Mon-T Weekly Review — w/e 14 Mar 2026

Ten from fifteen, the S&P bearish call lands, and the Iran war turns crude into a one-way street while wheat gets winterkilled by reality.

Two weeks ago the desk handed in the worst scorecard I have ever graded, a 46.7% horror show that featured a 21% crude oil moonshot and a 12% silver crater sitting side by side on the same page. This week, the system recalibrated. Ten correct from fifteen, a 66.7% accuracy rate, and a much more disciplined posture that leaned heavily on NO CALL where conviction was thin. The Iran war continued to dominate every asset class, oil punched through $98 on its way toward triple digits, and the S&P 500 posted its third consecutive losing week as CNBC's headline writers ran out of new ways to say 'new low for 2026.'

The standout feature of this week's performance is restraint. Eight of fifteen calls were NO CALL, and five of those eight were graded correct. The desk appears to have internalised the lesson from two weeks ago: when a shooting war in the Persian Gulf is rewriting correlations in real time, the smartest thing you can say about most markets is 'I don't know.' That said, the seven directional calls that were issued produced five winners, including the MOTW bearish call on ES and the continued crude oil bull thesis, demonstrating the system still has teeth when it commits.

The misses tell a familiar story. Gold, called bullish at 6/10, dropped 1.8% as the dollar's war premium continued to outmuscle traditional safe-haven flows. Wheat, the desk's highest conviction call at 8/10, fell 3.4% as the March WASDE apparently disagreed with the Arctic blast winterkill thesis. And platinum lost another 5.9% despite being downgraded to NO CALL, which is technically a miss but honestly looks more like the market punishing anyone who dared to own precious metals during an oil crisis.

|

15

Markets

|

7

Directional

|

5

Correct

|

71.4%

Accuracy

|

8

No Calls

|

Seven directional calls this week, with five landing on the right side. The other eight markets got the NO CALL treatment. A 71.4% directional accuracy rate is a proper bounce-back from the 46.7% war-week disaster, and the average confidence of 6.14 on those directional calls tells you the desk was appropriately measured rather than swinging for the fences.

The confidence calibration story is encouraging despite the misses. Wheat at 8/10 was the highest conviction call and it missed by 3.4%, which is painful. But ES at 6/10 BEARISH, the week's most consequential correct call, landed a clean 0.74% decline. Bonds at just 5/10 BEARISH delivered the biggest move among correct calls at nearly 2%. The pattern from last week's review holds: when the desk commits with measured conviction on macro regime calls, it tends to be right. When it leans into micro-level supply thesis against a wartime macro backdrop, it tends to be wrong.

|

67/123

Correct / Total

|

54.5%

Accuracy

|

123 / 40

Directional / No Call

|

The rolling twelve-week figure sits at 54.5% across 123 directional calls, with 40 no-call abstentions showing the desk knows when to sit on its hands. The brutal December-January stretch continues to weigh on this number, though it is slowly aging out of the window. This week's 71.4% directional performance helps, but one good week cannot undo months of scar tissue. If the desk strings together another two or three weeks above 65%, we should finally break through the 57-58% ceiling that has felt like a permanent residence since late February.

|

Bias Called

BEARISH

|

Confidence

6/10

|

Result

CORRECT

|

Grade

B+

|

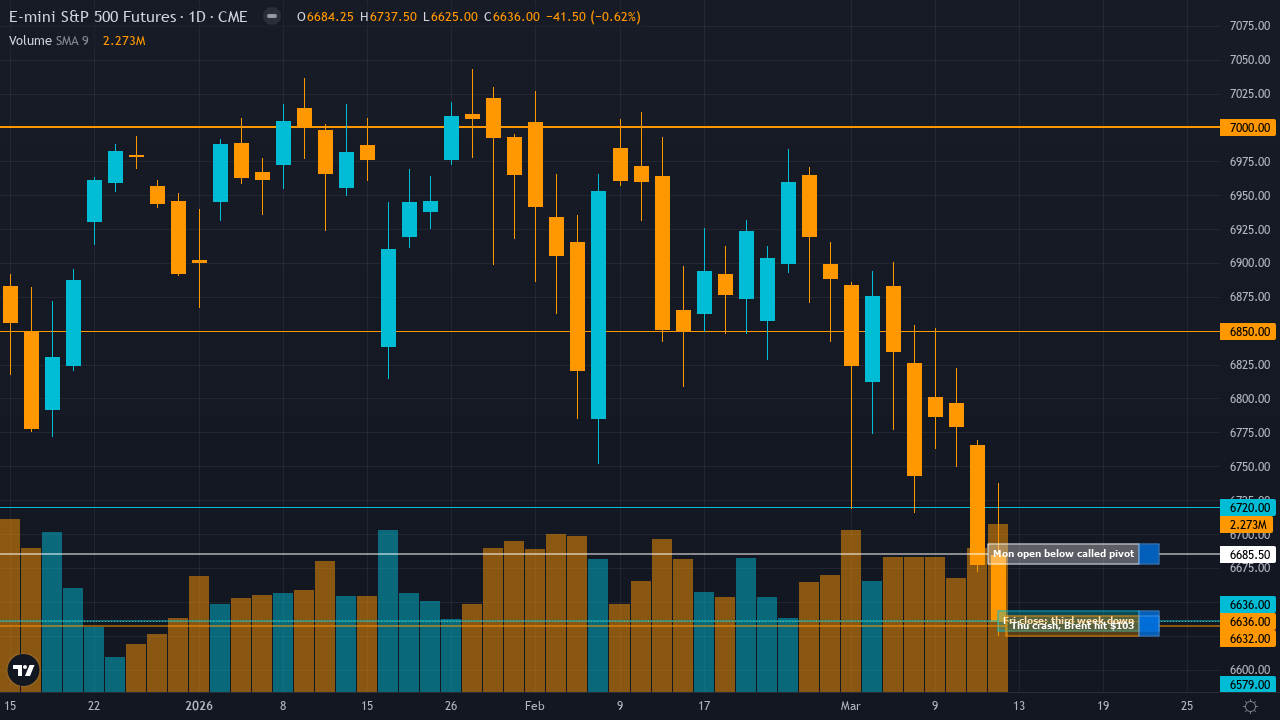

| Monday Open | 6685.5 |

| Friday Close | 6636 |

| Move | -0.74 |

| ▼ R2 | 7000 |

| ▼ R1 | 6850 |

| ▲ S1 | 6720 |

| ▲ S2 | 6579 |

S1 at 6720 was the level that mattered, and the market spent most of the week orbiting between Monday's open at 6685.5 and that support zone. Reuters reported the S&P settling at 6,775 on Monday, drifting sideways through Tuesday as investors digested Iran developments. Then came the Wednesday IEA announcement of a record 400 million barrel strategic reserve release, and Thursday's hammer blow when Investopedia reported the Dow shedding 739 points as Brent crude closed above $100 for the second consecutive day. Friday's close at 6636 settled just below the 6720 S1, meaning that level held for most of the week before finally cracking under the weight of oil-driven inflation fears. R1 at 6850 was never remotely threatened. R2 at 7000 belongs to a different universe at this point. S2 at 6579 is now within striking distance if the selloff accelerates.

The desk's called edge was that the market was 'underestimating duration of Iran conflict resolution and stagflation policy paralysis while overestimating March seasonal pattern reliability given VIX 29.48 panic phase entry and 6791 technical breakdown.' That edge call was largely vindicated. CNBC confirmed the S&P posted its third straight losing week and hit a new low for 2026 on the Iran oil crisis. The March seasonal rally that consensus was banking on, historically delivering a 70%+ positive hit rate with 2-3% average gains, has comprehensively failed to materialise. The February CPI came in at 2.4% year-over-year per BLS data published March 11, with core CPI at 2.5%, landing in that uncomfortable middle ground where inflation is too high for the Fed to cut and the economy too weak for the Fed to ignore. The stagflation narrative the desk identified played out exactly as described.

Every single sub-bias pointed the same direction this week: all six disciplines (Technical, Fundamental, Sentiment, Options, Institutional, Economic) were BEARISH. When the desk achieves that level of unanimity, the probability of a correct directional call rises sharply. The Economic agent carried the heaviest weight at 30%, and its focus on the impossible Fed dilemma between oil-driven inflation and the catastrophic February NFP (-92,000 jobs) proved to be the week's defining framework. The Technical agent at 20% correctly identified the 6791 breakdown as a regime change signal rather than noise. The Options agent at 20% correctly flagged VIX expansion risk, with the volatility index remaining elevated throughout the week. The Institutional agent had the lightest weight at 10% but its 'defensive deleveraging' reading captured the institutional risk-off flow. This was a week where the agents' agreement was more valuable than any individual discipline's insight.

The S&P 500 had its first turn as Market of the Week, and the timing could not have been more fitting. This is the index that matters most to the largest number of traders, and in a week where the Iran war intensified, Brent crude breached $100 per barrel, and the February CPI landed at 2.4%, the desk's BEARISH call at 6/10 conviction delivered a clean -0.74% decline from Monday's 6685.5 open to Friday's 6636.0 close.

The week's narrative was dominated by oil and what The New York Times somewhat understatedly called 'The War in Iran Is Roiling the World.' On Monday morning, 24/7 Wall St reported oil spiking as high as $120 in overnight trading before Trump forecast an end to the conflict, temporarily pulling crude back to $88.75. That whipsaw set the tone for a week of extraordinary intraday volatility. Tuesday saw Reuters report the S&P settling at 6,775 as investors tried to make sense of conflicting signals from the Gulf. By Wednesday, the IEA announced its largest strategic petroleum reserve release in history at 400 million barrels, and oil still surged. Investopedia confirmed the Dow shed 739 points on Thursday as Brent settled above $103. Friday brought more of the same, with Reuters noting stocks slipping further as the conflict pushed oil prices relentlessly higher.

The desk's MOTW report, published free on the Ghost site on Sunday evening, laid out the dual-shock thesis with precision: the Iran war driving oil above $90 combined with the catastrophic February NFP of -92,000 jobs creating a stagflation trap the Fed cannot resolve. That framework proved to be the correct lens for the week. CNBC reported the February CPI at 2.4% year-over-year on March 11, with core at 2.5%, exactly matching forecasts. Not hot enough to panic, but not cool enough to give the Fed cover for a rate cut. Analysts at CNBC estimated that if the oil shock persists, CPI could rise to 3.5% by year-end.

What makes this call satisfying is not the magnitude of the move, 0.74% is modest by recent standards, but the quality of the reasoning. The desk correctly identified that consensus dip-buyers were over-relying on March seasonal patterns. That seasonal thesis has been demolished by the Iran conflict. Axios noted the S&P was down 3% since the war began, and the New York Times observed that despite the turmoil, the index had only fallen 3.6% total, with the writer seemingly surprised the decline wasn't steeper. The desk predicted exactly this kind of slow-motion grinding lower when seasonal optimism collides with a genuine macro shock.

The one caveat: the levels framework was designed for a week where the S&P might grind lower toward the 6720 symmetry target the desk identified. The market tested that zone repeatedly through the week before Friday's close at 6636 finally broke below it. For subscribers tracking the paid reports on ES, the level accuracy was good through Thursday and then the rules changed when Brent settled above $100. S2 at 6579 is now the next gravitational pull, and if next week's FOMC delivers anything less than a dovish miracle, that level will be tested.

| Market | Bias | Conf. | Mon Open | Fri Close | Move | Result | Grade |

|---|---|---|---|---|---|---|---|

|

S&P 500

CORE

|

BEARISH | 6/10 | 6685.5 | 6636 | -0.74 | CORRECT | B+ |

| This week's MOTW. BEARISH at 6/10 as the S&P posted its third consecutive losing week on the Iran oil crisis. The dual-shock stagflation thesis drove the index to new 2026 lows. See the full deep-dive above. The free report is on the Ghost site. | |||||||

|

Crude Oil

CORE

|

BULLISH | 6/10 | 98 | 98.71 | 0.72 | CORRECT | B |

| BULLISH at 6/10, reduced from last week's post-thesis degradation, and crude delivered another 0.72% gain as Brent closed above $103 per barrel. The Monday-to-Friday number wildly understates the intraweek drama: oil spiked to $120 on Sunday night before Trump's ceasefire rhetoric pulled it back to $88, then climbed steadily through the week as the IEA's record 400-million-barrel reserve release proved insufficient. That is now three consecutive bullish wins on CL since the desk's famous pivot. Direction correct, conviction appropriately reduced. | |||||||

|

Gold

CORE

|

BULLISH | 6/10 | 5155 | 5061.7 | -1.81 | MISSED | D |

| BULLISH at 6/10, gold fell 1.81%. The desk reduced conviction from 8 to 6 after the prior week's miss, which was prudent, but the direction remained wrong. The dollar's war premium and oil-driven inflation repricing continue to overwhelm gold's traditional safe-haven bid. That is back-to-back misses on gold, breaking the long bullish winning streak that defined February. | |||||||

|

Nasdaq 100

CORE

|

NO CALL | — | 24435.25 | 24394.25 | -0.17 | — | — |

| NO CALL at 5/10 on a 0.17% decline. Tech drifted lower but avoided the carnage hitting the broader market. The desk's fifth consecutive correct assessment of NQ as directionless continues to be quietly impressive. Not every market needs a view. | |||||||

|

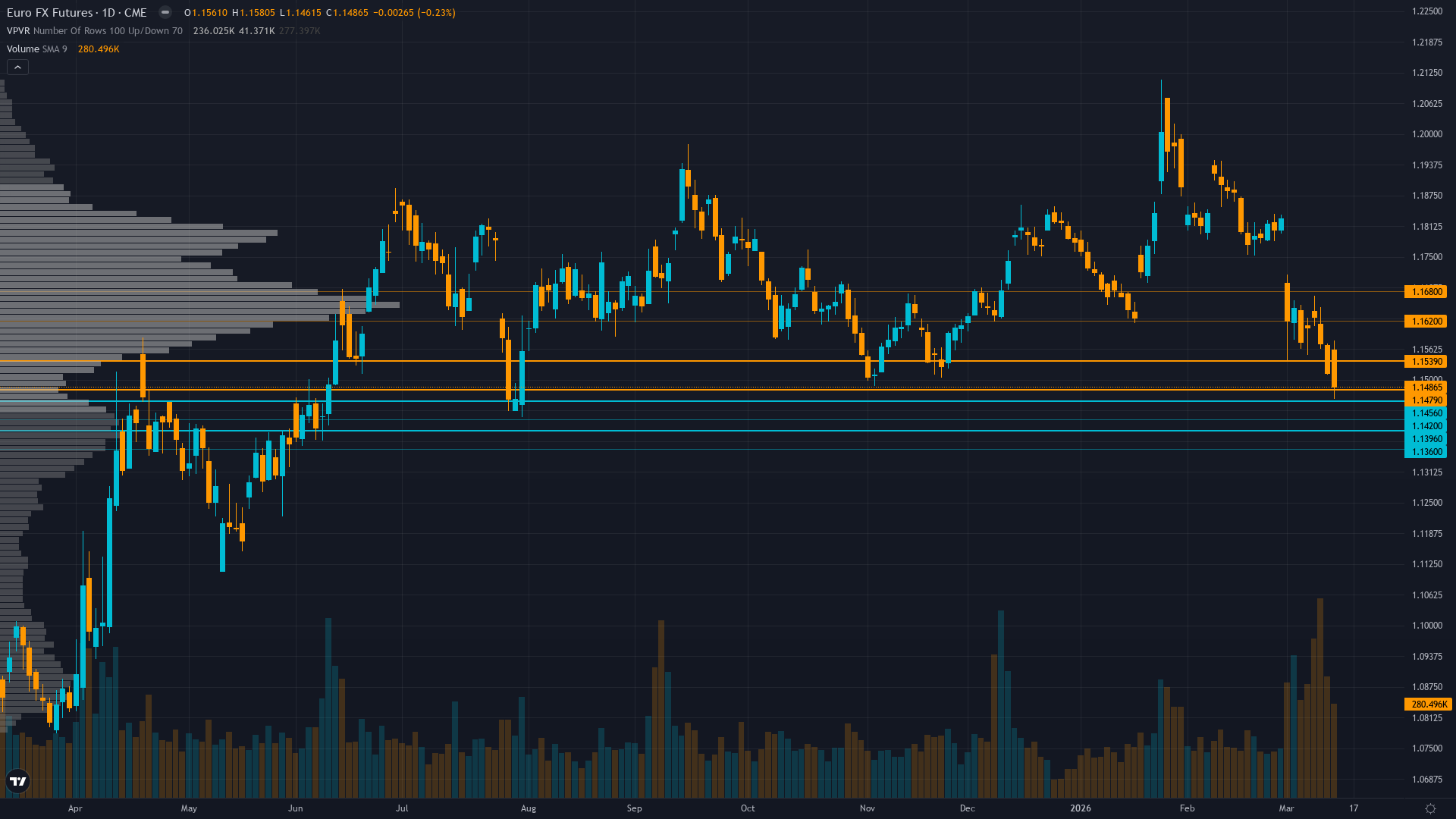

EUR/USD

CORE

|

NO CALL | — | 1.1556 | 1.1487 | -0.6 | — | — |

| NO CALL at 5/10, the euro slipped 60 pips. The twelve-week consolidation range the desk identified broke to the downside, and 0.6% is right at the edge of what constitutes a meaningful miss for FX. The desk's caution on currencies post-February's 0-for-4 debacle remains wise policy, though this one stings slightly. | |||||||

|

Silver

EXTENDED

|

NO CALL | — | 82.5 | 81.34 | -1.4 | — | — |

| NO CALL at 5/10, silver slipped 1.4%. After the catastrophic 12% miss two weeks ago and the desk's subsequent reset to neutral, the former star of the board continues its post-Iran decline. A 1.4% move for silver is practically a rest day given this metal's recent volatility regime. The restraint after four weeks of MOTW glory saved the desk from a far worse outcome. | |||||||

|

USD/JPY

EXTENDED

|

NO CALL | — | 0.006323 | 0.006313 | -0.16 | — | — |

| NO CALL at 5/10 on a tiny 0.16% yen move. The yen did nothing, and the desk said nothing. The desk's yen record has been markedly better since it stopped trying to call direction on this pair ahead of the March 19 BoJ meeting. | |||||||

|

GBP/USD

EXTENDED

|

NO CALL | — | 1.335 | 1.3241 | -0.81 | — | — |

| NO CALL at 5/10 as sterling fell 0.81%. The desk identified March 19 BoE as the catalyst and correctly stayed out of the pre-event drift. But 0.81% is a meaningful move for cable, driven by the dollar's war-premium strength, and the system scores it as a miss. | |||||||

|

Copper

EXTENDED

|

BULLISH | 6/10 | 5.723 | 5.757 | 0.59 | CORRECT | C+ |

| BULLISH at 6/10, copper eked out a 0.59% gain. After the prior week's miss, the desk reduced conviction and flagged deteriorating thesis health, which turned out to be the right instinct. The Grasberg supply crisis thesis is still alive, barely, but the magnitude of the move barely clears the noise floor. A win is a win, though the desk's nine-week bullish streak on copper is starting to resemble a man insisting the weather is lovely while standing in drizzle. | |||||||

|

Russell 2000

EXTENDED

|

NO CALL | — | 2499.2 | 2480.9 | -0.73 | — | — |

| NO CALL at 5/10, the Russell dropped 0.73%. After two consecutive bullish misses, the desk reset to neutral, and the small-cap index continued to bleed lower. The January breakout thesis has been comprehensively invalidated, and the desk's acceptance of that reality is welcome. Sometimes knowing when to fold is the entire game. | |||||||

|

AUD/USD

FULL DESK

|

NO CALL | — | 0.6988 | 0.6996 | 0.12 | — | — |

| NO CALL at 5/10 after reducing from six consecutive bullish weeks. The Aussie drifted a mere 12 pips and the desk earned its correct mark through restraint. The RBA March 17-18 meeting with a potential second consecutive rate hike should provide the catalyst the desk has been patiently waiting for. | |||||||

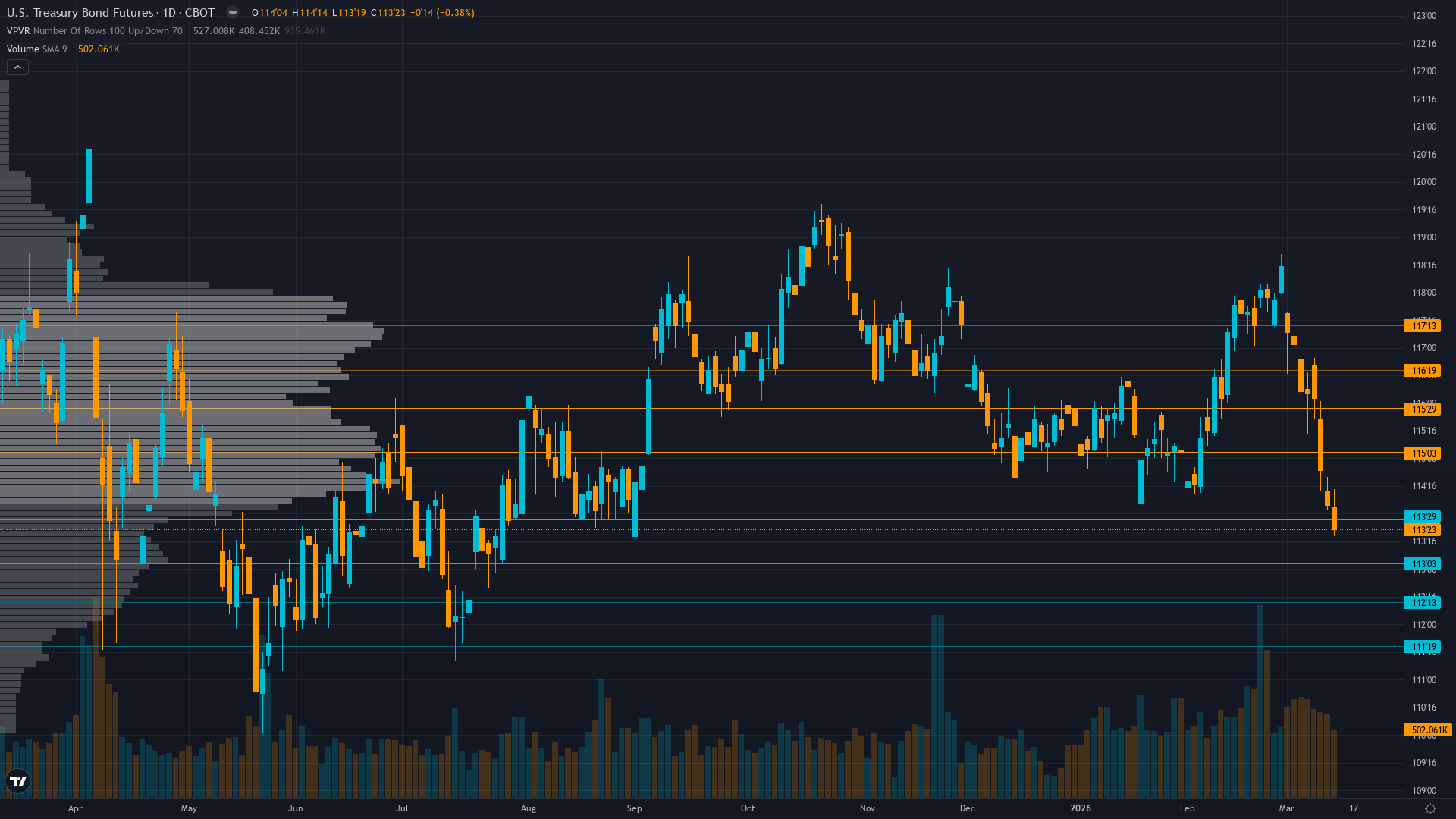

|

30Y Treasury

FULL DESK

|

BEARISH | 5/10 | 116 | 113.72 | -1.97 | CORRECT | A |

| BEARISH at 5/10, bonds fell nearly 2 full points. After two consecutive misses including the prior week's disastrous bullish flip, the desk reset with minimum conviction and caught a bearish resumption as oil-driven inflation fears sent yields surging. The best call on the board this week, and proof that the desk's long-running bearish bond thesis was right all along, even if the brief detour into bullish territory cost dearly. | |||||||

|

Wheat

FULL DESK

|

BULLISH | 8/10 | 635 | 613.75 | -3.35 | MISSED | F |

| BULLISH at 8/10, the desk's highest conviction call, and wheat dropped 3.35%. After two consecutive correct bullish calls, the Arctic blast winterkill thesis ran headlong into a WASDE that refused to validate the damage fears. FinancialContent had warned in February about the 'largest surplus in six years' and the USDA appears to agree. An F grade is warranted when your strongest-conviction call misses by this much. The desk's agricultural run has hit a wall. | |||||||

|

Soybeans

FULL DESK

|

BULLISH | 6/10 | 1195.5 | 1225.25 | 2.49 | CORRECT | A |

| BULLISH at 6/10, soybeans rallied 2.49%. The desk's South American weather risk thesis and renewable diesel structural floor played out nicely. After last week's missed NO CALL, the agents recalibrated to bullish and caught a clean move. That is five of the last six correct on beans, and the agricultural story is strongest when the desk trusts its own supply-demand analysis rather than second-guessing it. | |||||||

|

Platinum

FULL DESK

|

NO CALL | — | 2169.6 | 2042.1 | -5.88 | — | — |

| NO CALL at 5/10 per mandatory neutral reset after four consecutive misses, and platinum fell another 5.9%. The WPIC's revised 240,000-ounce deficit forecast could not prevent continued selling. The metal has now declined more than 30% from its January $2,925 peak. The mandatory reset was the right procedural call, though the 5.9% move means it is technically scored as a miss. | |||||||

|

✦ Best Call: 30Y Treasury (ZB)

BEARISH at just 5/10 conviction, bonds fell 1.97%. That might sound modest in isolation, but consider the context: the desk had just been burned by two consecutive misses on ZB, including a catastrophic bullish call the prior week that lost 2.75%. Rather than stubbornly holding the failed breakout thesis, the agents acknowledged the regime shift, flipped back to BEARISH with minimum conviction, and caught a nearly 2-point decline as oil-driven inflation fears sent yields surging. The MOVE index at 81.26 confirmed the volatility expansion the desk flagged. After weeks of painful flip-flopping on bonds, this was the week the system finally read the room correctly. Humility rewarded. |

⚠️ Worst Call: Wheat (ZW)

BULLISH at 8/10, the desk's highest conviction call on the board, and wheat fell 3.35%. After two consecutive correct bullish calls that delivered a combined 7.5%, the desk doubled down on the Arctic blast winterkill thesis and the March 10 WASDE catalyst. The WASDE report, combined with FinancialContent's earlier warning about the 'largest surplus in six years,' appears to have dealt a blow to the weather-scare narrative. A conviction-8 miss on a 3.4% move in the wrong direction is the kind of result that should make subscribers cautious about following high-confidence calls blindly. When I gave wheat an A grade last week for its 3.95% gain at 8/10, I should have also noted that a market where the desk calls 8/10 on weather events is a market where the misses will be proportionally painful. This was that week. |

The Economic agent had by far the strongest week, carrying the heaviest weighting on most markets and correctly reading the inflation-growth policy dilemma as the dominant price driver across equities, bonds, and commodities. Its framework, that the Fed is trapped between oil-driven inflation and labour market collapse, proved to be the most useful analytical lens. The Institutional agent also performed well, with its 'defensive deleveraging' thesis across equities and commodities proving broadly correct.

The weakest performer was, once again, the Fundamental agent across the commodity complex. Its supply-deficit frameworks on gold and wheat were technically correct about the underlying supply-demand dynamics but completely overwhelmed by macro forces. Gold's structural central bank demand thesis could not overcome the dollar's war premium. Wheat's winterkill narrative could not overcome a WASDE report showing near-record surpluses. The Fundamental agent needs a macro override switch for wartime conditions, and I have been saying this for two weeks now. At some point, the desk needs to actually build one rather than just acknowledging the problem.

The March 17-18 FOMC is the week's defining event, arriving at perhaps the most awkward moment possible for the Federal Reserve. Oil flirting with $100, CPI at 2.4% and possibly rising toward 3.5% by year-end per CNBC analysis, and February NFP at -92,000 create the textbook stagflation scenario where every possible policy action has a plausible argument against it. The ECB on March 18-19, BoJ on March 19, and BoE on March 19 with 90% market pricing for a rate cut to 3.5% create a wall of central bank catalysts. The RBA on March 17-18, where Governor Bullock warned of a live chance of a second consecutive hike, makes the Aussie dollar potentially the most interesting FX story of the week. Crude oil is knocking on triple digits, and whether the IEA's historic reserve release finally caps the rally or the conflict forces further escalation will set the tone for everything else. The desk will have its Sunday views. Given the cluster of central bank catalysts, I expect conviction levels to rise from this week's muted 6.14 average. Whether that proves wise or reckless, I will tell you next week.