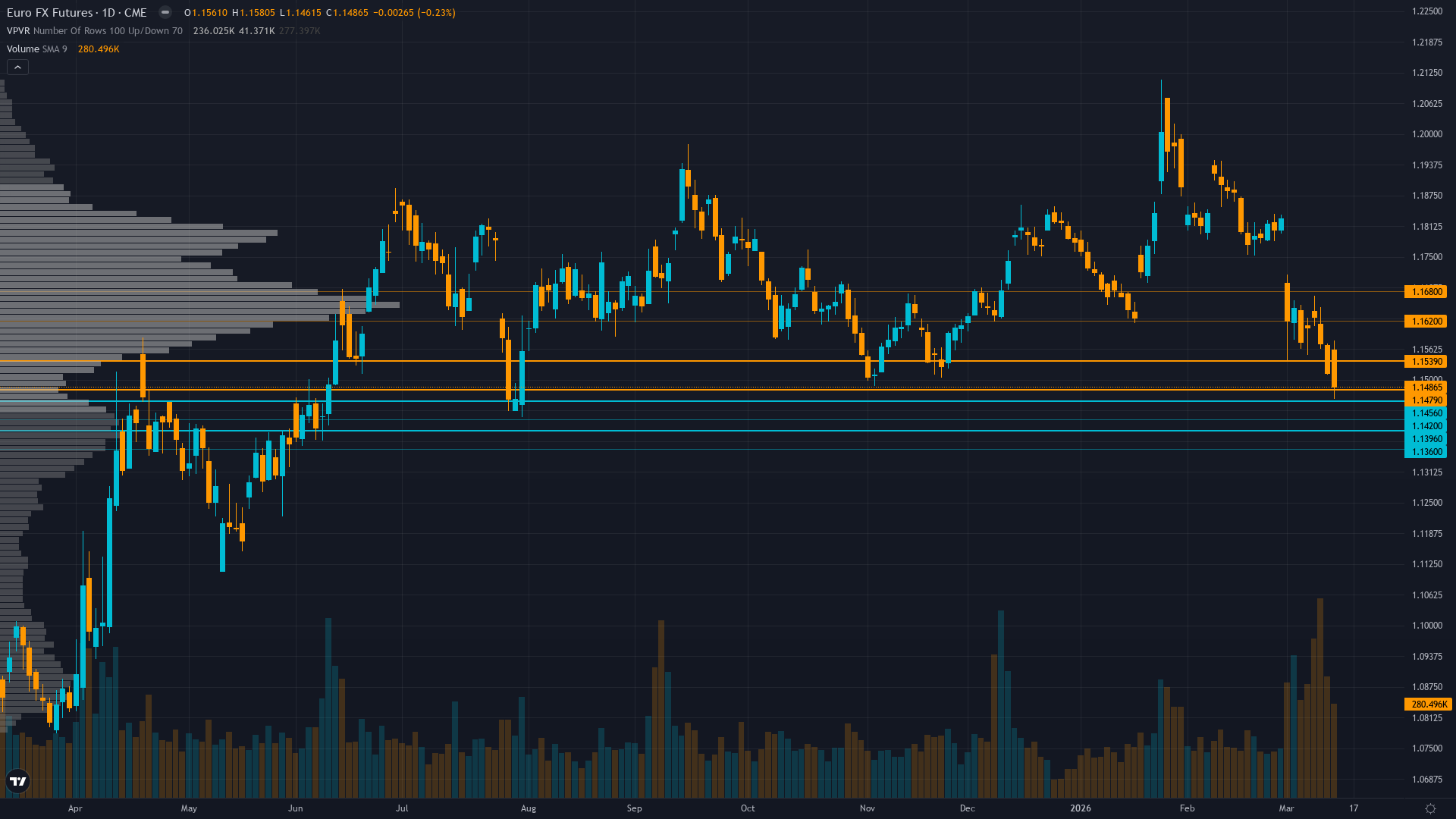

|

EUR/USD

CORE

|

BULLISH | 6/10 | 1.1885 | 1.1793 | -0.77 | MISSED | C |

| BULLISH at 6/10 and the euro dropped 77 pips. The desk's consolidation thesis was correct, but the direction was wrong. Low confidence softens the blow somewhat, but this adds to a mounting pile of FX misses that the agents need to address. | |||||||

|

Crude Oil

CORE

|

BEARISH | 7/10 | 63.3 | 66.39 | 4.88 | MISSED | F |

| Three consecutive BEARISH misses. BEARISH at 7/10 while crude rallied nearly 5% on Iran geopolitical risk and OPEC+ discipline. This is the desk's worst-performing market by a considerable margin. The structural oversupply thesis may be correct on a twelve-month horizon, but week after week the market goes the other way. An F is warranted when you miss by 5% at 7/10 confidence for the third time running. | |||||||

|

Nasdaq 100

CORE

|

BEARISH | 6/10 | 24789.75 | 25067.5 | 1.12 | MISSED | D |

| BEARISH at 6/10, the Nasdaq rallied 1.12%. After the NO CALL miss two weeks ago, the desk tried calling the direction this time and got it wrong again. The AI spending concerns may be real, but the market keeps buying the dip. Two consecutive NQ misses now. | |||||||

|

S&P 500

CORE

|

NO CALL | 5/10 | 6852.5 | 6923.25 | 1.03 | CORRECT | B |

| NO CALL at 5/10 on a 1% rally. Technically correct, and the desk's lowest confidence call on the board. ES drifted higher without drama. The desk wisely stayed on the sidelines rather than forcing a view with minimal conviction. | |||||||

|

Silver

EXTENDED

|

BULLISH | 7/10 | 75.35 | 82.283 | 9.2 | CORRECT | A+ |

| This week's MOTW and the best call on the board for the third consecutive graded week. A 9.2% gain on BULLISH at 7/10. See the full deep-dive above. The free report on the Ghost site laid out the thesis and the levels in advance. | |||||||

|

USD/JPY

EXTENDED

|

BULLISH | 6/10 | 0.006568 | 0.006458 | -1.67 | MISSED | D |

| BULLISH yen at 6/10 and the yen weakened 1.67%. That's a meaningful miss. The desk's persistent bullish yen bias has now been wrong more often than right over the rolling window. The post-election Takaichi policy uncertainty thesis has not translated into yen strength as the agents expected. | |||||||

|

GBP/USD

EXTENDED

|

BULLISH | 7/10 | 1.3652 | 1.3485 | -1.22 | MISSED | D |

| BULLISH at 7/10, sterling fell 1.22%. The BoE hawkish hold thesis did not translate into pound strength this week. A 1.2% miss at 7/10 confidence is a genuine error, not noise. | |||||||

|

Copper

EXTENDED

|

BULLISH | 7/10 | 5.6345 | 5.831 | 3.49 | CORRECT | A |

| BULLISH at 7/10, copper delivered a strong 3.49% gain. The Grasberg supply crisis thesis continues to work, and the desk has been consistently right on copper for weeks. Bloomberg reported in January that copper prices topped $14,500 per ton for the first time ever. The desk keeps catching these moves. | |||||||

|

Russell 2000

EXTENDED

|

BULLISH | 7/10 | 2650.9 | 2668.8 | 0.68 | CORRECT | B |

| BULLISH at 7/10 for a modest 0.68% gain. Direction correct, small move. The small-cap breakout thesis remains intact and the desk continues to catch the right side of the RTY tape, even if the weekly moves are modest. | |||||||

|

AUD/USD

FULL DESK

|

BULLISH | 7/10 | 0.7067 | 0.7078 | 0.16 | CORRECT | C+ |

| BULLISH at 7/10 for a 16-pip gain. Technically correct, but the move is so small it barely registers. The RBA rate hike thesis provided a floor but not a springboard this week. Given the FX carnage elsewhere, the Aussie gets partial credit for at least going in the right direction. | |||||||

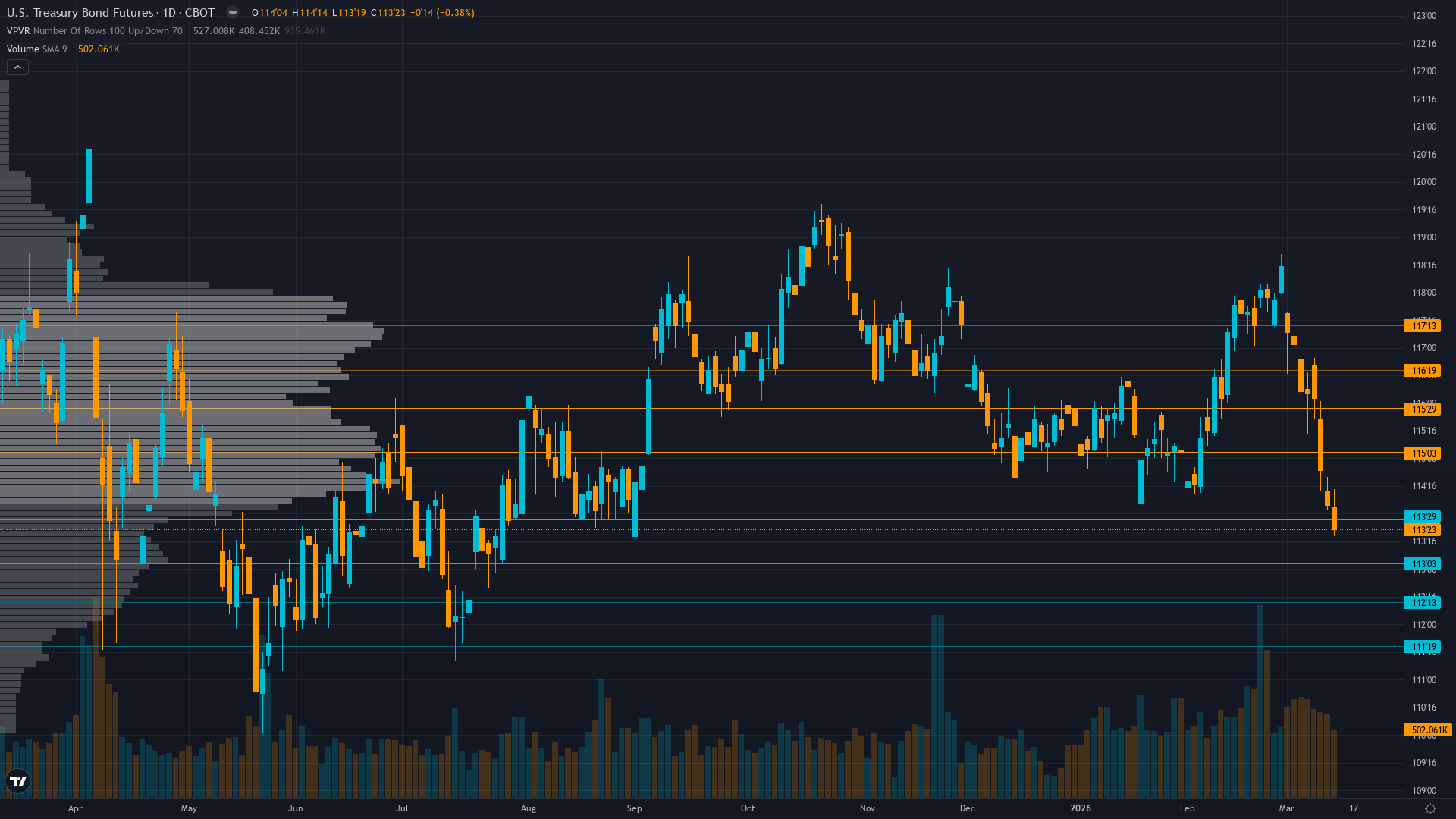

|

30Y Treasury

FULL DESK

|

BEARISH | 7/10 | 117.81 | 117.41 | -0.34 | CORRECT | B+ |

| BEARISH at 7/10, bonds fell 0.34%. Direction correct, modest move. The desk's conviction was dropped from its usual 9/10 to 7/10, which was sensible given the prior week's 2% miss in the wrong direction. The recalibration paid off with a cleaner result. | |||||||

|

Wheat

FULL DESK

|

NO CALL | 7/10 | 548.25 | 573.5 | 4.61 | MISSED | D |

| NO CALL on a 4.61% rally. The desk flagged Black Sea winterkill concerns and extreme short positioning as potential catalysts for a squeeze, then issued a NO CALL anyway. That is the kind of internal contradiction that turns a useful insight into a missed opportunity. The thesis was right. The call was wrong. | |||||||

|

Soybeans

FULL DESK

|

BULLISH | 7/10 | 1132.25 | 1137.5 | 0.46 | CORRECT | B |

| BULLISH at 7/10 for a marginal 0.46% gain. Direction correct, tiny move. The Trump-Xi 20 MMT upgrade thesis keeps beans supported, but execution uncertainty means the market is grinding rather than breaking out. Two consecutive correct weeks on soybeans. | |||||||

|

Platinum

FULL DESK

|

BULLISH | 6/10 | 2012.5 | 2169.7 | 7.81 | CORRECT | A+ |

| BULLISH at only 6/10, platinum delivered a massive 7.81% gain. Fortune reported platinum around $2,055-2,058 midweek before the rally accelerated into Friday. The confidence was far too low for the move that materialised. After the catastrophic 24% miss in late January and a 4% miss the following week, the desk has been gun-shy on platinum conviction. The metal has now proven the structural bull case twice in a row, and the desk needs to start trusting its own thesis with appropriate confidence. | |||||||

Highlights

|

✦ Best Call: Silver (SI)

For the third consecutive graded week, silver takes best call honours. A 9.2% gain on a BULLISH call at 7/10, with R1 cleanly breached and S1 holding the Monday dip to the dollar. The MOTW free report continues to justify the subscription all on its own. If you are reading this review without having read the Silver deep-dive first, you are doing it backwards. |

⚠ Worst Call: Crude Oil (CL)

BEARISH at 7/10, crude rallied 4.88%. That is now three consecutive bearish misses on CL, and the desk's structural oversupply thesis is starting to look like the economist who correctly predicted 12 of the last 3 recessions. CNBC reported on February 19 that oil prices rose on Trump potentially deciding to attack Iran within 10 days, a geopolitical wildcard the agents' models simply do not capture. The OPEC+ production freeze, seasonal tailwinds, and geopolitical risk premiums keep overwhelming the bearish fundamental case. At some point, being right about the fundamentals and wrong about the price for three straight weeks means you are just wrong. |

Agent Performance

The Fundamental agent dominated this week's winning calls, particularly across the metals complex where its supply-demand analysis drove correct BULLISH calls on silver (+9.2%), platinum (+7.8%), copper (+3.49%), and gold (+0.78%). The Technical agent provided useful support with its consolidation-to-breakout frameworks, particularly on silver where the $73-79 range resolved exactly as predicted. The weakest performance came from the Economic agent's contribution to FX calls, where its focus on central bank rate differentials and policy convergence narratives failed to capture the actual currency movements. Every FX pair moved against the desk's BULLISH bias, suggesting the weighting given to economic drivers in currency markets needs recalibration. The Sentiment agent's neutral readings across most markets were unhelpful but not harmful. The real problem child remains the collective assessment on crude oil, where every discipline agrees on bearish fundamentals while the market persistently disagrees.

Looking Ahead

March is approaching fast, and with it comes a wall of central bank meetings: Fed FOMC on March 17-18, ECB on March 18-19, and BOJ on March 19. That cluster of events will either validate the desk's range-bound currency views or force a rethink. The precious metals complex enters March on a wave of momentum, and the desk's thesis about weak February seasonality transitioning to March-April strength looks prescient. Wheat's 4.6% surge this week, which the desk missed with a NO CALL, deserves attention. If Black Sea weather concerns intensify, that market could be one of the more interesting stories in the ags space. The Nasdaq bounced 1.12% while the desk called it BEARISH, which is the second consecutive direction miss on tech. AI spending concerns may be real, but the market keeps finding reasons to buy the dip. The desk will have its Sunday views. I will be here next week with a red pen.